RYAAY - Wizz Air: A Buy On Long-Term Scaling Strength

2023-04-05 18:14:56 ET

Summary

- Wizz Air operating loss narrowed.

- Comparison with a comparable pre-pandemic quarter shows significant space for efficiency improvement to drive down costs.

- The longer term fleet plan shows a strong plan to drive down unit costs as well as fuel consumption.

Wizz Air ( OTCPK:WZZAF ) announced its Q3 2023 earnings in January and is set to release full year results in June. In this report, I will be analyzing the results and explain why the future looks bright for Wizz Air. For that I will be looking at the Q3 results supplemented with comparisons to pre-pandemic results and have a look at unit costs as well as the fleet plan.

Wizz Air Performance Shows Growth

{kind=link}

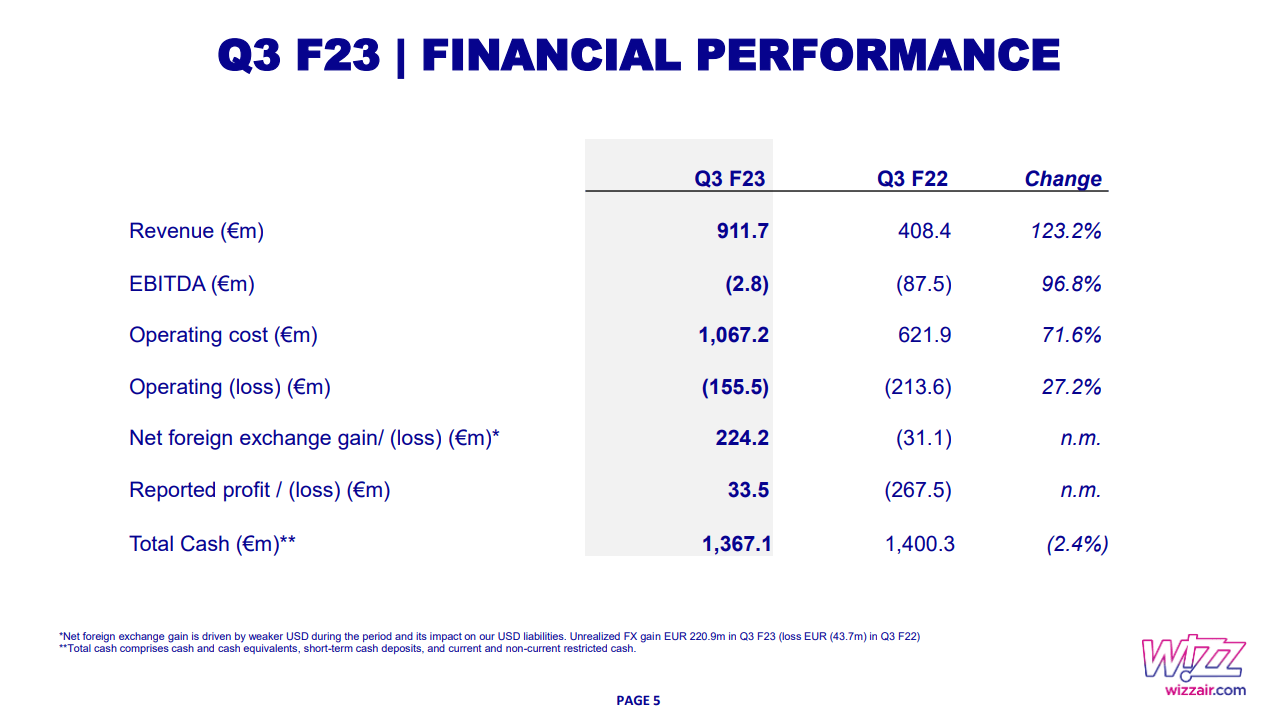

It should hardly come as a surprise that Wizz Air's results showed growth on all but one metric. Revenues more than doubled and are up 43% pre-pandemic, which I consider to be the more useful gauge. Passenger numbers grew 24% compared to pre-pandemic which led to a growth in ancillary revenues of 48.5% and 38.3% in ticket revenues supported by 3.6% growth in unit revenues. This was primarily driven by the ancillary revenues as the ticket unit revenues remained flat due to the 87.3% load factor being 5.2 percentage points lower than pre-pandemic levels.

On cost level, obviously year-over-year costs were up driven by 33% higher flight volume and a 140% surge in fuel prices. Wizz Air's fuel consumption was unhedged for the period so they were able to benefit from lower oil prices. Compared to pre-pandemic levels costs rose €464.4 million or 77% while ex-fuel costs rose 48%. What's interesting to note is that the ex-fuel costs growth grew more than the revenue growth. Ideally, we would like to see the cost growth being fully absorbed in the topline and that's clearly not the case partially due to lower load factors but more importantly lower utilization. In Q3 2023, the utilization was 10.5 hrs compared to 11.9 hrs in pre-pandemic times. What also should be kept in mind is that Q3 2020, Wizz Air was a different sized airline with 120 airplanes versus 173 airplanes now. So there's some scale advantage that has yet to propagate through the system.

All with all, the operating loss was €155.5 million compared to an operating profit of €34.6 in pre-pandemic levels. So from an operational point of view, Wizz Air has not yet recovered but that's also to be expected as the airline has used the pandemic and the subsequent recovery to increase capacity which has to mature. Driven by forex gains, the reported profit was €33.5 million compared to €21.4 million in the comparable pre-pandemic quarter.

Wizz Air Growth Drivers

{kind=link}

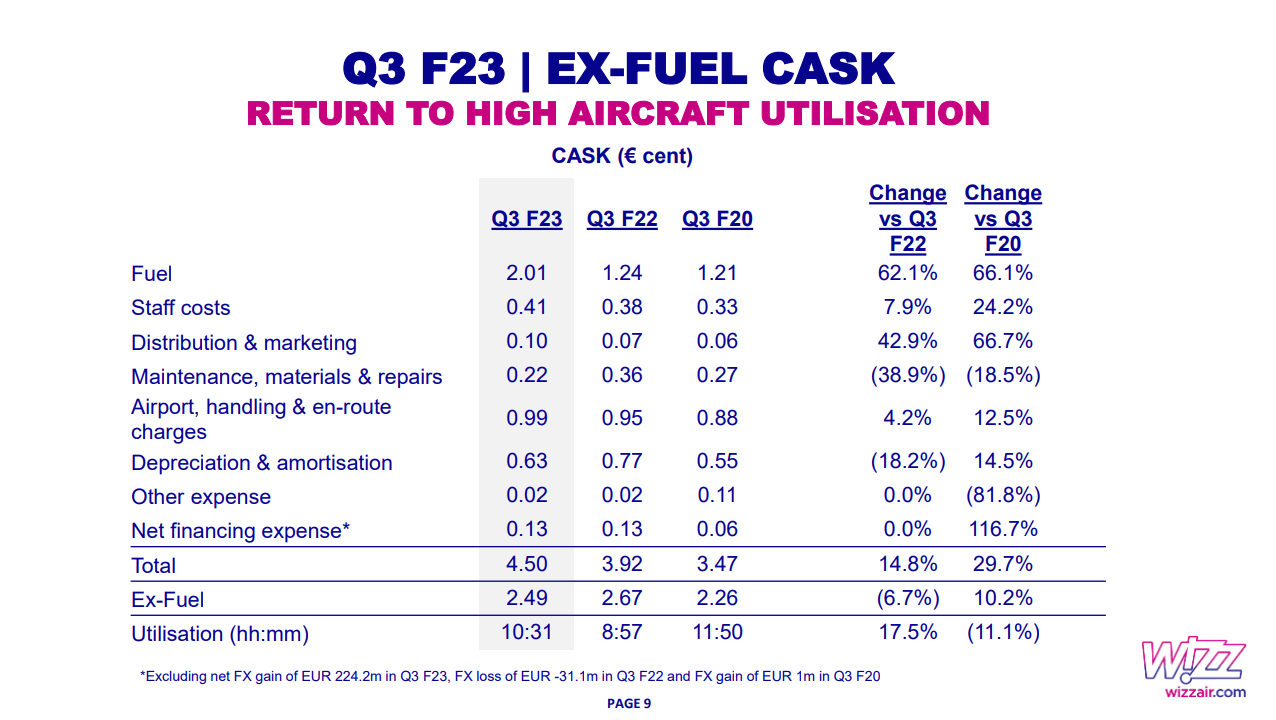

So, what we do see is that there is growth, but there is still significant room for improvement. In total the unit costs are €4.50 and €2.49 excluding fuel compared to €3.47 and €2.26 in the pre-pandemic quarter. So, the ex-fuel costs are 10.2% higher. If you keep in mind that utilization is still suppressed by 11.1% and the inflation since 2019 has been 14.9%, I do think the current unit costs compare favorably because once utilization does improve there should be a significant drive down on the existing cost items. By H1 2024, Wizz Air targets utilization of 12.4 hrs so that really shows that with the existing fleet there is a lot to gain from utilization perspective to drive unit costs down.

{kind=link}

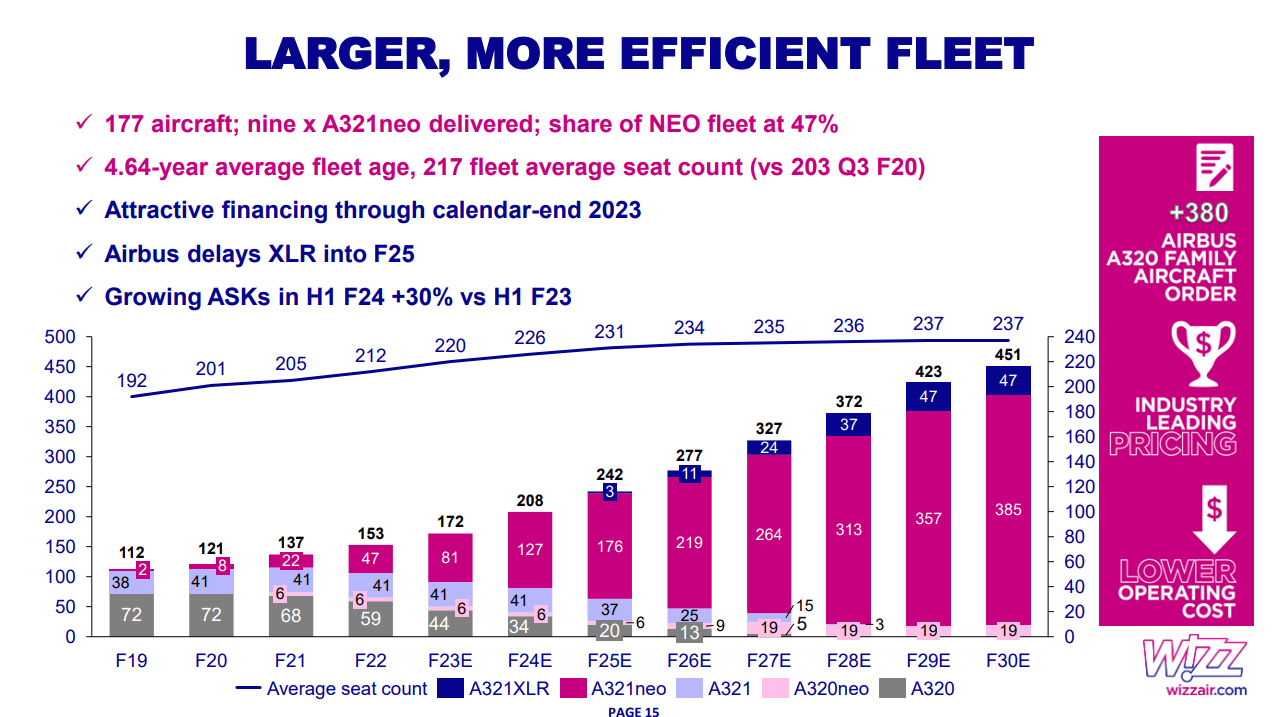

Furthermore, the fleet plan shows the longer-term driver to reduce unit costs. Over the past few years, Wizz Air has started to take deliveries of more Airbus A321neo airplanes and that's going to result in two things. The first one is a significant reduction in fuel burn, and secondly, the practice of upgauging will distribute costs over a higher number of seat-miles allowing Wizz Air to drive costs down and remain competitive on pricing. The current projections forecast that the number of seats per airplane will rise by 7.8% which can have a significant effect on unit costs.

What Are The Risks For Wizz Air?

{kind=link}

We also should address the risks that the low-cost airline could face. Obviously, oil prices are one of the risks. OPEC+ recently announced that it would be reducing production by 1.16 million barrels a day. So, oil higher oil prices are a risk but Wizz Air is partially shielded with absorbing more fuel efficient airplanes and the airline has hedged 59% of its fuel use in the current financial year and 45% next year.

Another risk is the competition in Europe among airlines. It's an extremely competitive field with Ryanair being the main competitor. Wizz Air has been able to expand its market share in Central and Eastern Europe to 27% from 18% pre-pandemic. So, the airline has used the pandemic to expand market share but that is something that most low-cost carriers did and we see that Wizz Air's flight activity expansion has been the most aggressive. So, I do feel comfortable about the trajectory but one also has to keep in mind that low-cost carriers have primarily expanded at the expense of mainline carriers and for the time being if the market share expansion drift switches from expanding at the expense of mainline to fellow low-cost carriers, Ryanair ( RYAAY ) might have a bit more weight in the game.

Passenger demand might also soften, but I do believe that low-cost carriers are strongly positioned to also be compelling for investments when fares soften as they will also aim extremely fast to drive down costs as well.

Is Wizz Air Stock A Buy?

For the London registered stock, 34% upside is seen by analysts, and if I look at how Wizz Air is managing and how some key metrics are improving, I can understand why. The company does not need to make major investments to drive down unit costs. The cost reduction objective is a dynamic of LCCs, so Wizz Air should do rather well, and as it scales and produces more hours per airplane, we should see significant relief on the cost side.

Conclusion: There's A Lot To Like About Wizz Air Stock

I believe there's a lot to like about Wizz Air. The company has used the pandemic to expand market share and it aims to improve utilization of existing aircraft which will reduce unit costs. Beyond that the company will scale its operations with aircraft with more seats bringing the unit costs down further due to higher seat count as well as higher fuel efficiency per seat. For FY2023 the business will still be in a loss position but as utilization improves and the company grows its fleet, network and frequency we should see a more cost efficient profitable airline. Perhaps what I'm missing is how the airline will manage revenue in the current revenue environment, but also in a lower revenue environment but realistically low-cost airlines have been doing quite well with offering competitive pricing.

For further details see:

Wizz Air: A Buy On Long-Term Scaling Strength