ON - Wolfspeed: Buy At The Pullback Despite Increasing Competition

Summary

- EV market growth creates a strong opportunity for silicon carbide and leads to tighter competition in the market.

- Despite pressing rivalry, I believe Wolfspeed’s market is well-protected by manufacturing complexities and its dominant position in the supply chain.

- Wolfspeed has shown a very strong performance recently. Additionally, it accelerated investments to meet the rising demand.

- When the Nasdaq declines further, I am buying the stock.

Today I would like to focus on Wolfspeed, Inc. ( WOLF ), an innovative supplier in the auto production chain that greatly benefits from the booming electric vehicle ("EV") market. It develops silicon carbide power semiconductors that help car makers save on costs, increase driving range, and introduce fast charging. Wolfspeed’s leadership is generously rewarded by the market.

Its price/sales multiple is 18x! Such a valuation attracts a lot of competitors who are eager to nip off Wolfspeed’s fame. Emerging competition makes some of Seeking Alpha's contributors concerned about the future of Wolfspeed’s share price development. In contrast to other authors, I believe that high entry barriers and Wolfspeed’s leading position in silicon carbide production will allow it to retain its market share. I would buy the stock at the next leg of the bear market.

High voltage rock 'n' roll

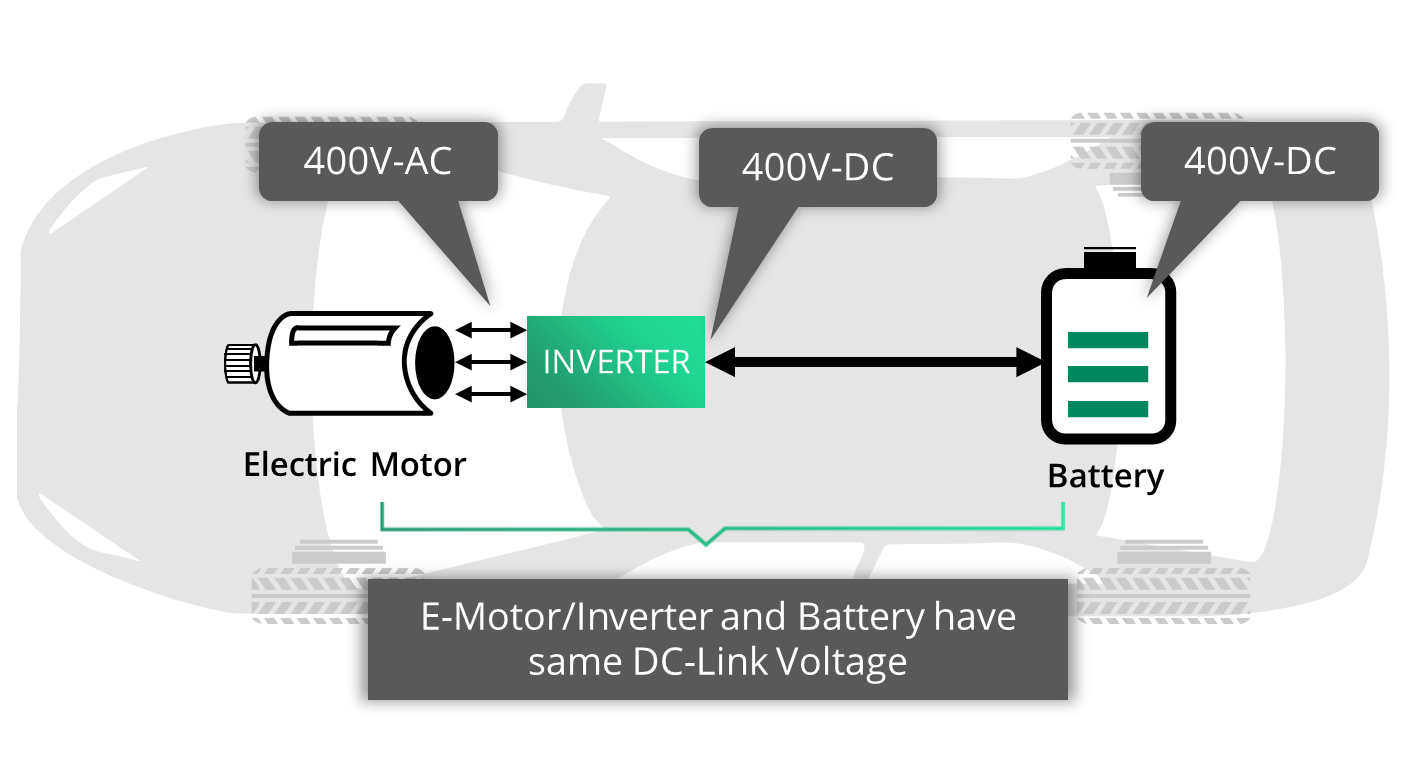

Before we make a deep dive into the stock fundamentals, let us ordinary non-physicists step onto this chaotic “highway to hell” and understand AC/DC differences. Not the band, the current flows. Highlighting the distinction between the two would help us understand the eagerness of auto producers to use silicon carbide.

AC stands for alternating current and presents the voltage that changes its direction and magnitude periodically. What is important for us to know is that AC flow can be converted to other voltages. DC is direct or constant current that is characterized by a current one-direction flow.

AC has a huge advantage in comparison to DC - its ability to be easily converted to higher or lower voltages. Additionally, DC cannot flow over long distances as efficiently as AC does. What do these differences have to do with EVs?

Electric vehicles’ batteries work on DC voltages, but the energy from the batteries must power and supply the AC motors. The engines use the current that sets up a constantly changing magnetic field, the one that is constantly changing in a rotational sense. Remember, we said earlier that AC changed its direction periodically. This is exactly what is needed for the motor.

In order to switch DC voltages to required magnitude, a DC-AC inverter is used.

{kind=link}

The inverter does its “switching job” thanks to electronic semiconductor devices, such as transistors. Today, they are primarily made from silicon, a widespread element located almost everywhere on the Earth which explains both its popularity and inexpensive price. However, an increasing number of EV players have been switching to silicon carbide transistors due to higher efficiency.

Silicon carbide was first applied by Tesla ( TSLA ) in the inverters for Model 3 in 2017 . Musk realized that the new technology could manage a larger battery more efficiently in comparison to the silicon alternative. The implementation of silicon carbide boosted the Model S’s range from 335 miles to 370 miles. About half of the advancements, five percent, can be attributed to the new material while the rest was a result of improved software and other measures.

With the introduction of the Taycan, Porsche ( POAHY ) became the first carmaker to propose an 800V-based EV. The main advantage of this change was a drastic reduction in battery charging time, as more power could be transferred away faster. Higher voltage also enabled the use of smaller, lighter, and cheaper electric cables in the car.

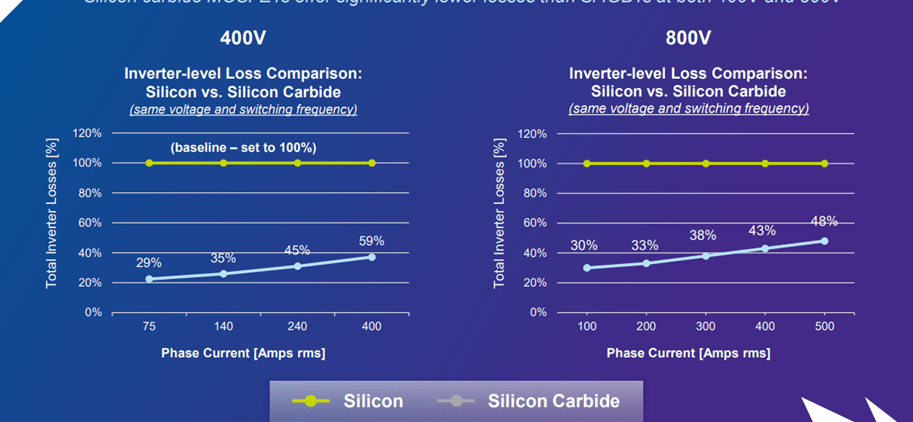

Unfortunately, doubling the battery voltage increases energy losses at the inverter, making it inefficient and decreasing the battery range. This problem can be solved by silicon carbide, a material more suitable for managing high voltages and decreasing the amount of energy lost.

{kind=link}

To summarize, inverters produced from silicon carbide increase the driving range, allow a 50% quicker charging, and make the battery smaller and lighter. The change impressed EV business leaders and rapidly raised interest in the material. Considering that Wolfspeed has been specializing on the technology for many years, it leveraged much of its first-mover advantage.

Competition and market

As shared by ZF at Wolfspeed’s Investor Day , EV penetration has significantly accelerated over the last few years. 2030 EV share was estimated at 16% in the 2019 forecast, but last year the 2030 forecast increased to 40%. Such a high industrial development attracted a lot of investments in the EV supply chain, and significantly increased the competitive pressure on Wolfspeed.

Increasing competitive pressure

Wolfspeed is under siege by competition from two sides. On one hand, silicon technology is constantly improving and becoming more efficient. On the other hand, powerful players are emerging in the silicon carbide field.

Recently, Renesas Electronics ( RNECF ), a supplier of semiconductor solutions, announced the development of a new generation of silicon inverters that lead to a 10% reduction in power losses. Such an invention makes the devices comparable with silicon carbide ones. Additionally, the company will vastly increase its manufacturing capabilities in 2023 and 2024, further cementing themselves as a strong competitor.

Higher demand in the EV industry has attracted new players all over the world. If we look at China , then we see a lot of start-ups in the field. For instance, Shenzhen-based Bronze Technologies is expected to open a new production facility in 2023 and aims to manufacture 2 million devices. San’an Optoelectronics invested about USD 2.5 billion in the manufacturing capabilities. SICC became the first listed Chinese company specializing in silicon carbide. II-VI of Coherent Corp. (COHR) set up a new production base in Fuzhou, southeastern China’s Fujian Province.

American players such as STMicroelectronics ( STM ) also pose a serious threat to Wolfspeed, as it was chosen by Tesla in 2017 as a supplier of silicon carbide inverters for their Model 3.

Another U.S. semiconductors supplier, ON Semiconductor Corporation ( ON ), announced the expansion of its silicon carbide production to a recently built New Hampshire production facility:

The facility will increase its silicon carbide capacity by five times year-over-year, helping to ensure supply of critical components for Onsemi customers

We clearly see high voltage in the field of competitors. Nevertheless, we must keep in mind that silicon carbide production is extremely complicated, and not all players will succeed. Let me briefly elaborate on the complexities of the manufacturing process.

Hot manufacturing process

Silicon carbide is an extremely rare natural material that can hardly be excavated. In order to produce it, you need to mix high-purity silicon powder with high-purity carbon powder at a tremendously high temperature. Extreme heat is required because the materials do not melt, but instead sublime, or turn into gas. The thing is: how hot is hot? With a temperature of 2500C, half the temperature of the surface of the sun and double that of molten lava, you can’t even look at the chemical mixture with the bare, unprotected eye.

Silicon carbide has a layered crystal structure which occurs in a number of different forms or polytypes . Composed of carbon and silicon in equal amounts, each atom is bonded to four atoms of the opposite type in a bond called a “polytipe.” There are 200 different versions of polytipes possible, and each one exhibits different electronics properties. Only a very specific type is suitable for manufacturing silicon carbide wafers. It is relatively easy to fail during the manufacturing process. And if you miss, you’ll get a “beautiful mess” instead of the required one.

{kind=link}

Why Wolfspeed can withstand competition

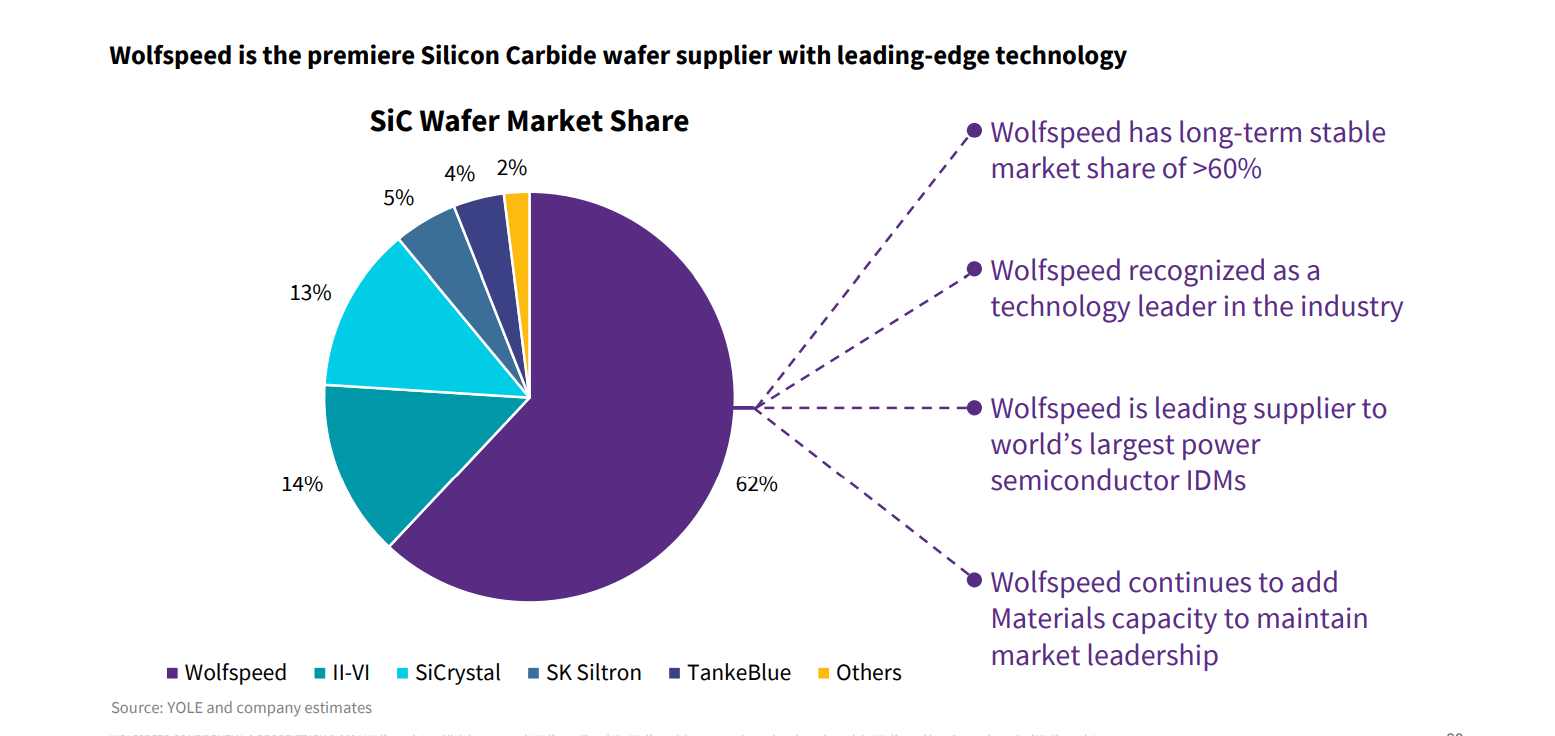

In contrast to many newcomers, Wolfspeed has 35 years of experience in manufacturing not only devices but also silicon carbide wafers. Although the industry is booming now, it may resemble the auto industry of 2021 when a diverse variety of start-ups attracted investors’ interest but eventually turned into pumpkins due to the inability to realize their plans.

Additionally, it is important to differentiate between silicon carbide material and silicon carbide devices. Although such companies as STMicroelectronics and Onsemi invest in silicon carbide manufacturing, they are customers of Wolfspeed and its materials to produce their devices. Wolfspeed, therefore, remains the global leader in the materials production.

{kind=link}

Theoretically speaking, Wolfspeed could limit supply of materials to its emerging competitors and hinder the production plans. However, it is not eager to take this step. Wolfspeed sells materials to their partners to accelerate market adoption. It is a comparatively small player in the production of industrial and car devices, with a revenue at about only $750 million. This is remarkably low compared to the entire market.

Although many EV producers are starting to acquire interest in silicon carbide as a material, many of them are still unaware or skeptical towards it. So it is in the favor of Wolfspeed when more producers go for the new technology. It would allow the company to expand the market and create a “bigger pie” where its share will also be bigger despite growing competition.

Another factor that could hinder the growth plans of newcomers in the industry lies in the lack of expertise in the field. It would not be easy to find a sufficient number of qualified professionals, as the technology was a niche one before the current EV boom.

Finally, Wolfspeed’s fundamentals

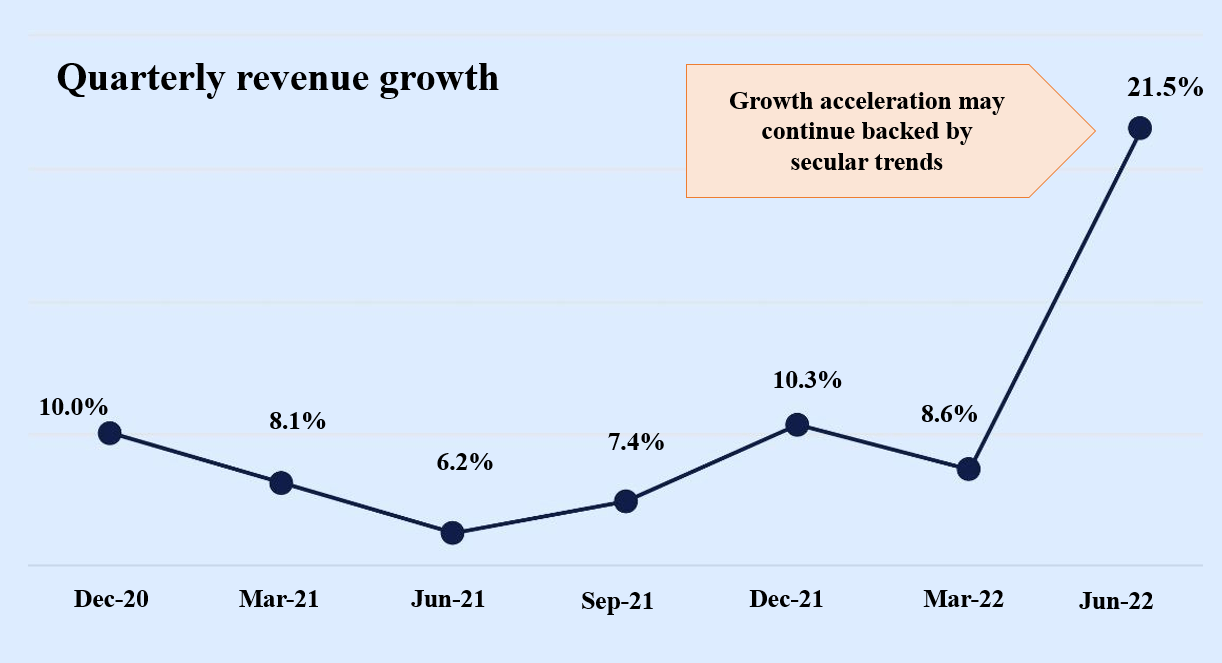

Over the last quarter (it is currently Q4 for Wolfspeed, as their financial year ends in June), Wolfspeed has shown spectacular results and accelerated its revenue development significantly. The growth largely came from improvements at the existing factory in Durham.

{kind=link}

Although the current sales are mainly generated by demand from the industry, Wolfspeed managed to leverage on accelerated EV transition. The company significantly increased the backlog of potential orders called “design-ins” mainly from auto producers. The entire pipeline won’t entirely convert into revenue, but it’s surely a strong indication of customers’ interest. Historically, Wolfspeed has converted about 50% of its design-ins into long term agreements. The management commented on it at Q4 earnings call :

The opportunity pipeline for silicon carbide has more than doubled to $35 billion in a single year. … So, we had 2 quarters of $1.6 billion, followed by this quarter of $2.6 billion, almost double the previous record. So nearly $6 billion of design-ins have happened since our last Investor Day.

Based on booming demand, Wolfspeed expects a 30-40% ramp-up in 2025 or 2026. It would result in almost 3.0 billion USD revenue compared with 2.1 billion USD expected earlier. The company understands that such a tremendous expansion will require additional spendings and investments in the production capabilities. Although the new factory in Marcy should have sufficient capacity to generate 1.5-2.0 billion USD revenue, it will be enough to meet 2025/26 revenue targets, but not sufficient for years beyond.

Construction of the Marcy plant took about two years because management was lucky to start building before the supply-chain crisis. The erection of such a factory now would take 3-4 years. Therefore, the company needs to act swiftly and start the process as early as possible to meet future demand. Consequently, Capex in fiscal 2022 was increased and distributed on expansion of existing facilities. Based on the recent indications, future Capex will be around 2022 levels. According to this, I estimate 2023 Capex at around 700 million USD, a triple fold increase when compared with 2022.

{kind=link}

Although some of the Capex may be supported by federal funds, like the recently legislated CHIPS, such an expansion would require additional funds. Given the current high valuation, it would be rational to issue further convertible bonds, but the issuance of 1.0 billion USD funds would be equal only to 8% equity dilution and could be easily digested by the markets.

I believe that at the upcoming Investor Day on the 31 st of October we will hear more details about future plans.

Valuation

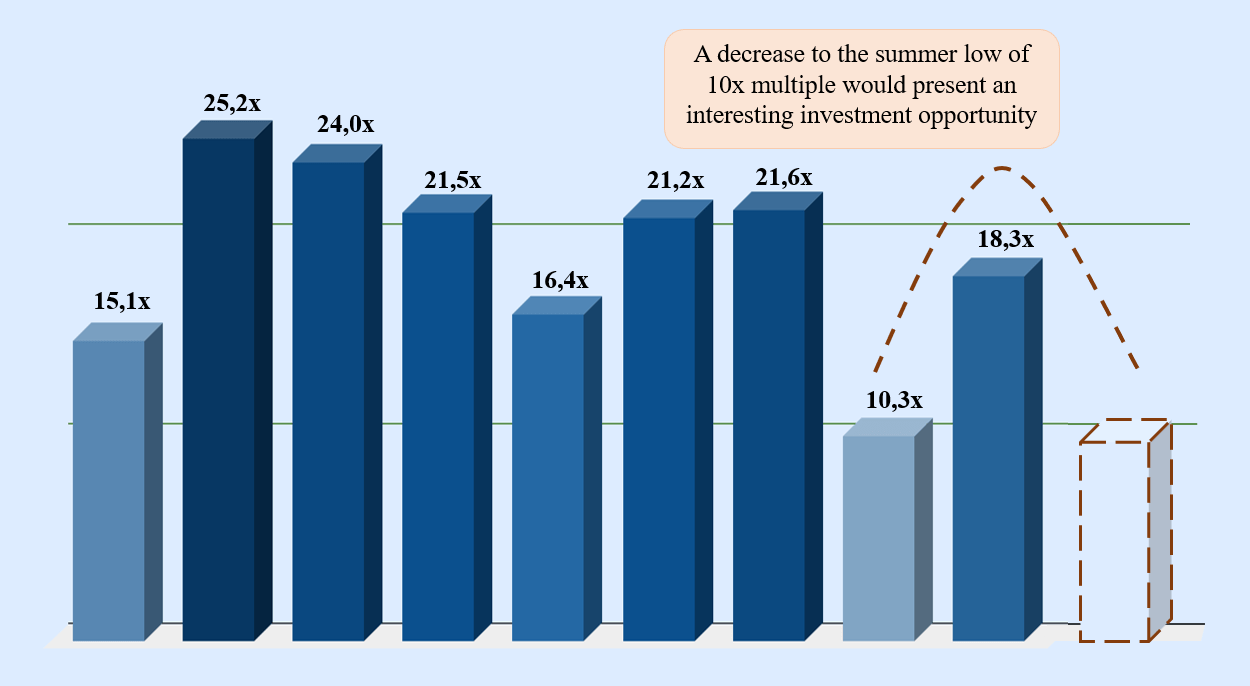

While Wolfspeed’s share price more than doubled since pre-pandemic levels, its journey was quite volatile recently. Still, its returns were constantly higher or equal to Nasdaq returns. We can see from the chart that Wolfspeed converged to Nasdaq returns and bounced back several times. If history repeats itself, further share price decrease may be expected assuming Nasdaq’s continued bear rally. I deem it quite possible, given recent news on oil supply. Less oil, higher prices, higher inflation. Let alone recession fears and upcoming real estate crisis resulting in lower index.

Prepared by author

Unfortunately, we cannot fully compare historic multiples with current ones, as Wolfspeed was a completely different company several years ago. Initially, it started with light bulbs and LED production. However, it later decided to sell this business to Smart Global Holdings for $300 million to focus on the inverter market. Therefore, we could only measure multiples over the last 1.5 years when its financial accounts were restated.

The current Price / Sales multiple of 18x seems elevated given potential equity dilution, accelerated competition, and recession fears. However, if the share price decreases to the summer low of 10x multiple, it would present an interesting investment opportunity.

{kind=link}

Risks

The main risks lie in Wolfspeed’s increasing competition, slower EV adoption, and its effect on gross margins. Currently, Wolfspeed expects to achieve around a 50% margin over the next few years. Given recent high investments in the production capacity, it may lead to excess supply if the demand for EVs slows down. It would delay the profitability path and may spark bearish sentiment among the investors. Additionally, if U.S. authorities take steps against Chinese battery producers due to child labor issues, it will affect the EV industry and demand for silicon carbide.

Conclusion

Despite intensified competitive pressure, I consider Wolfspeed stock to be a solid long-term opportunity given high entry barriers in the industry and secular EV trends. I would closely observe the share price development and buy if the multiple goes down closer to the single-digit territory.

For further details see:

Wolfspeed: Buy At The Pullback Despite Increasing Competition