STM - Wolfspeed: Poised For Supercharged Growth

2023-10-03 04:02:49 ET

Summary

- Wolfspeed, the global leader in silicon carbide semiconductors, is poised for super-charged growth due to SiC's superior characteristics over silicon.

- The company has faced challenges with production delays and an accounting change, but these issues have been resolved.

- Wolfspeed's production at the Mohawk fab will accelerate in 2024, and funding assistance for the new Saarland fab is expected by the end of 2023.

Introduction

The ubiquitous silicon (Si) chip has been the poster child of the technology revolution for the past 50+ years. It is the beating heart of personal computers, telephone equipment, personal devices, and a host of industrial, commercial, medical and consumer products. But silicon has limitations and better alternatives are needed for many products.

Silicon carbide (SiC) semiconductors have significant advantages over silicon and SiC is generating serious commercial interest. SiC devices can function at more extreme temperatures, they have better energy efficiency, they enable faster re-charge and they have improved reliability and safety. Above all, SiC devices come in smaller sizes which leads to lower weight and a reduced total cost of ownership.

SiC is seen as being particularly beneficial to the electronic motor vehicle market where the combination of faster battery re-charge, longer driving range, better safety, and overall lower weight and cost of production offer a compelling package of advantages. They also have notable benefits in the power tool construction business and in industry segments that involve extreme temperatures such as aerospace, smelting, mining, and many physical industries.

Exploding Market

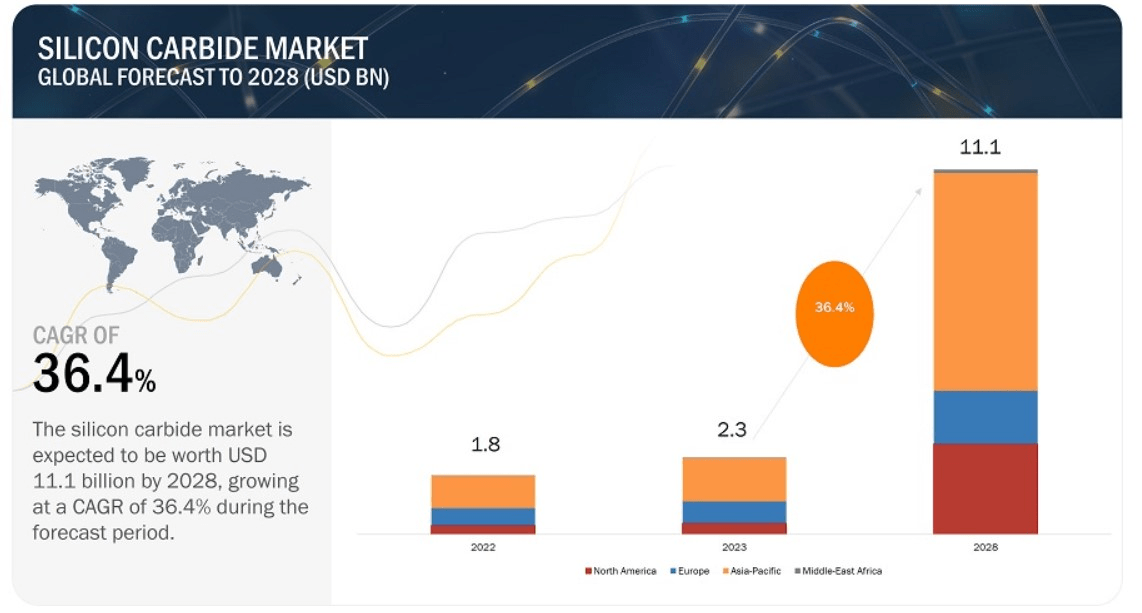

The big advantages of silicon carbide have led to industry experts forecasting that the SiC sector will evidence annual growth of anything from 25% to 40% through the end of the decade.

By way of example, here is a report from Markets And Markets with SiC growth compounding at over 36% from 2022 through 2028 – on track to achieve more than 1,000% growth between 2022 and 2030 by which time it may be worth north of $20 billion. Many similar estimates abound. Regardless of whichever forecast you choose it does seem certain that SiC has begun an inevitable period of extraordinary growth.

Silicon Carbide, Global Forecast 2028 (Markets And Markets)

{kind=link}

Manufacturing SiC

Manufacture of SiC is far from easy.

SiC manufacture requires temperatures of up to 2,500 degrees centigrade, highly specialised heating and cooling equipment and advanced know-how. When SiC ingots grow, they can develop into any of 200+ crystalline structures but only one functions properly - all others are waste. Once produced, the silicon carbide ingot (a boule ) is sliced into wafers and undergoes other processes such as dicing, grinding and epitaxy (epi) which, because SiC is one of the hardest materials in existence, comes with their own difficulties.

Until now, the complexity of producing silicon carbide has limited SiC wafer sizes to 6 inches or 150mm. This compares to regular silicon wafers which come in standardised 300mm (or 12 inch) format, having evolved over the past 40-50 years from 4 inch, to 6 inch, to 200mm (8 inch) and now 300mm (12 inch), and some fabs even moving to 450mm wafer sizes although 450mm is not yet in general use.

There are compelling economies of scale to be gained from migrating to larger wafer sizes. Larger diameter wafers allow for more die per wafer. According to this Wikipedia article , the move from 200mm to 300mm silicon wafers in the late 1990s enabled cost savings of 30-40% per die.

Wolfspeed

Wolfspeed Inc ( WOLF ) is the global SiC leader. The company has been producing SiC semiconductors and devices for over 30 years. It supplies 60% of the worlds SiC wafers. Driven by the wall of demand that lies ahead, other companies such as ST Microelectronics NV (NYSE: STM ), ON Semiconductor Corporation (Nasdaq: ON ), Infineon Technologies AG (IFNNY) and Japanese and Chinese competitors and many others, are all taking steps to advance their own SiC production. Whilst they will succeed, it should be noted that, because production of SiC wafers is so complex, they will encounter teething difficulties along the way and already-established incumbents will retain some important advantages. In any event, if market growth forecasts come anywhere close to being realized there will be room for many successful participants. This shared success viewpoint, rather than a winner-takes-all, is how investors should regard Wolfspeed.

Wolfspeed, via its newly commissioned Mohawk, New York fab, has become the first company to successfully migrate to 200mm SiC wafers. As well as benefitting from the physical economies of scale via larger wafer sizes, this new fab has the added advantage of being fully automated. Whilst SiC is an extremely hard material, it is also brittle and manual processes lead to damage, breakage, and loss. Most losses are eliminated via automation. The Mohawk fab is expected to reduce manufacturing costs by a full 50% and boost gross margins accordingly.

Business Review

Wolfspeed has two lines of business – materials and power devices.

The materials line is predominately bare SiC wafers but also includes epitaxial wafers and GaN epitaxial wafers. These are sold to customers worldwide who then incorporate them into power devices and other applications. Many of these customers are Wolfspeed competitors. Wolfspeed sells to competitors in good part to help grow the overall SiC global market.

The power device line includes power modules, SiC diodes and metal oxide semiconductor field effect transistors (MOSFETs). These are sold to customers and distributors who incorporate them into applications such as electronic vehicles, charge stations, solar inverters, and industrial and consumer power supplies.

“Design-ins” are one of the main yardsticks used by Wolfspeed to forecast long-term demand and future revenues. To qualify as a design-in, customers must provide Wolfspeed with written details of their future requirements, plans, pricing and so on. Design-ins can be cancelled for various reasons – for example changing technologies, cancelled projects etc. Recently about 40-50% of design-ins convert to revenue.

Wolfspeed design-ins were $2.9 billion in FY 2021, $6.4 billion in FY 2022 and $8.3 billion in FY 2023, leaving cumulative design-ins of more than $19 billion as of 30 June 2023 (Wolfspeed financial year end). These numbers dwarf Wolfspeed’s annual sales which, for FY 2023, were less than $1 billion.

Whilst the overall SiC market growth outlook remains excellent, Wolfspeed aims to grow even faster. During the company’s October 2022 Investor Day, management forecasted annual revenue growth of 40% culminating in total sales for financial year ended June 2027 of $4 billion.

Wolfspeed Revenue Target (Wolfspeed)

{kind=link}

These revenue targets appear excessively optimistic. Building the world’s first fully automated 200mm SiC fab when teething issues are unavoidable, doing much of that construction and kitting-out work whilst shackled by Covid, and then enduring post-Covid supply-chain issues – all this has led to inevitable slippage. Prudent investors might best view the entire schedule with a 1-year lag.

To accommodate the burgeoning growth pipeline, Wolfspeed has commenced an ambitious expansion program. Its existing and planned fabs are as follows:

Durham, North Carolina.

Until recently, this was Wolfspeed's only fab and it produced all Wolfspeed’s SiC wafers and SiC devices. The wafer output representing 60% of the global SiC market. Wafers are shipped to customers via long-term supply agreements. In FY 2023 this fab generated virtually 100% of Wolfspeed’s $922 million revenue.

Mohawk Valley, New York.

This new fully automatic 200mm wafer and device fab is seen as Wolfspeed’s blueprint for the future. Alas, its beginnings were less than stellar. The construction project began in 2020 - the same time as Covid-19. The fab production start-up encountered a delay of several months due to post-Covid supply-chain issues relating to equipment to fix a power sub-station failure. Also, the company experienced some “pinch points” in migrating from their old familiar 150mm processes at Durham to this new 200mm fab.

During the September 7, 2023, Evercore ISI conference – ref 2 mins in – CEO Gregg Lowe confirmed with clarity that recent glitches have been fully resolved, that the company has received its certificate of occupancy, that crystal production is ahead of expectations and at a level considered to be excellent.

Wolfspeed crystal production is in building #10 of the Mohawk fab and this enables the fab to get to 20% utilization level. This equates to a production run rate of $100 million per quarter and the company expects to achieve this in FY 2024. For the most part, Wolfspeed is currently qualifying production for customers and has already completed customer qualification for both its largest device and its most complex device. The big production ramp inflection occurs in Q3 and Q4 FY’24. Product inspection, testing, and order completion, leads to delays of some months between production and revenue recognition. Hence, whilst Wolfspeed would achieve a production run-rate of $100 million per quarter late in FY’24, it may be the beginning of FY’25 before all the $100 million quarterly figure shows up in sales.

At full capacity Mohawk generates $2 billion annual sales.

During the Evercore ISI Conference of September 7, 2023, the CEO was asked;

“based on today’s ramp plans, is it still reasonable to think that Mohawk will be running at the full $2 billion run rate in fiscal 2027…”

To which the CEO responded;

“We are still on track for fiscal 2027 on the full fit-out and production utilization of Mohawk. Nothing has changed and I think the demand that we have is well served by that full output. We have plenty demand that is even above that.”. Refer 26 minutes into the webcast.

To me this response is surprisingly positive. Mohawk is now operating almost a year behind its original schedule, and few would expect it to generate sales in FY’27 of $2 billion. Certainly not me. Recall that $2 billion equals full capacity. But perhaps the company may reach full capacity by late FY’27. Not quite to the original plan, but still encouraging from an investor perspective and it’s interesting that management seems confident that they may achieve some significant catch-up.

The ramp-up of capacity at Mohawk will be accentuated by the transfer of production from Durham because Mohawk operating costs are seen to be 50% lower than Durham’s. As of mid-2023, 100% of Wolfspeed power device revenue comes from Durham. By FY 2026, 80% is forecast to come from Mohawk.

Either way it appears that Wolfspeed will need additional fab capacity sometime during calendar 2027, or possibly beforehand if business comes in ahead of expectations.

Siler City, North Carolina.

When complete, this will be the world’s largest SiC materials facility. It is 10 times the size of Durham. The estimated cost is $1.5 billion. The fab was originally scheduled to commence operations before end of calendar 2024. In the Wolfspeed Q2’23 earnings conference call , the company re-confirmed expectations that wafer production at this facility would commence during the second half of calendar year 2024. According to that conference call, construction of the Siler City fab is proceeding to plan and no major obstacles are anticipated. In part, the Siler city fab is likely benefiting from the fact that Wolfspeed is again using many members of the same team that delivered the Mohawk Valley fab.

Saarland, Germany.

This is a new 200mm highly automated SiC power device fab. This facility is larger than the Mohawk Valley fab and, as of September 2023, has an estimated capex budget of about $2.5 billion. The original target date to start production is year-end calendar 2026.

This project appears to be progressing with exemplary German efficiency. The Saarland regional government has secured the land and are preparing it, tearing down old buildings, moving waterworks etc. They will own the land and lease it to Wolfspeed. The company has already hired the construction firm, completed architect’s designs, and hired the fab manager. The permitting process is expected to take 9 months and Wolfspeed should break ground Q3 calendar 2024. Construction should be faster than Mohawk because of the learning process. Production is scheduled to commence in Q4 calendar 2026.

Wolfspeed expects to receive funding aid via the European CHIPS Act . The company is in close dialogue with the regional government offices and matters appear to be progressing smoothly. From the September 7, Evercore ISI conference;

“Saarland, no official approval yet but we’re very comfortable. We anticipate it will happen soon, as per the signals we’re getting from Europe, possibly as early as the end of September and ‘certainly before the end of 2023’. We have a good understanding of how much we should get and we’re quite pleased at that”.

Funding

In the Wolfspeed October 2022 Investor Day presentation, the combined capex for Mohawk, Siler City and Saarland through FY 2027 was estimated at $6.5 billion. Net of capex already spent by the end of FY 2023, there remains an estimated $5 billion still to be outlaid.

At June 30, 2023 Wolfspeed had $3 billion cash. In July 2023 the company received a deposit of $2 billion on signing a 10-year supply agreement with Renesas . Between now and end of FY 2027 Wolfspeed should generate at least $1 billion in operating cash flow assuming Wolfspeed continues to lag its multi-year operating plans by a full year. [Note: In the unlikely case that Wolfspeed caught up with its original October 2022 schedule, the company would generate approximately $2.5 billion operating cash flow.]

Wolfspeed also expects to receive funding assistance via the US CHIPS Act and similarly, as noted above, from German government for the Saarland fab. Wolfspeed has given no estimates about the likely sizes of this funding assistance. I would hazard a wild guess that Wolfspeed might receive $1 billion or more in total from Germany and the USA.

Furthermore, it appears that the global SiC product and device demand is so tight that customers are prepared to pay upfront deposits to secure supply. The CEO said on September 7, 2023, that this additional funding avenue remains open.

All told, that leaves Wolfspeed with $7 billion cash to cover $5 billion capex by FY 2027.

So, despite losing a full year from its operating plans, it seems that Wolfspeed’s funding plans may still be ok albeit that, as always, shareholders would like to see more wiggle room.

I’ve read comments pointing to Wolfspeed’s need to raise additional funds to cover its supposedly burgeoning capex needs. Refer this SA article , noting that the author expresses cash flow concerns but does not have any capex estimates (not his fault, it’s really hard to get any clarity on this topic without doing a lot of digging – IR, please listen up). Anyway, cash flow concerns translate into a clear threat of shareholder dilution which overhangs the stock price, particularly during periods of negative news flow as has occurred since the company missed FY Q4’23 earnings estimates. That’s where we are today – the stock is being hammered by a potential dilution overhang.

However, and after a lot of digging and parsing of statements from investor conference webcasts , it seems that the true funding picture is not unhealthy. As demonstrated above, Wolfspeed has $7 billion available for its $5 billion capex plans. And, if needed, additional backup funding may come from customers along the lines of the Renesas deal. Consequently, I do not see any shareholder dilution on the horizon.

A word about the $2 billion Renesas deal. Renesas , based in Japan, is a leading global supplier of semiconductor-based devices particularly for the automotive and automotive charging industry. Via its July 2023 deal, Renesas secures from Wolfspeed a 10-year SiC device supply deal. Whilst the $2 billion cash is welcome the deal is notable on several levels: (1) It is the largest known advance deposit deal in the semiconductor industry; (2) Renesas chose to do this deal with Wolfspeed and not with any other SiC company , and; (3) This deal speaks volumes about the multi-year thirst for SiC demand that customers like Renesas observe in the pipeline. This burgeoning demand is real and will not disappear any time soon. EV cars, love them or hate them, are the future. Over time they will get better and better and, in the process, will generate a lot more SiC demand.

Valuation

Wolfspeed’s estimated sales for FY 2027 may be about $3.2 billion – being the company’s stated targets for FY 2026. Applying a sales multiple of 6 to 8 gives a range of EV valuations for 2027 of $19.2 to $25.6.

Wolfspeed, at $38 a share, currently trades on a sales/EV multiple of 6.5. Considering that the new larger, automated fabs should significantly boost profitability - EBITDA is expected to grow from 26% of sales to 45% - this should lead to Wolfspeed’s valuation in 3+ years’ time being towards the top of the range, implying a 2027 EV number closer to $25 billion.

Today, based on a $38 share price, Wolfspeed has an EV of $6 billion. For a like for like comparison with the 2027 EV calculation, deduct $1 billion operating cash flow, deduct $2 billion customer advance deposit, and add $5 billion capex. Today’s adjusted EV becomes $8 billion.

Going from $8 billion today to $25 billion in 2027 implies a share price in 2027 of 3.125 time the current $38 share price i.e. about $119.

Note: It was reported on September 22, 2023, that a conglomerate of 4 Japanese companies may be interested in taking a stake in Coherent’s SiC business at a valuation of $5 billion . Wolfspeed’s SiC business is several times larger than that of Coherent (NYSE: COHR ) and Wolfspeed’s entire market cap is currently less than $5 billion. View this as a reality-check, a healthy one.

Investor and Analyst Sentiment

In my view, analysts were noticeably disappointed on Wolfspeed’s FY Q4’23 post earnings conference call. Two issues arose. First, a non-GAAP accounting change whereby startup/underutilized factory costs are to be charged to the P&L whereas previously they had been excluded. This change seems to have been instigated by the SEC. Second, unforeseen delays in ramping the Mohawk fab which have had a knock-on effect re the timing of Wolfspeed’s multi-year plans. These two issues are obviously not sudden events - they would both have been simmering for some time. And yet, no heads-up was provided to either shareholders or to the investment banking community. It’s hard to imagine that some trust was not lost over this episode.

Perhaps the situation is best described by Morgan Stanley in their note dated September 25, 2023:

“Wolfspeed has ‘compelling narrative, but now it’s ‘show-me’ time.”

Acknowledging that sentiment towards Wolfspeed has been poor, analyst Joseph Moore said that sentiment could change if the company could put forth a couple of quarters of significant improvement.

I fully agree.

Furthermore, as an admirer of Warren Buffett, I also consider this dark period to represent a good investment opportunity.

Despite the considerable negativity towards Wolfspeed, it’s not all bad. Yes, they made some mistakes, and they will make more in the future.

I think the overall strategy of the company to be the largest, most automated, lowest cost SiC product supplier is correct. It’s the same strategy followed by Tesla, by Chinese battery makers, by the great robber barons of the early 20 th century (Rockefeller, Carnegie, Ford etc) and in recent decades by many of today’s tech giants. Certainly, it’s far better being the leading lowest cost producer than being one of the many second tier, struggling, also rans.

Still, whilst Wolfspeed will likely retain its title as the leading SiC company, it will inevitably face competition from many market players; Chinese fabs, On, STMicroelectronics etc. Currently, there is an insatiable multi-year demand pipeline and, based on the valuation numbers outlined above, and the steps being taken by management to fulfil their long-term plans, I consider Wolfspeed currently to be a good investment.

Summary

Wolfspeed stock has been beaten down because of temporary issues; glitches in migrating from 150mm to 200mm wafers, delayed sub-station equipment and, also because of an accounting change. The company is on track towards achieving outstanding multi-year growth. Understandably, the market awaits proof of this. In the words of Morgan Stanley Wolfspeed has a compelling story but it’s now “show-me” time.

Wolfspeed awaits confirmation of funding assistance it will get via the US CHIPS Act and the European CHIPS act. News from Europe is expected very soon, according to the company “certainly before 31 December 2023”.

Meanwhile, Wolfspeed’s Mohawk production is set to accelerate sharply at the beginning of calendar 2024.

Currently, there is a lot of negativity baked into Wolfspeed’s share price. However, within just 2-3 months from now, the company can satisfy the show-me audience and the share price will be free to move up.

At $38, the stock represents an attractive buying opportunity and I expect it to triple in the new few years.

Please, please, please do your own research.

Carpe diem.

For further details see:

Wolfspeed: Poised For Supercharged Growth