WOLTF - Wolters Kluwer: A Mix Of Positives And Negatives

2023-09-22 06:22:21 ET

Summary

- I have a favorable opinion of WOLTF's top line visibility supported by recurring revenue streams and its potential to allocate value in an accretive manner with its strong balance sheet.

- But I have concerns about the performance of Wolters Kluwer's Legal & Regulatory Division and the company's future profitability.

- I stick to my existing Hold rating for Wolters Kluwer, after taking into consideration the positive and negatives relating to the stock.

Elevator Pitch

I rate Wolters Kluwer N.V. (WOLTF) [WKL:NA] shares as a Hold.

Previously, I evaluated Wolters Kluwer's sales mix and valuation metrics with my March 15, 2021, initiation article . The focus of my current update is the company's key investment merits and major risk factors.

I have a Neutral view and Hold rating for WOLTF, as I find that there are both positives and negatives for the stock. I like Wolters Kluwer's financial strength and high degree of recurring revenue. However, I am less impressed with the company's elevated staff expenses and its underperforming Legal & Regulatory Division.

Strong Financial Position Supports Value-Accretive Capital Allocation Initiatives

Wolters Kluwer's net leverage or net debt-to-EBITDA metric was reasonably low at just 1.5 times as of June 30, 2023, as indicated in the company's Q2 2023 results presentation . As a comparison, WOLTF disclosed at the company's 2023 Annual General Meeting or AGM (transcript sourced from S&P Capital IQ ) on May 10 that the internal target for its net leverage ratio is much higher at 2.5 times.

The company's comfortable financial position and substantial debt headroom allow it to maintain a good balance between capital investment and capital return.

In its second quarter earnings presentation, Wolters Kluwer outlined its inorganic growth strategy of executing on "bolt-on acquisitions that meet (specific) strategic and financial criteria."

In 2023 thus far, the company has completed two M&A deals. The first transaction is the purchase of Invistics, a company engaged in "drug diversion detection and controlled substance compliance" as highlighted on its website , in June this year. At the beginning of the current year, WOLTF bought over NurseTim, which it referred to as a "provider of nursing education solutions" in its January 9, 2023, press release .

It is reasonable to assume that WOLTF's top line will continue to be boosted by inorganic growth drivers in the foreseeable future. Wolters Kluwer has the financial strength to support future M&As, and it has a clear focus on bolt-on deals.

Separately, Wolters Kluwer is expected to return a meaningful amount of capital to the company's shareholders this year.

The company's 1H 2023 dividend per share of EUR0.72 represents a +14% YoY increase as compared to its 1H 2022 dividend payout of EUR0.63 per share. On the other hand, Wolters Kluwer has already spent EUR503.5 million on share buybacks in the first seven months of this year, which means that the company is on track to meet its EUR1 billion share repurchase goal for the current year.

At the company's AGM in May this year, Wolters Kluwer committed to "rewarding our shareholders with a progressive dividend and a share buyback program", while still having the ability to "take advantage of investment opportunities."

Growing Recurring Revenue Contributions From Expert Solutions

Another key investment merit for Wolters Kluwer is the company's high percentage of recurring revenue, which is supported by the robust growth of its expert solutions business.

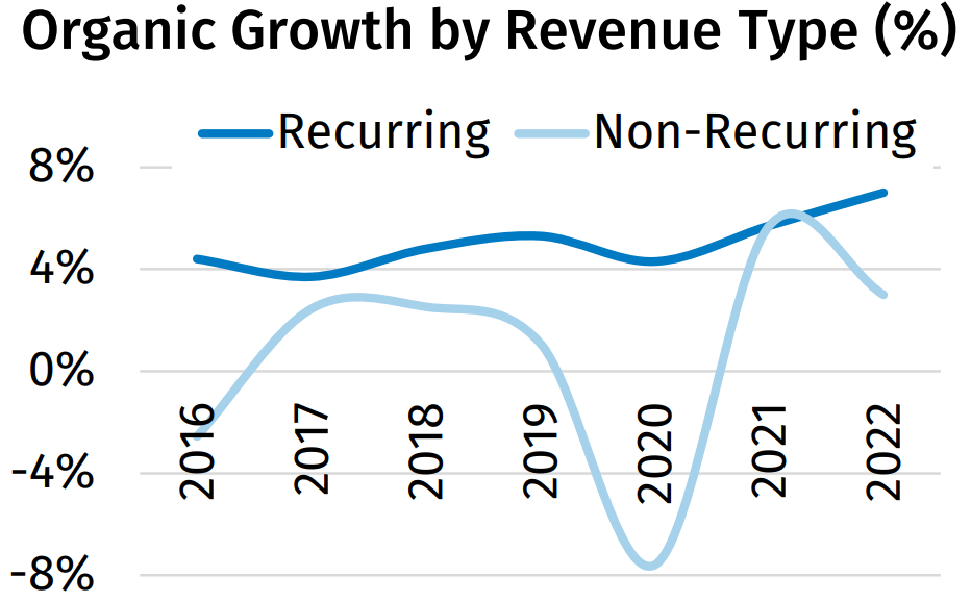

Historical Growth Trends For Wolters Kluwer's Recurring And Non-Recurring Revenue Streams

Wolters Kluwer's 2023 AGM Presentation

{kind=link}

As highlighted in the chart presented above, the company's recurring revenue has grown by at least +4% every year between 2016 and 2022, while its non-recurring revenue has been far more volatile in the same time period.

In other words, a bigger proportion of recurring revenue translates into top line stability for Wolters Kluwer. WOLTF's recurring revenue as a percentage of its total sales was as high as 82% for 1H 2023, and the good performance of its expert solutions business was a key driver.

Revenue derived from the expert solutions business grew by +7% YoY in the first half of this year and accounted for 58% of WOLTF's 1H 2023 top line. In particular, cloud-based expert solutions, a sub-segment of the expert solutions business, saw its revenue increase by +15% YoY for 1H 2023.

Wolters Kluwer explained at its AGM in May 2023 that "a record level of product development spending amounting to 11% of total 2022 revenues" had helped the company grow its revenue generated from expert solutions and recurring revenue sources.

High Personnel Expenses Were A Drag On Profitability

On a constant-currency basis, WOLTF's organic revenue expanded by +6% YoY in 1H 2023, but the company's normalized EPS only increased by +2% YoY in the same time frame.

Wolters Kluwer's operating profit margin contracted by -2.1 percentage points from 28.2% in 1H 2022 to 26.1% for 1H 2023, and this explained why the company's bottom line expansion was inferior to its top line growth.

The company noted in its Q2 2023 results presentation that the "increase in personnel cost" was the key item that hurt its profitability. Wolters Kluwer also acknowledged at its 2023 AGM that "we do see wage inflation on the increase with the current inflationary environment."

WOLTF's profit margins might still be under pressure in the second half of 2023. Based on the sell-side analysts' consensus financial forecasts sourced from S&P Capital IQ , Wolters Kluwer's normalized net profit margin is estimated to contract by -210 basis points YoY and -150 basis points HoH (Half-on-Half) to 18.2% for 2H 2023.

Legal & Regulatory Is A Weak Spot

Wolters Kluwer's Legal & Regulatory division was the worst performing segment for the company in 1H 2023.

The company's Legal & Regulatory division suffered from a -3% YoY top line contraction in the first half of the year. On the flip side, the other three divisions (Health, Tax & Accounting, Governance, Risk & Compliance) achieved positive YoY revenue growth in the first half of the year. Furthermore, the Legal & Regulatory segment's operating profit margin declined from 16.5% in 1H 2022 to 14.2% for 1H 2023.

At the AGM in May, WOLTF noted Legal & Regulatory is "still our most print-centric division" and mentioned that this division "operates over a number of different geographies all across Europe unlike some other divisions."

Print as a media format is suffering from secular challenges, so this will hurt the Legal & Regulatory division's revenue growth outlook. Also, the profitability upside for the Legal & Regulatory division driven by scale economies is limited by its geographically dispersed operations. This division has a presence in multiple European markets, which makes it hard to build up scale in any single market to benefit from positive operating leverage.

Closing Thoughts

Wolters Kluwer is still rated as a Hold. WOLTF isn't a clear-cut Buy or Sell, as there are both risks and rewards associated with a potential investment in the stock.

For further details see:

Wolters Kluwer: A Mix Of Positives And Negatives