WOLTF - Wolters Kluwer: A Well-Managed Company But Not Cheap

Summary

- Wolters Kluwer is a leader in providing professional information (health, legal, tax, etc.).

- The company jumped on the digitalization-train and now generates a substantial portion of its revenue from digital offerings.

- The stock isn't cheap, but Wolters may be worth it.

Introduction

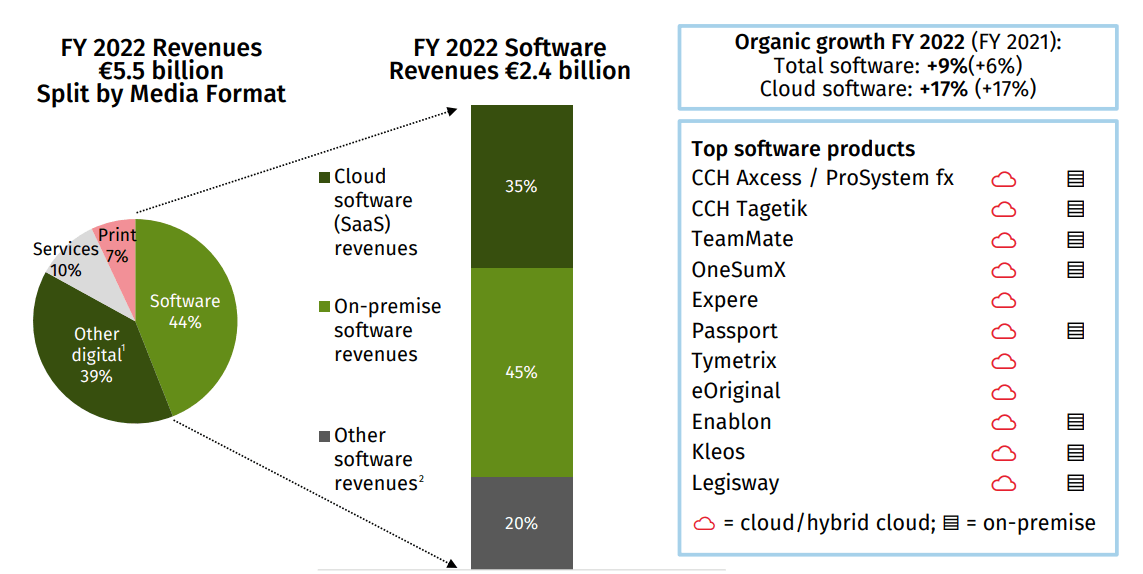

Wolters Kluwer ( WTKWY ) ( WOLTF ) is one of the global leaders in professional information where it has obtained a very strong position in the health, tax & accounting and risk & compliance sector. Wolters Kluwer used to be just a publishing house but hasn't missed the digitalization and the vast majority of its revenue is generated through digital formats (including software and online subscriptions to services).

Wolters Kluwer Investor Relations

Wolters Kluwer's primary listing is on Euronext Amsterdam where the stock is trading with WKL as ticker symbol . The average daily volume in Amsterdam is almost half a million shares per day, which represents a monetary value of in excess of 50M EUR. As it clearly is the most liquid listing, I'd recommend to trade in Wolters stock using the Amsterdam listing. Wolters Kluwer reports its financial results in Euro, so I will use the Euro as base currency throughout this article.

{kind=link}

In excess of 1B EUR of free cash flow in 2022

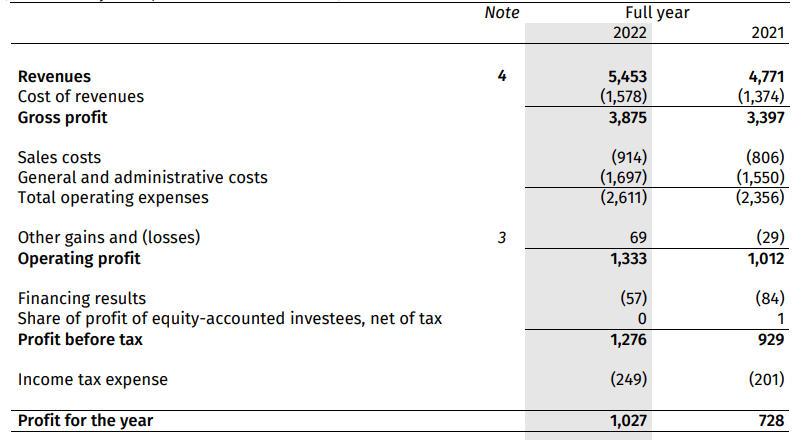

2022 was another year of strong growth. Wolters saw its revenue increase from 4.77B EUR to 5.45B EUR , an increase of just over 15%. Meanwhile the COGS increased at a slightly faster pace which resulted in a gross profit of 3.88B EUR, an increase of approximately 14%.

{kind=link}

But as Wolters Kluwer was able to keep the increase of its other operating expenses relatively low with an increase of just over 10%, the operating profit excluding the other gains and losses came in at 1.27B EUR versus 1.04B EUR in 2021, that's a 23% increase.

{kind=link}

The financing expenses continue to decrease and Wolters had to spend just 57M EUR on these expenses which resulted in a pre-tax income of 1.28B EUR and a net income of 1.03B EUR, an increase of in excess of 40%. The EPS came in at 4.03 EUR (up from 2.79 EUR) per share but that is based on the average share count of 254.7M shares for the year. Keep in mind that as Wolters continued to repurchase stock throughout the year, it ended the year with less than 249M shares outstanding and if you would use the existing share count instead of the weighted average, the EPS would be approximately 2% higher at just over 4 EUR per share.

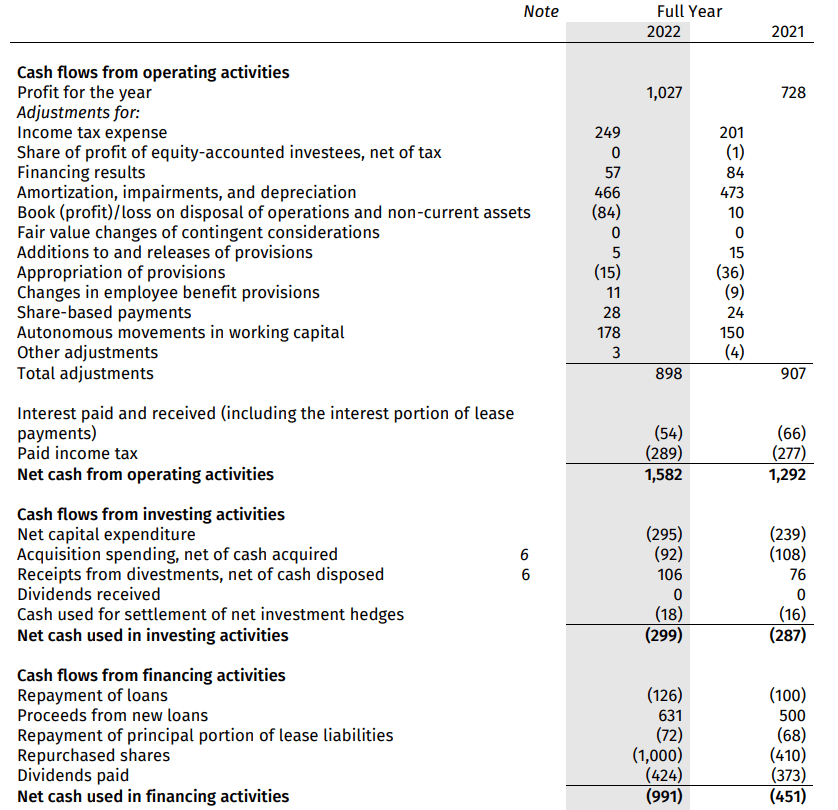

Thanks to the robust gross margins, Wolters Kluwer really is a cash flow story. The reported operating cash flow came in at 1.58B EUR but we need to deduct the 40M EUR in taxes paid that weren't owed based on the FY 2022 income statement while we should also deduct the 72M EUR in lease payments.

{kind=link}

This means the adjusted operating cash flow was roughly 1.5B EUR and with a total capex of just 295M EUR, the free cash flow result was 1.2B EUR. Keep in mind this includes 178M EUR in working capital changes so on an underlying basis, the free cash flow was approximately 1.02B EUR. Divided over the current share count, the free cash flow result per share came in at 4.10 EUR.

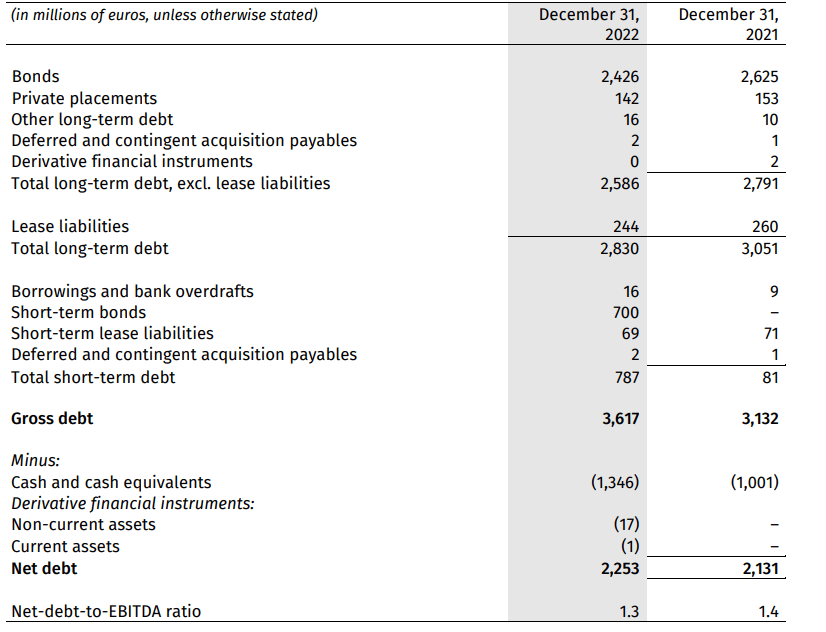

As of the end of 2022, Wolters Kluwer had approximately 2.25B EUR in net debt (including lease liabilities) for a debt ratio of 1.3 times EBITDA. That's very manageable and as Wolters expects its EBITDA to increase again this year, the debt ratio will likely continue to decline, even if Wolters doesn't reduce its net debt by a single Euro.

{kind=link}

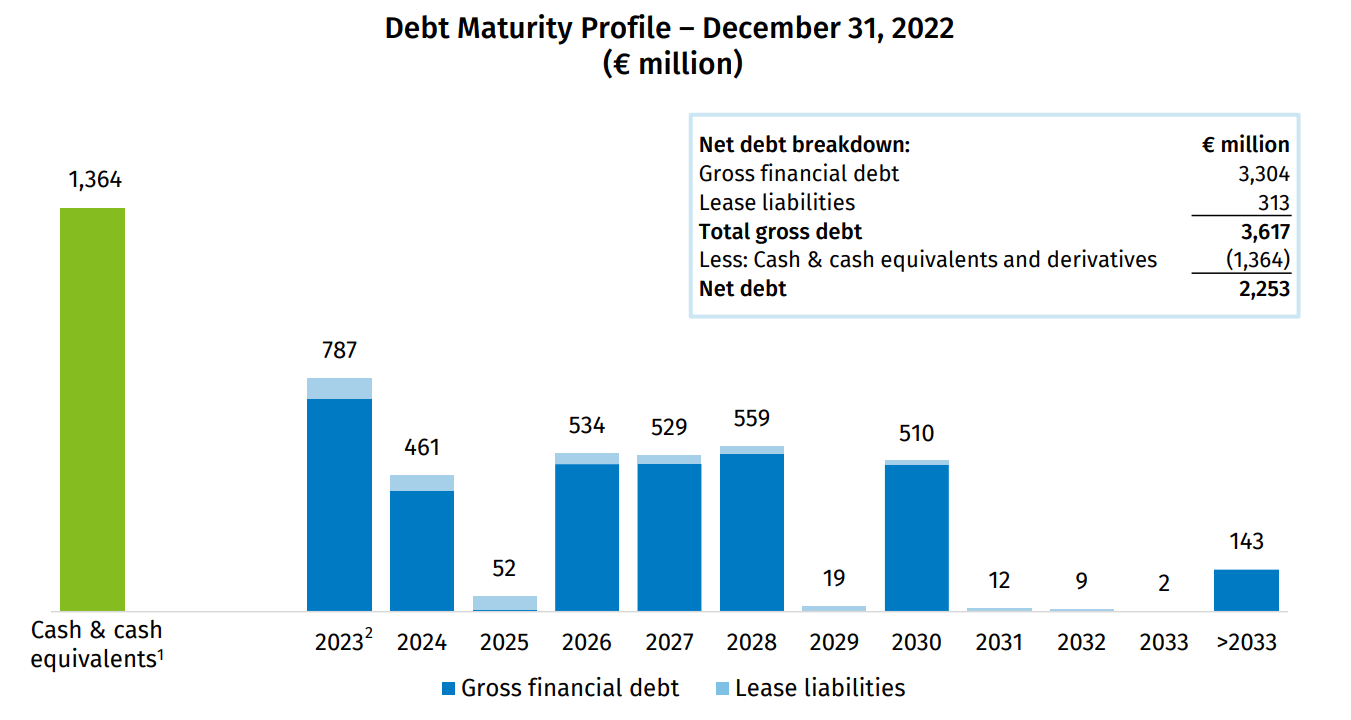

I don't expect debt or interest expenses to be a major issue. Right now, Wolters has enough cash on its balance sheet to cover all repayments until 2026 . And that ignores the cash that will come in during those years.

{kind=link}

Of course, Wolters won't be immune to increasing interest rates but looking at the bond market, it looks like the increases might be pretty benign. The 2027 bonds currently have a yield to maturity of 3.5% and even if I would use an average cost of debt of 4%, the total interest expenses would increase by just 60-70M EUR, which is just 2% of the revenue. So one inflation-related revenue hike would take care of the increased interest expenses, which explains why I'm not too worried.

Investment thesis

I usually would ignore a stock trading at a free cash flow yield of 3.7%. But Wolters Kluwer is appealing anyway as A) the company has not missed the digitalization trend and B) its dominant position in its core markets and the constant need for professionals to stay up to date on relevant news and updates are giving Wolters some moat. On top of that, as per the 2023 guidance , the ROIC will come in at 16.5-17% this year and the free cash flow should reach 1.2B EUR (although this includes changes in the working capital position so I am taking the guidance with a grain of salt). The dividend should increase as well from the 1.81 EUR that will be paid based on the 2022 performance.

The company is currently also working on a 1B EUR share buyback program which will reduce the share count by an additional 3-4% and this helps to boost the diluted adjusted EPS by a 'high single digit' percentage this year. Which likely means we can expect an EPS of around 4.4 EUR per share and an underlying free cash flow result that should be pretty similar.

I currently have no position in Wolters Kluwer as I always thought the company was expensive. Although WKL isn't cheap (trading at approximately 16.5 times EBITDA and a 4% FCF yield for this year), I now understand the appeal. I'm in no rush to get in, but I think any major correction on the markets would be a good opportunity to initiate a long position.

For further details see:

Wolters Kluwer: A Well-Managed Company, But Not Cheap