WWW - Wolverine World Wide: A Case For Cautious Optimism

2023-10-25 13:14:13 ET

Summary

- Wolverine World Wide has reduced its inventory by $97.3 million in the first two quarters of 2023, signaling a move towards leaner operations and better cost management.

- The company is focusing on growth through innovative products and its global direct-to-consumer footprint, offering multiple avenues for revenue growth.

- Despite short-term setbacks, Wolverine World Wide's proactive strategies position it well to navigate macroeconomic challenges and capture a larger market share in the long run.

- The company has a high shareholder yield and has maintained dividend payments for 36 consecutive years.

- Analysts anticipate sales declines in the current year.

Investment Thesis

Wolverine World Wide Inc. (WWW) presents a complex investment case with both promising operational strategies and concerning financial indicators. Its focus on inventory management and cost efficiencies, coupled with its global footprint and diversified sales channels, position it well for potential long-term growth. However, the company's high Debt Paydown Yield and declining EBITDA growth rates raise concerns about its liquidity and long-term profitability. The mixed financial signals make this a risky investment, particularly in a volatile market impacted by rising interest rates and inflation. Therefore, while the stock appears to be fairly valued at its current price, caution is advised.

Additionally, the company's downward revision in both revenue and EPS forecasts for Q3 2023 is concerning. It casts doubts on the company's near-term performance and could be indicative of deeper operational challenges that have yet to be addressed. In a volatile market marked by rising interest rates and inflation, these negative indicators cannot be ignored.

Given these varying factors, a 'Hold' recommendation seems most appropriate for current investors, who should keep a close eye on the Q3 earnings release and any strategic changes in the company. The investment thesis thus suggests caution and close monitoring of near-term performance indicators. For risk-averse investors, I believe it is better to sell the stock.

Overview

Wolverine World Wide specializes in the design, marketing, and licensing of footwear, apparel, and accessories. It aims to inspire and empower consumers to lead active lives, and its brands have an impressive reach, available in 170 countries. Though the company has navigated through a series of challenges-such as supply chain disruptions, increased inventory levels, and escalating costs- the firm has been proactive in inventory management. Specifically, it reduced its inventory by $97.3 million in the first two quarters of 2023 compared to Q4 of 2022. This move signals a tilt towards leaner operations and better cost management, especially significant in a market landscape fraught with macroeconomic pressures.

WWW is actively pushing for growth through multiple channels. A critical part of its strategy is the focus on innovative products and compelling brand propositions. The company is leveraging its global direct-to-consumer footprint and supply chain excellence as key growth catalysts. The DTC model is promising, offering higher margins and more substantial consumer data for personalization. Moreover, the company's existing footprint in 170 countries presents a springboard for global expansion through third-party distributors, licensees, and joint ventures, thus offering multiple avenues for revenue growth.

The industry outlook also complements WWW's proactive strategy. The retail environment is in turmoil, courtesy of rising interest rates, inflation, and escalating energy prices. However, WWW seems to be a step ahead, focusing on inventory management and cost efficiencies. This proactive approach will likely give them an edge over competitors who are more reactive to these macroeconomic challenges. Financially, the company has a clear roadmap. It targets a return to a 12% operating margin and plans a significant profit improvement by 2024. To bolster its liquidity and overall financial health, WWW is targeting a $225 million reduction in inventory by year-end.

However, there are a few red flags. The company faced a margin contraction of 430 basis points in Q2 2023 and ended the quarter with a net debt of $930 million. The company aims to reduce it to approximately $850 million, which is a step in the right direction. The abrupt CEO change, bringing Chris Hufnagel to the helm, does introduce an element of instability. However, Hufnagel seems to bring a fresh perspective, emphasizing brand-building and consumer-centric strategies that could reshape the company's future prospects for the better.

In comparison to industry benchmarks, WWW's recent performance saw its shares fall by 26%, and a cut in its full-year operating margin guidance from 8.5% to 5.0%. However, these are short-term setbacks. The company's targeted inventory reduction and focus on margin improvement demonstrate a commitment to long-term financial health. Overall, Wolverine World Wide is in a transitional phase, both in terms of leadership and strategy. Their emphasis on DTC growth, inventory management, and supply chain improvements could serve as significant catalysts for future growth. Despite the industry's macroeconomic challenges, WWW's proactive strategies position it well to not only navigate the storm but possibly come out stronger, capturing a larger market share in the long run.

Financial Analysis

{kind=link}

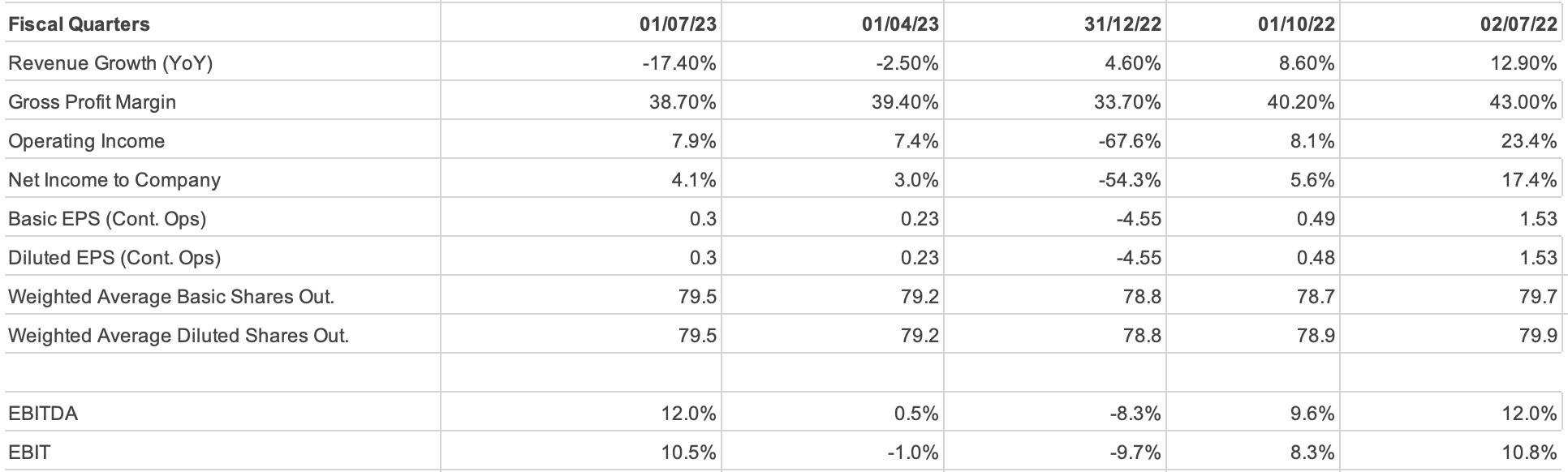

The company focuses on three segments - Active Group, Work Group and Life Style Group. The revenue for the Active Group, the company's main revenue generator, fell from $428.3M to $383.3M, marking a 10.5% decrease for the quarter and a 0.7% year-to-date drop. Similarly, the Work Group saw its revenue shrink from $139.5M to $117.8M, constituting a 15.6% quarterly and 16.4% year-to-date decrease. The Lifestyle Group experienced a drop from $121.1M to $74.9M, translating to a 38.2% quarterly and 30.1% year-to-date fall. The Other segment also declined from $24.7M to $13.1M, a 47% quarterly and 42.7% year-to-date drop.

This downward trend is consistent across all business segments, leading to a total revenue decrease from $713.6M to $589.1M, a 17.4% quarterly and a 10.5% year-to-date slump. The revenue decreased from $1,328.4M in H1 2022 to $1,188.5M in H1 2023, a 10.5% drop. The cost of goods sold fell by 11.1% quarterly and 4.7% half-yearly, indicating that the cost savings didn't translate to higher profits. Thus gross profit plummeted by 25.8% quarterly and 18.4% half-yearly.

But it's not just the revenue; operating profits are also in decline. The Active Group's operating profit fell from $72.7M to $39.8M, a 45.3% quarterly and 27% year-to-date decrease. The Work Group's operating profit decreased from $28M to $14.8M, a 47.1% quarterly and 43.4% year-to-date decline. The Lifestyle Group's operating profit dropped from $16.6M to $10.4M, a 37.3% quarterly and a 55.7% year-to-date decrease. Even at the corporate level, the operating profit moved from a positive $46.2M to a loss of $22M, a sharp 147.6% quarterly and 76.6% year-to-date decline. Consequently, the total operating profit decreased from $167.9M to $46.1M, a 72.5% quarterly and 51.3% year-to-date decrease.

The situation highlights some red flags. The Active Group generates most of the revenue, making the company vulnerable to any downturns in this segment. Secondly, the decline in operating margins across all segments, such as the Active Group's drop from a 16.9% operating margin to 10.3%, indicates reduced operating efficiency, possibly due to rising costs and operational inefficiencies. Thirdly, the overall decline in both revenue and operating profit suggests poor quality of earnings, raising questions about the company's long-term profitability.

Based on these trends, Wolverine World Wide would need a significant shift in strategy to reverse the negative trajectory. All segments are experiencing declines, which implies a systemic issue rather than isolated challenges in specific groups.

If the current trends persist, Wolverine World Wide can expect further contractions in both revenue and operating profit in the coming year.

Balance Sheet Analysis

The current assets have seen a year-over-year decline from $1,293.3 million to $1,163.9 million, a drop of 10%. Further, accounts receivable plummeted by 42.5%, from $420 million to $241.5 million, which could indicate faster collections and reduced sales. However, cash and cash equivalents improved by 18.2% to $176.5 million, providing some liquidity cushion. On the flip side, total inventories only slightly increased from $639.5 million to $647.9 million, a hike of 1.3%, which is concerning when juxtaposed with declining revenues.

Turning to long-term assets, we see a 12.9% reduction in goodwill, from $539.1 million to $469.7 million, suggesting the possibility of asset impairments. Total assets declined by 20.1% to $2,357.3 million. As for liabilities, there's an 11.9% year-over-year decrease in total current liabilities, from $1,094.7 million to $964.2 million. This could reflect debt repayment and a decrease in operational costs, but it adds stress to the company's liquidity, as confirmed by the current ratio of 1.21 and quick ratio of 0.43. Long-term debt saw a reduction from $727.4 million to $718.5 million, a decline of 1.2%, signaling that the company hasn't made significant repayments on its long-term obligations.

The company's retained earnings fell by a quarter, from $1,246.1 million to $933.8 million, possibly due to high dividend payouts and capital reinvestment in underperforming units. The debt-to-equity ratio stands at 1.96, indicating a high level of leverage and associated risk, especially if interest rates rise or revenues continue to slump.

In terms of forward-looking analysis, the consistent decline in both assets and retained earnings could put Wolverine in a difficult liquidity position. The decreasing trend in accounts receivable and retained earnings signifies a contraction in business activities and profitability, highlighted by a deteriorating operating margin. With high leverage and declining sales, the company's capital structure is heavily skewed towards debt, making it vulnerable to interest rate risks and cyclical downturns in its industry.

To sum it up, Wolverine's financials raise multiple red flags: high leverage, declining accounts receivable, and a decrease in goodwill, all pointing towards eroding financial health. These issues are corroborated by the SWOT analysis, which highlights strengths in liquidity but major weaknesses in revenue, profits, and leverage, compounded by threats from market demand decline and profitability.

Free Cash Flow Analysis

{kind=link}

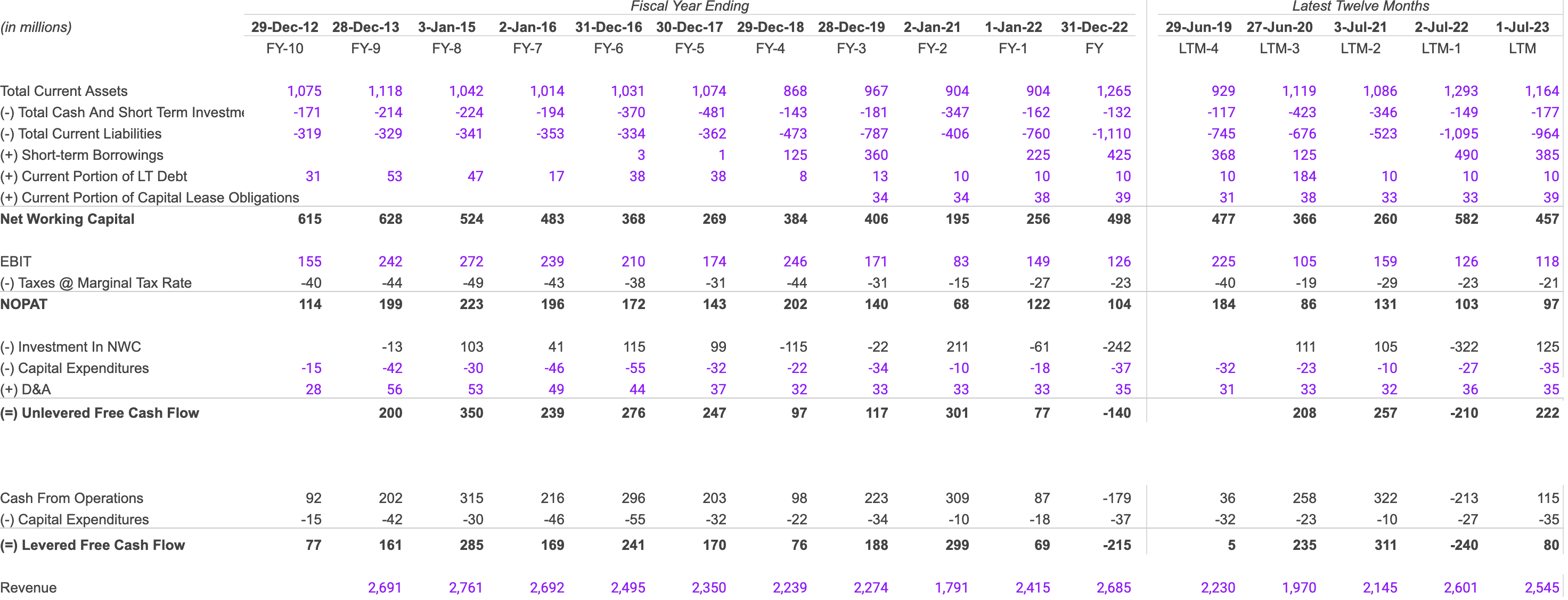

The total current assets increased by 19.05% from 2021 to 2022 but dropped by 9.98% in 2023, signaling liquidity issues that could affect the company's ability to pay off short-term debts. Net working capital followed a similar pattern: a drastic 123.85% increase from 2021 ($260 million) to 2022 ($582 million), then a 21.48% decrease to $457 million in 2023. This fluctuation is concerning for the company's short-term obligations. Revenue grew by 21.26% in 2022 but decreased by 2.15% in 2023, raising a red flag for future profitability.

The current ratio decreased from 2.08 in 2021 to 1.18 in 2022, and slightly improved to 1.21 in 2023. Despite the drop, it stays above 1, suggesting the company is still capable of covering its short-term liabilities. The debt-to-equity ratio shows inconsistency, being high at 1.85 in 2021, dropping to 0.97 in 2022, and slightly increasing to 1.16 in 2023. This fluctuation indicates a moderately leveraged capital structure, which could be risky if interest rates rise.

Capital Expenditures increased year-over-year: -$10 million in 2021, -$27 million in 2022, and -$35 million in 2023. This could be a sign of investment for future growth. At the same time, the company has declining working capital and volatile cash flows. For instance, Unlevered Free Cash Flows (UFCF) were $257 million in 2021 but went negative to -$210 million in 2022 and rebounded to $222 million in 2023. Levered Free Cash Flows (LFCF) also fell from $311 million in 2021 to -$240 million in 2022, before rising to $80 million in 2023. This volatility indicates a potential instability in cash generation, impacting debt servicing and shareholder returns.

To sum it up, while there are positive aspects like a high current ratio and potential growth indicated by CapEx, there are critical areas of concern such as declining working capital, inconsistent Debt to Equity ratios, and volatile cash flows.

Shareholder Yield

{kind=link}

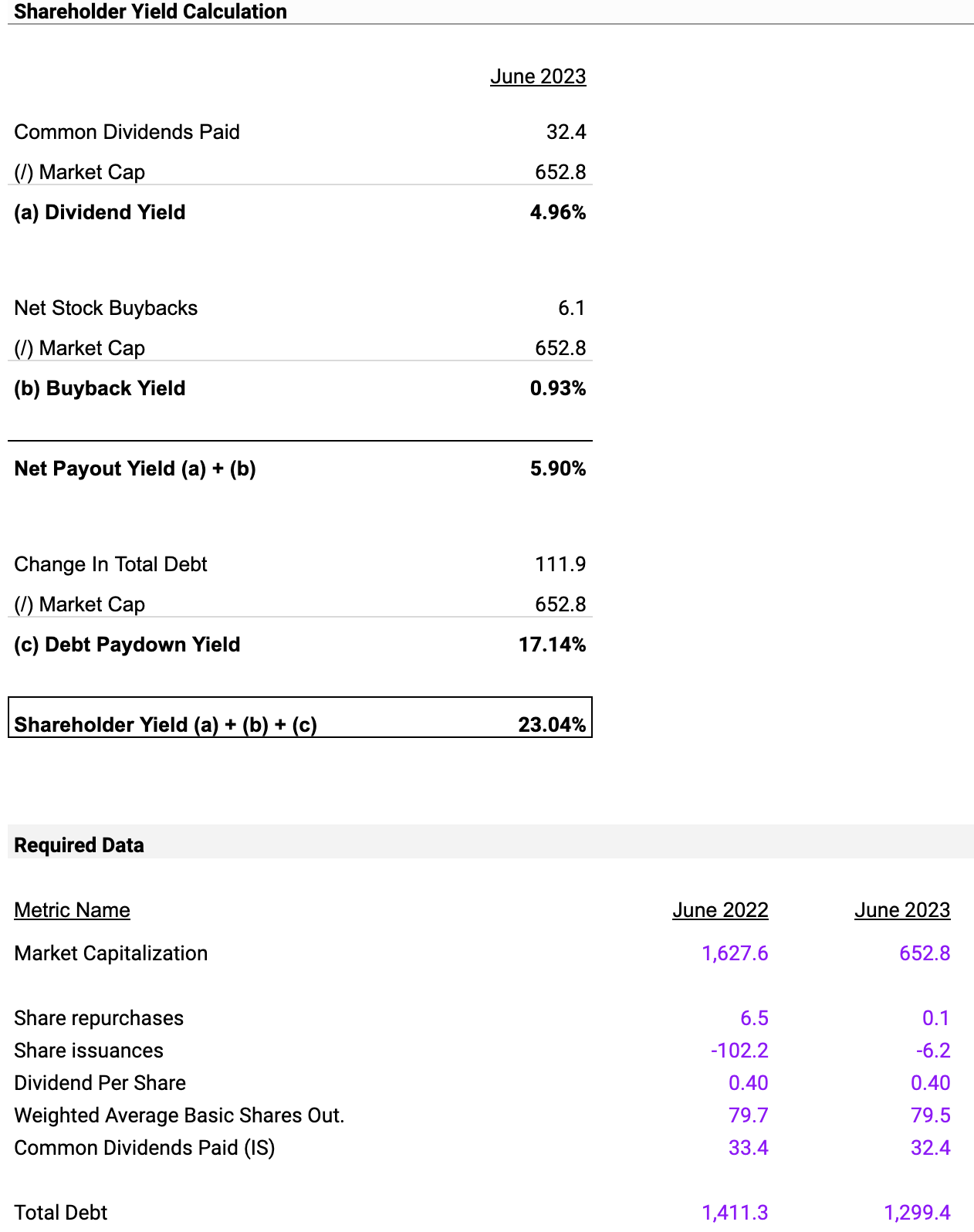

The Dividend Yield stands at 4.96%, calculated by dividing the common dividends paid of $32.4 million by the market capitalization of $652.8 million. While this could attract income-focused investors, it also hints that the company is not significantly reinvesting in growth. The Buyback Yield is comparatively low at 0.93%, calculated by dividing the net stock buybacks of $6.1 million by the same market cap. This implies that while the company sees its stock as undervalued, share buyback isn't a major part of its capital allocation plan. When combined, these yield a Net Payout Yield of 5.90%, suggesting a balanced approach to capital return to shareholders. On the other end, the Debt Paydown Yield is 17.14%, determined by dividing the change in total debt ($111.9 million) by the market cap. This indicates that the company is aggressively focusing on debt reduction, which could be good for long-term financial health but might stifle short-term growth opportunities.

Adding up the Dividend Yield, Buyback Yield, and Debt Paydown Yield, the total Shareholder Yield comes out to 23.04%. This high yield reveals a company highly committed to returning value to shareholders, whether that's through dividend payments, stock buybacks, or debt reduction. If the company maintains its current focus on debt and payout yields, investors should expect moderate returns and potentially lower future growth. In terms of financial health, while the company is solvent thanks to its focus on debt reduction, liquidity could be a concern, particularly if the company faces any operational hiccups.

In a nutshell, while the high Debt Paydown Yield and moderate Net Payout Yield provide an attractive short-term return for shareholders, they also signal potential limitations in operational flexibility and growth. The company's approach seems to be a defensive play, which while financially prudent, could leave it exposed to liquidity risks and operational challenges, especially in an economic downturn.

Earnings Preview For Q3 2023

{kind=link}

The company will announce its Q3 results on November 8, 2023.

The financial data for Wolverine World Wide Inc. shows changes in both revenue and Earnings Per Share forecasts from June to September 2023. Specifically, the average revenue forecast in June 2023 was $582.97 million, while in September 2023, it dropped to $513.937 million. This represents a contraction of approximately 11.84% in revenue estimates. Similarly, the average EPS forecast also decreased from 0.19 in June to 0.083 in September, showing a significant contraction of about 56.32%.

In summary, Wolverine World Wide is experiencing a downward trend in both revenue and EPS forecasts from June to September 2023. The revenue estimates declined by almost 12%, while the EPS faced a much steeper decrease of over 56%. These contractions might signal caution for potential investors in evaluating the company's near-term financial prospects.

Valuation

Analyzing the fair value of Wolverine World Wide Inc. is crucial for investors seeking to gauge its investment potential, and EV/EBITDA is an excellent metric for this purpose. EV/EBITDA offers a comprehensive picture of a company's valuation and profitability, eliminating the effects of different capital structures and tax environments. In the case of Wolverine World Wide Inc., this metric is particularly useful given the company's diversified product lines and international operations, which could involve complex tax and financial arrangements.

{kind=link}

For a comparative valuation, we include Crocs Inc. (CROX), Skechers U.S.A., Inc. (SKX), Deckers Outdoor Corporation (DECK), Steven Madden, Ltd. (SHOO), and Rocky Brands, Inc. (RCKY). These companies are selected because they operate in the same footwear and apparel industry and share a comparable business model, involving both retail and wholesale distribution channels. It's reasonable to assume that these companies are exposed to similar market trends and risks, thereby making the comparison meaningful.

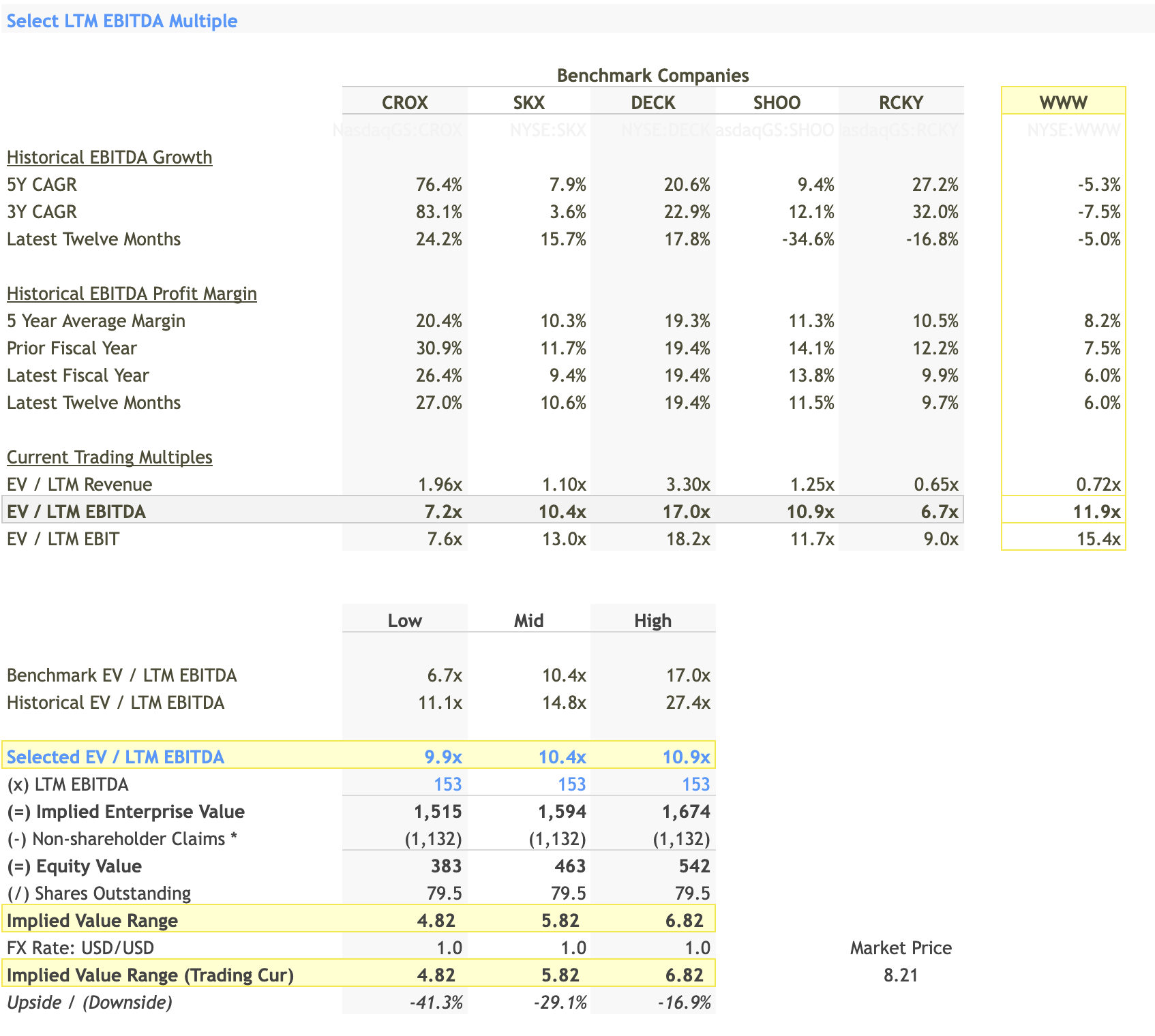

Select LTM EBITDA Multiples

{kind=link}

The historical EBITDA growth rates and margins among the benchmark companies vary significantly. Wolverine World Wide Inc. shows negative growth rates in the 5-year (-5.3%) and 3-year (-7.5%) CAGR, contrasting sharply with, for example, Crocs, which has a 5-year CAGR of 76.4%. The LTM EBITDA multiple of Wolverine World Wide Inc. stands at 11.9x, which is higher than its peers except for Deckers Outdoor Corporation (17.0x). For instance, Crocs and Rocky Brands have LTM EBITDA multiples of 7.2x and 6.7x, respectively. This is significant considering Wolverine's negative EBITDA growth over the last 5 years (-5.3%) and 3 years (-7.5%). This discrepancy between a high multiple and low growth can be a red flag. It suggests that the market might be overvaluing Wolverine, and that there are expectations of a turnaround. Given these considerations, a mid-range LTM EBITDA multiple of 10.4x is selected for the valuation, which aligns more closely with Skechers' 10.4x and Steven Madden's 10.9x.

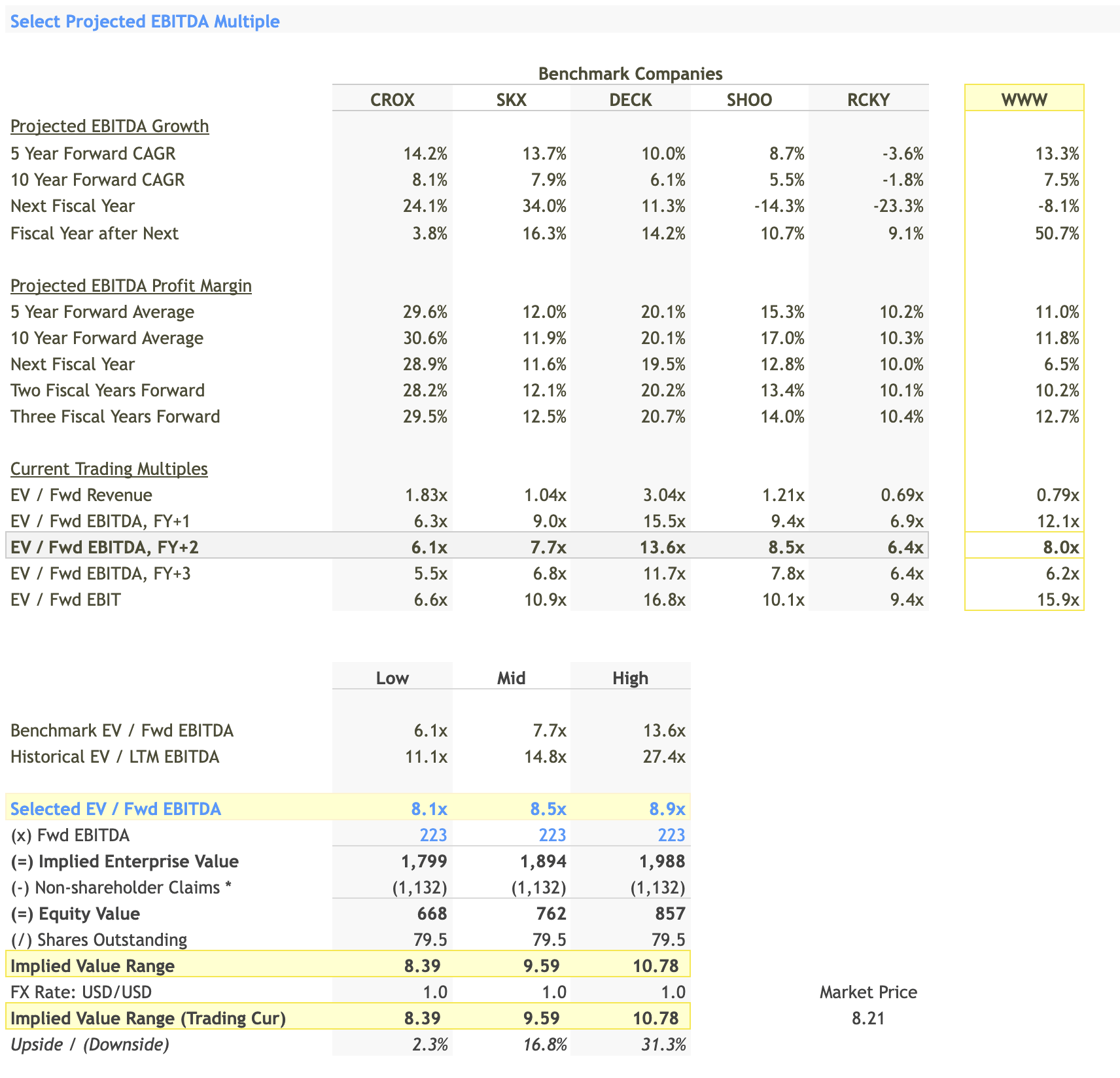

Select Projected EBITDA Multiples

{kind=link}

The forward-looking EBITDA growth rates are positive for Wolverine World Wide Inc., with a 5-year forward CAGR of 13.3%. This positive outlook suggests that the company might be on a path to recovery or growth. However, its EBITDA margin is projected to be around 11.0%, which is lower than Crocs' projected 29.6%. Given this, and considering that Skechers and Deckers have forward multiples of 9.0x and 15.5x, respectively, a conservative projected EBITDA multiple of 8.5x is considered appropriate for Wolverine.

Fair Value Range

{kind=link}

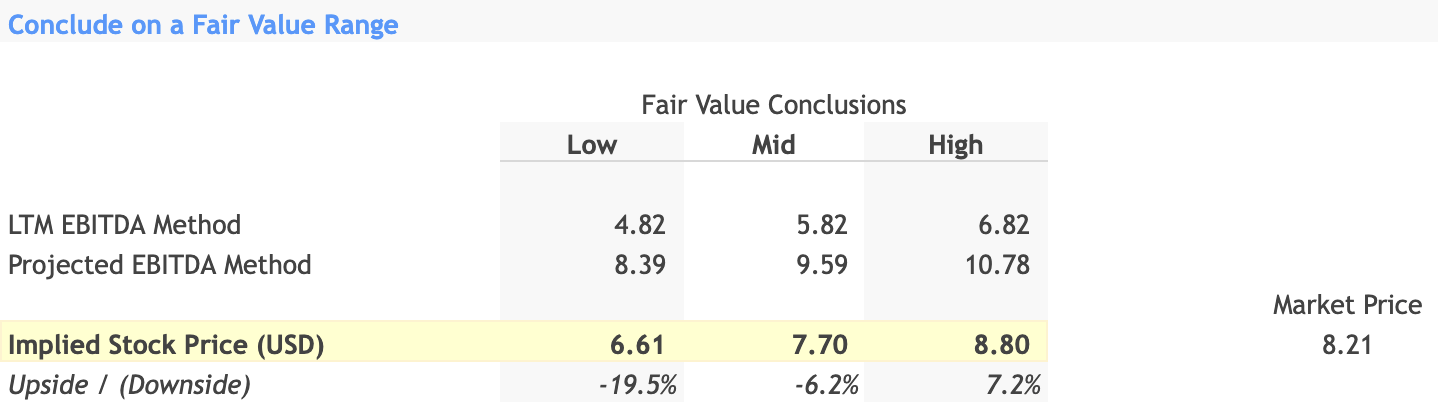

The fair value range was calculated using the selected LTM and projected EBITDA multiples. Using the LTM EBITDA method, the implied stock price ranged from $4.82 to $6.82. Using the projected EBITDA method, the range was significantly higher, from $8.39 to $10.78.This broad range suggests a high level of uncertainty around Wolverine's valuation.

Conclusion and Investment Decision

Combining both the LTM and projected EBITDA methods, we arrive at an implied stock price range of $6.61 to $8.80.

The LTM EBITDA method suggests a more conservative valuation, while the projected EBITDA method is more optimistic, primarily due to expected EBITDA growth. Given the current market price of $8.21, the stock seems fairly valued, leaning slightly towards being undervalued. If we weigh in the company's focus on reducing debt and a reasonable forward EBITDA growth projection, a "Hold" decision seems appropriate at this point.

At the same time, the company has shown a negative EBITDA growth rate over both the last 5 and 3 years, standing at -5.3% and -7.5% respectively. This historical contraction in profitability raises concerns about the company's ability to grow earnings moving forward, and it forms a strong basis for a "Sell" recommendation. Further, the company has a high Debt Paydown Yield of 17.14%. While this could be seen as a positive from a financial stability standpoint, it also raises flags about liquidity constraints. With aggressive debt paydown, the company is likely allocating a significant chunk of its free cash flows towards reducing liabilities, leaving less room for operational flexibility and unexpected challenges.

However, given the negative growth rates in the past, it may not be a strong "hold" either unless there are clear indicators of a strategic turnaround. Thus, my recommendation is to Hold for investors who already own the stock and wait to see if there is a turnaround considering the change in the leadership. For risk-averse investors, I would suggest not investing in this stock considering the current operational issues the company faces.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Wolverine World Wide: A Case For Cautious Optimism