WWW - Wolverine World Wide: Critical Improvements Highlighted In ICR Conference

2024-01-09 16:50:24 ET

Summary

- Wolverine World Wide has had issues in the company's brands' demand also resulting in deteriorating margins. The deteriorating earnings are leveraged by a high amount of debt.

- The company is focusing on turning around its business through several cost cuts, and an improved marketing & offering, as well as strategic divestments.

- The impact on revenues is yet to be largely seen, as the company still had a 20.8% revenue decrease in Q4 with preliminary figures.

- The current valuation seems to price in a fair baseline scenario. The investment case is very volatile, but I see the current price as reflective of fair current assumptions.

Wolverine World Wide ( WWW ) manufactures, markets, and distributes shoes as well as other apparel with a global presence. The company has a number of self-owned and licensed brands , including Wolverine, Merrell, Bates, Cat Footwear, Chaco, Harley-Davidson Footwear, Hush Puppies, Sweaty Betty, and Saucony.

The stock hasn’t been a great investment in past years. The stock has lost around 70% of its value in the past decade, and the company’s current dividend yield of 5.17% doesn’t excuse the poor appreciation. With a currently leveraged balance sheet and problems in keeping up a good earnings level, the dividend also seems to be in danger of a cut. While the company is focusing on transforming the business for a better future growth, as presented in the ICR Conference, results are yet to be largely seen in the financial performance.

{kind=link}

Ten Year Stock Chart (Seeking Alpha)

Financial Improvements Are Needed

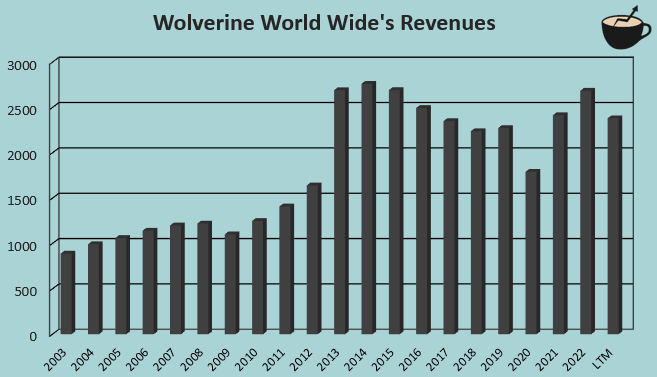

After the company achieved a good amount of growth in the 2000’s and in 2013 through an acquisition, Wolverine World Wide’s revenue profile has deteriorated. The company has seen several years of decreasing revenues , as revenues are still currently below the 2013 level with an acquisition and some divestments between the periods.

{kind=link}

Author's Calculation Using TIKR Data

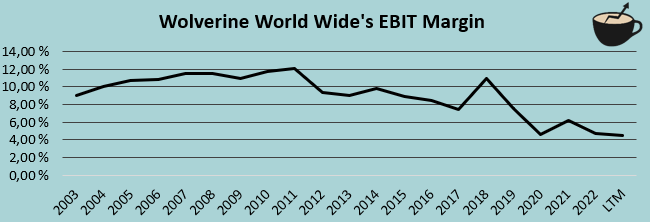

The poor financial performance doesn’t stop at revenues – the sales trend has followed into decreasing EBIT margins. The margins have gone from double digits in the 2000’s into a current trailing EBIT margin of 4.6%. While gross margins have stayed mostly stable, the lower sales level and slightly expanding SG&A have created issues in the earnings level.

{kind=link}

Author's Calculation Using TIKR Data

On top of a weak longer-term performance, the current financial profile for the company is terrible. The company reported its Q 4 preliminary results on January 8th, in cluding revenues of $527 million for the quarter. The result implies a wide year-over-year revenue decrease of 20.8%, deepening the company’s issues. In the Q3 earnings call , CFO & executive VP Michael Stornant relates the current issues to a soft macroeconomic environment, a hike category decline and grey market selling for Merrell, as well as a mismatch in the company’s production and customers’ demand in the quarter, including a lack of new products and color & trend missteps. While the decreases seem to be greatly impacted by temporary effects, some of the mentioned reasons could also signify longer-term negative effects. For example, I wouldn’t expect grey market selling to stop, or the company to necessarily to be able to renew its offering within trends very quickly. With a currently large debt balance of around $1.1 billion, shareholders are very leveraged, making the deteriorating earnings even more worrisome.

The ICR Conference – A Transformation In Progress

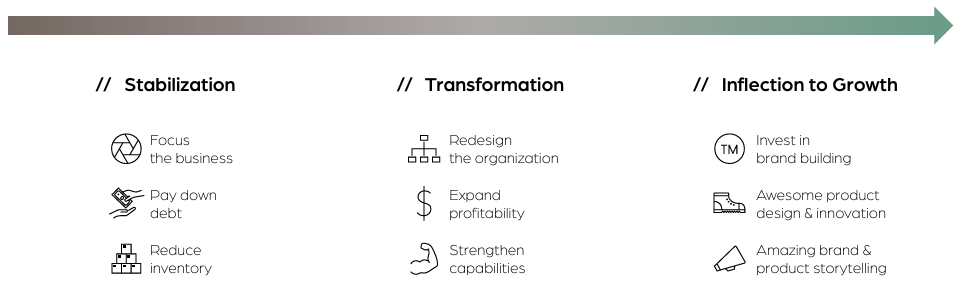

On the 8 th of January, Wolverine World Wide participated in the ICR Conference with a presentation & webcast . The company represented its strategic focus on the brand portfolio and financial profile. The strategic focus points were mainly in line with already introduced strategic initiatives , including the already sold businesses, the planned sale of the Sperry brand, and a further simplification of operations. The strategy going forward relies on first stabilizing the business, and then transforming the company to be capable for growth through building brands.

{kind=link}

Phases of Planned Company Transformation (WWW 2024 ICR Conference Presentation)

Wolverine World Wide has already progressed well in the pursuit to focus the business, including the sale of Keds and Hush Puppies’ intellectual property in China. The company is still in the process of finding alternative solutions for the Sperry brand, in my opinion most likely also ending up in the sale of the brand. While the business refocus has provided a good amount of proceeds from the non-core divestments, shareholders aren’t seeing the capital in the near term – as the company has a large amount of outstanding debt, the company plans to pay down a significant amount of debt with the proceeds. I believe that the debt paydown is a very good, and critical step in stabilizing the company’s future financials.

Refocus Initiatives (WWW 2024 ICR Conference Presentation)

The most critical part of the strategy in my opinion is the targeted profitability expansion. Quite impressively, the company expects annual gross savings of $215 million from organizational improvements, supply chain optimization, and other cost saving initiatives. Of the amount, Wolverine World Wide communicates to have realized $75 million in 2023 – with the guidance, around $140 million in further savings should still be seen in forward years. In addition, Wolverine World Wide expects supply chain costs to decrease due to transitory costs realized in 2023. Savings of $140+ million would make the company’s earnings profile very different, but I remain on the side of caution – despite high savings, the worrying sales trend is still continuing, possibly negating some of the savings’ effects with negative operating leverage in the future.

The company also introduced a number of product portfolio advancements, including new shoe models for Merrell, Saucony, and new apparel for Sweaty Betty. While the introduced products were not jaw-dropping, the conference did also show Wolverine World Wide’s initiatives in creating a more competitive offering and better-refined brands through a better marketing, showing interest in operational improvements instead of only capital allocation strategy. The improvements can’t yet really be seen in terms of better financials, though; I remain quite skeptical about the operational improvements until I see proof in better financials.

A Volatile Investment Case

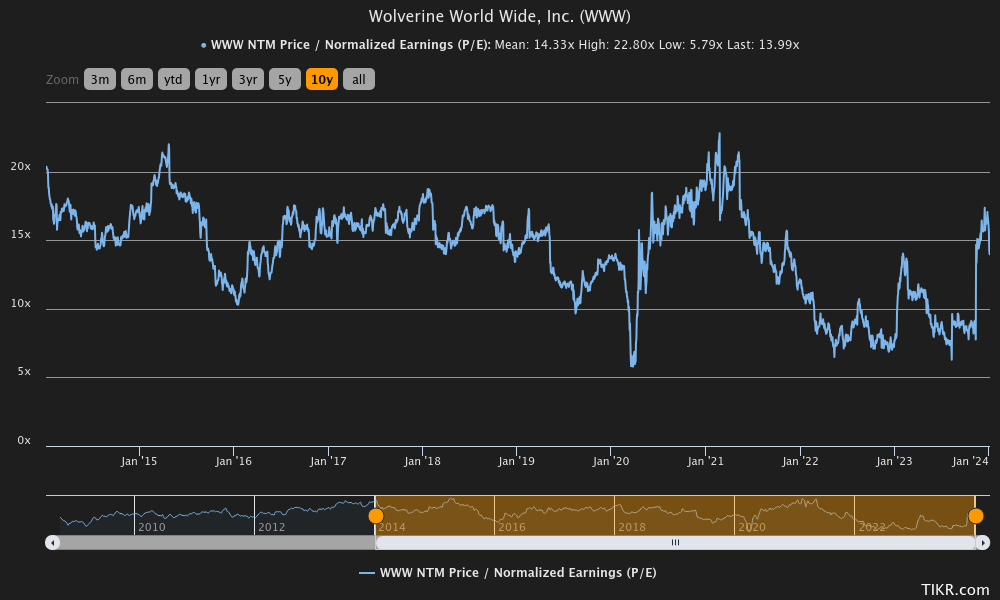

Wolverine World Wide currently has a forward P/E multiple of 14.0, near the company’s ten-year average of 14.3 – despite volatility, the multiple has landed near the historical average, not signaling an over- or undervaluation in terms of the history.

{kind=link}

Historical Forward P/E (TIKR)

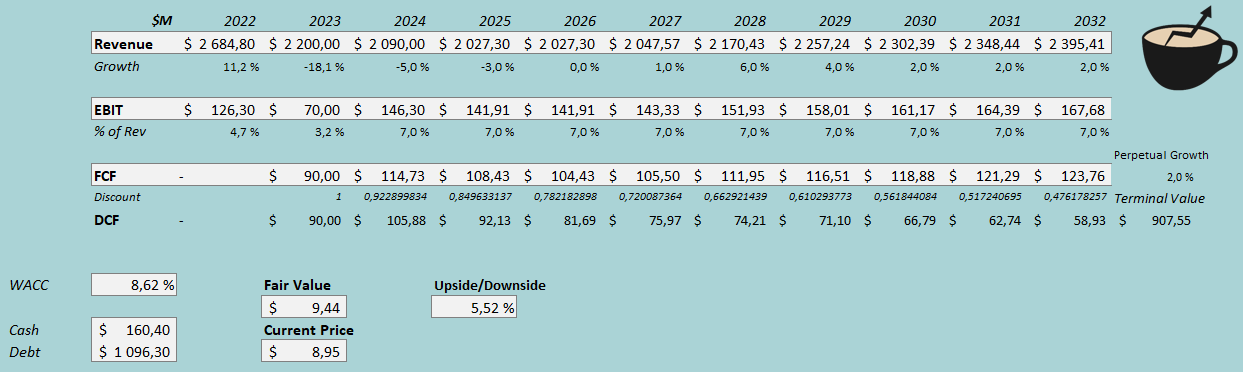

To estimate a fair value for the stock, I constructed a discounted cash flow model. In the DCF model, I factor in financials where Wolverine World Wide is able to slowly turn around its topline from decreases into a couple of years of growth; after 2023, I estimate revenues to still decrease in 2024 and 2025. Slowly, I estimate the marketing and other initiatives to have an effect on demand, recovering the revenues into a modest and temporary growth for 2028 and 2029. Afterwards, I estimate a perpetual growth of 2%, demonstrating a stable demand.

For the margins, I estimate a significant jump after 2023. Due to the company’s cost savings, and an eventually improving consumer spending, I estimate the EBIT margin to jump from 3.2% in 2023 into 7.0% in 2024 and forward. As Wolverine World Wide has minimal growth in the estimates, I believe the company should have a good cash flow conversion going forward, including inventory reductions in Q4/2023.

With the mentioned estimates along with a cost of capital of 8.62%, the DCF model estimates Wolverine World Wide’s fair value at $9.44, around 6% above the stock price at the time of writing; the stock seems to be valued roughly for the financials that I estimate. It has to be noted, though, that the investment case is incredibly volatile – financials for the future are still quite tough to predict, and the company’s debt balance further leverages the estimates’ effect on the stock value. If marketing efforts are better than I estimate, the stock could easily turn into a very worthy investment. On the other hand, if cost improvements fail and margins continue on the long-term downward trend, the stock could be near worthless.

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Wolverine World Wide had $15.5 million in interest expenses. With the company’s current amount of interest-bearing debt, Wolverine World Wide’s annualized interest rate comes up to 5.66%; while a high-risk company, Wolverine World Wide has quite a reasonable interest rate. The company’s balance sheet is likely to stay highly leveraged for a long while, which is why I estimate a long-term debt-to-equity ratio of 80%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.01% . The equity risk premium of 4.60 % is Professor Aswath Damodaran’s latest estimate for the United States, made on the 5 th of January. Yahoo Finance estimates Wolverine World Wide’s beta at a figure of 1.71 . Finally, I add a small liquidity premium of 0.25%, crafting a cost of equity of 12.13% and a WACC of 8.62%.

Takeaway

Wolverine World Wide currently has very rough financials. The company has a large amount of debt, so the poor long-term revenue and margin trends are highly leveraged for shareholders. The company acknowledges issues with the operations, and has communicated planned improvements both in the ICR Conference and prior to the event. The communicated cost savings are very significant, and the company also targets to improve the brands’ image through a better branding and offering. Currently, I believe that the stock is valued for a fair baseline scenario, but the investment case is very volatile due to the mentioned factors. Until the financial performance is shown to be either better or worse than I anticipate, I have a hold rating.

For further details see:

Wolverine World Wide: Critical Improvements Highlighted In ICR Conference