WWW - Wolverine World Wide's Valuation And Mediocre Competitive Profile Make It A 'Hold'

2023-10-26 07:36:48 ET

Summary

- Wolverine World Wide operates in the competitive footwear, apparel, and accessories industry, with a diverse brand portfolio and operational efficiency.

- Despite declining revenue and escalating supply chain costs, WWW's strategic restructuring and revised revenue outlook indicate stability and potential for long-term growth.

- Sales of non-core assets like Hush Puppies intellectual property and U.S. WWW Leathers business are part of the restructuring strategy to channel resources towards growth-oriented brands.

- However, stagnant revenues and lukewarm competitive dynamics overshadow its near-term potential, making WWW stock a "hold" for now.

Wolverine World Wide ( WWW ) operates within the highly competitive landscape of footwear, apparel, and accessories, marrying a rich heritage with a forward-thinking, growth-oriented strategy to address market challenges. The company's diverse brand portfolio and operational efficiency position it distinctively within the consumer discretionary sector, notably the footwear industry. Despite experiencing a 14% YoY revenue decline in Q2 2023 and escalating supply chain costs, WWW's asset restructuring and revised revenue outlook indicate stability. In my opinion, the proactive measures taken toward debt reduction, brand development, and effective inventory management exhibit a potential for long-term growth, which is a persuasive indicator of the company's strategic foresight. Moreover, it could lead WWW to benefit from secular tailwinds. However, the present scenario of stagnant revenues and lukewarm competitive dynamics overshadow its near-term potential. This is a concern for investors seeking immediate returns. Consequently, my valuation model suggests that the shares are valued appropriately, rendering WWW a "hold" at current market levels.

Business Overview

Wolverine World Wide is a global footwear, apparel, and accessories player with a heritage from 1883. It operates through three segments—Active Group, Work Group, and Lifestyle Group, designing, manufacturing, and marketing a wide range of products across multiple regions, including the United States, Europe, and Asia Pacific. WWW's brand portfolio includes casual, performance outdoor, athletic, and industrial footwear, among others. Notable brands under its umbrella are Bates, Cat, Chaco, Harley-Davidson, Hush Puppies, Merrell, and Saucony, along with licensing agreements for the Stride Rite brand. The company extends its brand equity beyond footwear with apparel and accessories under the Merrell and WWW brands. It also licenses non-footwear products like Hush Puppies apparel and WWW-branded eyewear. The WWW Leather division markets pigskin leather, while its sourcing division offers extensive consulting services in product development, quality assurance, and materials procurement.

In my view, WWW's diversified brand portfolio and strategic focus on operational efficiency have positioned it distinctively within the consumer discretionary sector, especially in the footwear industry. This is evident from its ongoing efforts to streamline operations and foster brand resonance through a mix of retail stores, third-party licensees, and consumer-direct e-commerce platforms. The company employs around 4,300 individuals, showcasing a significant footprint in its domain. I believe the blend of heritage, diversified brand portfolio, and a modern approach to market outreach encapsulates the essence of WWW's business model, current developments, and its journey to its present status. This dynamic approach amplifies its market presence and forms the bedrock of its revenue generation strategies. Through the lens of revenue generation, the strategic divestitures and operational streamlining are particularly commendable as they align with current market demands while upholding the rich heritage that WWW is known for.

Realignment, Competitive Profile, and Market Position

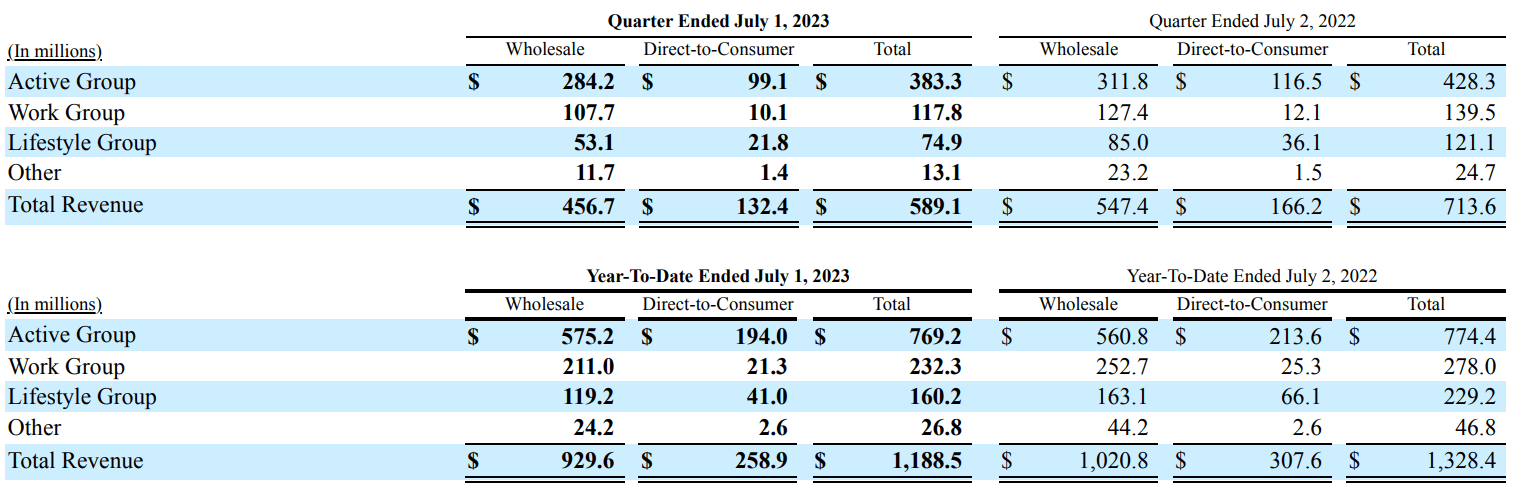

The figures from the segments reveal a marked decline in revenue and operating profit for the quarters ended July 1, 2023, and July 2, 2022. The Work, Lifestyle, and Active segments bear the brunt of this downturn more than the Active and Other segments. The transition of the Active segment from profitability to a loss is striking. I believe these declines underscore possible operational challenges, necessitating a strategic re-evaluation to strengthen financial performance.

{kind=link}

WWW’s divestiture of certain intellectual properties and businesses, like the sale of the Hush Puppies intellectual property in select Asian regions for $58.8 million and the U.S. WWW Leathers business to New Balance for around $6 million, underscores a keen focus on channeling resources towards growth-oriented brands and enhancing shareholder value?. Additionally, the sale of the Keds brand to Designer Brands, Inc. aligns with this transformative agenda, as does WWW’s reaffirmed 2023 outlook and the strategic alternatives for the Sperry brand?. Financially, WWW is currently dealing with supply chain costs estimated at $90 million in 2023, with a forward outlook toward mitigating inventory liquidation costs?.

Furthermore, the company's latest earnings call disclosed revenue of $578 million for Q2 2023, marking a 14% YoY decrease. The adjusted gross margin was 39%, falling short of expectations due to a slump in full-price sales and lower margin shipments. Additionally, while liquidating old inventory adversely affected gross margins, it facilitated a $25 million greater reduction in stock than originally planned, bringing the adjusted operating margin to 5.8%. Looking ahead to the close of 2023, the company has revised its revenue projection to $2.26 to $2.28 billion, driven by cautious retail practices and order cancellations. This new forecast indicates a decrease from the prior gross margin guidance of 42% to 40%.

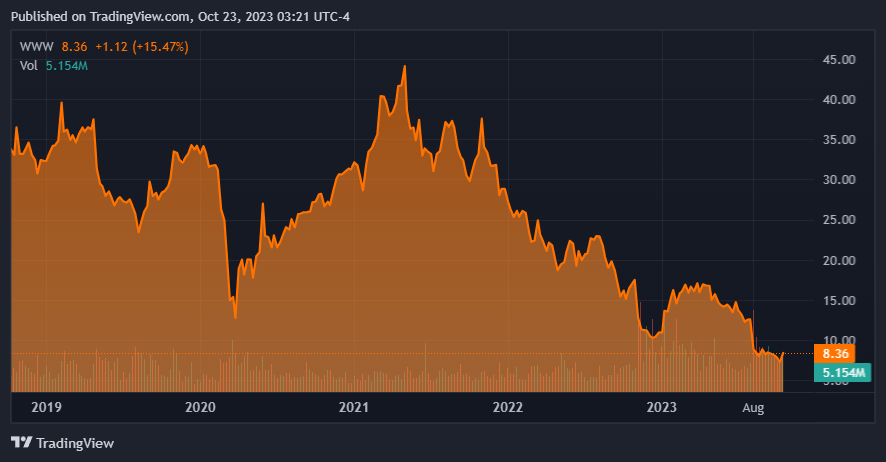

WWW has had stagnant revenues and even worse stock performance. (TradingView.)

{kind=link}

Despite this, a strategic blueprint is in place for profit augmentation and debt diminution in the upcoming months, eyeing an operating margin of 12% for 2024 . The revenue estimate for Q3 2023 is pegged at approximately $515 million, marking a 21% decline YoY. Among the financial tactics deliberated was the divestiture of non-core assets aimed at lowering the year-end net debt to circa $850 million , with a further descent to sub $700 million envisioned by the close of the subsequent year. Lastly, the focus was directed toward brand development and adept inventory management as crucial catalysts for growth and heightened financial resilience amidst the ongoing market adversities.

A cautious projection for H1 2024 was articulated during the Earnings Call, paired with hopes of a rebound in H2 2024, substantially driven by Direct-to-Consumer (D2C) sales. There's an underscored need for a solid product pipeline in 2024 to maintain consumer allure and stimulate sales. Brand dynamics displayed a spectrum, with Merrell gaining traction in market share in the hiking niche while Saucony experienced a downturn. Despite the dichotomy in performance, the overarching brand vitality is viewed as strong, although there's a recognized imperative for enhanced brand cultivation and product ingenuity. The journey toward exploring strategic avenues for Sperry remains in full swing, with a formal marketing document expected to emerge soon. Transitory expenses, primarily from supply chain and surplus liquidation, are forecasted to recede by 2024.

Source: Technavio, from Cision - MediaStudio View Media.

A notable shift in international business is observed between Q3 and Q4 due to early sales of the spring line to international distributors. The projected growth in the global footwear market between 2023 and 2027, with a CAGR of 5.69% , presents an opportunity for WWW to expand its market share and revenue. However, the intense competition from leading brands could pose a challenge. The market dynamics in APAC and Europe, being significant consumption regions, might influence WWW's strategic market positioning and investment in innovation to meet consumer preferences, enhance brand appeal, and maintain a competitive edge. The company's ability to navigate these market conditions will be crucial for its growth and profitability.

Valuation Analysis

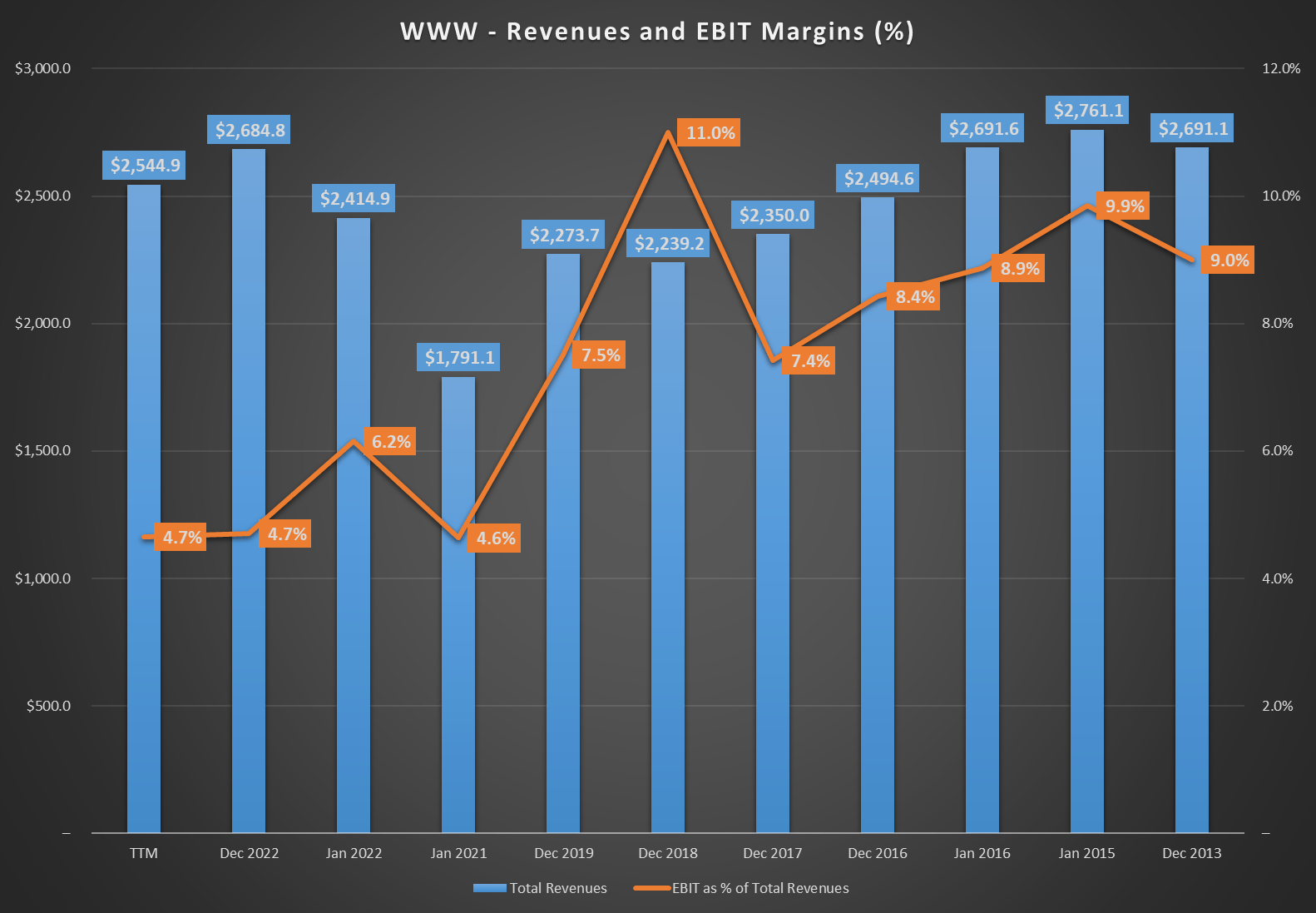

From a numbers perspective, WWW hasn’t established itself as a growth entity in recent years. Specifically, since 2013, the revenue pattern of WWW has largely remained stagnant, showing a minor decline. This static performance could indicate a competitive weakness compared to dominant market competitors such as Nike and Adidas. My assessment is supported by the broader market dynamics, where the footwear industry has seen a noticeable expansion since 2013, with the growth expected to continue at a CAGR of 5.69% through 2027. On the contrary, the revenue of WWW has experienced a CAGR of -0.03% over the same period, which I believe suggests a declining market share. If sustained over time, this negative market share trend could present serious concerns for investors. The divergence between the industry growth and WWW's revenue trajectory underscores the competitive challenges faced by WWW. I believe addressing these competitive gaps is essential for WWW to improve its market position and provide a favorable return to its investors.

{kind=link}

Nevertheless, we can value WWW by utilizing its historical data , analysts' forecasts for 2023 and 2024, and the historical metrics for D&A, CAPEX, NOWC, and Taxes. Using an FCFF DCF model, I discounted the anticipated cash flows at the firm's WACC, which is 7.9%. This rate is considerably lower than the 13.3% discount rate derived from the CAPM, a discrepancy primarily attributable to WWW's leveraged balance sheet . WWW's enterprise value (EV) is pegged at $1.79 billion, with its debt accounting for $1.30 billion of this valuation. Consequently, the composition of its EV is significantly debt-driven, constituting 72.7% of the value.

This high debt ratio has a diminishing effect on WWW's WACC. In my view, the lowered WACC due to the leveraged balance sheet presents a mixed financial outlook for WWW. While on the one hand, it implies a lower cost of capital, which can be advantageous in growth and expansion strategies, on the other hand, it underscores a potentially higher financial risk due to the sizable debt portion. The current credit rating of Ba1 and Ba2 for WWW suggests a bond yield of roughly 6.72% , which effectively mirrors the forward cost of debt for the company. I believe that the Ba1 and Ba2 credit ratings, albeit not in the prime grade, still offer a glimpse of creditworthiness that could help to restructure the debt or seek better financing terms to improve WWW’s financial resilience.

Author's elaboration.

Upon careful analysis, my valuation model suggests that WWW is appropriately valued at its present levels. WWW's historically stagnant revenues, coupled with its mediocre competitive standing, underscores the rational pricing of its shares in the market. I believe these factors collectively justify a neutral stance. Hence, a "hold" rating for WWW at this juncture is sensible, primarily due to its prevailing market valuation, which accurately mirrors its financial and competitive dynamics. Despite the average competitive positioning, this balanced position is further supported by the relative stability in the company's revenue streams over the years. Accordingly, it's prudent to maintain a cautious approach toward any immediate action on WWW's shares until a significant change is observed.

Conclusion

WWW’s blend of heritage and modern, growth-oriented strategies to tackle its market challenges makes it a notable company in the consumer discretionary sector. However, its diversified brand portfolio and operational adeptness, particularly within the footwear industry, are not without hurdles, as evidenced by a 14% YoY revenue decline in Q2 2023 and rising supply chain costs. Still, as WWW focuses on reducing debt, enhancing brand value, and proficiently managing inventory, it unfolds a spectrum of potential long-term growth catalysts. And I believe WWW’s stagnant revenues and mild competitive dynamics raise a valid concern for investors. Accordingly, my valuation analysis indicates that the shares are reasonably priced at this stage, leading to a "hold" rating for WWW.

For further details see:

Wolverine World Wide's Valuation And Mediocre Competitive Profile Make It A 'Hold'