WWW - Wolverine World Wide: There Are Still Better Fits Out There

Summary

- Wolverine World Wide announced financial results covering the final quarter of the company's 2022 fiscal year.

- Despite financial results being in-line with expectations, overall financial data was mixed.

- This performance continues a disappointing trend and shares are not cheap enough to justify a purchase because of that.

Generally speaking, I tend to stay away from the fashion industry. This is because of the highly competitive nature of it, the sometimes rapidly changing consumer attitudes toward particular brands, and other reasons. However, every so often, I will find a fashion-oriented company that is interesting to me. One such firm is Wolverine World Wide ( WWW ), a producer and seller of casual footwear and apparel, performance outdoor and athletic footwear, industrial work boots, and more. Recently, financial results reported by management have been quite mixed. That creates a problem, even though shares look reasonably attractive from a valuation perspective. Ideally, I would love nothing more than to see the company get to a point where it would make sense for a value-oriented investor like myself to buy into it. Unfortunately, after the earnings release that the company reported covering the final quarter of its 2022 fiscal year, I remain unconvinced that the day in question is near.

Still not a great fit

Back in late September of 2022, I found myself drawn to Wolverine World Wide. At the time, I felt as though shares of the company were attractively priced. However, the mixed operating history of the firm was a big downside to me. After all, I place a lot of value on financial performance consistency. On top of that, I was turned off by general market uncertainty and the fact that there were cheaper prospects in the same space that Wolverine World Wide operates in that were more appealing at the time. Because of this, I ended up rating the business a ‘hold’ to reflect my view that shares should generate upside or downside that would more or less match the broader market moving forward. Since then, the company has underdelivered. While the S&P 500 is up 9.2%, shares of Wolverine World Wide have generated a loss for investors of 3.2%.

{kind=link}

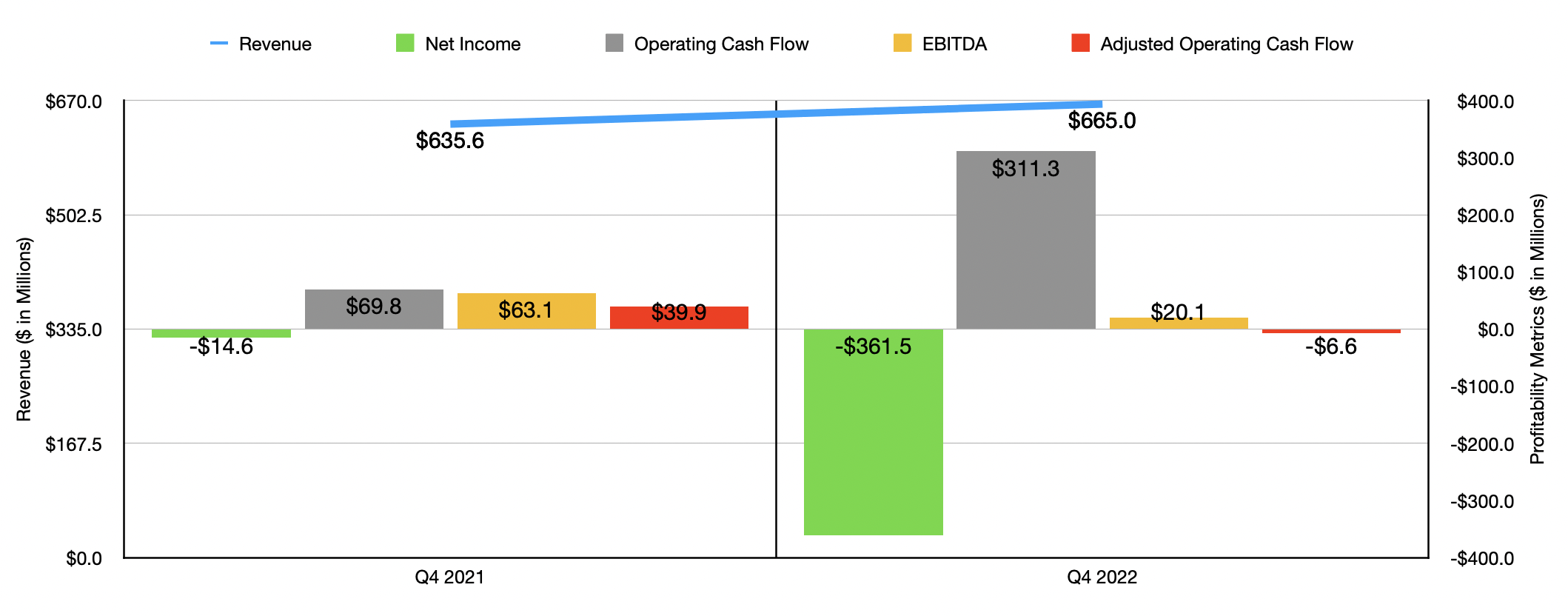

This return disparity was in spite of a 6.3% surge in share price on February 22nd. That move higher was driven by financial results covering the final quarter of the company's 2022 fiscal year. For the most part, the picture was not all that bad. Revenue of $665 million came in approximately in line with what analysts anticipated. It also represented an increase of 4.6% over the $635.6 million reported for the final quarter of the company's 2021 fiscal year. It's important to note that, under the hood, there's a lot going on here. For instance, had it not been for foreign currency fluctuations, sales growth would have been 8.4% year over year. But even factoring that in, we see a lot of volatility based on the company's different segments. On a GAAP basis, its Active Group segment reported a year-over-year increase in sales totaling 16.8%. The Work Group also increased, inching up 3.3% year over year. However, there were portions of the company that worsened during this time. For instance, the Lifestyle Group reported a 20.6% drop in revenue, while all other brands combined reported a decline of 35.1%.

On the bottom line, things looked really messy. The company went from generating a net loss of $14.6 million in the final quarter of 2021 to generating a net loss of $361.6 million in the final quarter of 2022. This implied a loss per share for the quarter of $4.59, missing analysts' expectations by $4.40. However, on an adjusted basis, the loss per share of $0.15 was in line with what analysts expected. This massive disparity between earnings and adjusted earnings was driven largely by a $428.7 million impairment associated with goodwill and other intangible assets that the company booked during the quarter. Other profitability metrics were also mixed. Operating cash flow, for instance, surged from $69.8 million to $311.3 million. If we adjust for changes in working capital, however, it would have declined from $39.9 million to negative $6.6 million. Meanwhile, EBITDA for the company plunged from $63.1 million to $20.1 million.

{kind=link}

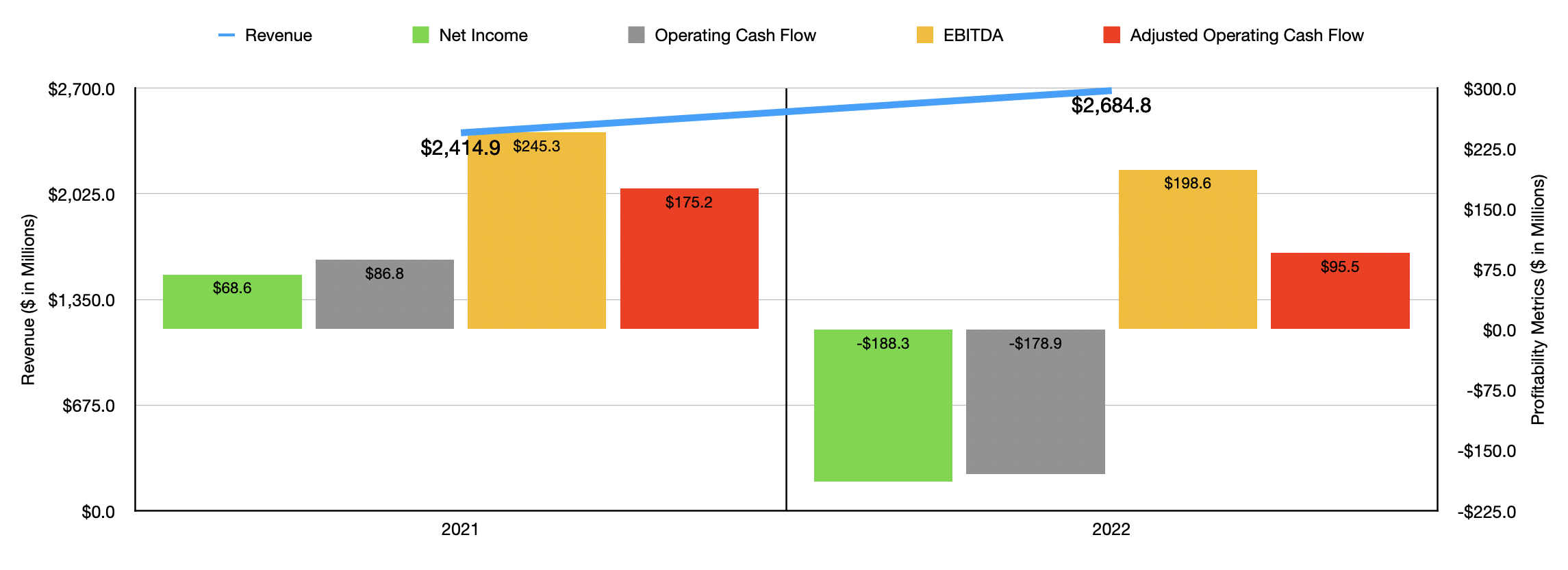

The messy fourth quarter of the year also resulted in the year as a whole being messy. Revenue of $2.68 billion reported for all of 2022 came in nicely above the $2.41 billion reported for the 2021 fiscal year. On the other hand, profits plunged from $68.6 million to negative $188.3 million. Operating cash flow followed a similar trajectory, declining from $86.8 million to negative $178.9 million. On an adjusted basis, it also dropped, declining from $175.2 million to $95.5 million. And finally, EBITDA for the company shrank from $245.3 million to $198.6 million.

When it comes to the 2023 fiscal year, management said that revenue should come in slightly lower than it did in 2022. The current forecast is for sales of between $2.53 billion and $2.58 billion. However, this decline is being driven by some divestiture activities, including some assets that are in the process of being sold. Adjusting for these changes, revenue should be between flat and 2% higher than what the company reported for 2022. On a constant currency basis, growth is actually slated to be between 1% and 3%. The current forecast calls for earnings per share of between $1.50 and $1.70, with adjusted earnings of between $1.40 and $1.60. Both of the earnings estimates imply a $0.14 per-share impact associated with foreign currency fluctuations. But using the midpoint numbers provided by management, we should end up with earnings of $126.9 million. No guidance was given when it came to other profitability metrics. And given how volatile the company's bottom line results have been, I don't think it would be wise for us to make any assumptions on that front with what little data we have.

{kind=link}

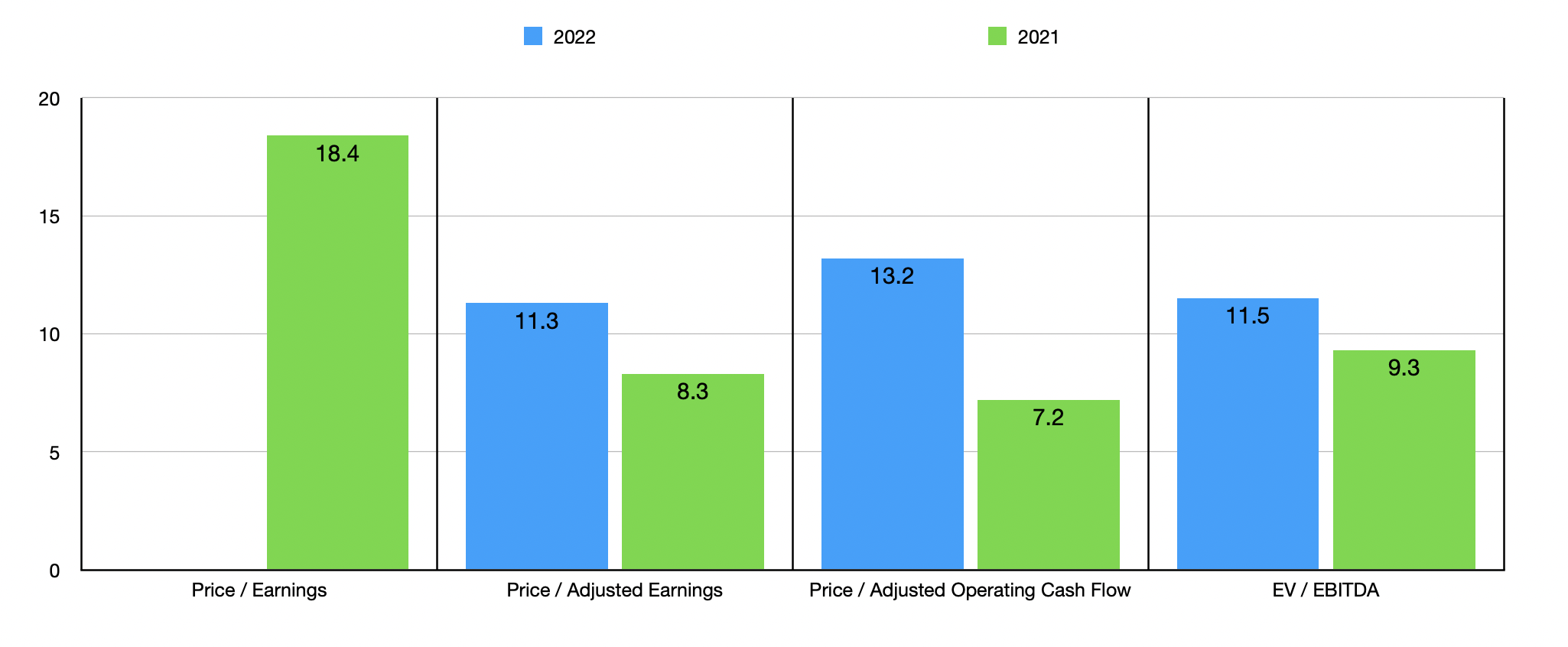

Using data from 2022, I was able to value the company. Obviously, the negative earnings make it impossible to provide a price-to-earnings multiple. But in the chart above, I did also price the company using its adjusted earnings. In this case, we end up with a multiple of 11.3 compared to the 8.3 reading that we get using data from 2021. The price to adjusted operating cash flow multiple should also increase year over year, climbing from 7.2 in 2021 to 13.2 in 2022. Meanwhile, the EV to EBITDA multiple should range from 9.3 to 11.5. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 7.6 to a high of 21.8. Using the adjusted numbers for 2022, we can see that two of the five companies were cheaper than Wolverine World Wide. Using the price to operating cash flow approach, the four companies with positive results had multiples ranging between 12.9 and 107.8. In this case, only one of the four companies was cheaper than our prospect. And finally, using the EV to EBITDA approach, the range should be from 7.3 to 13.9. In this case, four of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Wolverine World Wide |

| 11.3 |

| 13.2 |

| 11.5 |

| Steven Madden ( SHOO ) |

| 10.6 |

| 20.5 |

| 7.3 |

| Rocky Brands ( RCKY ) |

| 7.5 |

| N/A |

| 8.3 |

| Crocs ( CROX ) |

| 14.4 |

| 12.9 |

| 10.6 |

| Skechers U.S.A. ( SKX ) |

| 18.4 |

| 107.8 |

| 10.2 |

| Deckers Outdoor ( DECK ) |

| 21.8 |

| 25.6 |

| 13.9 |

Takeaway

Although I find the business model and brand portfolio of Wolverine World Wide to be interesting, I don't see much opportunity here for investors. Management did say that they intend to further fuel growth associated with their Active Group and will sustain momentum for their Work Group, while simultaneously addressing the underperforming brands that it owns. Until we see some degree of certainty though, I just can't get behind the company from an investment perspective. It would be different if shares were trading at incredibly cheap levels. While they are near the low end from a valuation perspective relative to similar firms, they aren't cheap enough on an absolute basis to warrant anything other than a ‘hold’.

For further details see:

Wolverine World Wide: There Are Still Better Fits Out There