WOOD - WOOD: China Is Somewhat Of A Problem

2023-08-13 06:33:54 ET

Summary

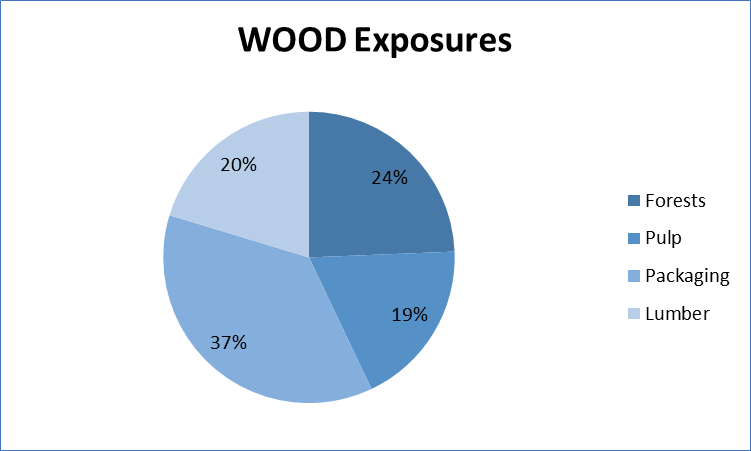

- WOOD includes commodity exposures in lumber, pulp, and cyclical exposures in packaging companies.

- Packaging companies are suffering due to pressure from faltering Chinese demand.

- Lumber, timber and pulp prices also have downside from current levels given outstanding economic risks. Current price data has shown some declines since last reports.

- With WOOD prices tracking halfway back to highs, lessened risks from further intense rate hikes have already been acknowledged by markets in our view.

The iShares Global Timber & Forestry ETF ( WOOD ) features some more commodity exposures in lumber, pulp and forests, but also packaging companies that directly and indirectly depend on these inputs for making packaging products. While commodity deflation is already happening, to some extent the negative effects are unlikely to mount much further. The bigger issue is with packaging companies whose margins should be suffering further due to the pressure in the Chinese markets. We're not buyers yet.

WOOD Breakdown

Let's begin with a breakdown of WOOD. Because there are quite a lot of relatively independent exposures in terms of commodities within WOOD, we've broken it down coarsely in this way.

{kind=link}

We posit that things are still not going in the right direction for WOOD and it's still an uncertain proposition. The first thing to mention is pulp. While pulp continued to ride high despite initial pressures on demand and the slowdown in the goods boom, there has been some pressure on pulp prices for the first time in a long time. While declines of 5% or so are not massive , they do begin to send the earnings of pulp producers in the wrong direction.

While this could be good for the packaging companies that aren't vertically integrated with their own pulp mills, it's unfortunately not good enough since packaging prices are also falling. While pulp falling is more of an inevitability considering its momentous rise, the declines in the prices for packaging end products is more concerning since it's coming from pressure, mostly from China, in industrial demand for packaging products which are declining at a faster rate than the prices for pulp . This should also be a seasonally strong moment, but packaging demand has instead been quite weak. Given the continual failure of a Chinese recovery despite major accommodation by government, there is legitimate concern that this is becoming a perennial problem.

The demand for pulp and packaging have some bearing on forest and lumber prices but not much. While lumber is specialised timber and therefore depends on lumber mills to make the supply of the market, timber also has alternative uses that go beyond just becoming fiber for the production of pulp. At any rate, these commodities are the most volatile , and lumber prices are not doing terribly well. There has been some favourable dynamics in the fact that the impact of higher rates on housing has been less than expected, with housing demand fundamentals being solid enough to resist major recession as expected. With soft landing expectations the lumber outlook will have improved, but there isn't any major reason for there to be a major uptick in lumber prices and volumes besides the onset of greater certainty around terminal cost of capital conditions.

Timber is a more difficult picture to paint because the markets are more local and more mixed. Fiber logs aren't doing well, but sawlogs are doing pretty well. Still, there is pressure on some forest businesses due to lower pulp and lumber mill realisations. Lumber as said is a little better, as well as other engineered wood products used in construction, and wildfires in Canada may help the supply situation a little for the US market. But again, timber is as upstream as you get for these industries and the value add and processing scarcity is in later stages of the value chain. There is net pressure here as well in pricing from what we see . Also timber has a perennial problem where all land has it, and it can come from non-vocational sources in meaningful volumes.

Bottom Line

There are remaining struggles in the global economy, not just the US, that can affect components of WOOD like packaging profits. Moreover, the US economy is still not out of the woods yet. While the risks of rising rates seem to be considered more balanced by the Fed, and therefore further rate hikes to hit end-markets that matter to WOOD have become more unlikely, there is still the last 1% of inflation that will need to be stubbornly stamped out. There is general downside for the economy that needs to be respected, and these cyclical and commodity exposures don't fare well in an environment with downside. WOOD has started tracking halfway back to highs from local lows, and while this makes some sense due to lessening risks and the total recovery in price hasn't happened yet, it's hard to imagine WOOD being exceptionally good value at this point in time. The demonstrated resilience of housing so far is probably reflected in current prices.

For further details see:

WOOD: China Is Somewhat Of A Problem