WWD - Woodward Blows Past Q2 Estimates But Still Isn't Worth Buying

2023-05-02 17:22:14 ET

Summary

- Woodward, Inc. continues to generate strong sales and cash flow growth, though profits did take a step back in fiscal Q2.

- Overall, the company exceeded analysts' expectations and the future looks promising.

- But Woodward, Inc. shares are still lofty and better opportunities exist out there.

May 1st turned out to be a fantastic day for shareholders of Woodward, Inc. ( WWD ). After the market closed, the management team at the company announced financial results covering the second quarter of the company's 2023 fiscal year. This earnings release revealed that the company reported revenue and adjusted profits that exceeded analysts’ expectations. Management also was able to increase guidance for the 2023 fiscal year.

Naturally, this is all great news that investors should rejoice in. But it doesn't change my view that Woodward, Inc. company is more or less fairly valued at this time. Given this stance that I have on the firm, I do believe that investors can probably find better opportunities elsewhere. As such, I have no choice but to keep it rated the "Hold" I had it rated previously.

Fantastic results

After the market closed on May 1st, the management team at Woodward announced financial results covering the second quarter of the company's 2023 fiscal year. In response to what can only be called a fantastic quarter, shares of the business skyrocketed in after-hours trading. At one point during after-hours trading, the stock was up 18.6% compared to what it closed at on May 1st.

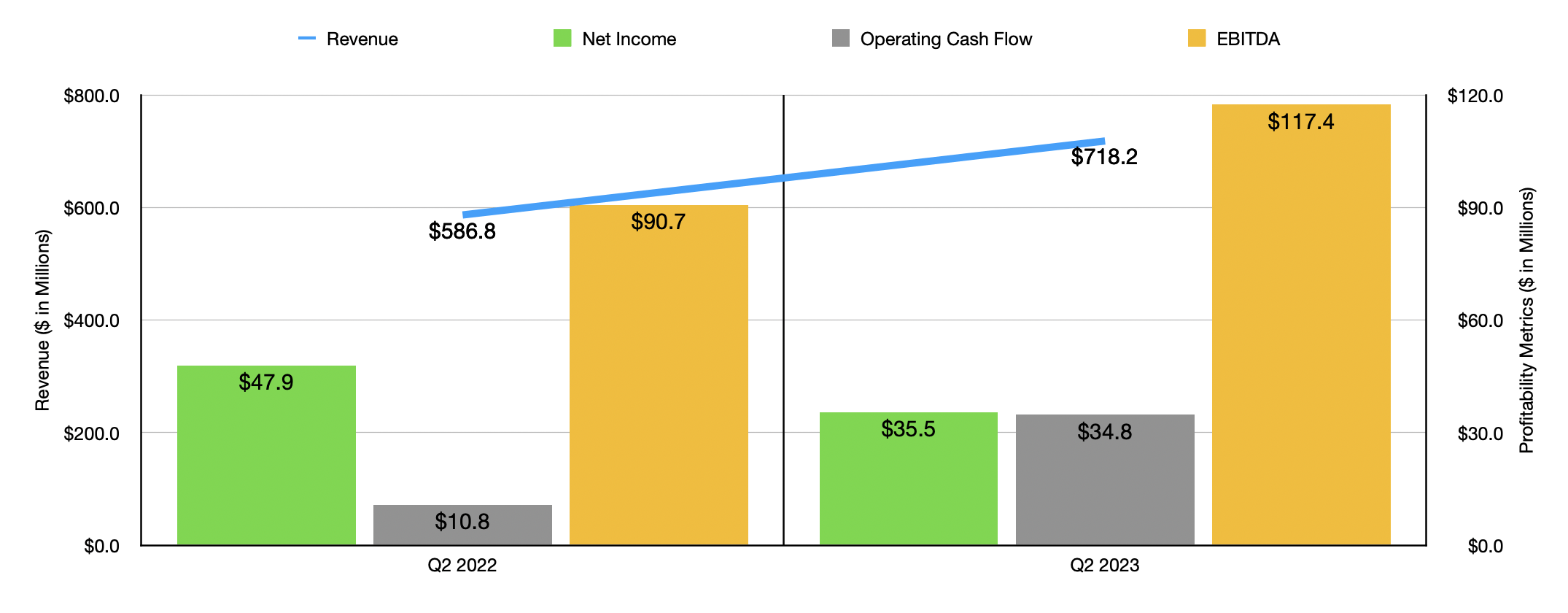

This move higher was driven by a number of factors. For starters, revenue data reported by management was particularly robust. During the quarter, management reported sales of $718.2 million. That's 22.4% higher than the $586.8 million the company reported one year earlier. It also managed to beat analysts’ expectations by $69.6 million.

{kind=link}

What's really fascinating about this is that Woodward, Inc. management indicated that financial performance would have been even greater had it not been for factors outside of the company's control. They claimed that ongoing challenges in the industry, such as supply chain problems and labor disruptions, continued to impact sales. The firm also said that foreign currency fluctuations impacted sales negatively to the tune of $14 million. Interestingly, the growth the company experienced was not where I would have anticipated. The biggest growth, by far, came from its Industrial segment. This is the part of the enterprise that produces and services systems and products for the management of fuel, air, gases, electricity, and more. Particular examples include valves, fuel injection systems, sensors, and more. Revenue for this segment spiked 31% thanks to higher volumes across all of its markets. And this was in the face of $11 million of foreign currency fluctuations that impacted the company negatively.

Truth be told, the segment that I thought would have performed the best was the Aerospace segment. Following the conclusion of the COVID-19 pandemic, the aerospace market has seen a significant resurgence. An increase in travel, combined with years of underinvestment, resulted in significant demand in this space. And yet, revenue growth here was a more modest, but still impressive, 17%. Sales would have been higher, according to management, had it not been for weak defense spending, particularly centered around guided weapons. But management did say that of passenger traffic recovery and higher aircraft utilization rates helped to propel revenue up. For context, defense spending was down about 10% year over year. By comparison, commercial OEM spending was up about 30%, while commercial aftermarket spending grew 28%.

On the bottom line, the picture was a bit more complicated. Earnings per share for Woodward, Inc. actually worsened year-over-year, falling from $0.74 to $0.58. This brought total profits down from $47.9 million to $35.5 million. On the other hand, adjusted earnings actually rose, climbing from $0.72 per share to $1.01 per share. This exceeded analysts’ expectations by $0.30 per share. The disparity between official earnings and adjusted earnings was largely driven by two factors. One of these was a specific charge for excess and obsolete inventory totaling $0.15 per share. The other was $0.13 per share associated with product rationalization. In short, these are one-time items that the company had to contend with in order to optimize its operations and write down the value of certain assets.

{kind=link}

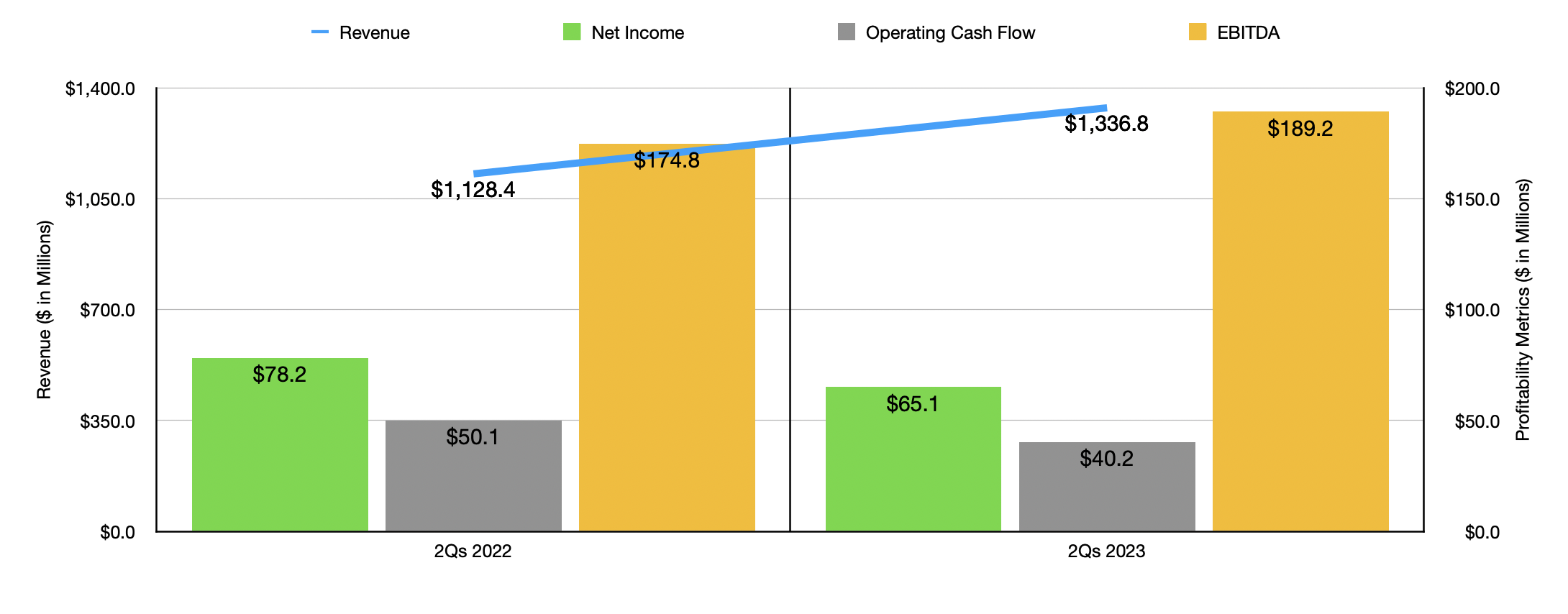

Other profitability metrics for Woodward, Inc. actually fared better. Operating cash flow, for instance, shot up from $10.8 million to $34.8 million. Generally, I like to provide an analysis that adjusts this for changes in working capital. But management has not provided these estimates and has not filed their 10-Q as of this writing, so I am unable to provide that. Meanwhile, EBITDA for the business grew from $90.7 million to $117.4 million. Though I won't dig into the numbers, opting instead to focus on other factors, I would encourage you to check out the chart above, which also looks at financial data for the company for the first half of the 2023 fiscal year relative to the same time of the 2022 fiscal year.

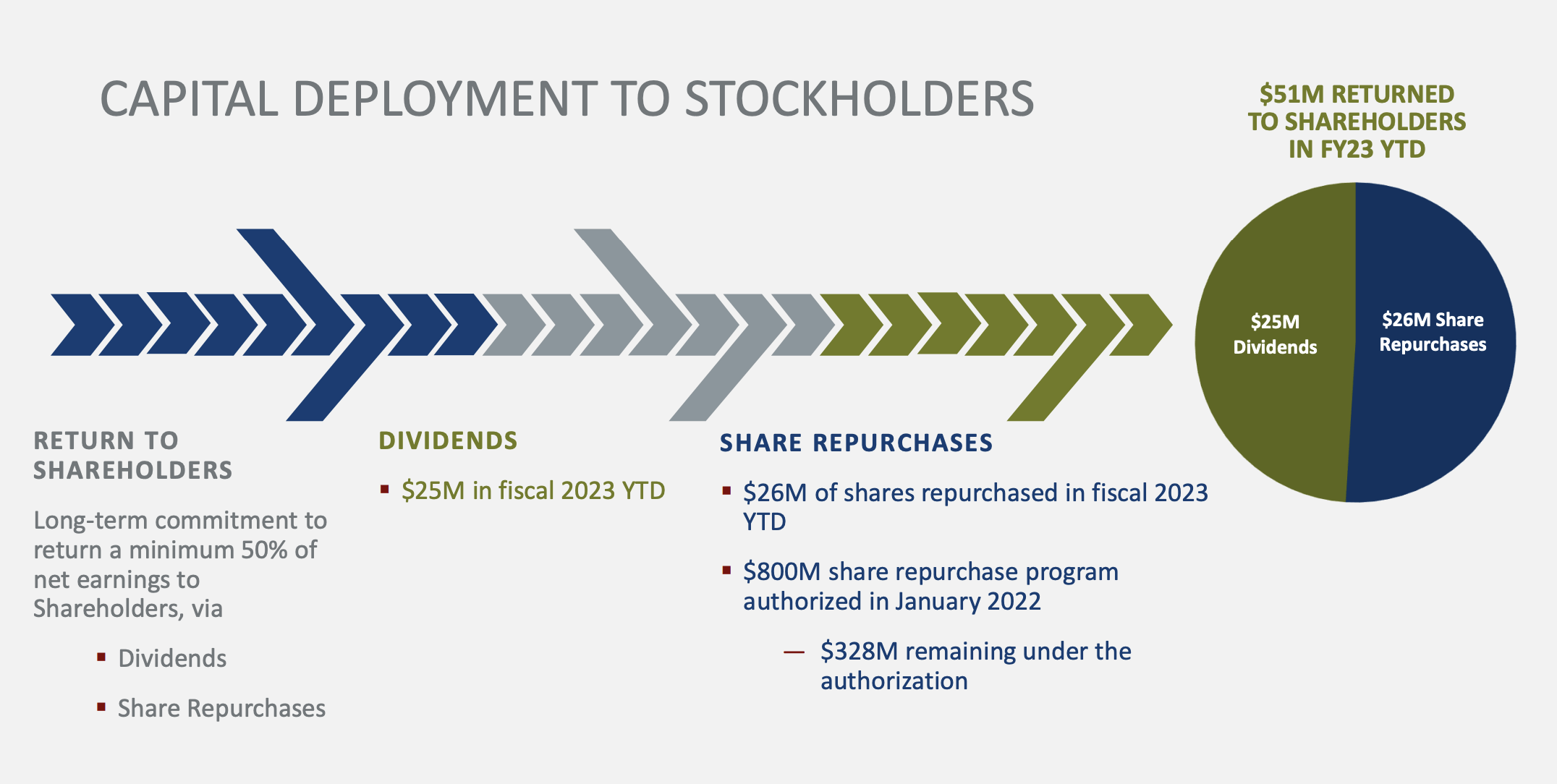

Given the results the company has experienced, Woodward, Inc. management has been confident enough to reward shareholders accordingly. For the first half of the year, management allocated $51 million toward investor rewards. $25 million of this came in the form of dividends, while the remaining 26 million was attributable to share buybacks. This leaves $328 million left in the company's $800 million share buyback program that was launched in January of 2022.

{kind=link}

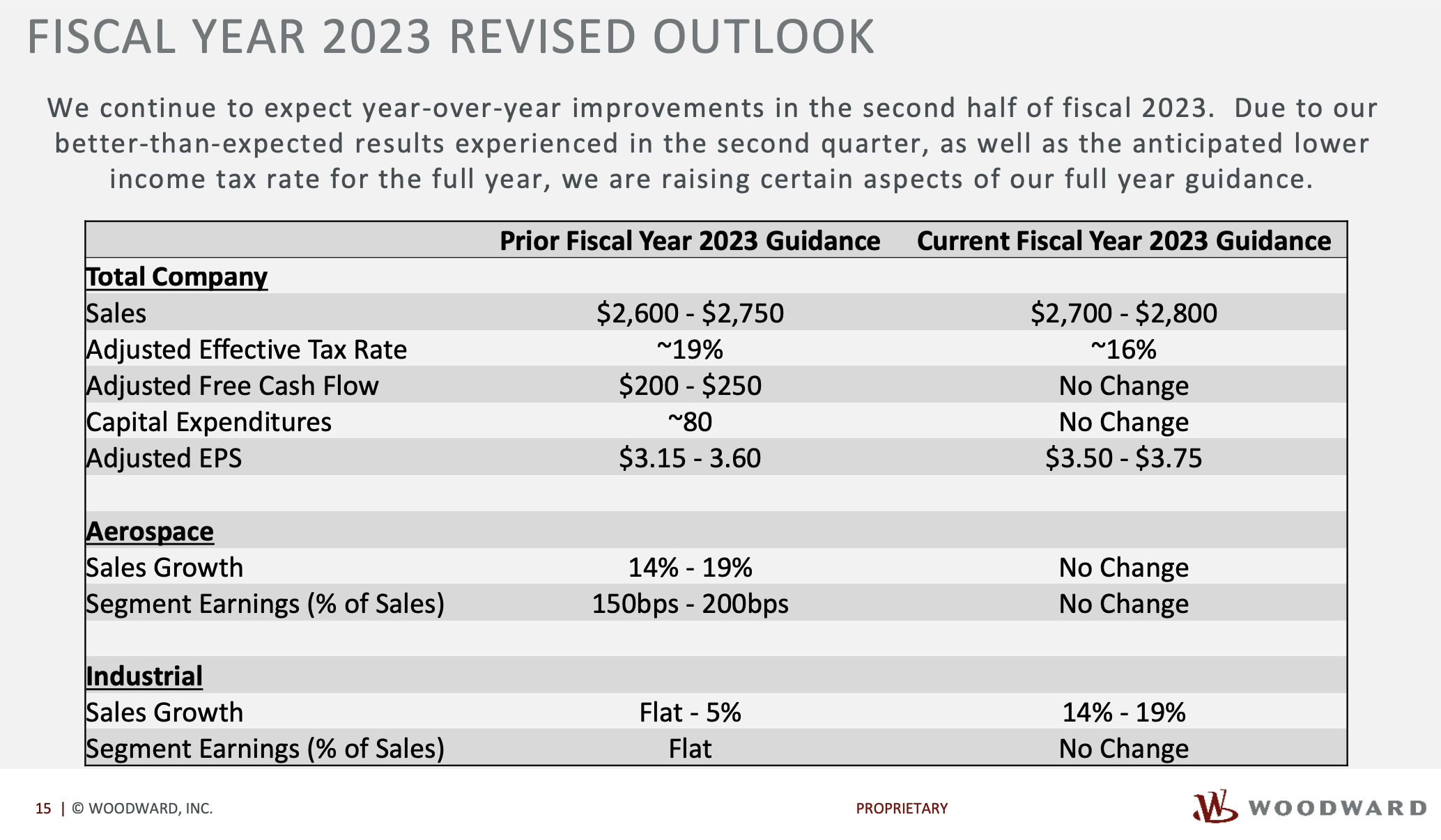

Another positive that the market seemed to appreciate was a revision and expectations that management has for the 2023 fiscal year as a whole. Previously, management forecasted revenue for this year to be between $2.60 billion and $2.75 billion. That number has now been moved up to between $2.70 billion and $2.80 billion. At the midpoint, this would imply an extra $75 million in sales for the year. It would also result in revenue that is 15.4% above the $2.38 billion the company reported for 2022. That would suggest some slowing down in the second half of the year since the first half saw revenue come in 18.5% above what it was one year ago.

{kind=link}

On the bottom line, Woodward, Inc. management believes that earnings per share will be between $3.50 and $3.75. That's up from the $3.15 to $3.60 that the company was forecasting previously. At the midpoint, that would imply an upward revision of 7.4%. Based on the company's current share count, this would translate to net profits of about $221.9 million on an adjusted basis. The other estimates of management provided indicate that adjusted operating cash flow should come in at around $305 million. If we assume that EBITDA will increase at the same rate, then it should come in for the year at around $377.9 million.

{kind=link}

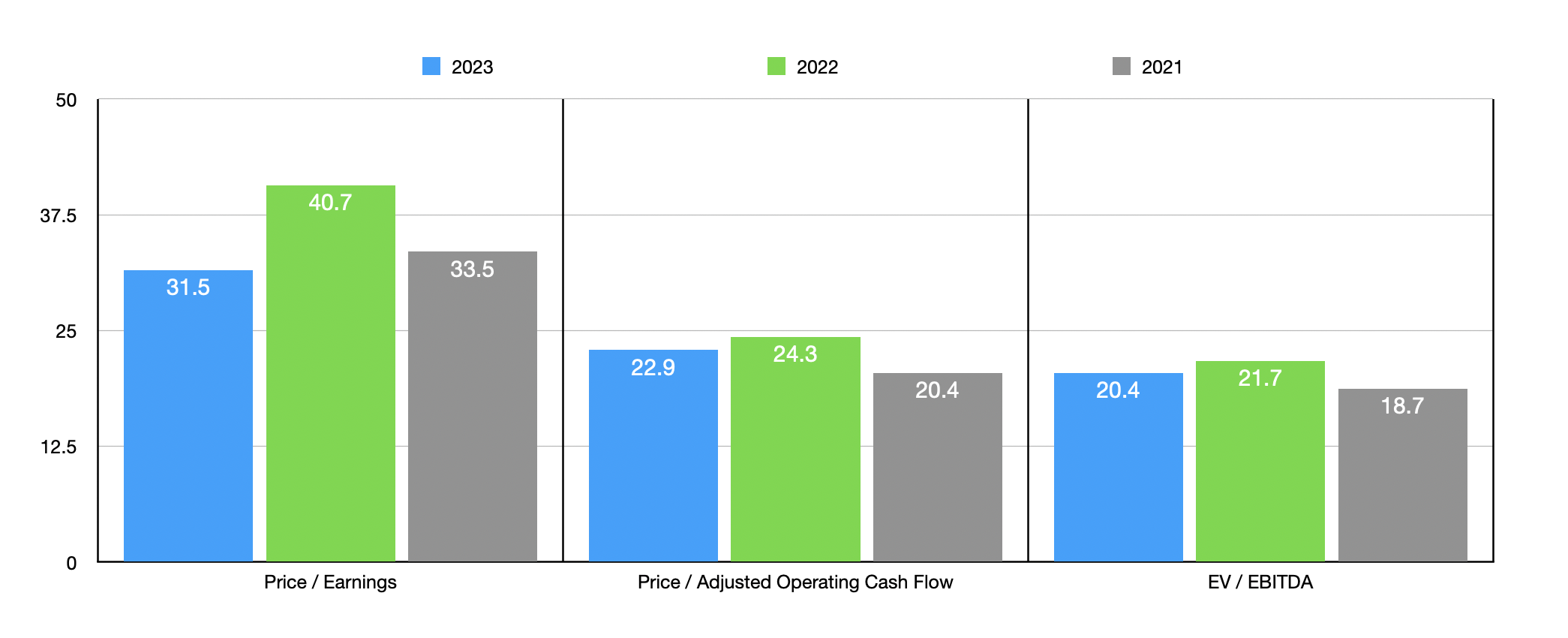

With the data that I already laid out, we can easily value the company. In the chart above, you can see how shares are priced using results from 2021 and 2022, as well as estimates for 2023. We do see that 20/22 was a bit of a difficult year for the firm compared to the others. But it is nice to see the picture improving. Unfortunately, Woodward has a history of volatile earnings. This makes relying on the price to earnings multiple a bit iffy. But in the table below, you can see that, using that method, only one of the five companies I compared the firm to was cheaper than it. On a price to operating cash flow basis, two of the five were cheaper. Meanwhile, when it comes to the EV to EBITDA approach, four of the five companies were cheaper than Woodward.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Woodward |

| 31.5 |

| 22.9 |

| 20.4 |

| BWX Technologies ( BWXT ) |

| 24.9 |

| 24.2 |

| 16.9 |

| Hexcel Corporation ( HXL ) |

| 40.7 |

| 36.3 |

| 19.6 |

| Curtiss-Wright ( CW ) |

| 22.6 |

| 22.5 |

| 13.7 |

| Parsons Corporation ( PSN ) |

| 49.7 |

| 20.9 |

| 16.4 |

| Aerojet Rocketdyne Holdings ( AJRD ) |

| 62.6 |

| 154.2 |

| 24.3 |

Takeaway

Operationally speaking, things are going quite well for Woodward, Inc. Although official earnings were down, adjusted earnings were quite strong. Cash flow data was encouraging, which marks an improvement over what the company experienced during the first quarter of the year. The spike in revenue was particularly interesting, as was the increase in guidance for the year.

But none of this changes my mind that the company makes for a "hold" rather than as a "buy." I believe that my stance has been validated by recent share price movements. Back in March of last year, for instance, I wrote my last article on Woodward. In that article, I ended up rating the company a "hold." Even if the 18.6% surge in after-hours trading is what holds, the stock would only be up 0.7% compared to when I last wrote about it. By comparison, the S&P 500 (SP500) is down a modest 0.8%.

When I rate a company a "hold," my general conclusion is that shares should perform more or less along the lines of what the broader market should. And that is exactly what has happened over more than a year for Woodward, Inc. Moving forward, I suspect this trend will continue for Woodward, Inc., stock even in spite of the stellar performance achieved by management.

For further details see:

Woodward Blows Past Q2 Estimates, But Still Isn't Worth Buying