BL - Workiva Reduces Operating Losses As Firms Gear Up For SEC ESG Rules (Upgrade)

2023-08-16 14:28:53 ET

Summary

- Workiva Inc. recently reported Q2 2023 financial results, beating revenue and EPS estimates.

- The company provides compliance and regulatory reporting software for enterprises worldwide.

- Management has made progress in reducing operating losses, and the market for regulatory compliance software is expected to grow.

- My outlook on Workiva stock is a Buy at around $98.00 per share.

A Quick Take On Workiva

Workiva Inc. ( WK ) reported its Q2 2023 financial results on August 3, 2023, beating both revenue and EPS consensus estimates.

The firm provides a compliance and regulatory reporting platform for enterprises worldwide.

I previously wrote about Workiva with a Neutral [Hold] outlook on a lower 2023 revenue growth forecast.

Management has made material progress in reducing operating losses.

I'm bullish on Workiva Inc. shares as companies seek to improve their governance stance and ESG, especially in light of the expected upcoming SEC rules on ESG reporting.

For patient investors, my outlook on WK is a Buy at around $98.00.

Workiva Overview And Market

Ames, Iowa-based Workiva Inc. was founded in 2008 to develop a regulatory and compliance platform to integrate various major human capital, finance, and customer relationship systems for enterprise customers.

The firm is headed by recently appointed Chief Executive Officer Julie Iskow, who joined the firm in 2019 as COO & President and was previously Chief Technology Officer at Medidata Solutions and Chief Information Officer at WageWorks.

The company's primary offerings include a wide range of functional reporting across all aspects of the enterprise.

Its software helps organizations to simplify complex processes, streamline data management, and analyze activity across siloed functions.

Workiva acquires customers through its in-house direct and indirect sales & marketing efforts, business development activities, and through word of mouth and partner referrals.

According to a 2021 market research report by IndustryARC, the global market for regulatory compliance management software was estimated at $27.8 billion in 2020 and is forecast to reach $56.4 billion by 2026.

This represents a forecast CAGR of 12.5% from 2021 to 2026.

The main drivers for this expected growth are growing governmental regulations and complexity, along with improved technological options for enterprises.

Also, the pie chart below shows the relative market share by geography in 2020:

Regulatory Compliance Management Software Market (IndustryARC)

Major competitive or other industry participants include:

- MasterControl.

- MetricStream.

- IBM.

- Intelex Technologies.

- SAP SE.

- BlackLine.

- Others.

Workiva's Recent Financial Trends

-

Total revenue by quarter has continued its upward trend; Operating losses by quarter have been reduced sequentially in the most recent quarter.

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has trended slightly lower more recently; Selling and G&A expenses as a percentage of total revenue by quarter have been volatile in recent quarters.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have remained heavily negative and highly volatile in recent quarters.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP).

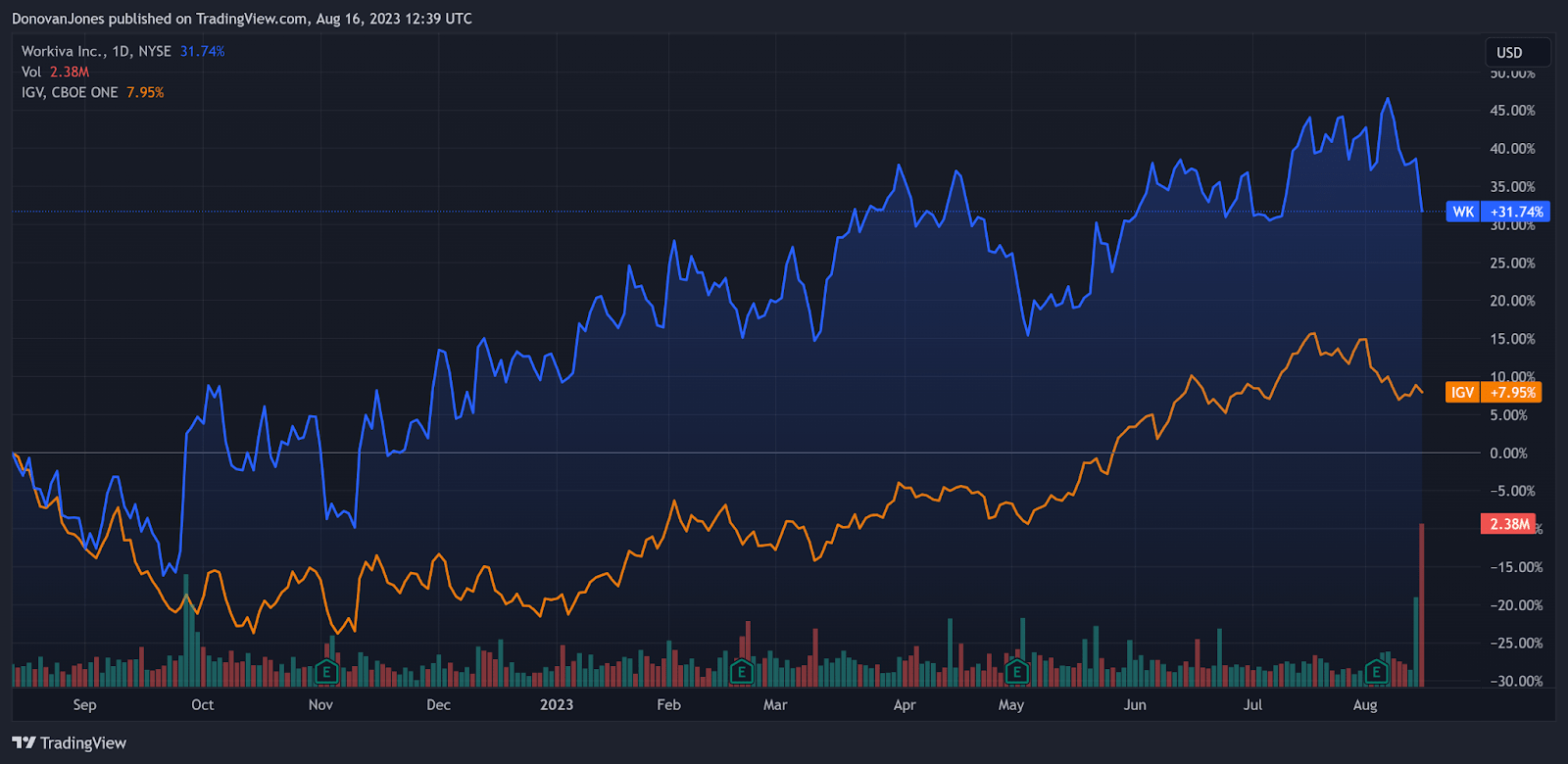

In the past 12 months, WK's stock price has risen 31.74% vs. that of the iShares Expanded Technology-Software ETF's ( IGV ) growth of 7.95%, as the chart indicates below:

52-Week Stock Price Comparison (TradingView)

{kind=link}

For the balance sheet , the firm ended the quarter with $466.3 million in cash, equivalents, and short-term investments and $340.9 million in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $32.0 million, during which capital expenditures were $3.1 million. The company paid a hefty $95.6 million in stock-based compensation in the last four quarters, the highest trailing twelve-month figure in the past eleven quarters.

Valuation And Other Metrics For Workiva

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 9.3 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 9.5 |

| Revenue Growth Rate |

| 17.6% |

| Net Income Margin |

| -19.0% |

| EBITDA % |

| -16.5% |

| Market Capitalization |

| $5,530,000,000 |

| Enterprise Value |

| $5,430,000,000 |

| Operating Cash Flow |

| $35,130,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.07 |

(Source - Seeking Alpha).

As a reference, a relevant partial public comparable would be BlackLine, Inc. (BL); shown below is a comparison of their primary valuation metrics:

| Metric [TTM] |

| BlackLine |

| Workiva |

| Variance |

| Enterprise Value / Sales |

| 6.3 |

| 9.3 |

| 49.0% |

| Enterprise Value / EBITDA |

| 965.2 |

| NM |

| --% |

| Revenue Growth Rate |

| 17.8% |

| 17.6% |

| -1.1% |

| Net Income Margin |

| 1.8% |

| -19.0% |

| --% |

| Operating Cash Flow |

| $97,350,000 |

| $35,130,000 |

| -63.9% |

(Source - Seeking Alpha).

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

WK's most recent unadjusted Rule of 40 calculation was 1.1% as of Q2 2023's results, so the firm has produced lower results in this regard than those of Q4 2022, per the table below:

| Rule of 40 Performance (Unadjusted) |

| Q4 2022 |

| Q2 2023 |

| Revenue Growth % |

| 21.3% |

| 17.6% |

| EBITDA % |

| -13.4% |

| -16.5% |

| Total |

| 7.9% |

| 1.1% |

(Source - Seeking Alpha).

Commentary On Workiva

In its last earnings call ( Source - Seeking Alpha ), covering Q2 2023's results , new CEO Julie Iskow highlighted the growth in its subscription revenue as driving the revenue results above the high end of previous guidance.

Notably, large customers (revenue > $100k) have grown by 24%.

Management believes that the increased scrutiny on companies and their executives will drive demand for its governance, risk, and compliance [GRC] software.

The company's subscription and services net revenue retention rate was 111%, including add-ons, indicating improving product/market fit and sales & marketing efficiency.

Total revenue for Q2 2023 grew by 17.9% year-over-year, and gross profit margin fell by 1.0%.

Selling, G&A expenses as a percentage of revenue dropped 5.5% year-over-year, indicating improved efficiency in sales and marketing, and operating losses were reduced by 19.5%, a meaningful improvement.

The company's financial position is reasonably solid, with more liquidity than debt and reasonably good free cash flow.

However, the firm's Rule of 40 performance has been disappointing, dropping from Q4 2022's already low results.

According to consensus estimates, full-year 2023 revenue is expected to grow at approximately 16.7%.

If achieved, this would represent a decline in revenue growth versus 2022's growth rate of 21.32% over 2021.

Analysts questioned company leadership about its recent large-customer success. Management said they are focusing on sourcing larger deals through partners, and it is seeing 'high engagement' in that regard.

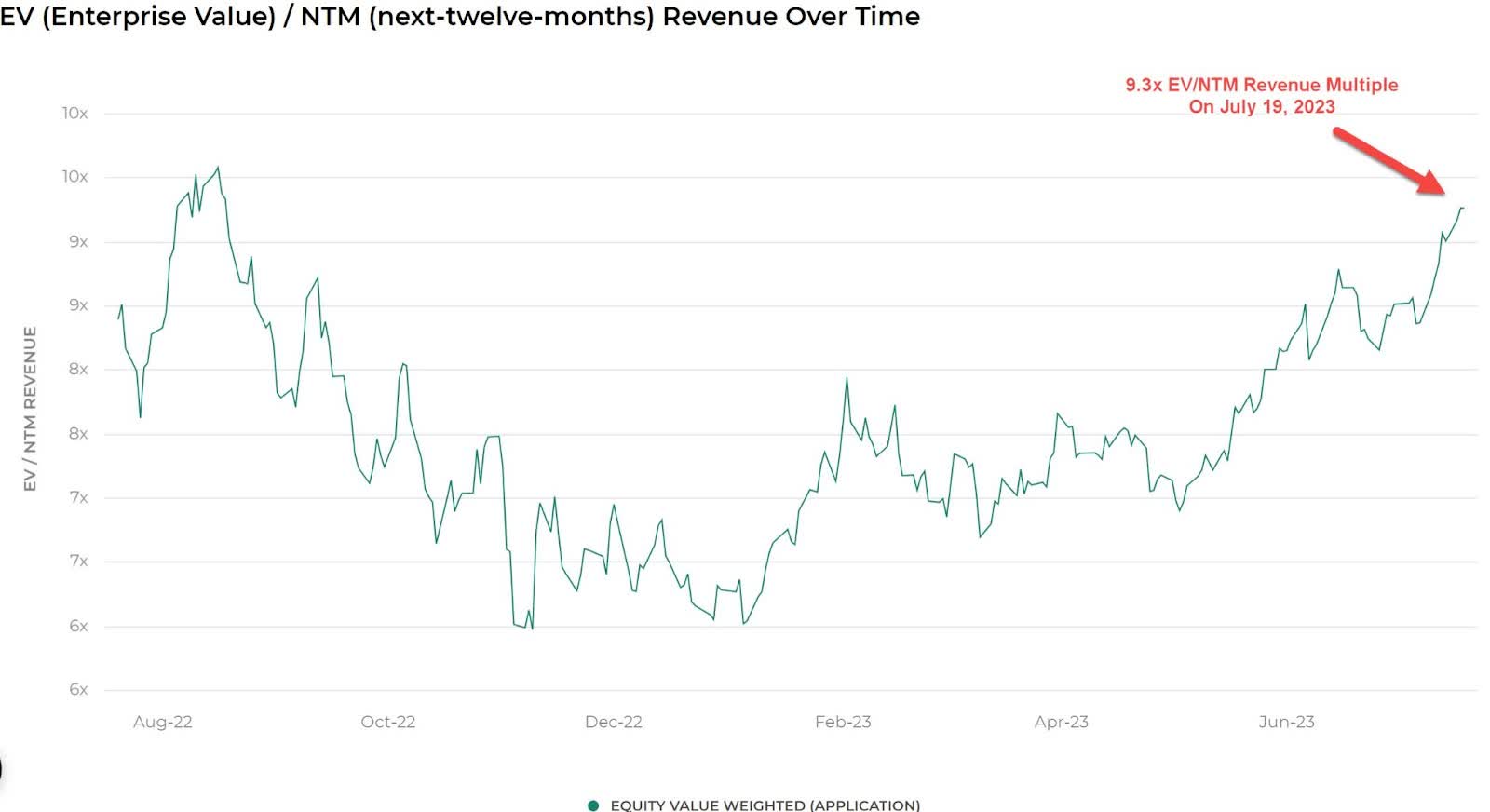

Regarding valuation, the market is valuing WK at an EV/Sales multiple of around 9.3x on a TTM revenue growth rate of forward growth estimate of 16.6% against a median Meritech SaaS Index implied ARR growth rate of 21% ( Source ).

The Meritech Capital Index of publicly held SaaS application software companies showed an average forward EV/Revenue multiple of around 9.3x on July 19, 2023, as the chart shows here:

EV/Next 12 Months Revenue Multiple Index (Meritech Capital)

{kind=link}

So, by comparison, WK is currently valued by the market equal to the broader Meritech Capital SaaS Index, at least as of July 19, 2023, despite slightly slower revenue growth.

Risks to the company's outlook include reduced credit availability which may affect customer/prospect spending plans, and management's recognition of lengthening sales cycles, which may reduce its revenue growth potential in the near term.

The market appears to be valuing WK at a multiple equal to a higher forward revenue growth rate than the median of the Meritech index.

Investors looking to be cautious may want to put the stock on a watch list for further consideration, but I'm more bullish on WK as companies seek to improve their governance stance and ESG reporting, especially in light of the expected SEC rules on ESG reporting.

For patient investors, my outlook on Workiva Inc. is a Buy at around $98.00 per share.

For further details see:

Workiva Reduces Operating Losses As Firms Gear Up For SEC ESG Rules (Upgrade)