WKSP - Worksport: Long-Term Potential But Price Correction Imminent

2023-07-17 02:06:08 ET

Summary

- Worksport, a manufacturer of truck tonneau covers, saw a 12% increase in share price after receiving four new orders, bringing its year-to-date price gains to 206%.

- Its innovative products, including a solar charging truck bed cover with connected battery power storage, can result in long-term sales gains and are potentially driving investor optimism too.

- This potential overrides the recent drop in revenues but has increased its market valuations above comfortable levels. It's due for a price correction, though long-term investors may well see gains over time anyway.

On Thursday, July 13, the manufacturer of truck tonneau covers, Worksport ( WKSP ) saw a 12% increase in share price after it said it has received four new orders. This brings its year-to-date [YTD] share price gains up by a massive 206%.

{kind=link}

Price Chart (Source: Seeking Alpha)

The sales restructuring and innovative new products it is currently developing certainly go in Worksport’s favour, possibly driving investor optimism. The latest orders further confirm that progress is underway. But is it enough to justify the extent of the share price rise? Or is a correction in store? We will know once the company’s story is unpacked, which is exactly what I do here.

The Company

Earlier known as Franchise Holdings International, the West Seneca, New York, based company changed its name to Worksport Ltd. in 2020. Besides manufacturing soft and hardcovers for the back of pickup trucks, available for pre-order now is its innovative solar charging truck bed cover.

Called SOLIS, this solar cover can power up the company's COR portable energy storage system. In other words, Worksport is making solar-powered vehicles a reality. The tonneau cover soaks up solar power and stores it in the battery pack. This energy is accessible through an inverter, which in turn extends the vehicle’s range.

As the company’s CEO, Steven Rossi put it “You’ve got access to green power without a plug.”. Speaking of its impact, he says “It’s said that the average American drives 30 miles a day, and we can handle all of that from our sun power products.”. The prospects for the product are positive already, with Hyundai’s electric pickup truck expected to come equipped with it.

The market

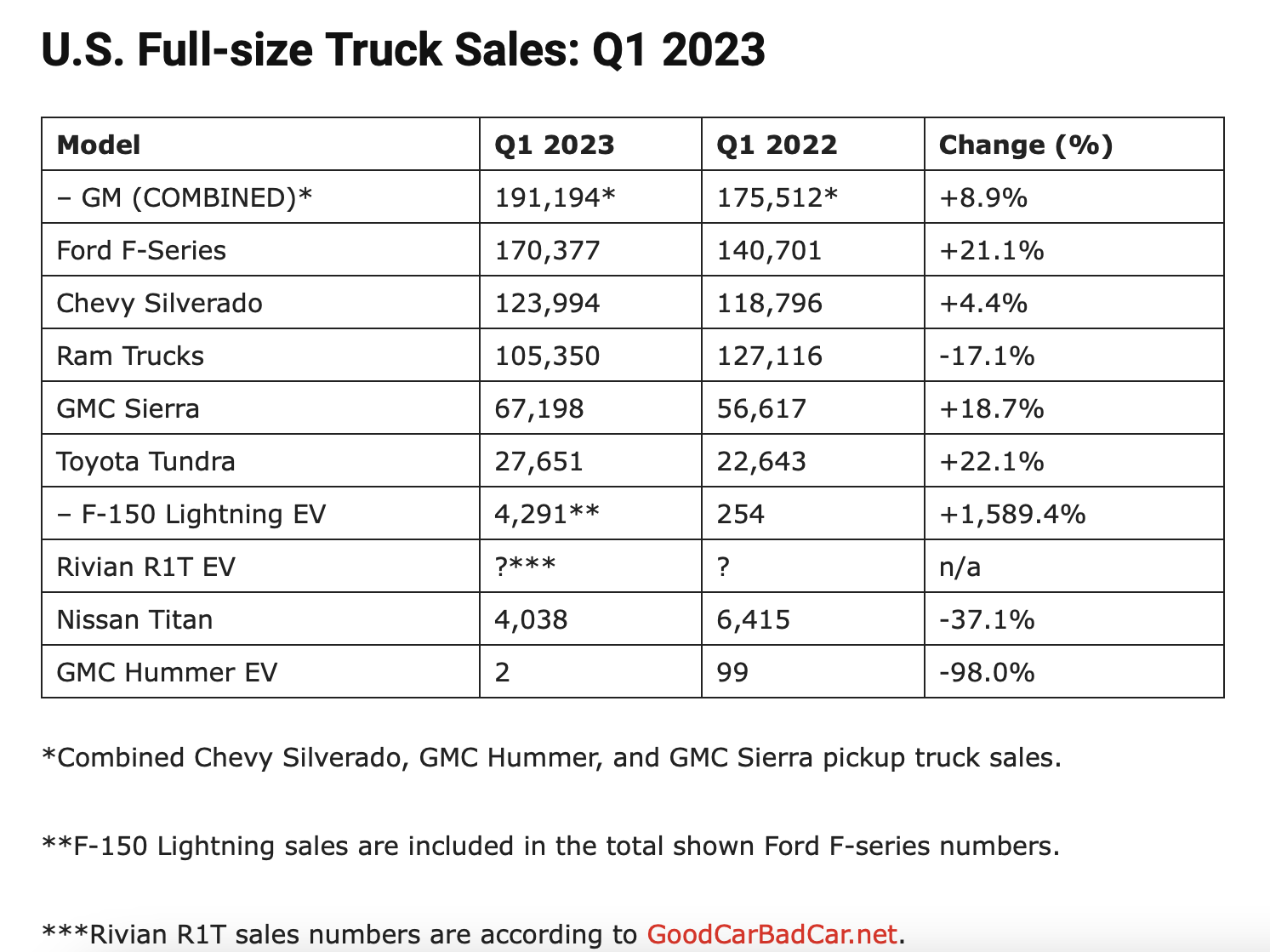

While the innovations sound both promising and groundbreaking, the reality is that so far, the company’s growth is directly linked to sales of pickup trucks. This is good news, considering that sales of full-size pickup trucks have picked up nicely in the first quarter of 2023 (Q1 2023), as evident in numbers from key manufacturers like GM and Ford (see table below).

{kind=link}

Source: TFLTRUCK

However, the company isn’t terribly optimistic about trucks' sales growth. It has pointed to factors like supply chain shortages, high-interest rates and high inflation as holding it back. Further, it says that it may take up to 2025 for new vehicle sales to return to pre-pandemic levels. Between 2023 and 2027, the market is expected to see a compounded annual growth rate [CAGR] of 1.7% in the US.

That said, there is high potential for its SOLIS and COR products as electric pickup trucks have seen strong growth of 29.7% between 2022 and 2023. They are also expected to see gains in market share up to 2035. With electric trucks being popular in areas even with less developed charging infrastructure, Worksport's new products can be particularly well placed for them.

In any case, it sounds more upbeat about the portable power station market, saying it is “much younger and globalised”. It is expected to grow by 3.9% between 2022 and 2031. The North American market, where the company already operates, is expected to have the biggest market share.

Revenue upturn expected

Financially, though, the company’s in a funk. It reported annual revenues in 2022 of a little over USD 116 thousand , a drop of 62% from 2021. The decline continued in Q1 2023, by a lesser 33% , though. The company attributes it to restructuring its sales channels. Better sales representation across the US, its own e-commerce platform and listing its products on leading e-commerce marketplaces are some of the changes underway.

That sales decline is expected to turn around in 2023 though, after it won four orders worth USD 720,000 yesterday. Worksport doesn’t say when it needs to deliver on them, but even if it delivers just one of the four equally sized orders this year, that is additional revenue of USD 180,000 in the second half of the year. This is already a big jump from 2022’s figure.

The one analyst whose revenue projections are available, is certainly bullish, expecting revenues to jump to USD 1.7 million this year. The positive momentum is expected to have started in Q2 2023 itself, which is slated to grow through the remainder of the year and beyond.

Strong gross margin

Despite the recent drop in revenues, the company’s gross margin is noteworthy. For the full year 2022, it was at 51.1%, a massive rise from the 13.6% seen in 2020 (the company was loss-making at the gross level in 2021). The margin declined in Q1 2023 to 38.1%, but it still stays strong from a historical perspective (see chart below), as the cost of sales declined proportionately more than revenues.

Source: Seeking Alpha

Cost of sales in turn declined because of “increased efficiency associated with improved supply chain logistics”, says the company. However, with the consistent increase in its operating expenses last year, it remains to be seen if it can clock an operating profit anytime soon. Projections for the company also indicate that it is unlikely to make net profits in the next years.

What next?

There’s no doubt that Worksport has high potential. But there is also risk involved if its new products and sales changes don’t quite work out the way they are expected. In the meantime its forward price-to-sales (P/S) ratio has risen to a massive 26.8x , indicating that a steep price correction is likely in the near future.

I believe, however, that the real reason for the stock’s rally is on account of long-term potential. EV trucks are a fast-growing market segment and Worksport’s innovations can facilitate their functioning. The company’s more predictable truck tonneau cover market is also expected to continue growing, albeit at a much slower pace.

If I had already bought the stock, I think there could be a case for long-term stock growth, so I'd continue to hold it, even if there's a price correction in the near term. And if I was waiting to buy it, I’d do so at a price correction. Anyway, I look at it, it’s a Hold.

For further details see:

Worksport: Long-Term Potential, But Price Correction Imminent