WRDLY - Worldline: An Uppercut After Q3 Results

2023-10-26 04:15:00 ET

Summary

- Worldline's share price fell more than 50% after the company cut its full-year guidance due to a slowdown in its most important market, Germany.

- The company's new guidance suggests a stable operating margin and a decrease in revenue growth, resulting in lower margins.

- The market's reaction to the guidance cut is overblown, as Worldline's business model is not collapsing, and it's still profitable.

Introduction

While the market already was signaling it wasn't expecting a strong performance from payment provider Worldline (WWLNF) (WRDLY), the company's share price fell by more than 50% on Wednesday after the company had to cut its full-year guidance. I think this decrease is overblown although it's clear my targets for 2024 and 2025 are now completely unrealistic.

{kind=link}

Worldline has its primary listing in Paris, where it's trading with WLN as its ticker symbol . The average daily volume in Paris is approximately 60,000 shares (this will increase as the trading volume on Wednesday will likely be 20-25 times the average volume) The current market cap of the company is approximately 2.75B EUR as the share price has now lost almost 70% in the past few months.

Yes, there's still growth, but the guidance looks substantially weaker

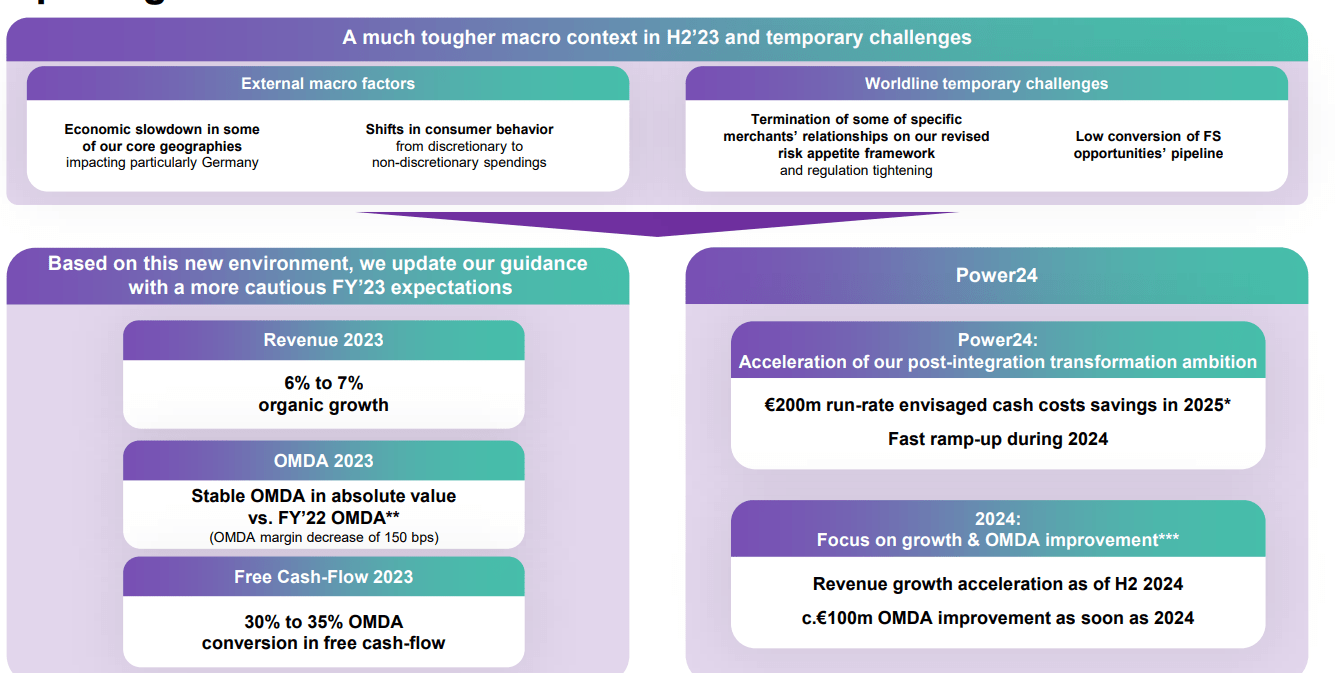

Let's focus on the main elements. Due to a slowdown in Germany (Worldline's most important market), the company's full-year guidance has come under pressure. Revenue will still increase but at a slower pace, but the operating margin will decrease. As you can see below, Worldline is guiding for a " stable OMDA" on an increasing revenue .

{kind=link}

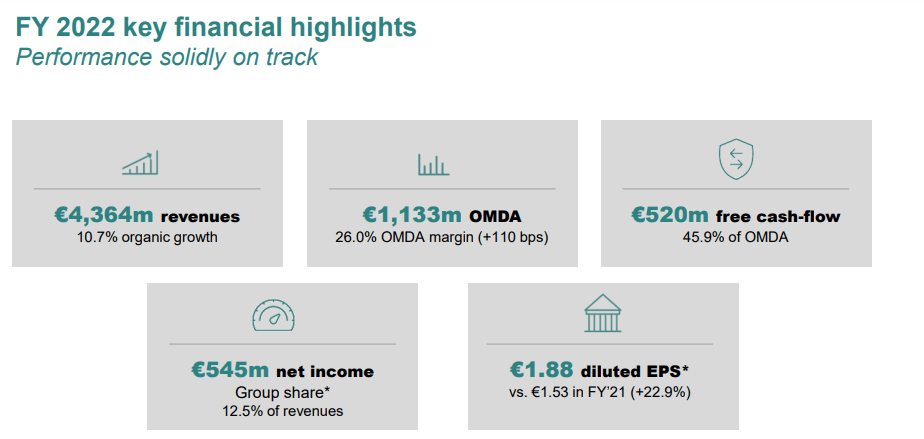

Let's re-read the new guidance. Basically Worldline says this year's OMDA will come in line with last year's OMDA (which is comparable to the normalized EBITDA). So Worldline is not guiding for a 25% or 50% lower OMDA, but for a stable OMDA. Let's now pull up the 2022 results . As you can see below, the total OMDA was 1.13B EUR at a 26% OMDA margin. Applying a 6% revenue increase to the 4.36B EUR revenue would result in a 4.6B EUR revenue and an OMDA margin of 24.5% would indeed result in an OMDA of 1.13B EUR.

{kind=link}

So let's use the OMDA of 1.13B EUR as a base case scenario. Last year, the free cash flow conversion was 45.9% of the OMDA, resulting in a free cash flow result of 520M EUR. However, as the image below shows, the "reported free cash flow result" included a 100M EUR contribution from working capital changes.

Worldline Investor Relations

If you would calculate the free cash flow conversion rate excluding the working capital contribution, you would end up with 420M EUR on a 1.13B EUR OMDA for a conversion rate of 37%.

While the updated guidance for this year - which now assumes a conversion of 30-35% of the OMDA into free cash flow is indeed worse than that, it's a pity Worldline has not provided additional color on the impact of working capital changes on that updated guidance. Because if there would be a 50M EUR working capital investment this year, the conversion rate will immediately suffer as well. As we established a 37% conversion rate in 2022 excluding the impact of working capital changes, a moderate working capital investment of 50M EUR would have reduced the conversion rate to 32.5% which is exactly the midpoint of the updated guidance for this year. That being said, if the guidance of 30%-35% includes a positive contribution from working capital changes, I would be very disappointed.

Don't get me wrong, I'm not sugarcoating anything here. The lower guidance is most definitely disappointing and the targets for 2024 and 2025 are now completely unachievable. But the market is reacting as if Worldline is in serious trouble while it isn't.

{kind=link}

Assuming a 32.5% conversion rate of the OMDA to free cash flow , the free cash flow will be 370M EUR for a free cash flow result of 1.27 EUR per share. Does that justify a share price of 30 EUR? Not really. But it most definitely also doesn't justify a share price below 10 EUR. Because the reported free cash flow still includes the integration and transaction costs (which should decrease in the near future) and the underlying free cash flow is likely even 100-150M EUR higher for an additional 0.30-0.50 EUR per share.

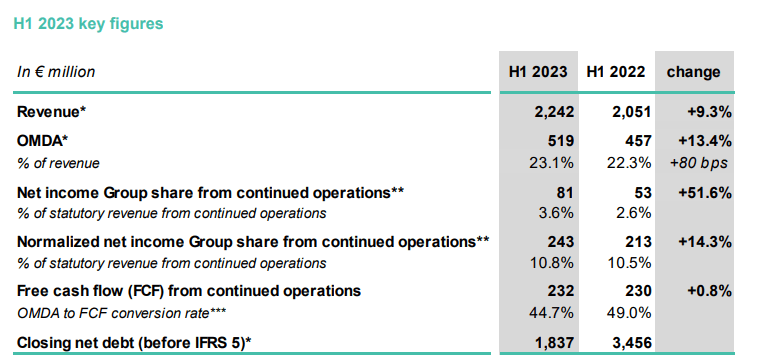

Interestingly, the updated guidance does not imply a lower OMDA result in the second semester. As you can see below, and as explained in the previous article, the OMDA in the first semester was approximately 519M EUR . The "stable OMDA" guidance of 1.13B EUR implies a H2 OMDA of 600M EUR. While that's lower than the H2 2022 OMDA, it's not like the OMDA is completely cratering.

{kind=link}

The image above also shows the net debt position of Worldline. This is very reasonable as it represents a multiple of just 1.7 times the OMDA. That's very reasonable, and as Worldline currently does not pay a dividend, the incoming free cash flow will further reduce the net debt.

I also think the financing risk is low. The company recently issued 600M EUR in five-year bonds with a fixed coupon of 4.125%. The next bond to mature is the September 2024 bond with a 0.25% coupon so the interest expenses will for sure increase from 2025 on, but those increases should be manageable as even the 2028 bond is trading with a yield to maturity of less than 5%. Clearly the bond market isn't worried about Worldline. And nor should it, as Worldline will still be profitable while posting a positive free cash flow.

Investment thesis

I'm not looking for excuses. The Q3 results were relatively weak and the guidance cut is a blow. There's no denying that and my expectations for a free cash flow result of 3 EUR per share in the next few years are no longer feasible. But the market appears to be pricing Worldline as if its business model is completely collapsing, which it isn't. The OMDA will remain stable this year and Worldline is working on a 200M EUR cost cutting plan and hopes to realize the majority of the benefit in 2024. Meanwhile the transaction and integration costs from previous acquisitions should continue to trend down which will further increase the free cash flow - but obviously not at the same pace as I originally anticipated.

I have added to my position in Worldline today. The company is currently trading at just 4 times the OMDA (its peers like Adyen and Nexi are still trading at a double digit EBITDA multiple) and that's just way too cheap for the European leader. Yes, competition is increasing, and yes, margins are under pressure. But the 60% share price drop this year appears to be a massive overreaction.

For further details see:

Worldline: An Uppercut After Q3 Results