WRDLY - Worldline: On Track For 3 EUR Per Share In Free Cash Flow Next Year

2023-03-29 14:43:51 ET

Summary

- Worldline is a payment and transactional services provider based in France.

- The company is still digesting the large Ingenico acquisition and some smaller acquisitions. The total integration & restructuring expenses exceeded 150M EUR in 2022.

- We should see a high single-digit revenue increase in 2023 and in 2024.

- Meanwhile, the EBITDA margin will increase, too, while the FCF conversion rate will be boosted as well.

- Depending on the changes in the working capital position, Worldline still has a shot at generating 3 EUR/share in FCF in 2024 but could be delayed until 2025.

Introduction

Worldline's ( WRDLY ) ( WWLNF ) share price has been very volatile in the past few years as the company was initially cheap, became pretty expensive in 2021 and is now trading at an attractive valuation again . I initially got interested in Worldline after the announcement it was acquiring Ingenico , a payment specialist I owned, and I kept tabs on Worldline. Unfortunately the share price has been trading pretty flat for the past five quarters despite generating increasing free cash flows which allowed Worldline to strengthen its balance sheet. In January 2022, the mid-term guidance called for a free cash flow result of 3 EUR per share in 2024 so I wanted to check up on this promise to see if Worldline will be able to meet its own target.

{kind=link}

Worldline has its primary listing in Paris where it's trading with WLN as its ticker symbol . The average daily volume in Paris is approximately 650,000 shares for a monetary value of north of 20M EUR. The current market cap of the company is approximately 10.5B EUR as there are just over 281 shares outstanding. I will use the Euro as base currency throughout this article.

Cash flow is king, and 2022 wasn't any different

In this article, I will mainly focus on Worldline's financial results and its guidance for 2023 and 2024. For a better understanding of the company's business model and history, I'd like to refer you to my older articles on Worldline .

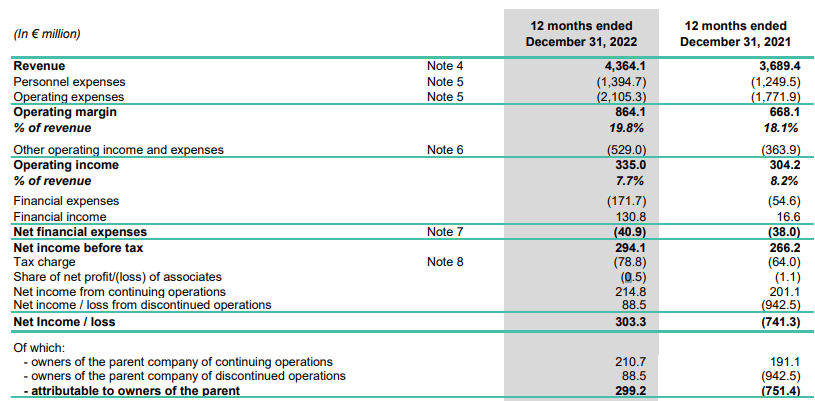

The total revenue in 2022 came in at 4.36B EUR , which resulted in an operating margin of 864M EUR and an operating income of 335M EUR. The net financial expenses came in at 41M EUR which resulted in a pre-tax income of 294M EUR. The total net income was 303M EUR including almost 89M EUR from discontinued operations. Of the 303.3M EUR in net income, approximately 299.2M EUR is attributable to the shareholders of Worldline.

{kind=link}

As the company had an average weighted share count of just over 281 million shares the total EPS came in at 1.06 EUR per share, of which approximately 0.75 EUR came from the continuing operations.

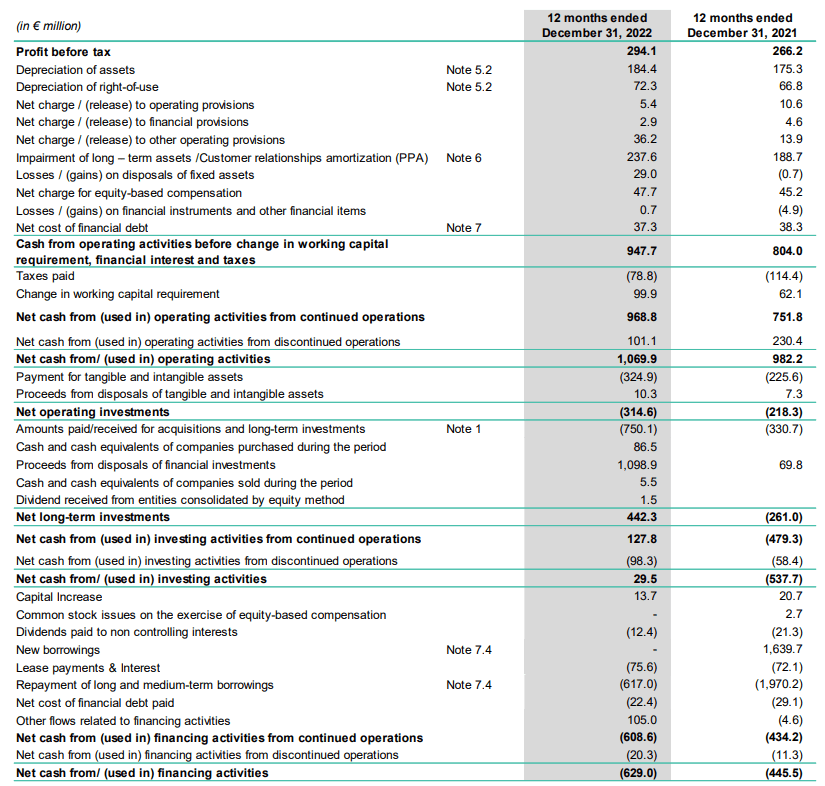

The free cash flow result in 2022 was pretty good as well as the company had recorded an impairment of the long-term assets and an accelerated amortization expense related to its customer relationships. As you can see below, the total operating cash flow was 1.07B EUR of which 101M EUR was generated from the discontinued operations. This also includes a 100M EUR investment in the working capital investment. On an adjusted basis (excluding the working capital changes and the discontinued operations) the operating cash flow was 870M EUR.

{kind=link}

We also should deduct the 76M EUR in lease payments and interest and the 22M EUR in net costs associated with the financial debt. These elements further reduce the operating cash flow by 98M EUR to 772M EUR.

We also see the total capex was 325M EUR which means the underlying free cash flow result was approximately 447M EUR or 1.59 EUR per share. Worldline's number of 520M EUR in free cash flow includes the contribution from working capital changes and that's an element I have filtered out in my calculation as you cannot consistently release 100M EUR per year in working capital elements.

{kind=link}

Interestingly, the free cash flow result provided by Worldline (I will use the official numbers for the time being as that will help to establish the 2023 and 2024 targets in the next part of this article) shows it still contains about 155M EUR in transaction and integration expenses. So once those are filtered out and the Ingenico transaction is fully included, the net free cash flow result will increase by more than 100M EUR on an after-tax basis (assuming the majority of the 155M EUR in transaction and integration expenses were tax deductible in 2022).

So based on the 2022 results, you probably wouldn't buy Worldline. I didn't buy the stock either.

A look at the implications of the mid-term guidance

But instead of having a backward looking view, we should have a look at how the company expects to perform in 2023 and 2024.

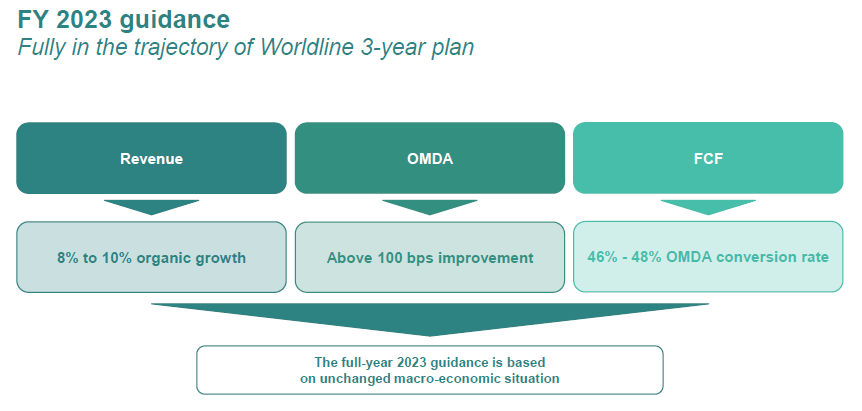

In 2023, Worldline expects to generate an organic revenue growth of 8%-10% and an OMDA margin improvement (Operating Margin before Depreciation and Amortization, so basically the EBITDA) of 100 basis points. The 2022 margin was 26% so this will increase to 27%. Applying that OMDA margin to the anticipated revenue increase of 8% (the lower end of the spectrum) to 4.71B EUR, the OMDA will increase from 1.13B EUR in 2022 to 1.27B EUR in 2023. At the same time, Worldline expects a free cash flow conversion rate of 46% to 48%. Using the lower end of that range again, the free cash flow result would increase to 585M EUR. That's 2.08 EUR per share.

In 2024, the revenue should increase again (Worldline is pursuing a 9%-11% CAGR revenue increase in the 2022-2024 period). Again using the lower end of that range, the implied revenue in 2024 would be 5.1B EUR while the OMDA margin should increase again towards 30%. That implies an OMDA of 1.53B EUR.

{kind=link}

As the free cash flow conversion rate should also increase to 50%, Worldline's 2024 guidance implies a free cash flow result of 765M EUR or 2.72 EUR per share.

That's using the lower end of Worldline's guidance. If I would use the upper end of the revenue guidance, the free cash flow result would come in at 800M EUR or in excess of 2.8 EUR per share. Keep in mind this calculation still includes the working capital changes and the restructuring and integration expenses incurred by Worldline. This means the adjusted free cash flow result (excluding working capital changes) will likely be somewhat different from the calculation above, but there shouldn't be a material difference.

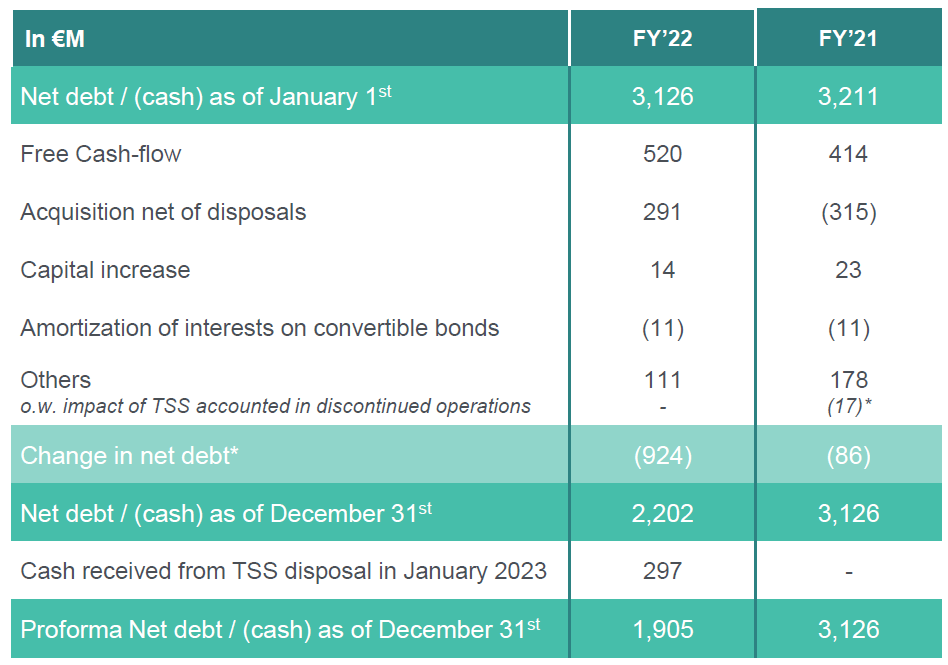

As of the end of 2022, Worldline's net debt had decreased to 2.2B EUR which subsequently dropped to 1.9B EUR upon receiving the cash proceeds from the sale of the discontinued operations I was referring to earlier. This currently represents a leverage ratio of 1.7 times EBITDA, so the balance sheet is pretty healthy.

{kind=link}

Assuming the OMDA target of 1.27B EUR will be met this year, the leverage ratio will decrease to 1.5 and this excludes the impact of debt reduction. Worldline currently does not pay a dividend so the anticipated 585M EUR in free cash flow should be integrally added to the balance sheet (subject to additional M&A activity beyond the Italian acquisition this year, of course). This should reduce the net debt to just over 1.3B EUR and reduce the leverage ratio to just 1.

Investment thesis

Based on the updated guidance for 2024, it looks like Worldline will miss my expectation to generate a free cash flow result of 3.00 EUR per share by a few percent. But considering the guidance includes integration expenses and working capital changes, the adjusted free cash flow may still come in around that 3 EUR mark so it's a bit too early to draw conclusions so I would argue the company remains "on track" to meet my expectations.

But even if Worldline would miss the expectations and the FCFPS would come in at 2.85 EUR, the stock would still be pretty cheap at a free cash flow yield of 7.7% based on today's share price. Meanwhile, the net debt should decrease to 650-700M EUR by the end of 2024 (again based on the guidance) which implies a total enterprise value of 11.3B EUR which implies an EBITDA (or OMDA) multiple of just around 7.3. That's also pretty cheap for the robust revenue generator Worldline is.

I currently have no position in Worldline but just like last year I'm considering writing some out of the money put options. Around the 30 EUR level, for instance, the anticipated free cash flow yield will increase to almost 10% while the stock would then imply an EV/EBITDA ratio of 6 in 2024.

For further details see:

Worldline: On Track For 3 EUR Per Share In Free Cash Flow Next Year