WPP - WPP Group: Recent Performance Reflects Slower Growth And Challenges Ahead

2023-09-21 11:00:16 ET

Summary

- WPP Group's financial performance has been weak, with lower revenue and margins over the past five years.

- The company's 2Q results were dismal due to a decrease in spending from their most important customer segment, tech companies in the US.

- Management has lowered their guidance for FY23, signaling a lack of confidence in the business and adding to the already weak revenue guidance.

Investment action

Based on my current outlook (initiation) and analysis of WPP Group ( WPP ), I recommend a hold rating. WPP's financial performance has not been stellar over the past five years, with revenue and margins both lower than 2018 results. Due to a decrease in spending from their most important customer segment, tech companies in the US, the company also had a dismal 2Q. In addition, this issue has worsened in the 2Q. Management signaled their lack of confidence and the weakness of WPP's business by lowering their guidance for FY23 on the heels of the poor 2Q result. With the slow progress of office space consolidation, the anticipated savings benefits are not expected to materialize until 2025, adding to the already weak revenue guidance.

Basic information

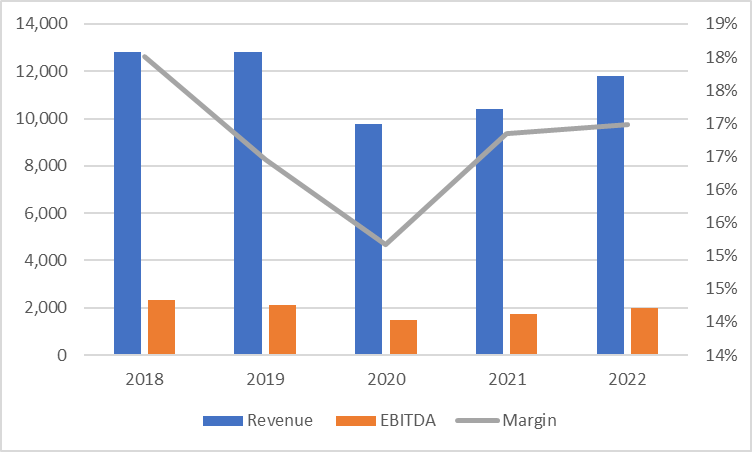

WPP plc is a creative transformation company that provides services in the areas of communications, experience, commerce, and technology. The business is split up into global integrated agencies, PR agencies, and specialist agencies. It provides media planning and buying services in addition to advertising, marketing, brand strategies, and campaigns in all forms of media. It also supplies content services, data and technology, and investment in the media. Public relations and specialized agency services are also provided by the business. WPP is headquartered in London. WPP's financial performance over the past five years has been subpar. Its revenue CAGR is negative 1.7%. Its revenue in 2022 was £11.8 billion, down from £12.8 billion in 2018. In 2022, the EBITDA margin is 17%, down from 18% in 2018. Earnings per share are also disappointing. As of 2022, it had decreased to £98.5 from £108 in 2018.

WPP's financial performance over the past five years has been less than impressive. Its revenue CAGR has been negative, declining at a rate of 1.7%. In 2022, its revenue stood at £11.79 billion, down from £12.82 billion in 2018. The year 2020 saw a significant 23% drop in revenue, mainly due to the effects of the Covid-19 lockdown, which prompted many companies to reduce their advertising budgets. Following this, revenue exhibited a feeble recovery as persistent and high inflation led to companies scaling back their marketing expenditures.

Despite the challenges WPP faces in terms of revenue growth, its EBITDA margin remains robust, consistently hovering around the 17% mark. This demonstrates WPP's effective management of costs, even in the face of soaring inflation and the devastating impact of Covid-19.

{kind=link}

Review

The lackluster performance of WPP in Q2 is certainly encouraging where 2Q like-for-like growth slowed to 1.3%. The company's operating margin for the quarter was 11.5%, with net revenue of £2.98 billion. Client spending cuts and project delays in the technology industry in the US were to blame for the slowdown. Given that 18% of WPP's revenue comes from technology companies, the hit on WPP is significant. Customers in the technology and digital service industries we re spending less on marketing as a result of ongoing budget cuts following the COVID outbreak.

The condition of the advertising sector is closely linked to the state of the economy. In light of the exceptionally high inflation rates and ongoing uncertainty regarding a potential economic downturn, many advertisers have taken steps to reduce their marketing expenditures. As of August 2023 , inflation has reached 3.7%, which significantly exceeds the Federal Reserve's benchmark interest rate. It appears that inflation is likely to persist, given the Federal Reserve's indication of prolonged higher interest rates . Over the next few quarters, I anticipate that technology companies will continue to adjust their marketing budgets. Should inflation prove to be persistent or increase further, it could result in additional reductions in advertising spending.

As a result, sales in the North American market fell by 4.1% during 2Q. Given that this weakness in tech spending was already present in 1Q but it accelerated in 2Q, it indicates that the weakness is still present, and potentially deteriorating into 3Q as per management comments in the call.

"The part of our business that we have seen a shortfall has been in the United States with the gap versus our expectations in the prior year, really been focused on technology clients and technology-related projects. We did flag earlier this year that we've seen some slowdown in spending from technology clients on marketing but this accelerated in the second quarter. Perhaps it took us maybe a little bit by surprise ." 2Q23 call

WPP's like-for-like growth guidance for FY 2023 was also lowered from 3-5% to 1.5–3.0% as a result of weaker 2Q results and a spending slowdown by its largest customer group. The weak guidance indicates the lack in confidence over the near-term. That said, management do expect underlying margin to stay the same, which is a good indicator of cost management that will improve the business long-term margin profile structurally. Specifically, management cited the consolidation of office space on campuses across the US as one of the measures taken to reduce expenses. While positive, this will result in a full-year impairment charge of around £220 million, which will affect margins. Management also noted that opening the campuses would result in higher energy and facility costs, so any additional savings from the transformation program wouldn't be realized until 2025 at the earliest. Therefore, on a headline basis, I expect this to further weigh on the stock.

Valuation

I anticipate that WPP's growth prospects in FY2023 and 2024 will remain subdued, with an expected increase of only 1%. This conservative outlook is primarily driven by the company's recent financial performance trends, which have been on a decline over the past five years. Notably, WPP's revenue CAGR has registered a negative figure of 1.7%.

One significant factor contributing to this stagnation is the reduced spending from their largest customer segment, namely tech companies in the United States. This decline in spending was prominently reflected in the company's most recent quarterly report, which presented discouraging results. Adding to the pessimism, the company's management lowered its guidance for fiscal year 2023 following the disappointing second-quarter results.

When considering valuation metrics, WPP's forward EV/EBITDA multiple currently stands at 6.55X. In comparison, the median forward revenue multiple for its competitors, which includes industry giants like Omnicom Group and Publicis Groupe, stands higher at 7.07X. Given the challenges facing WPP in terms of revenue and margin expectations, the lower multiple appears to be justified. Furthermore, WPP reports an EBITDA margin of 12.99%, which significantly lags behind the 17.59% average EBITDA margin observed among its competitors. This disparity underscores the company's struggle to maintain profitability in comparison to industry peers.

Taking all these factors into account, my target share price for WPP is set at 823.27 pence. At this valuation, there appears to be limited potential for upside gains. Moreover, should WPP's future financial results fall below expectations, it could lead to further reductions in its valuation multiples, ultimately exerting downward pressure on the company's share price.

Author's work

Risk and final thoughts

Potential risks for WPP encompass reductions in client spending, vulnerability to cyclical advertising shifts in both established and emerging markets, challenges in managing increased inflation-related costs, and unanticipated hits to profit margins amid a demanding economic backdrop. The advertising agency sector is fiercely competitive, heightening the possibility of losing significant clientele. Moreover, the industry faces structural transformations due to the rise of new platforms in technology, e-commerce, and generative AI, introducing additional risks.

I recommend a hold rating for WPP based on its recent lackluster performance, weakened growth prospects, and inherent risks. Over the past five years, WPP has struggled to maintain revenue and margin levels, and the second quarter of this year revealed further challenges. Reduced spending from tech companies in the US, a significant customer segment, has led to a decline in sales, making the company's outlook uncertain. Management's lowered guidance for FY23 reflects their lack of confidence in near-term prospects. While cost-saving measures are in place, such as office space consolidation, the benefits won't materialize until 2025.

For further details see:

WPP Group: Recent Performance Reflects Slower Growth And Challenges Ahead