WSPOF - WSP Global: Strong Backlog Should Translate To Higher Revenues

2024-01-13 04:27:03 ET

Summary

- WSP Global is a leading engineering company in Canada, providing a wide range of services to government and private sector clients.

- The company has a strong track record of performance, outperforming the TSX Composite Index and showing consistent revenue and EBITDA growth.

- WSP Global has a growing backlog of contracts, indicating future revenue growth, and management is optimistic about future acquisitions and market share expansion.

- With good growth expected as a result of its backlog, shares look reasonably priced at 16x EBITDA.

Please note all $ figures in , not , unless otherwise stated.

Company Overview

While WSP Global Inc. ( WSP:CA ) may not be a household name, it's one of the largest companies in Canada. As an engineering company, WSP Global serves both government and private sector clients by providing them with a wide range of consulting services including design-build, environmental due-diligence, project management and more. The applications for these services can vary widely and includes things like transportation developments, large infrastructure projects, and complex constructions.

Some examples of these projects include providing multidisciplinary services like structural engineering and geotechnical expertise on the Kangaroo Point Green Bridge project and being involved in the designing and building of the a low-temperature hot water system for the National Capital Region's District Energy System that is helping the project transition to become more energy efficient.

With over 67,000 employees working in several capacities like engineers, scientists, engineers, and environmental professionals, WSP Global has the technical expertise and know-how to take on consulting for some of the world's largest and most complex projects. With sustainability and ESG becoming paramount and even required considerations in consulting, WSP Global has won several industry awards as being recognized as a leader within the field.

ESG Accolades (Investor Introduction - Jan 2024)

{kind=link}

Strong Performance

One of the things that impressed me the most about WSP Global has been its track record of performance over the years. When looking at the share price performance of the company, WSP Global has outperformed the TSX Composite Index over the last decade, returning 489.6% (not including dividends) compared to the TSX's return of just 51.8% over the same time period. This makes WSP Global one of the best performing stocks over the last decade, returning an annualized CAGR of about 10.64% excluding dividends.

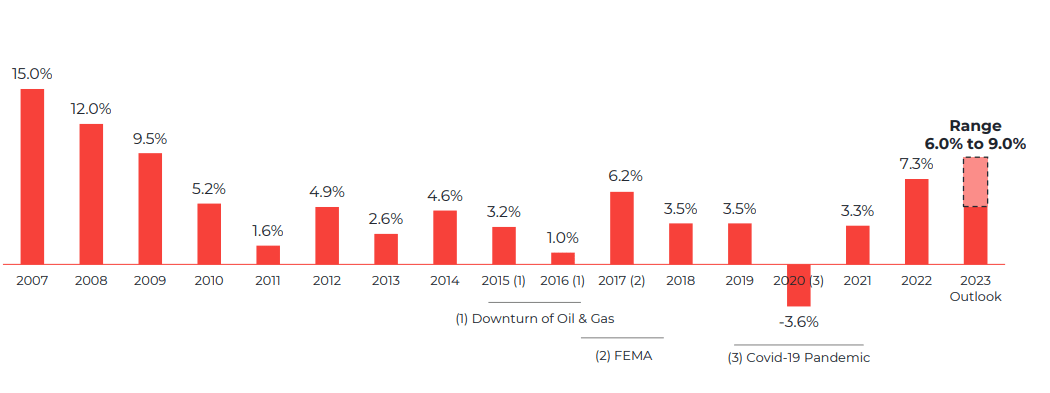

This strong share price outperformance hasn't been without strong growth in company financials. Since 2016, its grown its revenues by 87% and has more than tripled adjusted EBITDA, showcasing how it's been able to grow sales and concurrently expand margins over time. And despite M&A activity fueling a fair bit of the growth, we can see from the chart below that organic growth has been positive over its life as a public company, with the only exception being in 2020 as a result of the pandemic. In my view, this speaks to the resiliency of WSP Global's business model, being a great business to own even during weaker economic periods, as there always seems to be a strong demand for its services.

Organic Growth (Investor Introduction - Jan 2024)

{kind=link}

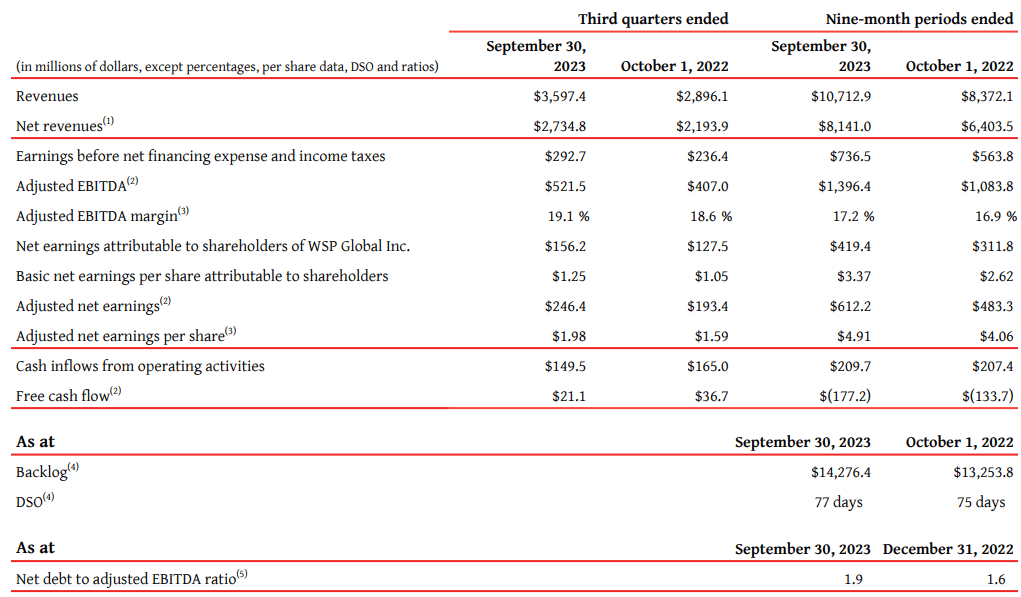

One of the reasons I believe there always seems to be demand for WSP Global's services is because of the company's backlog. At quarter end , the company had backlog of $14.3 billion, up 7.5% from last year's backlog at $13.3 billion. Historically, the company's backlog has been a pretty good indicator of what we can expect revenues to look like in the future, because backlog results from signed contracts for services yet to be completed. So with a growing backlog, it's a pretty safe bet that the company's revenues will continue increasing.

According to IBIS World , the engineering services market in Canada is a $45.9 billion industry with several players. The largest player is WSP Global with 3.6% market share. Growth in this industry is driven by various factors including infrastructure development, environmental sustainability, government investments, energy sector developments and population growth. As an international company, WSP also benefits from these same factors in international markets where the population growth and infrastructure growth is growing much faster. Globally, infrastructure spend is expected to increase at about a 6.3% CAGR, so I believe WSP will be well positioned to capture some of these tailwinds and continue to grow its backlog at a decent rate.

One of the major growth catalysts for WSP is its environmental and water business. This was a business that if we look back six years ago when the company wanted ramp up its investment in the space, it was representing just 10% of company revenues. Today, that business represents over a third of sales. Showcasing this growth, the company employees over 20,000 people in the environmental and water business (30% of its workforce) and this business will only continue to grow over time. As the market leader in the space, I believe WSP will be a partner of choice for organizations, both public and private, especially as the company has deep expertise in soft earth and environmental services, social acceptability studies, and other related services for this segment, experience that is critical for those customers.

Recent Results

We've already discussed backlog, but let's take a look at the rest of its Q3 results to get a better sense of the recent business performance.

When looking at the recent Q3 results of the company, WSP Global observed an increase in net revenues to $2.73 billion, up 24.6% from Q3 of last year. We also saw adjusted EBITDA up 28.1% year over year, with 50 basis points of margin expansion.

{kind=link}

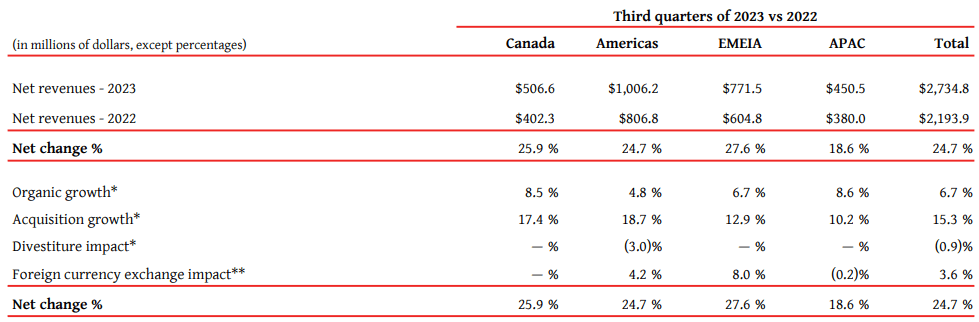

In analyzing the company's results for the quarter, I would say this was an exceptional quarter for WSP Global. In all geographical segments, the company generated positive year over year organic growth during the quarter with the highest being in Canada and APAC up 8.5% and 8.6%, respectively, and the weakest one being the Americas up 4.8%.

Segmented Financial Information (WSP MD&A)

{kind=link}

Despite a lower figure on the organic growth front in the Americas region, management noted on the earnings call that the company's sub backlog in the U.S. was about 50% higher since Q3 last year and 30% higher than it was since early 2023. As I mentioned earlier, with stronger backlog, this should translate to higher revenue growth in the coming quarters for the Americas segment.

It's important to note that this backlog is backlog that the company has bid on contracts for and now just needs to execute and finish the work. So there's not a big risk to this backlog not translating into higher sales. In addition to this, management also mentioned that its win rate is higher than it was against last few years, winning more projects than its competitors. This is a good indication that the company is gaining market share in the U.S. and will likely continue to do so.

With acquisitions contributing net revenue growth of 15.3% year on year and the company having now completed its largest acquisition of the year (the environment and infrastructure business of John Wood Group), management still seems optimistic on the opportunity set it has to continue to be acquisitive:

Jonathan Lamers

On the Wood E&I integration, is that complete now? And how do you feel the overall WSP is positioned for next acquisition?

Alexandre L'Heureux

Yes. Look, it's a one-year anniversary. So we are very pleased with the way the Wood E&I performance have gone so far, but also on the integration front. Obviously, this was - in terms of numbers, the largest acquisition we had completed in our history. So there's still obviously some, I would say, some stream of activities that we continue to complete and must complete to have like a full integration completed. However, I feel that we are in a very, very good position at this point in time. When you look back on the effort and what we were able to achieve over the last 12 months. So I think that if your question more specifically, is that a road block to future acquisitions, the answer is absolutely not.

In my view, supporting this optimism is also the company's balance sheet. At quarter-end, the company had $1.57 billion in available short-term capital resources. While the company did take on a bit of debt to fund the John Wood Group acquisition, the company's long-term debt is still very manageable at $3.7 billion with a Debt/Equity ratio of 15.8% and a Net Debt to EBITDA ratio of 1.9x. While the company did see higher financing expense as a result of the debt brought on by the acquisition as well as higher interest rates, 45% of WSP Global's long-term debt is insulated through interest rate swaps or fixed rate debt to project against changes in interest rates.

Valuation

Based on the 9 equity research analysts who cover WSP Global's stock, there are 8 buys and 1 hold. Collectively, the average target price from these analysts is $211.33, with a high estimate of $220.00 and a low estimate of $205.00 (S&P Capital IQ). From the average target price of $211.33, this implies one-year upside of 14.7% indicating that analysts are bullish on the company's outlook going forward.

I would be inclined to agree with the analyst community's assessment here. Comparing WSP Global to its historical EV/EBITDA range, the company has historically traded within a range of 6.9x and 24.3x EV/EBITDA, clocking in at about 16.1x EV/EBITDA at present. While this is closer to the higher side of the historical range, I still think the valuation is justified here, despite shares off 4.5% from the recent peak.

The reasons for this are that the backlog continues to remain very strong, the company has a balance sheet with continued capacity to make acquisitions, and the management's confidence in the business outlook. In Q2, they revised guidance upwards by $100 million (reaffirmed this quarter) which would equate to $1.9 billion for the full year, and so I believe with the recent results they should be able to meet, if not exceed, that guidance.

We can also compare WSP Global to its competitors to get a better sense of its relative valuation. When comparing WSP Global to its peers, the company trades slightly above the median forward multiples of the peer group at 19.8x earnings and 12.7x EBITDA.

What I think is important to remember here, however, is that WSP is a much higher growth company than its peers. For example, Stantec ( STN:CA ), which would be the closest Canadian large-cap peer, is engaged more in construction where WSP is solely involved in design, services, and consulting. In addition, with much more environmental presence as a consequence of its acquisitions, the company has more of an international presence and can grow faster. So given this, I believe that WSP is worthy of its higher valuation when compared to the peer group.

Comparables (Author, based on TD Securities' estimates)

{kind=link}

Risks

In terms of the risks here, the key risks to the investment thesis would be the company's ability to maintain and manage its growth as well as the cyclicality of the construction industry. While the construction industry ebbs and flows with the economy and can be cyclical, I'm confident about the company's backlog as its growing over time as well as the fact that there's strong industry tailwinds for the company long-term.

Finally, the last risk would be a shortage of skilled labor. Engineers and other skilled professions are hard to come by in this labor market so this is a risk to monitor. On the earnings call, management had this to say about the hiring situation:

Well this year, we will come in excess of 10,000 newcomers within the company, which is a testament of our ability to recruit talent within the company globally. And also, we have seen a sharp reduction in turnover and now back to close to historical level. So when you combine our ability to recruit and a reduction in turnover, I'd say that now, I think we're obviously feeling better than perhaps where we were 18 months ago as a result of it.

So overall, based on management's comments, I'd say the company has taken the right steps to retain and recruit talent. While competitors may be facing challenges, it seems like WSP is handling it better by constantly looking out a few years ahead and make sure it takes care of employees, with a 4 out of 5 stars on Glassdoor.

Conclusion

In summary, WSP Global provides investors with an opportunity to own a high quality Canadian company with both organic and inorganic growth potential. The company has put up good organic growth over the years and should be able to grow organically at around 5% for the foreseeable future. With additional growth expected through potential for future M&A, this increases my expectation for what overall growth will look like going forward. At a valuation of just 16.1x EV/EBITDA, the valuation seems reasonable when we consider the company's track record of growing revenues and expanding margins over time. For these reasons, I rate shares of WSP Global as a buy today.

For further details see:

WSP Global: Strong Backlog Should Translate To Higher Revenues