WTV - WTV: Too Small Value Exposure Does Not Justify A Bullish Outlook (Rating Downgrade)

2023-09-26 01:58:04 ET

Summary

- WTV, a shareholder yield-centered actively managed ETF, has been mostly a disappointment since my previous coverage in February 2023.

- Since the previous article, the portfolio has seen only minor changes, yet there were notable metamorphoses regarding factor story under the surface.

- I downgrade WTV to a Hold, but not because of its sluggish performance; the culprit is the current market environment and the fund’s too-small value exposure.

WisdomTree U.S. Value Fund ETF ( WTV ), a shareholder yield-centered actively managed fund, has been mostly a disappointment since my previous coverage back in February 2023 as it has not lived up to bullish expectations and underperformed the S&P 500 index amid the growth rotation. Today, I would like to provide an update on its portfolio composition, factor exposure, and explain why I downgraded it to a Hold. A quick spoiler before we delve into the data: this is not because of its sluggish performance; the culprit is the current market environment and the fund’s too small value exposure.

WTV Favors Rich Shareholder Yields Backed By Quality

According to its website , incepted in February 2007, WTV became actively managed in December 2017. It is said that the fund now

seeks income and capital appreciation by investing primarily in U.S. equity securities that provide a high total shareholder yield with favorable relative quality characteristics.

In the previous article, I provided the following summary of the strategy based on the prospectus :

What is the cornerstone of its strategy today? In short, as described in the prospectus, the goal is to select about 200 stocks that sport high total SY which is essentially a sum of dividends paid and the funds directed to share repurchases as well as decent quality manifested in substantial Return on Equity and Return on Assets.

How the WTV Portfolio Has Changed: Reasons For a Downgrade

As of September 22, WTV had 121 holdings vs. 124 as of the previous coverage. The first conclusion that can be drawn upon looking at WTV's holdings is that its portfolio remains more or less homogeneous over time despite its active strategy, which, in theory, should welcome more frequent additions and deletions. To corroborate, since the previous note, just 5 companies were removed, namely the following:

| Company |

| Sector |

| Weight as of February 14 |

| Wells Fargo & Company ( WFC ) |

| Financials |

| 0.99% |

| PDC Energy (traded with the ticker PDCE) |

| Energy |

| 0.98% |

| Zions Bancorporation, National Association ( ZION ) |

| Financials |

| 0.92% |

| CF Industries Holdings ( CF ) |

| Materials |

| 0.64% |

| Murphy USA ( MUSA ) |

| Consumer Discretionary |

| 0.54% |

Created using data from WTV

It is important to note that PDC Energy was acquired by Chevron ( CVX ) in August, so its disappearance from the basket is understandable.

At the same time, only two companies were added, namely CVX, an energy supermajor, and Salesforce ( CRM ), an application software industry heavyweight, now accounting for 2.4% combined. CVX has both a generous dividend and a stock buyback program backed by massive free cash flow thanks to supportive oil market sentiment. For instance, in H1 2023, the company generated about $6.75 billion in FCF after all investing activities factored in. It returned about $13.6 billion to shareholders via dividends and net purchases of treasury shares and still ended Q2 with $10.4 billion in cash, cash equivalents, and restricted cash. However, the PDC acquisition mentioned above had an impact on the company's shareholder rewards, with the buyback temporarily paused in July. For better context, here are VP and CFO Pierre Breber's comments shared during the earnings call in July:

Since PDC's proxy solicitation on July 7th, we've not been permitted to buy back our shares. After we close the acquisition in August, we plan to resume buybacks at the $17.5 billion annual rate, which we expect to continue through the fourth quarter.

CRM has only a share repurchase program, but a sizable one. As CEO Marc Benioff said during the most recent (Q2 FY2024) earnings call :

Now through the second quarter, we have returned and this is amazing, $8 billion in share repurchases since we started the buyback program a year ago. So we've bought $8 billion of stock over the last 12 months that is really awesome.

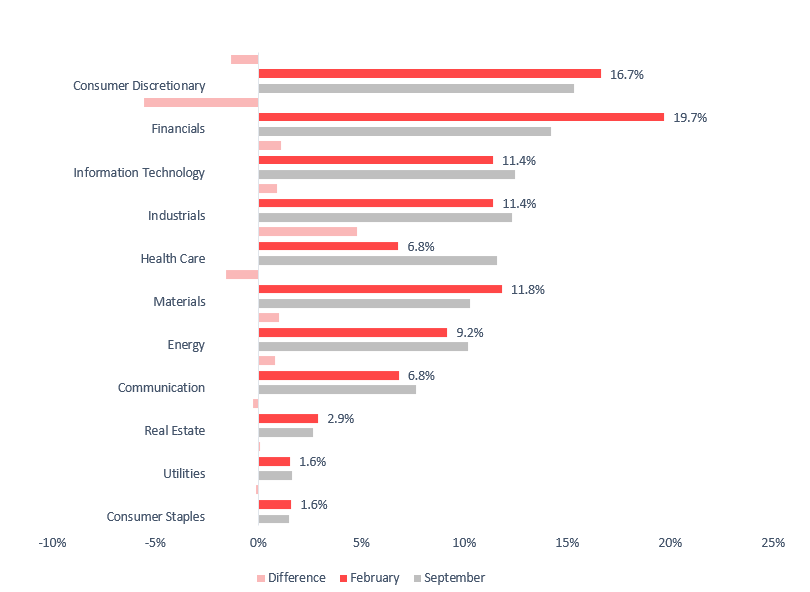

Regarding sectors, the fund now has much smaller exposure to financials, which were its largest allocation back in February.

Created using data from the iShares Russell 3000 ETF and WTV

{kind=link}

Obviously, the primary reason for the sector losing about 5.5% was not removals but its sluggish performance. To corroborate, among the 20 financial stocks the fund has in its portfolio at the moment, 13 have delivered negative price returns YTD (as of September 24).

In the meantime, healthcare has gained solidly, now accounting for around 11.6% of the net assets, mostly because 4 names from the sector delivered double-digit gains (compared to their share prices as of February 15).

| Ticker |

| Company |

| Price as of February 15 |

| Price as of September 24 |

| Change |

| ( CAH ) |

| Cardinal Health Inc |

| 78.58 |

| 88.96 |

| 13.2% |

| ( MCK ) |

| McKesson Corp |

| 363.64 |

| 438.66 |

| 20.6% |

| ( MEDP ) |

| Medpace Holdings Inc |

| 208 |

| 242.69 |

| 16.7% |

| ( AMGN ) |

| Amgen Inc |

| 240.065 |

| 267.7 |

| 11.5% |

Calculated using data from Seeking Alpha and the fund

Now, this is how the key value, growth, and quality parameters changed:

| Metric (weighted-average) |

| September |

| February |

| Market Cap |

| 55.9 |

| 37.8 |

| EY |

| 7.8% |

| 11% |

| DY |

| 1.8% |

| 1.7% |

| Revenue Fwd |

| 2.7% |

| 8.9% |

| EPS Fwd |

| 5.2% |

| 10.9% |

| ROE |

| 27% |

| 42.3% |

| ROA |

| 8.6% |

| 10.4% |

| Quant Valuation B- or higher |

| 24.3% |

| 31.6% |

Calculated by the author using data from Seeking Alpha and the fund; financial data for the September column as of September 24

The factor story presented above is hardly supportive of a bullish thesis, with the main reason being insufficient value exposure. In fact, the fund now has a significantly larger weighted-average market cap (with the contributors being CVX and other mega-cap league members), which, alas, comes with a smaller earnings yield. However, the compression of the EY is not necessarily an issue, as it was principally driven by NRG Energy's ( NRG ) negative LTM net income. Oddly enough, NRG had a positive EY as of the previous note, about 23%, being one of the top contributors to the fund's EY. Nevertheless, there is a much more serious problem: just 24.3% have a B- Valuation rating. I appreciate the fund's solid quality, especially its meaningful ROE and ROA and almost 91% of the net assets allocated to companies with a B- Quant Profitability grade or higher, but amid the higher-for-longer narrative, value should be prioritized.

Performance Overview: WTV Is Lagging IVV YTD Due to The Financial Sector

The sluggish performance of stocks like banks, asset managers, etc. amid the short-lived banking crisis back in the spring is the essential reason why WTV has underperformed the S&P 500 index as well as the iShares Core S&P 500 ETF ( IVV ) since my previous article and also since the beginning of the year (by about 4.28% as of September 25).

Seeking Alpha

In the previous note, I mentioned that WTV had beaten IVV since the strategy change (the January 2018 - January 2023 period). With the new data factored in, it looks much weaker, as it trailed IVV during the January 2018 - August 2023 period. Compared to peers with relatively similar strategies, it underperformed the Cambria Shareholder Yield ETF ( SYLD ), but did better than the Principal Value ETF ( PY ) and iShares Core Dividend ETF ( DIVB ).

| Portfolio |

| IVV |

| WTV |

| PY |

| SYLD |

| DIVB |

| Initial Balance |

| $10,000 |

| $10,000 |

| $10,000 |

| $10,000 |

| $10,000 |

| Final Balance |

| $18,567 |

| $17,262 |

| $14,698 |

| $18,649 |

| $16,808 |

| CAGR |

| 11.54% |

| 10.11% |

| 7.03% |

| 11.63% |

| 9.60% |

| Stdev |

| 17.97% |

| 21.52% |

| 23.43% |

| 26.34% |

| 18.75% |

| Best Year |

| 31.25% |

| 30.57% |

| 34.82% |

| 48.30% |

| 32.73% |

| Worst Year |

| -18.16% |

| -8.27% |

| -13.34% |

| -13.53% |

| -10.51% |

| Max. Drawdown |

| -23.93% |

| -31.43% |

| -33.46% |

| -37.12% |

| -24.50% |

| Sharpe Ratio |

| 0.61 |

| 0.48 |

| 0.34 |

| 0.49 |

| 0.49 |

| Sortino Ratio |

| 0.91 |

| 0.71 |

| 0.48 |

| 0.75 |

| 0.74 |

| Market Correlation |

| 1 |

| 0.94 |

| 0.9 |

| 0.85 |

| 0.96 |

Created using data from Portfolio Visualizer

Investor Takeaway

WTV's inability to beat IVV this year is not the key reason for a downgrade. In fact, WTV might remain an interesting shareholder rewards-centered strategy to consider for the long term, thanks to the attention paid to quality. However, it is unattractive tactically owing to small value exposure, principally manifested in less than a quarter of its holdings having a B- Quant Valuation grade or better.

For further details see:

WTV: Too Small Value Exposure Does Not Justify A Bullish Outlook (Rating Downgrade)