XFOR - X4: Dip Following Mixed Results In Chronic Neutropenia Indication Worth Buying

2023-12-13 23:43:55 ET

Summary

- X4 Pharmaceuticals has dipped considerably following updated results presented in ASH suggesting that mavorixafor may not be effective as monotherapy in chronic neutropenia (excluding WHIM).

- Mavorixafor will likely still have a role in chronic neutropenia as add-on to G-CSF. Mavorixafor can enable reductions in G-CSF dosing, which can improve tolerability and is meaningful for patients.

- FDA has granted priority review for mavorixafor in WHIM, with a PDUFA date of April 30, 2024, and a potential PRV worth $100M upon approval.

- Considering premium (ultra orphan) pricing potential, I expect meaningful revenue potential from just WHIM indication, sufficient to justify upside from current XFOR's valuation.

- XFOR is sufficiently funded into 2025, not considering monetization of PRV and access to debt facility, which would considerably extend cash runway.

Brief summary of prior coverage

X4 Pharmaceuticals (XFOR) is developing mavorixafor for WHIM (a rare inherited form of chronic neutropenia), as well as for a broader chronic neutropenia patient population. Mavorixafor's mechanism of action is ideal for WHIM and results from clinical trials are very convincing for an eventual approval in WHIM. In my prior coverage I recommended XFOR as a "Buy" considering de-risking by WHIM indication and potential label expansion in chronic neutropenia, which is a larger target market. My thesis remains unchanged, despite the considerable dip (-53%) since my prior coverage. An update follows below.

Thesis update

XFOR announced a poster presentation in ASH updating the course of the first 3 patients enrolled in the chronic neutropenia phase 2 trial. Unfortunately the market had false expectations for mavorixafor's monotherapy potential in chronic neutropenia. Results show that mavorixafor is not going to replace G-CSF, the current standard of care. On the other hand, mavorixafor might still have a role as add-on therapy to decrease dose/frequency of G-CSF, to correct neutropenia in patient that remain neutropenic on G-CSF and most importantly to reduce risk of infection in these patients.

On more positive news, FDA has accepted NDA submission for WHIM indication, granting priority review (PDUFA date April 30, 2024) and a potential Priority Review Voucher (PRV) upon approval, the latter typically worth about $100M. Considering orphan designation and ultra orphan indication I expect premium pricing of mavorixafor for WHIM, at least $100K per patient per year (while others estimate even higher pricing potential). Therefore, despite the small pool of eligible patients there is good revenue potential for XFOR and I believe XFOR remains de-risked based on WHIM potential.

This is the 3rd dip buying opportunity I am covering, following recent coverages of ATRA (+>150%) and MOR (+82%). Note, however, that I don't expect as fast upside from XFOR. Unless there are positive surprises (e.g. insiders buying), the main price-moving catalysts to expect is FDA decision on WHIM and update on the so far n=15 enrolled patients in chronic neutropenia ph2 (anticipated in H1 2024). There is a risk that the downtrend may even continue. The major risk for XFOR investors now is a CRL for WHIM, which would negatively impact cash runway, despite eventual approval being certain in my opinion.

Update on WHIM

XFOR recently announced acceptance by the FDA of the NDA submission for WHIM indication. Most importantly, FDA has granted a priority review, which means not only a faster review (PDUFA date April 30, 2024) but also potential for a PRV (typically worth $100M) upon approval. These news significantly de-risk XFOR because of the potential to extend cash runway with the PRV, as well as considerable (relatively to current XFOR valuation) revenue potential in just WHIM.

To sum up market potential from my prior coverage and considering about 1000 patients in US (estimate by XFOR that matches my estimate based on the limited available epidemiological data);

Considering orphan drug designation annual pricing of >$100K ( others have predicted a pricing of $200-300K/year) per patient is not unlikely, corresponding to market opportunity of >$100M ( x1.6 if European patients are included). Considering efficacy in the phase 3 trial and current lack of alternative treatments for WHIM syndrome, XFOR should be able to capture a big share of the above market opportunity (as long as the estimated 1000 WHIM patients can be found). Conservatively assuming just 20% market share, i.e. just 200 patients, this would correspond to peak revenue of >$20M just in US. Based on an EV/revenue multiple of 7.1 a fair EV at peak sales would be $140M (compared to a current EV of $96M ). Add to that patients outside US as well as the potential for priority review voucher (typically worth $100M).

My point is that based on just (conservatively estimated) market potential for WHIM syndrome XFOR seems undervalued. Therefore, even in case of setbacks with the rest of the pipeline downside risk is limited.

Outside US, XFOR has partnered with Abbisko Therapeutics for development and commercialization of mavorixafor in Greater China. According to the deal XFOR is eligible to receive potential development, regulatory and commercial milestone payments of up to $214 million. XFOR is also entitled to royalties in the low double-digits.

Note that I generally tend to be conservative to avoid creating false expectations. However, there is no competition in WHIM, no other approved product and clinical efficacy is impressive. Therefore, market penetration is most likely going to be higher, e.g. 50-75%, which would correspond to peak revenue of $50-75M just in US. Furthermore, ultra orphan drugs can have twice the price of orphan drugs. At twice the price the peak revenue potential would increase to >$100-150M just in US (vs a current market cap of $100M and EV of about $18M ). Also, the target market may prove to be higher due to lack of awareness, lack of routine genetic testing and potential underdiagnosis/underreporting of WHIM syndrome. For example, one study has estimated a prevalence of 1803 to 3718 WHIM look-alike patients in the US. The availability of an effective treatment will likely increase awareness and diagnosis of WHIM. Estimates for yearly costs for treating WHIM patients are not available, but based on data from patients with other immunodeficiencies could range from $100-150K per year. Therefore, a price in this range (and even higher) seems justifiable, given mavorixafor's efficacy. Notably, others have estimated even higher peak potential revenue of $300M in US (assuming pricing at $300K/year and larger target market) but I prefer not to be as optimistic.

XFOR plans to go alone in US, estimating a needed sales force size of just " couple dozen " to begin commercialization. XFOR has already partnered with Abbisko Therapeutics in Greater China and will also likely partner in Europe, although this remains to be decided. XFOR plans an MAA submission (Europe) for WHIM in late 2024 . By then XFOR should have more data on chronic neutropenia. This is important because potential partners would be interested in the broader chronic neutropenia population, not just WHIM. Considering lack of competition and decent cash runway XFOR is not in a hurry to seal a deal in Europe (the later the deal in clinical development, the higher the value will be).

Update on chronic neutropenia

As discussed in more detail in my prior coverage , considering mavorixafor's mechanism of action (ideal for WHIM but not for other chronic neutropenias);

My main concern here is whether mavorixafor can result in durable increases in white blood cells, because simply mobilizing neutrophils from the bone marrow doesn't really solve the problem (which is reduced production or increases apoptosis of neutrophils in the bone marrow). Theoretically, for durable increases in peripheral neutrophil counts increased mobilization should be accompanied by a matched increase in neutrophil production.

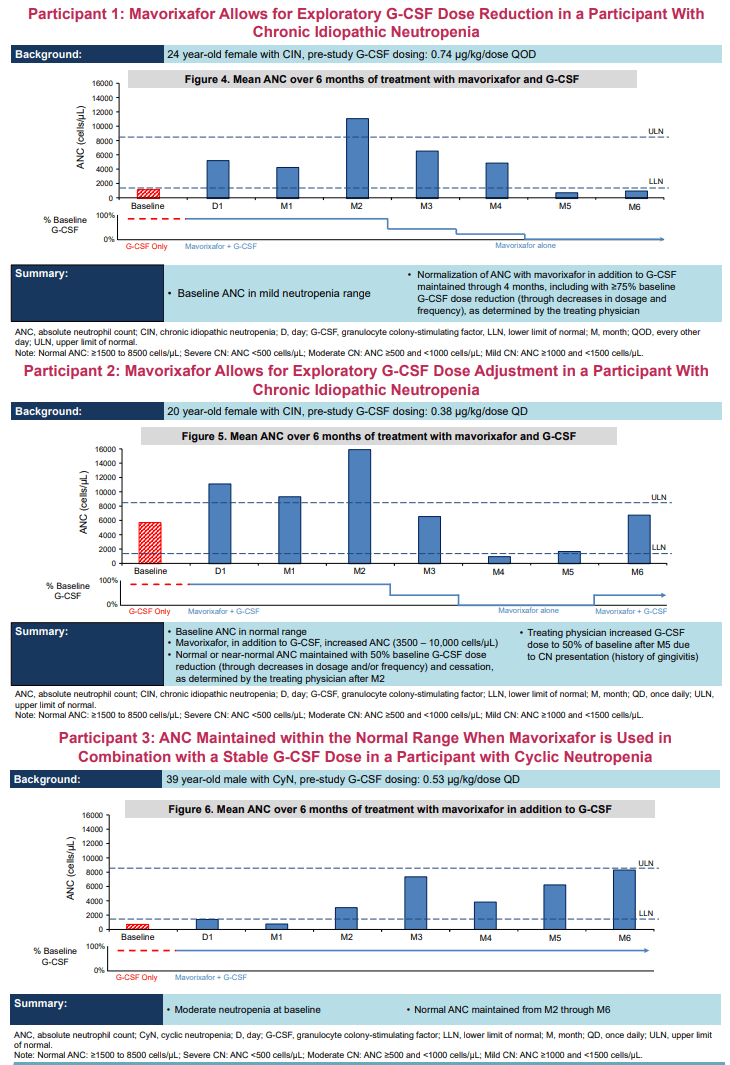

My durability concern was partly alleviated by then reported data from the first 3 patients, showing durable increases in neutrophil counts with mavorixafor as add-on to G-CSF. However, as expected based on its mechanism of action, mavorixafor was not able to allow G-CSF withdrawal according to the updated presentation in ASH. Specifically, in both patients that G-CSF withdrawal was attempted (Participants "1" and "2" in the image below) neutropenia recurred while on mavorixafor monotherapy. However, there is still some glimmer of hope that mavorixafor might work as monotherapy;

- In Participant 1, neutrophil count at month 6 (while on mavorixafor monotherapy for 2 months) was very close to neutrophil counts at baseline (while on G-CSF). In other words, the patient's neutrophil count was similar comparing G-CSF monotherapy to mavorixafor monotherapy.

- Participant 2 had a normal neutrophil count (above LLN) at month 5, while on mavorixafor monotherapy for 2 months, albeit much lower compared to baseline (while on G-CSF).

- Participant 3 was neutropenic at baseline while on G-CSF. G-CSF dosing regimen remained stable throughout the 6-month follow-up. Addition of mavorixafor improved neutrophil counts only after the 2nd month of treatment, and even more after the 3rd month of treatment. Therefore, there might be some late-onset benefit from mavorixafor treatment, and the 2-month withdrawal duration in above 2 participants may not have been enough to demonstrate this.

- There were no infections at months 3-6. In other words, participants 1 and 2 remained infection-free despite reductions/withdrawal of G-CSF and despite a decline in neutrophil count. Note however, that there were 4 infections during the first 2 months of treatment, albeit none severe (Participant 1; laryngitis, pharyngitis. Participant 2; nasopharyngitis, cystitis). However, these data are too limited to make any conclusions regarding mavorixafor's potential to reduce infection rate. Furthermore, baseline infection rate in these patients is unknown.

- Chronic neutropenia is a heterogenous condition. Failure of mavorixafor monotherapy in 2 patients does not preclude efficacy in other patients with different causes of chronic neutropenia. Even small augmentation in neutrophil counts may be protective of infection (i.e. patients can be neutropenic and still protected from infection).

However, in my opinion, the chances of mavorixafor monotherapy succeeding is low based on the very limited available data so far. As of November 2023 >15 patients have enrolled in the trial and an update is expected in 1H 2024. This could be price moving if data continue to support potential for dose/frequency reduction in G-CSF, or if there are positive surprises of successful mavorixafor monotherapy.

Updated results on the first 3 patients enrolled in the phase 2 trial (Poster presentation in ASH)

{kind=link}

Despite failure of mavorixafor as monotherapy, there is still significant potential as add-on to G-CSF as explained in the image below, because G-CSF is an injectable (patients obviously prefer less frequent injections) and often associated with adverse effects (reducing G-CSF dose could improve tolerability). Based on participants 1 and 2 it appears that mavorixafor can allow dosing reductions by ? 50% while maintaining normal or near-normal neutrophil count.

Reductions in dose/frequency of G-CSF is meaningful for patients (Poster presentation in ASH)

{kind=link}

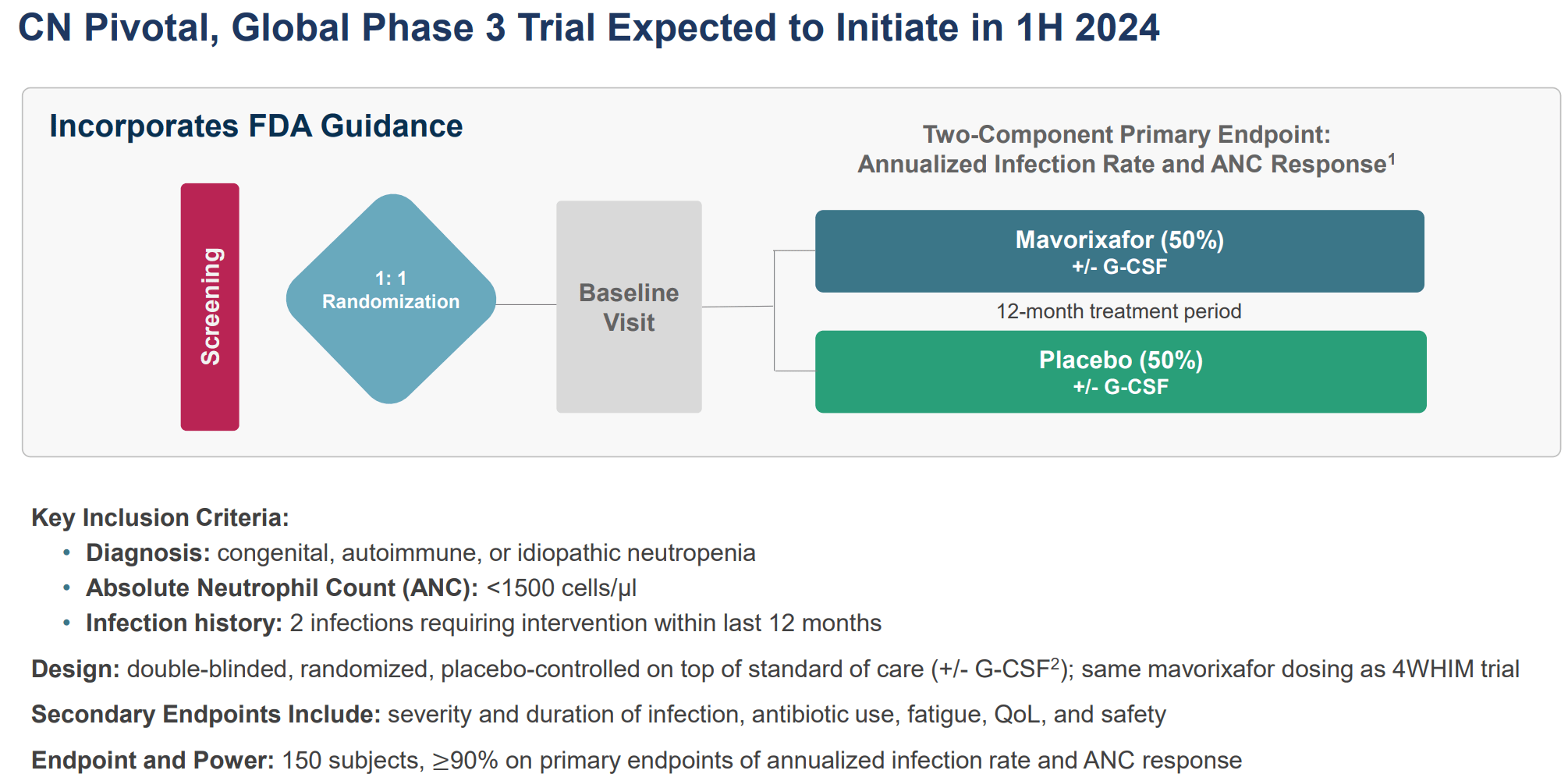

Design and goals of the planned Phase 3

Design of the phase 3 is summarized in the image below and also published in ClinicalTrials.gov ;

Design of phase 3 trial in CN. (X4 Investor Deck Nov 2023)

{kind=link}

The following are important to note about the phase 3 design and goals;

- The 2 primary endpoints, and goals of the phase 3, is to show that mavorixafor; (1) can correct neutropenia, and more importantly (2) can reduce annualized infection rate. Note that treatment of neutropenia with G-CSF is recommended only when patients have frequent infections. Therefore, the real goal is to reduce infection rate. There are many patients with chronic neutropenia that remain asymptomatic and thus do not need treatment. In other words mavorixafor needs to meet both endpoints, but more importantly needs to show a reduction in infections compared to standard of care.

- Enrolled patients won't necessarily be on G-CSF at baseline. Options at baseline include, but are not limited to granulocyte-colony stimulating factor (G-CSF), immunoglobulin replacement therapy, prophylactic antibiotics, or "watchful waiting". Now this is a concern, because it seems that mavorixafor won't work as monotherapy (although we have data for just n=2 patients so far). In my opinion the study should have limited enrollment only to patients that remain neutropenic on G-CSF and/or would benefit from dose/frequency reduction to improve tolerability. Enrolling a high proportion of patients without G-CSF could increase the chance of failure. Nevertheless, I wouldn't completely exclude yet monotherapy potential for mavorixafor.

- XFOR claims that with n=150 patients the study will be overpowered (?90% power for both primary endpoints). I agree that mavorixafor will easily meet the neutrophil count endpoint based on available data (at least as add-on to G-CSF). However, whether this will translate in reduced infections remains to be proven. Data we have from the first 3 patients (discussed above) are insufficient to make any firm conclusion on this. Also the cut-off for enrolment (2 infections within 12 months requiring interventions) seems a bit low. For comparison, in WHIM syndrome annualized infection rate was reduced from 4.5 (placebo) to <1 (mavorixafor). The lower the expected infection rate for placebo the higher the necessary sample to meet statistical significance. In contrast to WHIM, I don't expect as high efficacy from mavorixafor in chronic neutropenia (which would also mean the need for a larger study size).

- The study protocol does not include G-CSF dose down-titration. In fact, "for those treated with G-CSF at baseline, G-CSF dose and frequency are required to remain constant throughout the trial unless adjustment is needed for safety reasons". Furthermore, G-CSF dose/frequency reduction is not among the endpoints. Therefore, the goal of phase 3 is not to show that mavorixafor will reduce dose/frequency of G-CSF, but to show that mavorixafor can reduce infection rate.

Target market in chronic neutropenia

Not being able to replace G-CSF significantly reduces the market potential of mavorixafor in chronic neutropenia beyond WHIM. Therefore, XFOR's original estimation for 15K patients target population in US may be overoptimistic. However, mavorixafor could still have a role in the following cases;

- Patients that would benefit from a reduction in dose/frequency of G-CSF to improve tolerance.

- Patients that remain neutropenic and continue to have infections while on G-CSF. In such cases the goal of add-on mavorixafor would be to reduce incidence of infection by correcting the neutropenia.

- Patients that remain neutropenic and continue to have infections (although as already explained I am skeptical about mavorixafor's potential as monotherapy).

As explained above, the planned phase 3 will only address the latter two indications. However, assuming lack of potential as monotherapy (failure in indication 3), the first indication would actually have a much larger target market than the 2nd indication. The first indication is being evaluated in the ongoing phase 2 study, but I suspect another phase 3 might be necessary to support the first indication. In my opinion, such a phase 3 would enroll patients with chronic neutropenia on G-CSF. The goal would be to show whether adding mavorixafor can allow reductions in G-CSF dose, while not increasing infection rate (a non-inferiority design would be sufficient for this and would also be less demanding in terms of study size).

Potential in oncology?

After a strategic re-prioritization, XFOR is only currently advancing mavorixafor in chronic neutropenic disorder indications, including WHIM syndrome, while pre-clinical programs (including oncology programs) have been paused and progress in oncology programs is dependent on partnerships. However, as briefly mentioned in my prior coverage, there is potential for CXCR4 inhibitors in oncology, and there are other biotechs developing CXCR4 inhibitors for such indications (which further validates the potential). With regards to mavorixafor (that has the advantage of being orally administered) there are already 3 publications ( 1 , 2 , 3 ) suggesting potential in haematology/oncology. Also "ongoing trials in triple-negative breast cancer are being undertaken by Abbisko, our strategic partner for development and commercialization in greater China". XFOR has also developed two pre-clinical candidates: "X4P-003, a second-generation CXCR4 antagonist designed to have enhanced properties relative to mavorixafor, potentially enabling broader opportunities in CXCR4-dependent disorders and primary immunodeficiencies; and X4P-002, a CXCR4 antagonist with a unique distribution profile and a demonstrated ability to cross the blood-brain barrier".

My thesis is not dependent on the oncology potential but this could prove to be a nice positive surprise in a few years.

Update on financials

XFOR reported $142.7M in cash, cash equivalents, restricted cash, and marketable securities as of September 30, 2023. Total operating expenses were $27M (R&D $19M, SG&A $8M). Assuming stable expenses and available cash this should be enough for 15 months (i.e. up to the end of 2024). However, R&D expenses are likely to increase after the initiation of the phase 3 trial. Nevertheless, XFOR believes is sufficiently funded to support company operations into 2025. Importantly, this guidance does not account the potential monetization of a PVR (=$100M) from WHIM approval, or additional potential drawdowns from its debt facility.

Specifically, the following is available to XFOR from its debt facility; (1) a tranche of up to $20.0 million following potential U.S. approval of mavorixafor in WHIM. (2) an additional tranche of $7.5 million, following achievement of a certain clinical development-related milestone, (3) an additional tranche of up to $32.5 million, which will be available subject to approval by Hercules in its sole discretion. XFOR currently has a long-term debt liability of $54M. "Borrowings are repayable in monthly interest-only payments through March 1, 2025, and in equal monthly payments of principal and accrued interest from April 1, 2025". The loans mature on October 1, 2026 (which can be extended July 1, 2027 under certain conditions). So there is no short-term risk from debt liability and potential revenues from mavorixafor should be more than sufficient to repay the debt.

Risks

- Although I am very confident of eventual approval of mavorixafor in WHIM, regulatory delays cannot be excluded. A CRL would significantly impact XFOR's cash runaway because it would (1) delay monetization of a potential PRV upon approval, (2) delay revenues from commercialization of mavorixafor.

- Another risk is disappointing results in the 1H 2024 update from the ongoing phase 2 trial in chronic neutropenia. However, considering markets expectations by now this is highly unlikely.

- WHIM target market may prove to be smaller than estimated and/or pricing may be lower, despite anticipated premium pricing.

- Assuming lack of potential for mavorixafor as monotherapy, there is a good chance that the planned ph3 trial (which will also enroll patients not on G-CSF) may fail. XFOR plans to start the trial in 1H 2024 but I wouldn't be surprised if the trial protocol is modified by then. Alternatively, I assume XFOR might have to start another ph3 to assess mavorixafor's potential as add-on to G-CSF to reduce dosing requirements for G-CSF.

Conclusion

XFOR valuation has declined significantly since my last coverage, especially after updated results suggesting that mavorixafor may not work as monotherapy in chronic neutropenia beyond WHIM. However, I believe the dip represents a good "Buy" opportunity considering (1) cash runway into 2025, (2) potential extension of the cash runway after approval of mavorixafor in WHIM ($100M-worth PRV, access to $20M debt, revenue from sales), (3) considerable revenue potential from just WHIM due to premium (ultra orphan) pricing potential, (4) potential label expansion to chronic neutropenia of mavorixafor as add-on to G-CSF, (5) potential revenue (milestones-royalties) from existing Greater China licensing deal, (6) potential revenue for new partnership in Europe. The major risk to the thesis is regulatory delays with regards to WHIM indication.

Your feedback is appreciated

Please comment below if you have any feedback (positive or negative), if you spot any mistakes, or if you believe I missed something important in my analysis.

Also I suggest tracking comments if you are interested in following the stock as I may post updates there.

For further details see:

X4: Dip Following Mixed Results In Chronic Neutropenia Indication Worth Buying