XHR - Xenia Hotels: Occupancy Rate Increases As Divestitures Continue

2023-12-15 04:16:26 ET

Summary

- Xenia Hotels & Resorts is selling underperforming hotels, leading to higher FFO/net sales and higher EV/FFO.

- Analysts have increased their FFO expectations for the next quarter, indicating positive growth.

- XHR's solid balance sheet and strategic investments may bring demand for the stock and enhance its valuation.

Xenia Hotels & Resorts, Inc. ( XHR ) recently delivered lower than expected FFO , but analysts recently increased their FFO expectations for the next quarter. The occupancy rate also seems to increase as XHR appears to be selling underperforming hotels, which may lead to higher FFO/net sales and higher EV/FFO. With many years in the process of acquiring hotels, I would be expecting further cash increases if adequate sales of hotels continue. I also believe that further repurchase of shares in the open market could lead to growing demand for the stock. Yes, there are risks from a lack of buyers or sellers for hotels, inadequate financing sources, lower bookings than expected, or changes in consumer behavior. With that, Xenia Hotels & Resorts does look undervalued.

Xenia Hotels & Resorts

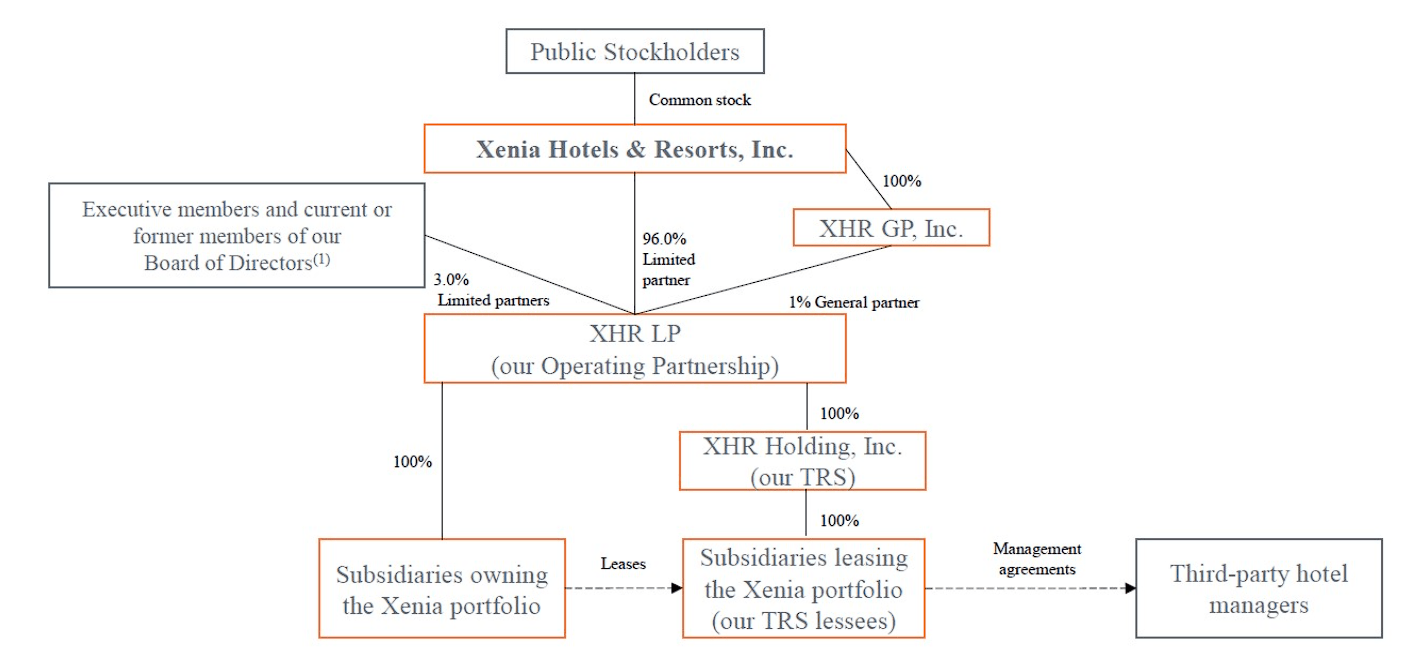

Xenia Hotels & Resorts is a Maryland corporation specializing in luxury hotel and resort investments in major lodging markets and key travel destinations in the United States. The company operates as a real estate investment trust, leasing properties to its taxable subsidiary, XHR Holding, which in turn contracts with third parties for hotel management. The company operates through the Operating Company and XHR Holding.

{kind=link}

Xenia focuses on various client groups to generate income, highlighting transient businesses, group businesses, and contract businesses. Individual businesses or leisure travelers, especially in the business segment, constitute a significant portion of transient demand. Groups of reserved rooms and blocks of rooms sold to specific companies, such as airline crews, contribute to group and contract business. Revenues come primarily from hotel operations, highlighting revenues from rooms, food, and beverages as well as other ancillary revenues. Occupancy, ADR, and distribution channel mix are key factors driving revenue. With that about the business model, current valuation is what, in my view, matters the most. In the last quarterly report, Xenia noted lower FFO, net sales, and EPS than expected. Quarterly net sales stood at close to $232 million. The numbers were not that beneficial, and the recent stock dynamics reacted showing downward pressure in the stock price. Having said so, incoming quarter earnings include positive FFO, and there are more increases in the last FFO revisions than decreases in the last 90 days. I believe that there is room for optimism.

Source: 10-Q

Other analysts' forecasts include net sales growth and FCF growth for 2024 and 2025. The forecasts of other analysts include 2025 total sales of $1.068 billion, 2025 EBITDA of $257 million, an EBIT of $98 million, an operating margin of about 9.14%, and earnings after taxes of $19 million. Finally, market estimates include net income of close to $20 million.

Source: Market Screener

Solid Balance Sheet With A Significant Amount Of Properties

The results for September 2023 showed that the land was valued at $460 million along with the buildings and another improvement of $3.157 billion, making a total of $3.617 billion. With accumulated depreciation, the total investment in properties is close to $2.572 billion.

With cash in hand close to $219 million, accounts and rents receivable of $39 million, and intangible assets of $4 million, total assets stand at about $2.962 billion. The asset/liability ratio stands at about 2x, so I believe that the balance sheet is stable.

Source: 10-Q

The total amount of debt is lower than the net investment properties. With debt, net of loan premiums of about $1.394 billion, I am not really concerned about the total amount of debt obligations. Finally, with accounts payable and accrued expenses worth $107 million, total liabilities stand at about $1.591 billion.

Source: 10-Q

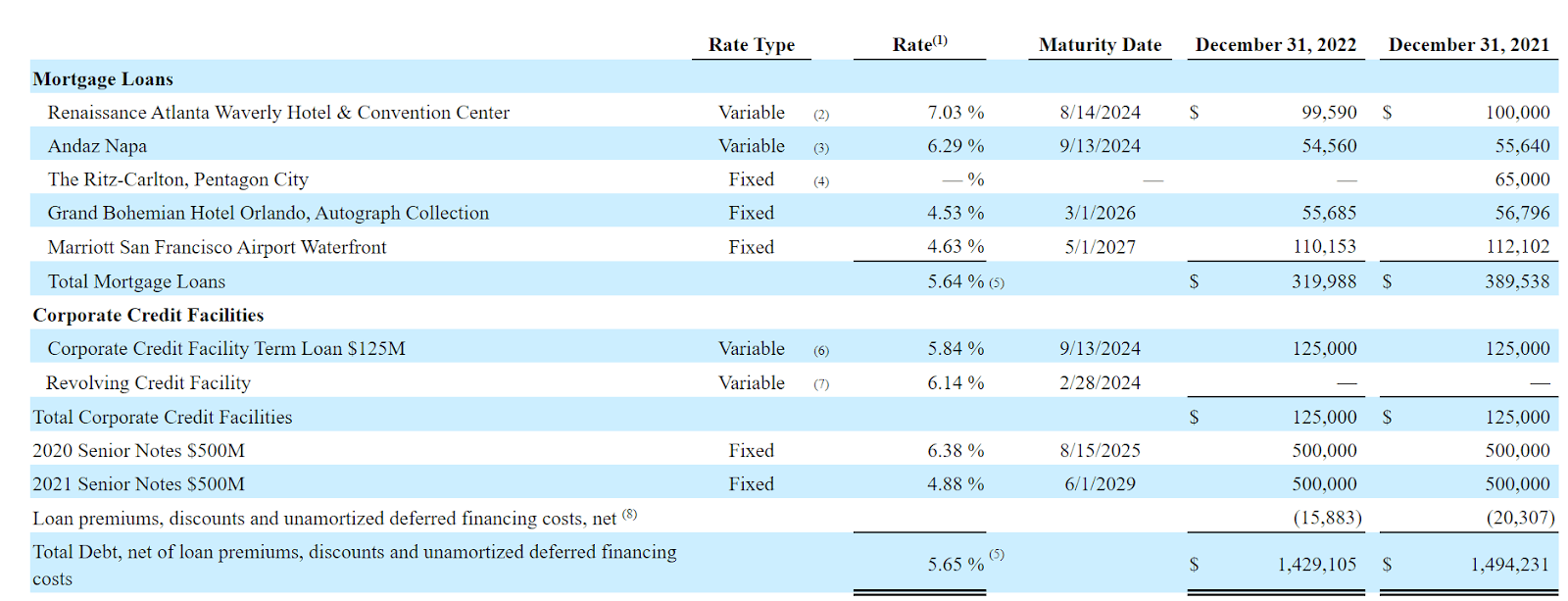

According to the last annual report, the weighted average debt maturity varied for different types, being 2.8 years for mortgage loans, 4.2 years for corporate lines of credit, Senior Notes, and revolving credit lines, and 3.9 years for total debt. The company refinanced its corporate line of credit term loan in January 2023, and adjusted interest rates effective that date. The interest rate reported stands between 4% and 7%.

{kind=link}

Current Strategy And Further Cash Increases May Bring Demand For The Stock

The company is dedicated to strategically investing in a diversified portfolio of luxury hotels and resorts in exclusive locations, focusing on major lodging markets and key tourist destinations in the United States. Its investment approach includes seeking opportunities based on market, asset, and transaction characteristics.

To drive growth, the company adopts proactive asset management, makes strategic capital investments, and employs internal teams for project and asset management. Its objective is to optimize the performance and quality of the portfolio, maintaining a solid competitive position.

In the portfolio , I could see that the oldest property was bought in 2007. I believe that Xenia has accumulated a significant amount of know-how in the industry, which will most likely enhance future negotiating processes in the coming years.

It is also worth noting that most properties were acquired between 2007 and 2015. Given the inflation increase in the last ten years, I believe that many of the properties are worth much more than the price paid for them. With this in mind, I would not worry if Xenia decides to sell some hotels to enhance the total amount of cash in hand. Please note how cash in hand has been increasing significantly since 2020.

Source: Ycharts

Occupancy Continues To Trend Higher, And Xenia Appears To Be Selling Lower Performing Assets

Xenia appears to be selling hotels with lower occupancy rate, which may bring higher occupancy rate and FFO/net sales increase. In the last quarterly report, Xenia noted the sale of two Hotels, so the number of hotels appears close to 32 right now.

The sale of Bohemian Hotel Celebration, Autograph Collection in October 2022 and Kimpton Hotel Monaco Denver Source: 10-Q

Source: 10-Q

The number of rooms decreased, however the occupancy rate increased. With a large portfolio acquired for many years, I believe that management is in a position to select the best hotels, and sell those that do not perform. As a result, we may see increases in profitability.

Source: 10-Q

The Stock Repurchase Program Could Enhance The Stock Price And The Demand For The Stock

Given the recent stock repurchases at around $15.52 per share, I would say that the Board Of Directors does not seem to believe that the stock is correctly valued at $15.52 per share. In my view, further acquisition of shares will most likely bring stock demand and may enhance the stock valuation.

During the three and nine months ended September 30, 2023, 2,070,777 and 6,516,485 shares were repurchased under the Repurchase Program, at a weighted-average price of $12.09 and $12.85 per share for an aggregate purchase price of $25.0 million and $83.7 million. During the three and nine months ended September 30, 2022, 120,978 shares were repurchased under the Repurchase Program, at a weighted-average price of $15.52 per share for an aggregate purchase price of $1.9 million. As of September 30, 2023, we had approximately $82.7 million remaining under our share repurchase authorization. Source: 10-Q

Source: 10-Q

My Income Statement Expectations Based On Previous Assumptions, And Previous Financial Statements

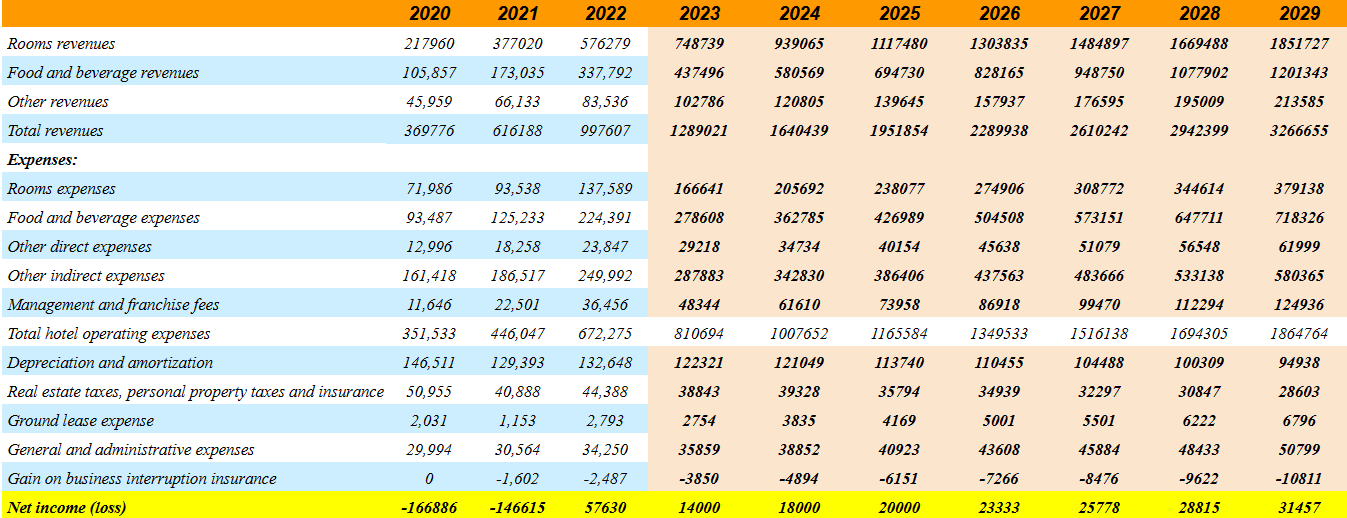

I expect 2029 rooms' revenue to be close to $1.851 billion, while the profit from food and drink could be around $1.201 billion. The other profits could be $213 million, giving us a total revenue of $3.266 billion.

My income statement also included the following assumptions. 2029 Room costs are $379 million, and food and beverage expenses are $718 million. Other direct expenses could be $61 million, with indirect expenses of $580 million. Management and franchise tax is estimated to be $124 million, and the hotel's total operating expenses are estimated at $1.864 billion. While depreciation and amortization could be around $94 million, real estate expenses are expected to be $28 million, with land leases of $6 million. The general and administrative expenses are estimated at $50 million, with a 2029 total of net income of $31 million.

{kind=link}

Valuation

HXR's P/AFFO stands at close to 8.27x, and the sector median is equal to 13.54x. The percentage difference to the sector is close to -35.47%, so Xenia appears significantly undervalued as compared to peers.

Source: SA

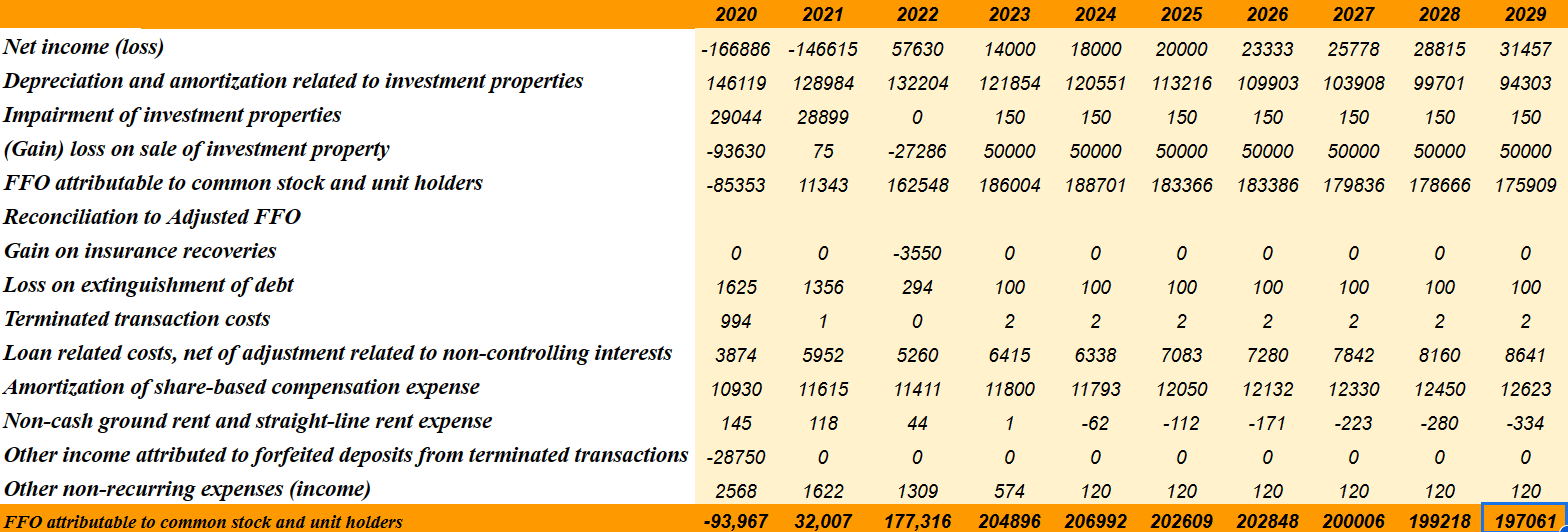

My cash flow projections are shown below. By 2029, the net income could be close to $31 million, and the depreciation and amortization on the invested properties may be $94 million.

Additionally, the impairment of investment properties could be around $1 million, with debt extinction close to $1 million, amortization expenses for shared compensation expenses of $12 million, and non-monetary ground rent and linear rental expense of -$3 million. Finally, FFO attributable to common shares and unit holders would stand not far from $197 million.

{kind=link}

My DCF model includes a WACC of 6%-10% with an exit multiple of about 8x-13x, which implies a valuation without debt of $1.901-$2.982 billion, with a median of $2.385 billion, and a maximum of $2.982 billion.

Source: DCF Model

I also predict that the implicit will range between $17 and $26, with a median of $21, and a maximum of $26. My results also included an internal rate of return between 4.86% and 17.09% and a median IRR of 10.33%.

Source: DCF Model

Competitors

Xenia apparently faces intense competition in the American hotel industry, competing with other hotels and alternative accommodation options. Factors such as room rates, quality, services, location, and brand affiliation are determining factors. Competition, specific to individual markets, includes new, existing hotels and short-term rental options. Affiliation with leading brands confers competitive advantages, but increased competition could negatively affect occupancy and revenue, and may require additional investments.

Additionally, competition for hotel acquisitions comes from various competitors with greater financial resources and market knowledge, which could impact investment opportunities and acquisition terms.

Risks

In my opinion, the company faces significant risks related to global and regional economic conditions. The luxury and high-end hotel portfolio is sensitive to factors such as economic growth, recession, unemployment, consumer confidence, and disruptive global events.

During adverse economic periods, the preference for cheaper options may negatively affect bookings and revenues. Reliance on multiple distribution channels, such as online travel intermediaries, presents risks of higher commissions and loss of brand loyalty.

My Opinion

With hotels acquired during the last two decades, right now, Xenia appears to be selling those assets that are underperforming. As a result, the FFO/net sales will most likely increase as the occupancy rate trends higher. I believe that higher profitability would most likely lead to a higher Price/FFO ratio. The financial position, with well-structured debt and varied terms, reflects a prudent approach, however there are some risks related to the total amount of debt. Besides, if Xenia fails to sell hotels at a decent price, the FFO may also diminish. With that all being said, I believe that the company appears significantly undervalued.

For further details see:

Xenia Hotels: Occupancy Rate Increases As Divestitures Continue