XERS - Xeris Biopharma Holdings: On Track To Be Cash Flow Positive

2023-09-14 21:41:10 ET

Summary

- Xeris Biopharma Holdings Inc. is making strong progress on the top line and is on track to achieve a positive cash flow breakeven point in 2023.

- The company holds a substantial number of patents globally, contributing to its success in the pharmaceutical industry.

- Xeris Pharmaceuticals' notable product, Gvoke, has experienced significant market share expansion, providing reassurance for potential investors.

Investment Rundown

The biopharma space is full of interesting companies, but perhaps a lot of risky investments as well. One has to be able to handle a lot of volatility to get exposure to the industry. Xeris Biopharma Holdings Inc ( XERS ) has been such a company for me as the last write-up I had on it has only netted me a negative return. The share price has decreased by around 24% since then but the company continues to make strong progress in my opinion on the top line and is on track to achieve a positive cash flow breakeven point in 2023.

XERS has been very active in trying to get a lot of patents in the pipeline and initiative opportunities in different markets to drive growth and deliver appealing investor returns as well. With revenues growing by 50% YoY and the first positive EPS expected to come in 2026, I think that XERS is a long-term addition to a portfolio. I still like the business and the rapid expansion they are having is intriguing, this means that I am reiterating my buy rating for it.

Company Segments

XERS holds a substantial portfolio of 171 patents on a global scale, with 32 of them already issued in the United States. Furthermore, the company has an additional 112 patents pending approval on a global scale. This proactive and aggressive approach to securing their intellectual property rights is proving to be a strategic advantage for XERS and contributes to its overall success in the pharmaceutical industry.

{kind=link}

Company Overview (Investor Presentation)

XERS is a biopharmaceutical company based in Illinois, focused on the development and commercialization of innovative therapies for niche markets. Among its notable products, the company has successfully brought Gvoke to market—a ready-to-use, liquid-stable glucagon designed to address severe hypoglycemia. Additionally, Xeris is actively involved in the promotion of Keveyis, a therapy specifically tailored for the treatment of hyperkalemic conditions.

Markets They Are In

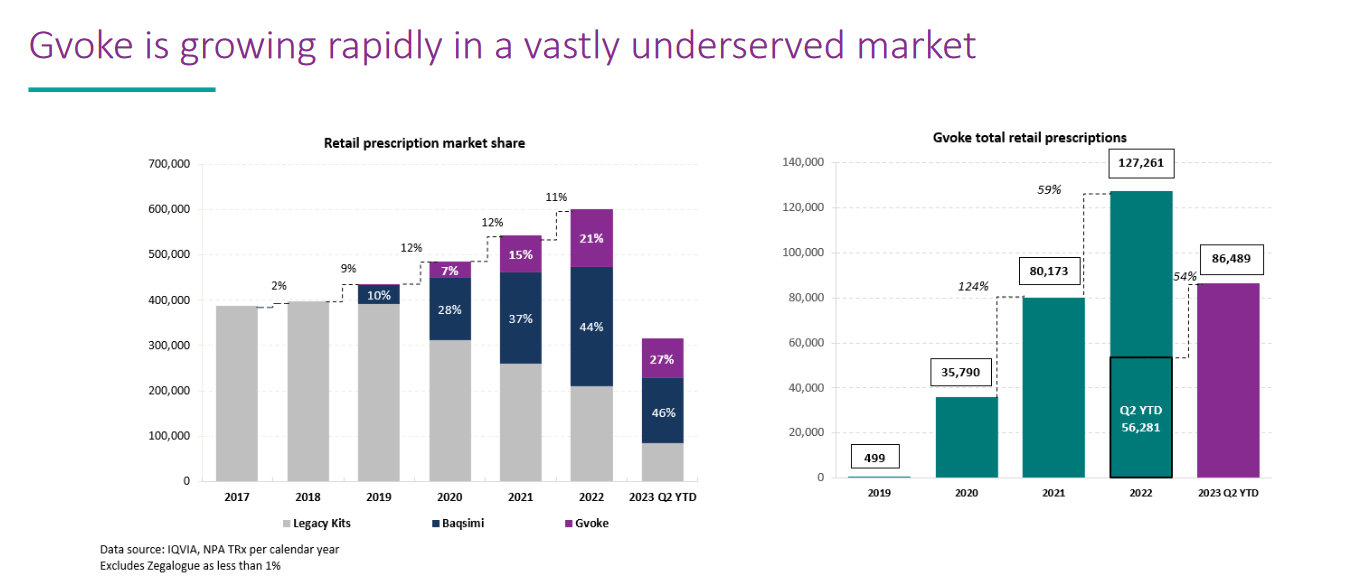

Among Xeris Pharmaceuticals' notable products is Gvoke, which is very appealing as the market size is expanding noticeably, and so is the market share for XERS's product. Gvoke's market share has experienced substantial growth, currently standing at 27%, a significant leap from 7% in 2020. This remarkable development provides strong reassurance for potential investors in the company.

{kind=link}

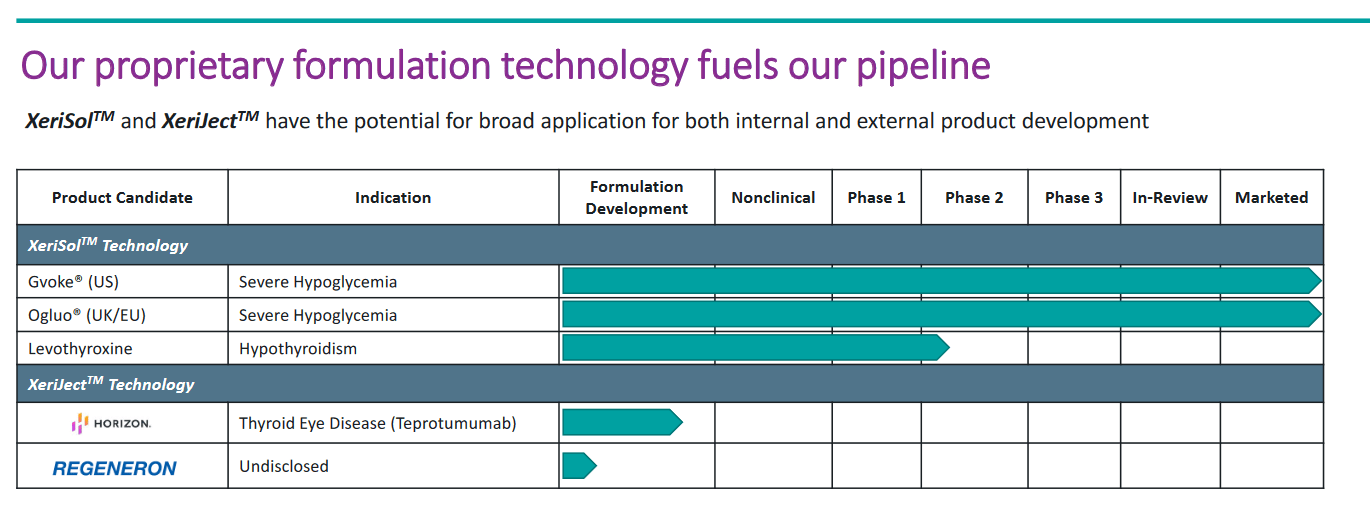

Pipeline (Investor Presentation)

The expanding market share (Page 12) not only signifies increased revenues year-over-year but also underscores XERS' progress, with Q2 alone yielding $15.6 million in revenue (Page 13). This growth trajectory suggests the company is on track to achieve $60 million in revenues from Gvoke for 2023. This remarkable growth is primarily driven by heightened awareness and adoption of the product, as highlighted by the company.

Earnings Highlights

As I mentioned earlier, the growth for XERS has been very impressive over the years and I continue to have a high conviction that the company will be able to achieve a strong EPS result eventually.

{kind=link}

Earnings Results (Investor Presentation)

The last quarterly result ended with the management of XERS tightening the guidance on the lower end and expecting it to come in between $145 - $165 million for 2023 in total. If they achieve the higher end of that estimate it would represent a YoY growth rate of 50%. The cash position is also expected to be slightly higher than previously anticipated, which I think is great news as the net incomes are positive, XERS is forced to dilute shares to raise capital for debt and maintain operations. That is putting some downward pressure on the share price, but should eventually blow over I think in the long term as margins improve.

{kind=link}

Gvoke Growth (Investor Presentation)

As mentioned before, one of the appealing factors of XERS continues to be the rapidly growing market share for some of its products, most notably Gvoke. The market share for Gvoke right now is 27% YTD in 2023, a strong improvement from 21% in 2022. YTD comparisons for the Gvoke total retail prescriptions are up 54%. If XERS can continue to maintain this momentum they will be able to drive significant earnings growth from these markets in my opinion.

Looking at the p/s for XERS it's at an over 50% discount to the rest of the sector right now which I think indicates a very solid entry point for investors interested in the biopharma space. I think a fair p/s for XERS is something along the lines of 2, which indicates a pretty immediate upside potential as the current multiple is 1.83 on an FWD basis. I think basing any investment on the forward prospects is the only way to go and I think a fair FWD p/s for XERS is 2. The industry that XERS is in has a p/s of 3.87 on a FWD basis. With a near 50% discount to the rest of the sector, it leaves a good amount of margin of safety but also some immediate upside potential as XERS trades below it. As for the p/e that I would be willing to pay, something along the lines of 15 I think is fair. Estimates suggests 2026 will result in EPS of $0.2 and with the current share price a p/e of around 10. By 2026 that leaves an upside of 50% based on earnings estimates that I think will come true if XERS just keeps up their market share expansion. By 2026 that would result in an annual growth rate of around 16% at least. Why I think XERS could have a 15x earnings multiple comes from the growth aspect of it. Higher growing companies get a higher p/e in most cases.

Risks

Investing in XERS comes with the primary risk of the company not yet being profitable. This introduces uncertainty for investors, as the company lacks a solid foundation of fundamentals to rely on for valuation. Instead, XERS' valuation hinges on its future growth prospects, which appear promising. With the impressive revenue growth and cost-saving measures that XERS is implementing, achieving a positive net income by 2026 seems highly feasible. While this profitability timeline may present some risk, it is offset by the company's potential for substantial growth and success shortly.

Bottom Line (Seeking Alpha)

Final Words

XERS has been able to keep up the momentum from previous quarters and the last report showcased strong revenue growth and tighter guidance for 2023. XERS is yet to achieve a positive net income, but that doesn't worry me as the sheer amount of market share they are gathering up will be converted and leveraged into better earnings in my opinion in some time. The p/s for the company is at an over 50% discount to the rest of the sector, which I find to be a very fair point to get in at. I have covered the company before, and I am reiterating my buy rating for it.

For further details see:

Xeris Biopharma Holdings: On Track To Be Cash Flow Positive