XERS - Xeris Biopharma: Picks And Shovels Play Has Long-Term Growth Potential

2023-03-28 06:24:51 ET

Summary

- Shares have lost over half their value during the past year.

- Commercial momentum appears to be building with management guiding for break-even cash flow by the end of 2023.

- Keveyis is facing generic competition in PPP and Recorlev is still in the early innings of launch for Cushing's disease.

- Long patient acquisition cycle for its rare disease drugs could delay profitability and the company has yet to iron out concrete deal terms for XeriJect/XeriSol Technologies.

- XERS is a Buy. A prudent strategy is to make a pilot purchase, then wait for confirmation of the thesis via news flow and quarterly updates before filling out the position.

Shares of Xeris Biopharma ( XERS ) have lost over half their value during the previous twelve months. 18% loss over the last three years does not inspire confidence either.

Nevertheless, I decided that a deeper dive into this unique story was merited given diversified revenue basis (three commercial assets), rare disease-focused infrastructure and value proposition underlying Xerisol & Xeriject drug delivery technologies.

Additionally, ROTY Biotech Community member Osmium.Research, whom I credit for keying me on to TransMedics ( TMDX ) early on, provided helpful commentary on the merits of Xeris' delivery technology. He noted that it's designed to address limitations of aqueous formulations for certain drugs, solving an old problem with a new approach. Chemists often struggle to develop a dosage form for a drug that has limited solubility in water (need to administer it and then needs to be absorbed). Osmium made a comparison to Halozyme Therapeutics ( HALO ), which incorporates an enzyme to allow large biomolecules (typically antibodies) to be given with an injection instead of a 2-4-hour infusion. HALO takes a small piece of huge revenue streams and has created a real moat for itself. The conclusion, with the usual caveats, is that Xeris' platform could have a significant advantage and its approach using non-aqueous matrix should be made widely available.

Given the above, let's take a closer look at this one to determine if it has potential for inclusion in our Core Biotech (commercial-stage) portfolio.

Chart

{kind=link}

Figure 1: XERS weekly chart

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, we can see share price as high as $8 at the height of the biotech bubble in early 2021. In March of that year, the company ran a $27M private placement at $4.12/share (led by then key fund Deerfield Management). 2 months later, Xeris announced acquisition of Strongbridge Biopharma for $267M to get its hands on lead rare disease drugs Keveyis and Recorlev. From there, share price steadily declined to present lows in the $1.30 range. My initial take is that long-term investors with medium-level risk tolerance (who are interested in the name) would do well to purchase a pilot position and then only add exposure as quarterly updates confirm that a turnaround indeed is taking place.

Overview

Founded in 2005 with headquarters in Illinois (355 employees), Xeris Biopharma currently sports enterprise value of ~$200M and Q4 cash position of $122M providing them operational runway beyond Q4 of this year where management projects they'll achieve breakeven cash flow.

Keep in mind there are ~136M shares outstanding and $138M debt (term loan and convertible notes). Accumulated deficit to date is $554M, which seems on the high side and perhaps speaks to management's poor stewardship of resources in the past.

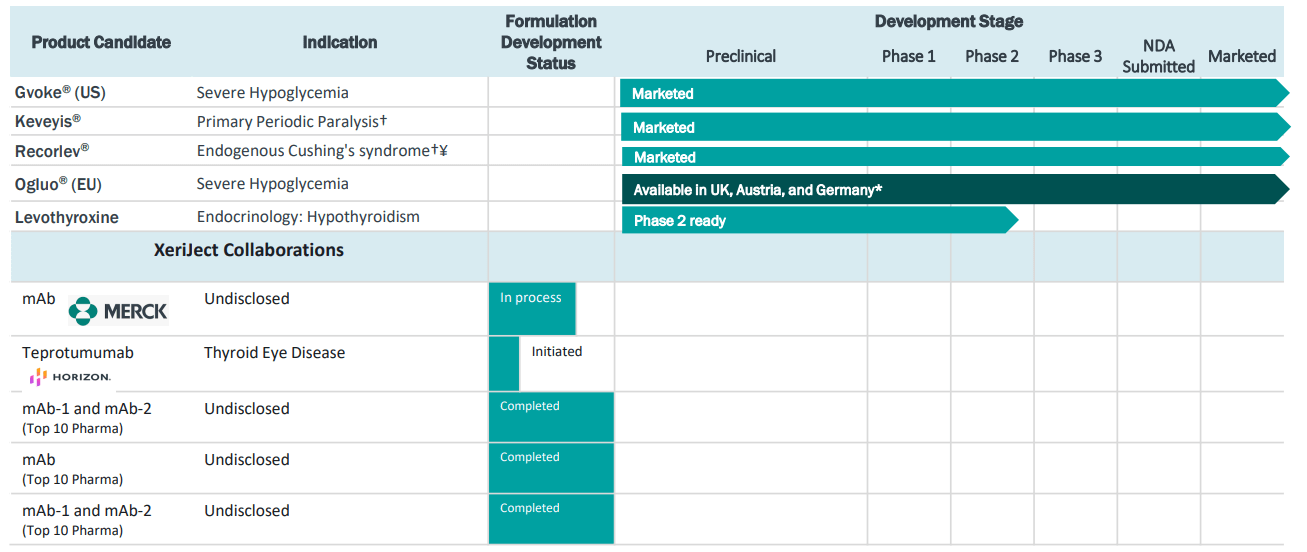

Xeris is a rather unique company in that it has a diversified revenue base consisting of 3 commercial products, one addressing a larger market and the latter two in the rare disease category. The other part of the business comes from its proprietary formulation science (Xerisol and XeriJect) to generate partnerships as well as utilize with internal assets.

{kind=link}

Figure 2: Pipeline

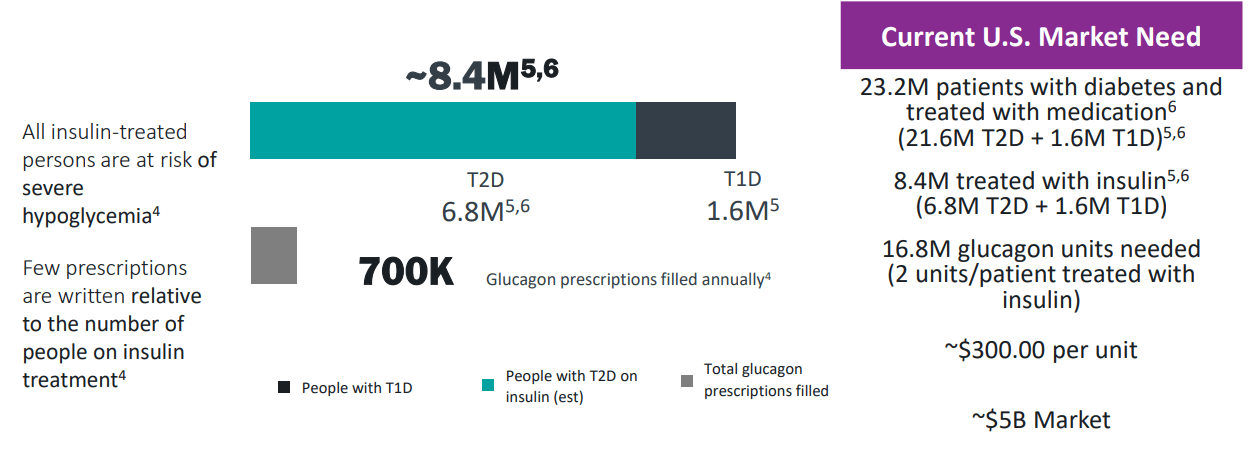

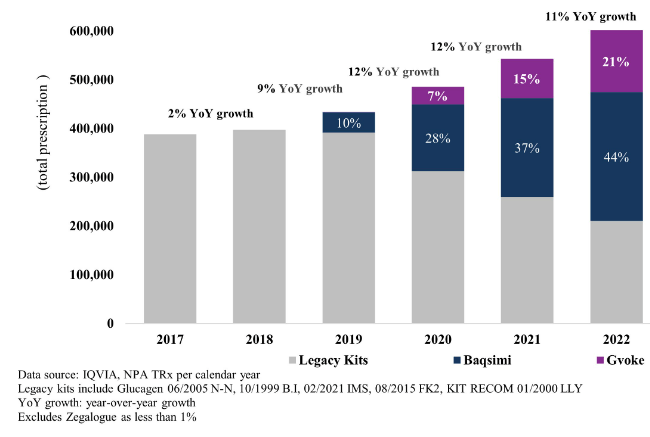

Starting with Gvoke, this is a ready-to-use, liquid-stable glucagon for the treatment of severe hypoglycemia. It is indicated for use in pediatric and adult patients with diabetes (ages 2 years and above) and is incredibly easy to use (2-step process, no dose calibration required). Essentially, much like how people facing life-threatening allergic reactions keep an EpiPen around, Gvoke and its competitors serve to address low blood sugar emergencies for diabetics. Per the company, total addressable market opportunity is $5B in the US and growing due to prevalence of diabetes and health trends in our society today. Awareness and urgency for ready-to-use glucagon is quite low relative to something like EpiPen, and Gvoke competes with Eli Lilly's ( LLY ) ready-to-use Baqsimi (nasally administered glucagon powder). Gvoke had nearly 25% market share as of year-end 2022 and generated a quarter million prescriptions since launch.

{kind=link}

Figure 3: Gvoke market opportunity

{kind=link}

Figure 4: Total prescriptions by Glucagon Rescue Product for retail market only

One last fact here to support my previous statements is that roughly half of the approximately 30M people with diabetes in the United States should have handy ready-to-use rescue glucagon, while current prescription volumes suggest that fewer than 1M of them do.

Moving on to Keveyis is the first of two rare disease drugs that came from the Strongbridge Biopharma acquisition in 2021. Keveyis is approved to treat hyperkalemic, hypokalemic, and related variants of Primary Periodic Paralysis ((PPP)). PPP is a rare genetic, neuromuscular disorder that can cause extreme muscle weakness and/or paralysis- some forms are commonly associated with myotonia or muscle stiffness. There are an estimated 4,000 to 5,000 people affected by PPP in the US and number of patients prescribed Keveyis therapy has steadily grown since its introduction in 2017. On the downside, a generic competitor was approved year end 2022. However, since patient identification and capture is extremely difficult and time-consuming, the company might not be as adversely affected as is typically expected (at least at the outset of generic launch).

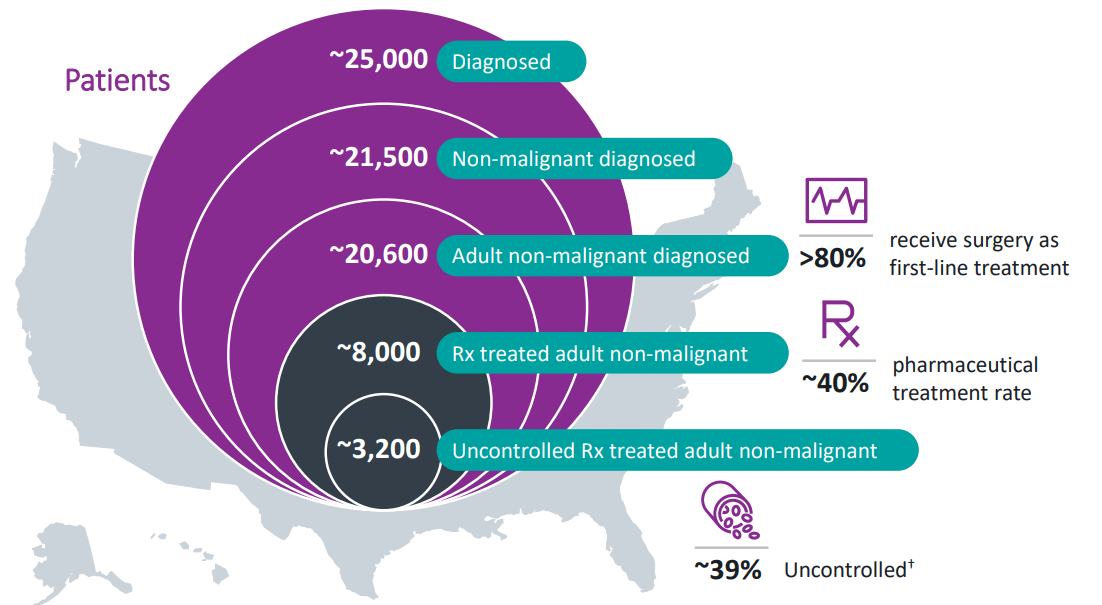

As for Recorlev, it is a cortisol synthesis inhibitor approved for the treatment of endogenous hypercortisolemia in adult patients with Cushing's syndrome for whom surgery is not an option or has not been curative. The condition is potentially fatal (caused by chronic elevated cortisol exposure) and addressable market is $3B in the US. For context, competitor Corcept Therapeutics ( CORT ) sports a $2.2B market capitalization and Korlym is on track to do $430M-$450M of revenue for 2023. Recorlev

{kind=link}

Figure 5: 8,000 Rx-treated Cushing's patients in the US, of whom 40% are not normalizing cortisol

Moving on to XP-8121 (levothyroxine), this clinical-stage candidate addresses a large opportunity but is ~5 years from market (entering dose-finding phase 2 followed by FDA discussion before pivotal trials). XP-8121 is intended as a maintenance therapy in patients with congenital or acquired hypothyroidism who require continuous thyroid hormone replacement. Goal of therapy is restoration of the euthyroid state which can reverse the clinical manifestations of hypothyroidism and significantly improve quality of life. Treatment of choice today is oral administration of levothyroxine, one of the most widely prescribed drug products in the US. Unfortunately, nearly 40% of patients being treated with oral levothyroxine are either over-or-under-treated due to drug formulation, use with food, adherence, use of concomitant medications and pre-existing medical conditions. Many patients simply fail to reach target thyroid stimulating hormone ((TSH)) levels and thus are given a higher dose. The problem is that the oral drug has a narrow therapeutic index and so small deviations from proper dose can cause clinically meaningful shift in pharmacological effects (titration of oral drug is an incremental process).

Corporate Slides

Figure 6: Market opportunity for subQ levothyroxine therapy

The thinking is that subcutaneous administration via XP-8121 would mitigate many of these challenges with its sustained plasma exposure profile and similar Cmax (allowing for weekly dosing, also bypassing the adverse GI events). It appears there is already some derisking here, as phase 1 data showed slower absorption, lower peak plasma and higher extended exposure as compared to Synthroid PO at comparable 600 ?g dose (suggested dose conversion factor of 4x). There are estimated 20 million people in the US affected by hypothyroidism and for the last 100 years oral levothyroxine has been the only available option (more than 100M prescriptions currently written annually).

As mentioned prior, Xerisol and Xeriject technologies can be utilized to create ready-to-use, room-temperature stable, highly concentrated, injectable formulations of both small and large molecules. These in turn enable subcutaneous or intramuscular administration as opposed to IV infusion, providing the benefits of convenience, cost-effective storage and improved experience for both patients and caregivers. As you can imagine, applications for such technology are very broad and theoretically many partnerships could come from this (where Xeris benefits via milestones and royalties for reformulating blockbuster IV drugs).

Select Recent Developments

In November, the company announced that the European Journal of Endocrinology (EJE) published the extended evaluation ((EE)) results of the SONICS study (NCT01838551) evaluating longer-term effects of levoketoconazole on cortisol levels, biomarkers of Cushing's syndrome ((CS)) comorbidities, clinical signs and symptoms of CS, and quality of life. One key takeaway was that by month 6, 61% of patients (33/54 with data) exhibited normal mean urinary free cortisol (mUFC). At Months 9 and 12, 55% (27/49) and 41% (18/44) of patients with data had normal mUFC. Also, improvements were observed across a variety of measures at Months 9 and 12 including mean fasting glucose, total and LDL-cholesterol, body weight, body mass index, abdominal girth, Cushing QoL, and BDI-II scores. Discontinuation rate during EE was just 6.7%, with most common adverse events including arthralgia, headache, hypokalemia, and QT prolongation. Importantly, no patient experienced ALT or AST >3x ULN, QTcF interval >460 msec, or adrenal insufficiency during EE.

Also in November, Xeris entered into research collaboration and option agreement with Horizon Therapeutics ( HZNP ) to utilize XeriJect to develop a subcutaneous formulation of teprotumumab (Tepezza). Specific financial terms were not disclosed, making an estimate of the deal's value quite difficult. Xeris would be due development, regulatory and sales-based milestones as one would expect (along with royalties on future sales).

The next month, Xeris announced feedback from a Type C meeting with the FDA which in turn prepared the way to proceed with a phase 2 study for subcutaneous levothyroxine sodium injection as a replacement therapy for hypothyroidism. Data is expected 2H 23 and would in turn facilitate a future phase 3 program. Prior phase 1 data showed that subjects receiving XP-8121 SC have slower absorption, lower peak plasma, and higher extended exposure compared to Synthroid PO at the comparable dose of 600 ?g. In addition, exposure was proportional over the range of ascending XP-8121 doses and simulations suggested that exposure from weekly XP-8121 1200 ?g SC doses overlaps daily Synthroid PO 300 ?g (dose conversion factor of 4x). All doses were safe and well tolerated.

In January the company updated its full year 2022 outlook with expectations of net product revenue in the top range ($105M to $110M). Year-end 2023 cash balance was projected at $110M to $120M (also higher than previously projected). Management credited this to strong patient demand for Recorlev and Keveyis along with greater prescription growth for Gvoke. Also in Q4, the company drew down the final $50M tranche in its Hayfin debt facility and received upfront payment from the Horizon Therapeutics collaboration and option agreement.

Other Information

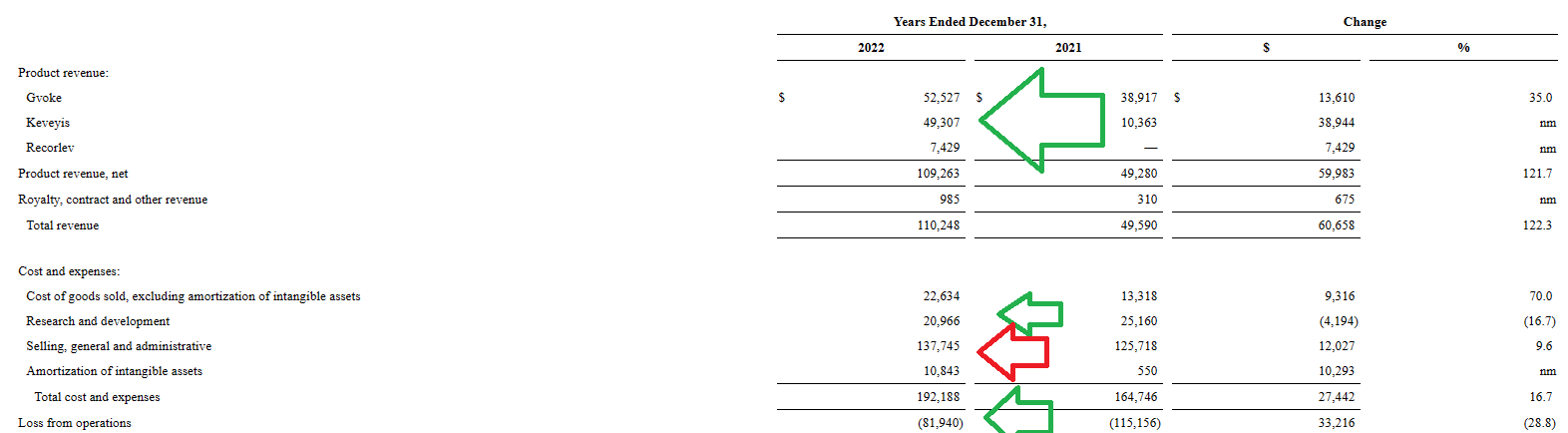

For the fourth quarter of 2022 , the company reported cash and equivalents of $122M as compared to net loss of $12.9M. SG&A decreased by $19.8M for the quarter, while R&D expenses came down by $5.1M. Management is guiding for cash utilization from operating activities of $57M to $77M for full year 2023, with combined revenues (from Gvoke, Keveyis, Recorlev and other) of $135M to $165M. Projected YE cash position is $45M to $65M with break-even cash flow by Q4 (sounds overly optimistic to me, but certainly possible). To my eyes, leadership would be wise to access one final financing to get them over the hump to profitability (especially in currently volatile environment for markets and biotech).

{kind=link}

Figure 7: Product revenues on the rise, while expenses and loss from operations steadily fall

Here are a few nuggets from the quarterly call :

- CEO Paul Edick highlights progress with Gvoke upon attaining 28% share of new prescriptions in the glucagon market. Ready to use products now represent nearly 75% of total new prescription market for rescue glucagon (still over 7 million people who remain at high risk and don't have RTU Gvoke available, just in case).

- Keveyis continues to impress with 33% quarterly growth for Q4 and no negative impact from first generic entry (so far). The interesting dynamic of PPP market also adds to my optimism here, as it's quite challenging and requires a lot of work to identify patients and get them on therapy. The fact that Xeris continues to invest in Keveyis also reinforces the possibility that growth runway in the near to medium term is still possible.

- Recorlev recorded 51% growth over Q3 (generating $3.8M). Total 2022 revenue for the drug was $7.4M and that's only included 3 quarters of patient referrals and initiations with minimal dose titration (in-line with expectations). I continue to believe there's potentially a high ceiling here for ultimate growth, but it will involve a steady increase in number of patients started on therapy over time. Also, those new to therapy will slowly be titrated up to their average daily dose.

Moving onto the presentation at SVB Leerink , here are a few incremental nuggets:

- Keveyis is addressing 4,000 to 5,000 PPP patients in the US. Every patient is different in terms of trigger for these spontaneous paralytic attacks that last hours to days. They are often unrecognized by practitioners or physicians, but an algorithm has been developed to identify these patients (company then contacts physician office, who in turn make the identification and bring them in for testing and analysis, which can be a very long process). Once the patient is on therapy, the company surrounds them with care connections, patient managers, mentors, etc to get them on therapy, stabilized, work through dosing, titration, early side effects BUT then the reduction in paralytic episodes is dramatic. Growth is going very well at 42% CAGR and no impact on business so far from generic approval.

- As for Recorlev, Cushing's syndrome is all about the overproduction of cortisol and the goal for patients is normalization of cortisol levels (what Recorlev does with a relatively modest adverse event profile). Compared to other drugs in its category, management thinks that over time it will become the preferred option (small universe of patients). Their target is 8k prescription drug-treated population that represents a multibillion-dollar opportunity. On the con side, in the short term they are getting just the patients that are uncontrolled, not stable, cortisol not being normalized. Over time they expect to get a broader cross section of patients (there is a longer acquisition cycle to get them on therapy and then titrated properly).

- Regarding Xeriject and Xerisol technologies, they have a number of collaborations ongoing including 3 large pharma companies that have completed formulation work (a matter of whether they decide to move their asset forward with Xeris' tech). Merck collaboration is progressing well with a number of optimizations on formulation and IND-enabling studies left to do. For Horizon Pharma, the goal is to take Tepezza and turn into a prefilled syringe in 15 second injection (dramatic change). Keep in mind this drug alone represents a $3 billion franchise which currently is 100% IV infusions. I thought it a bold statement that says a lot when management remarked said " Any monoclonal antibody or large molecule someone has given us, we've been able to formulate successfully". Each program is different, one undisclosed asset took 4 months to optimize and others can take much longer (ie. up to 14 months). Unfortunately, there's no defined timeline here.

- For Recorlev, while it's true that Cushing's is a crowded market, management notes that it's also a highly unsatisfied market. Lots of products out there are not doing the job and one has high androgenic side effects. Korlym does not normalize cortisol yet sells quite a bit (doing over $400M annually). Doctors are happy with Korlym because patients feel good on it. In the short-term, Recorlev is getting the "train wrecks", the patients who tried everything that doesn't work for them and cortisol is not normalized. Recorlev actually normalizes cortisol levels and provides an opportunity for patients to do better than Korlym. Over time, the drug will also take share from others that have greater side effects (progress will take time ).

Moving on, I would be remiss to not at least delve a bit more into the levothyroxine/XP-8121 opportunity. Here are a few notes from phase 1 topline results' webcast :

- Over 105M prescriptions dispensed of oral levothyroxine annually. It seems like compliance is a significant issue here given high % of patients who either have comorbid GI condition impacting oral absorption or another medication interfering with the drug. At the end of the day, if you only take 7% of that 105M prescription market you end up with 62M weekly doses per year at average prescription size and price ($2 billion to $3 billion opportunity). XP-8121 would be the first injectable levothhyroxine for these patients, would bypass GI tract and improve regimen compliance with once-weekly administration. Small volume, Ready to Use, room temperature-stable, subQ injection would be a significant advantage for patients.

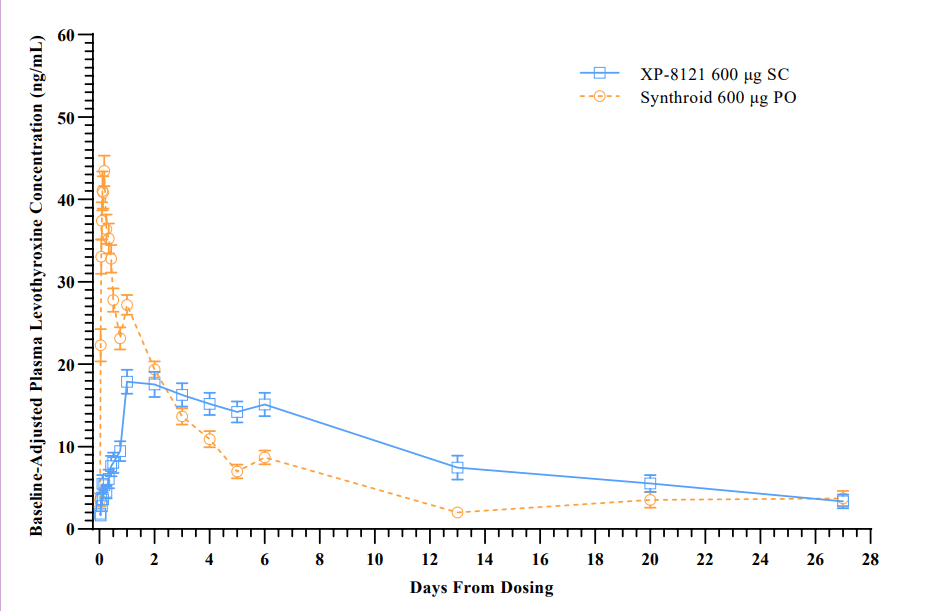

- XP-8121 data over 28 days for 600 microgram doses (versus oral Synthroid). The latter has rapid rise followed by rapid decline (Tmax of 3 hours and Cmax of 48). In comparison, blue line (8121) has more prolonged Tmax of 48 hours, about half the Cmax at 22. Comparing AUCs, we see about 35% more exposure for subQ in later portion of data collection (blue line above orange line at later timepoints).

{kind=link}

Figure 8: Single dose administration comparison of 8121 to Synthroid oral

- Dose proportionality was observed at 1200 and 1500 microgram doses. Safety assessment showed typical adverse events (no difference between any of the groups, all mild to moderate and transient). Simulation of chronic dosing (5 weeks oral therapy at 300 micrograms) resulted in cumulative AUC that was comparable to 1100 to 1200 single once-weekly microgram dose of XP-8121. Best fit was 1200 for conversion factor of 4x and confidence is higher that they are in the right dosing range.

- Idea farther out could be to do a staged phase 2 into a phase 3 program. Phase 2 is to do confirmation of what was previously observed in PK model (conversion factor of 4x or close to it). Devil's advocate from analyst question is that lower Cmax and lower time to Tmax than oral could correlate to slight differences in efficacy for patients. Management, however, notes that the steady state situation is what they are trying to accomplish (chronic replacement therapy). If they can get a comparable AUC (and Cmax is a little lower and Tmax a little later), it's still fine.

Switching gears back to Recorlev, I would like to remind readers of the crowded nature of the marketplace (Signifor, Isturia, ketoconazole, metyrapone, cabergoline, mitotane and etomidate used off-label). It doesn't stop there, as there are quite a few products in development for Cushing's syndrome as well (Corcept's recorilant in phase 3, AstraZeneca's 11BHSD1 inhibitor AZD-4071 in phase 2, Sparrow Pharmaceutical's HSD-1 inhibitor SPI-62 in phase 2 and assorted programs in phase 1 including SST5 agonist from Sosei Heptares and ROTY holding Crinetic's ACTH antagonist CRN04894). Also, keep in mind that Recorlev has a black box label for QT prolongation and hepatotoxicity (perhaps a limiting factor in its uptake).

As for manufacturing, the company uses third parties (contract manufacturing organizations or CMOs) in order to maximize cost-efficiency. The downside to this is having less control versus what in-house facility could provide. Additionally, the have no plans to build internal capabilities (I like this because they can keep costs low and focus on their bread and butter, building out royalty streams via Xerisol and Xeriject technologies in a manner similar to Halozyme). I am a bit concerned about the auto-injector used to deliver drug product in Gvoke being sub-assembled in Taiwan before final assembly in Florida (in the event of China invasion, could disrupt the supply chain here). Recorlev is the sole source of Recorlev, but it is a larger more reliable company I'm familiar. Resurgence of a global pandemic or similar situations would put pressure on supply chain partners ability to manufacture Xeris' products (would become lower priority).

As for institutional investors of note , I don't see much in the way of familiar funds here but Stonepine Capital Management does own an 8% stake. Generalist funds Vanguard and BlackRock own 6.5M and 8.5M shares, respectively. Moving on to insiders , I'm actually encouraged to see a lack of selling over the past couple years (a rarity in biotech) and a few sizeable purchases (including COO John Shannon buying $200k worth in late 2021). CEO Paul Edick bought $416,000 worth in late 2021 and another $140k worth in mid 2022.

As for relevant leadership experience, Chairman and CEO Paul Edick served prior as CEO of Durata Therapeutics (acquired by Actavis for $675M). President and Chief Operating Officer John Shannon spent 2 years as CEO of Catheter Connections (bought out by Merit Medical), 3 years as Chief Commercial Officer at Durata Therapeutics and 10 years at Baxter Healthcare (led growth of billion-dollar brands Advate and Gammagard). CFO Steve Pieper served prior as CFO at (you guessed it) Catheter Connections and held Director of Finance position at Durata Therapeutics. The fact that several members of management experienced success together at previous ventures is a green flag in my book.

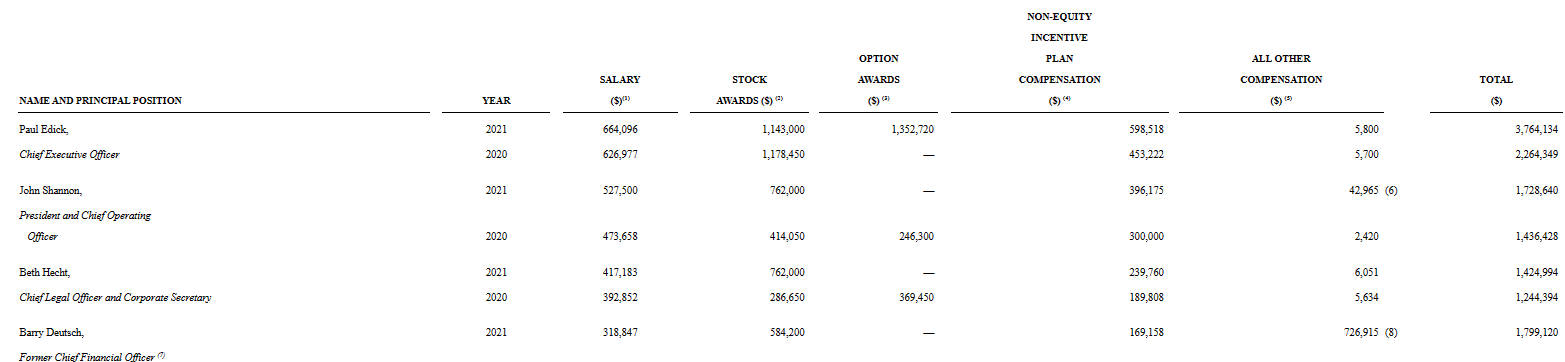

Moving on to executive compensation, cash portion of salary does appear on the high side including $664k for CEO. Conversely, level of stock and options awards is more than reasonable (on the low end, to my eyes).

{kind=link}

Figure 9: Executive Compensation Table

The important thing is to avoid companies where the management team is potentially in it for self-enrichment instead of creating value for shareholders, and looking at compensation is one of several indicators in that regard.

Moving onto useful nuggets from members of the ROTY community, post Q4 update TDMInvest stated that it looks like management is starting to run a business with SG&A down considerably from very high prior spending. They added $100M to debt (puts them at $187M) and he was encouraged to see Q4 loss down to just $12.9M (a major improvement).

On the other hand, Ravid shared that he's quite skeptical of the opportunity in hypothyroidism as he takes Levoxyl (simple administration, thyroid tests readily available via bloodwork to narrow down the dosage level that applies to you). It's supposed to be taken on an empty stomach in the morning before eating any meals, thus Ravid thinks simple compliance here versus a weekly injection to be laughable.

While this is far from an apples-to-apples comparison, a look at enterprise value gap between Halozyme Therapeutics and Xeris shows the kind of potential the latter is capable of should it get its act together, ink several big pharma collaborations and deliver on them.

Figure 10: Enterprise value comparison

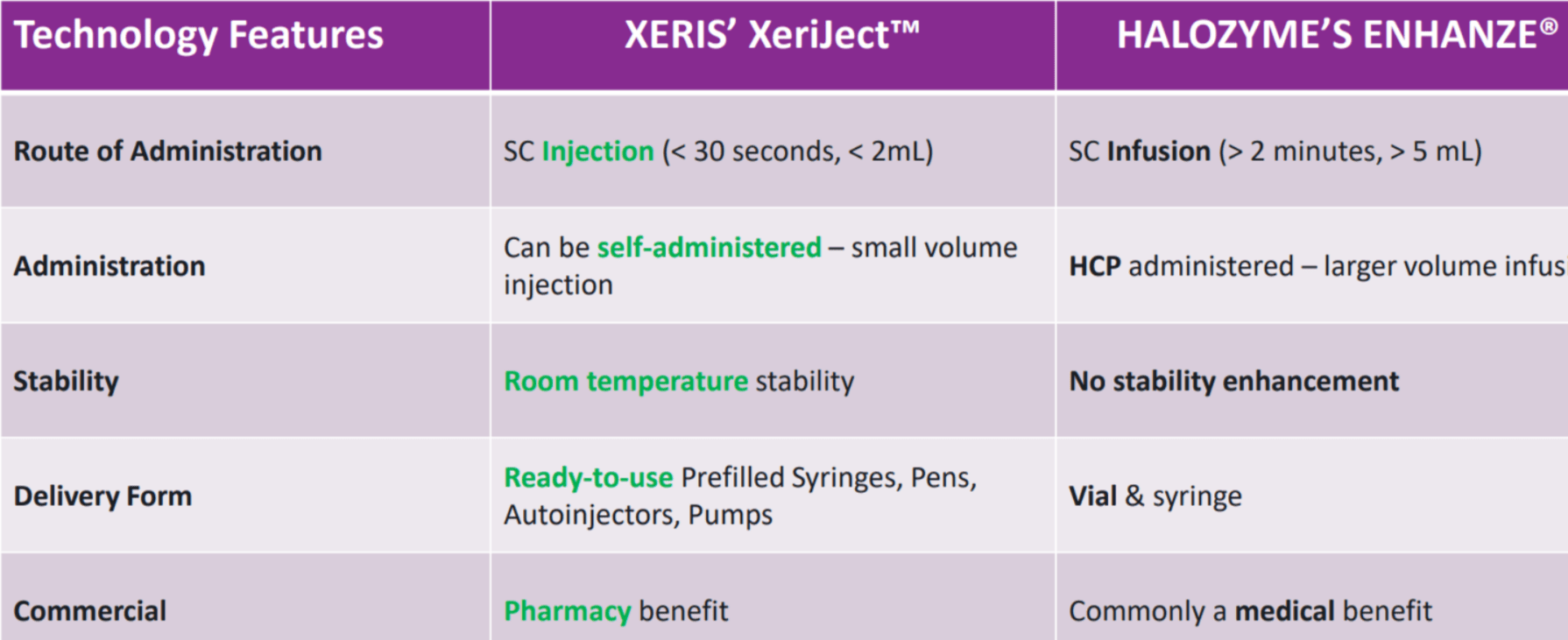

Halozyme's primary business model is receiving royalties from ENHANZ technology collaborators (converting from IV to convenient subcutaneous delivery). A comparison of the two companies' technologies reveals that XeriJect has some noteworthy advantages that could translate into long term success for the company as well as taking share from its larger competitor.

{kind=link}

Figure 11: Comparison of XeriJect to ENHANZ

As for IP, Xeris currently owns 176 patents issued globally including composition of matter covering their ready-to-use glucagon formulation (expiration in 2036). They have 59 granted patents globally related to platform technologies (including 7 patents granted in the United States and listed in the United States FDA Orange Book). These also cover proprietary formulations of levoketoconazole (the active pharmaceutical ingredient in Recorlev) and the uses of such formulations in treating certain endocrine-related diseases and syndromes (expirations in 2040).

Final Thoughts

To conclude, with current enterprise value of ~$200M, Xeris looks quite interesting in terms of expected sales growth for 3 approved programs especially the multi-year acceleration expected for Gvoke and Recorlev. I originally thought that Keveyis sales would erode due to generic competition, but due to the unique nature of PPP market that might not be the case.

Conversely, I remain a bit skeptical on the levothyroxine opportunity after Ravid's remarks and also don't like the lack of visibility with their big pharma collaborations for XeriSol/XeriJect technologies (no pre-negotiated terms that I can see, makes these deals hard to value). Given the extended patient acquisition cycle in Cushing's disease, it could take longer than expected for Recorlev sales to reach numbers that are truly meaningful enough ($100M+) to affect share price and valuation.

For readers who are interested in the story and have done their due diligence, XERS is a Buy and I suggest initiating a pilot position in the near term. A prudent strategy could be to make initial purchase, then wait for successive quarterly updates to confirm that thesis is strengthening before adding more exposure.

Taking a long-term perspective (3 to 5 years), IF management can clean up the balance sheet and company makes the transition to cash flow positive and IF they can ink concrete deals with pharma for their unique technology, this small cap player could treat shareholders very well.

For our Core Biotech portfolio, I'm currently prioritizing other names with greater potential for accelerating sales growth in the near to medium term. However, I will be keeping an eye on Xeris' progress in case we enter a position later this year or next.

Key risks include balance-sheet related (another financing later this year), big pharma competition for Gvoke (Baqsimi), generic competition for Keveyis and increasingly crowded market in Cushing's disease. I still have little confidence in ultimate commercial potential for XP-8121 (levothyroxine), though the prospect of a more convenient once-weekly thyroid hormone replacement therapy is intriguing. I'm encouraged that net losses are narrowing as company does not take on the huge task of internal manufacturing (outsourcing to CMOs). The most outsized potential is in the technology collaborations with big pharma, but again the risk here is that shareholders get strung along by incremental news tidbits with absence of actual concrete deals delivered this year or next.

Author's Note: I greatly appreciate you taking the time to read my work and hope you found it useful. While I post research on many companies that interest me, in ROTY (clinical stage) and Core Biotech (commercial stage) portfolios I own just 15 or fewer names in order to focus on stories that are highest conviction for me.

For further details see:

Xeris Biopharma: Picks And Shovels Play Has Long-Term Growth Potential