XERS - Xeris Biopharma: Remarkable Market Share Expansion

2023-06-16 20:41:21 ET

Summary

- Xeris Biopharma Holdings Inc is a growing healthcare company with strong revenue growth and a solid balance sheet, making it an attractive investment option.

- XERS has a range of successful products, such as Glucagon and Gvoke, and is aggressively securing patents to stay ahead of competition.

- XERS is expected to achieve profitability soon, with a breakeven cash flow by Q4 2023, and an estimated EPS of $0.23 by 2026.

Investment Rundown

For investors seeking a solid healthcare play that is growing revenues at a strong rate while at the same time maintaining a solid balance sheet, then Xeris Biopharma Holdings Inc ( XERS ) is worth taking a look at. What first drew me to the company was the impressive revenue growth they have had over the last few years, and they seem to maintain this momentum too going into 2023.

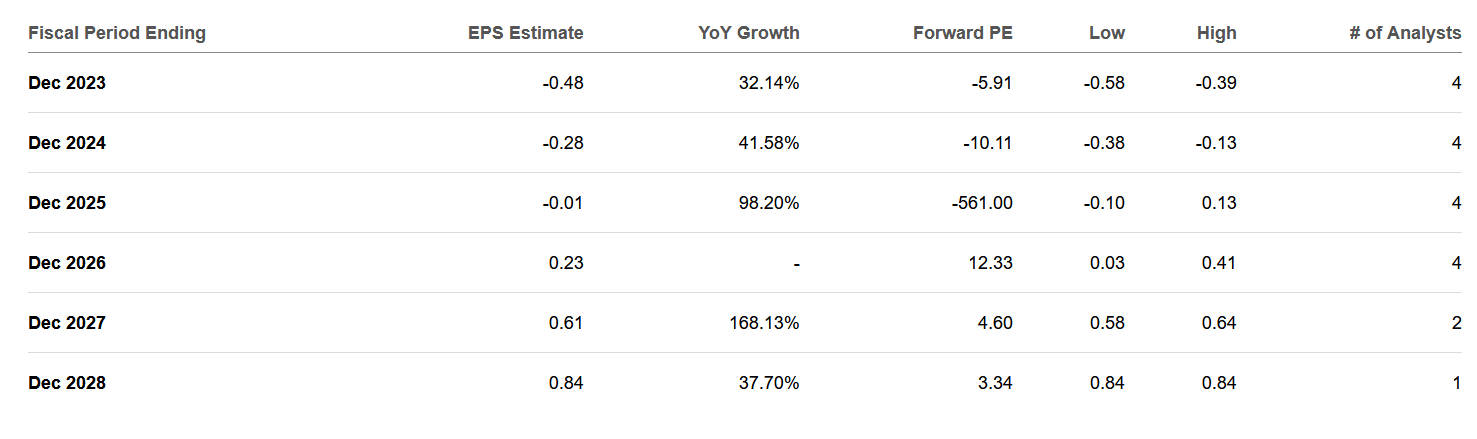

The bottom line has taken strong steps towards profitability and the last quarter had the company improvise substantially, going from negative $0.25 per share in Q1 2022, to negative $0.12 for the last quarter. I don’t think XERS is far away from achieving a positive net income, and I am all here for it. Estimates suggest an EPS of around $0.23 by 2026, which would mean an FWD p/e of 12 given the current share price. I think this is well within reach as XERS is at a strong rate taking both market share and developing new groundbreaking products, like the Glucagon. XERS is rated a buy.

Recent Developments

A recent announcement by the company is the patent they have issued for their XeriSol formulations. The strategy with XERS is to patent early and often in order to get ahead of the competition and ensure their products are theirs, and they can begin capitalizing from it and get it on the markets.

Right now, XERS has 178 patents globally, whereas 33 are issued in the US and another 128 are pending globally too. This aggressive approach to ensuring their products is playing out very well for the company.

Gvoke Growth (Investor Presentation)

{kind=link}

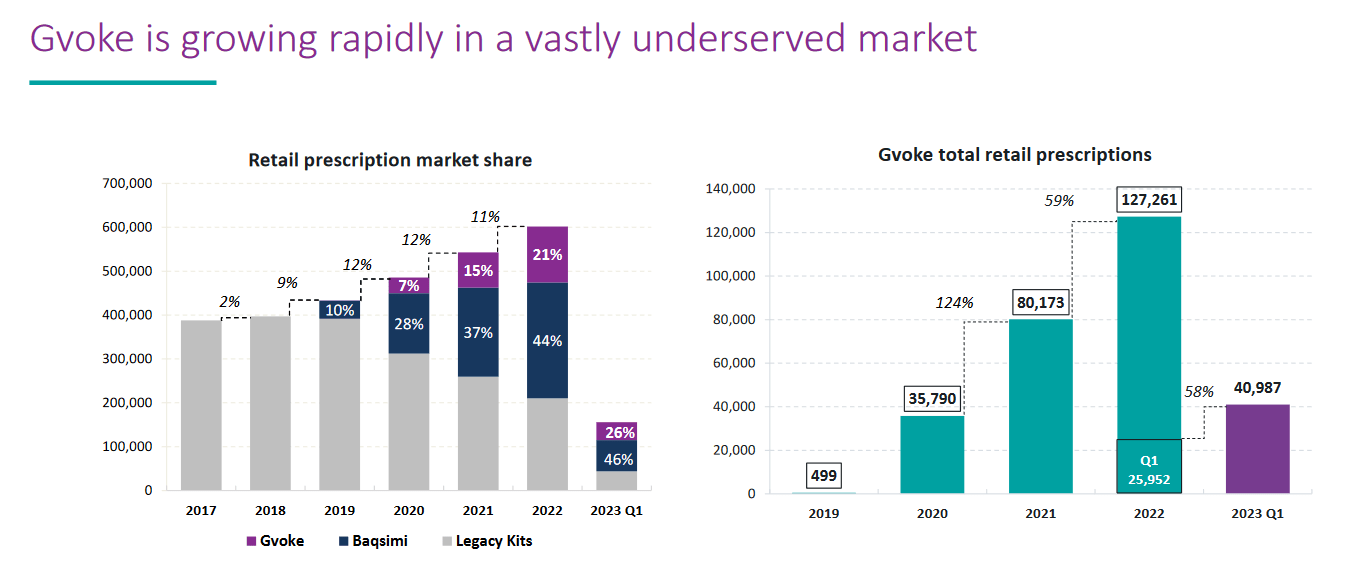

Some of the major products that XERS has is the Glucagon and the Gvoke. Gvoke is particularly interesting as they are growing their market share with this product at an impressive rate. Right now sitting at a market share of 26%, up from 7% in 2020, this development is incredibly reassuring to see for an investment case in the company. The market share growth is of course also meaning that XERS is generating more revenues YoY from it, with Q1 netting them $15 million, they are on their way to achieving $60 million in revenues from it for 2023, with growth driven by increased awareness and adoption as noted by the company.

US Market Opportunity (Investor Presentation)

Looking ahead, news regarding their developments on Oral levothyroxine will be particularly interesting, seeing as the TAM here is over $2 billion. With such a large market opportunity for XERS, it will be crucial for them to ensure patents and gain a solid foothold in the market.

Profitability Is Soon To Come

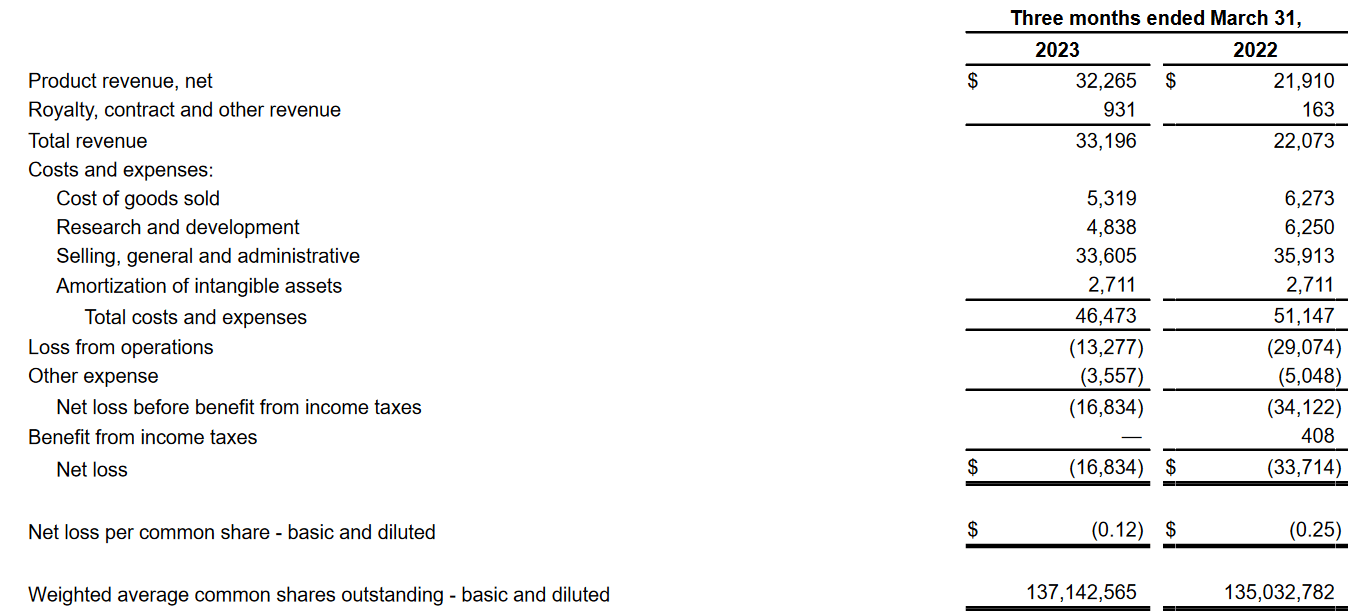

Mentioned previously was that XERS is yet to have a profitable bottom line, but the last few years have certainly pushed them in the right direction and I don’t think we are many years away now from seeing a positive bottom line. The loss for the first quarter of 2023 was $16 million, down a lot from the year prior, which was a negative $33 million instead. Many thanks to the increased revenues, the company saw an increase in the EPS, but worth noting is that the expenses the company has had also decreased on a yearly basis, indicating they are taking good measures in progressing towards profitability. The R&D costs are down 29% YoY, and the cost of goods sold is down 16%. Seeing decreases like this whilst also growing revenues is breeding optimism regarding their future.

{kind=link}

One of the major goals for 2023 is that XERS will achieve cash flow breakeven by Q4. That would be a major improvement to the financials and earnings of the company and make the future a little more clear as to what potential lies here. With a break-even cash flow, the dilution of shares should decrease and XERS can focus on building up its balance sheet and at the same time make meaningful investments into new products and patents. Much of the growth I think will come from the Recorlev improvements in the business. The revenues here grew massively on a YoY basis, from $134 000 in Q1 2022 to $4.4 million in Q1 2023. The product is approved for all etiologists of Cushing's and helps patients achieve long-term stabilization of their cortisol levels. Generating $7.4 million in 2022, Recorlev is set to help XERS grow revenues at a fast rate in 2023 and ensure they reach their target of breakeven cash flows by Q4 this year.

Risks

The most obvious risk with investing in XERS is that they aren't yet profitable. That brings a lot of risks to investors, as the company doesn't necessarily have any strong fundamentals to trade on or fall back on. Instead, the valuation is based on the future prospects of the business, which I think are very bright. Reaching a positive net income by 2026 seems very manageable given the sheer revenue growth and cost measure that XERS is putting in place.

With an estimated EPS of $0.23 by 2026 I think the current price is fair to pay given that would value XERS at a p/e of around 12 then if the share price stays the same.

Earnings Estimates (Seeking Alpha)

{kind=link}

Another risk facing the business is the reduction of costs they need to have. With the current cash position of $50 million, it means they could only support operational expenses for another 4 quarters before the operational losses would be too great. That means dilution is very much on the table to ensure the company can keep running. But with smaller companies like XERS, this dilution often comes with strong growth potential, unfortunately, but it's a price I am willing to pay anyway.

Company vs. Peers

There are plenty of companies in the healthcare sector and looking at a similar-sized company, Theseus Pharmaceuticals Inc ( THRX ) comes to mind. Where I see more benefit to owning XERS would be the higher likelihood of them achieving a profitable bottom line sooner. THRX is expected to see profitability first in 2028, and even then estimates vary wildly, with EPS going from $0.92 in 2028 to $7.43 in 2032.

THRX has managed to grow their balance sheet rather well over the last few years and with a $250 million cash position they are in a good place to deploy plenty of capital to fund research given they are also debt free. The cancer treatment market that THRX is in is however very competitive and capital intense. The same could be said for markets that XERS are in, but they have a proven track record of being able to take market share aggressively and reflect the new market share in their revenues. That is one of the advantages that come with owning XERS instead, and that is the tipping point for me and the reason I would go with XERS.

Final Words

XERS is a company that is aggressively taking market share in their industry and providing plenty of value to investors as a result of it. The new products the company is launching are proving very successful and will be key growth drivers for the coming years. With profitability not far away, I am confident in the business and investing at these price levels. XERS is a BUY.

For further details see:

Xeris Biopharma: Remarkable Market Share Expansion