XROLF - Xero: All Eyes On The International Growth Potential

Summary

- Xero suffered a blow to its UK growth hopes with the announcement of a delay to its ‘Making Tax Digital’ initiative.

- The company could cut costs to offset the sub/revenue growth shortfall in the meantime, so the near-term earnings impact should be limited.

- With a strategic uncertainty from the latest CEO reshuffle and the stock still priced expensively, I think a neutral stance makes the most sense here.

New Zealand-based cloud-based accounting software provider Xero ( OTCPK:XROLF ) remains a compelling option to gain exposure to the secular small/medium business ((SMB)) growth tailwind. Having already cemented its foothold in Australia/New Zealand, the company is now in the midst of expanding overseas via a ‘platform’ strategy across key growth markets. One key market is the UK, which recently suffered a setback with the announcement of a multi-year ‘Making Tax Digital’ ((MTD)) delay. The impact will be mostly felt at the revenue line, with lower sales and marketing expenses likely to support profitability in the meantime. It also marks a challenging start to new CEO Sukhinder Singh Cassidy’s international growth ambitions, though the massive SMB addressable market means Xero has ample opportunity to refocus its efforts elsewhere. All in all, I like the fundamentals but paying ~7x fwd EV/Revenue (~10x trailing) in this environment for <20% top-line growth seems pricey; I think a wait and see approach makes the most sense here.

MTD Delay is a Blow to the Near-Term UK Growth Hopes

The UK government has undergone several regime shifts in recent months but the announced delay in implementation of the next phase of its ‘Making Tax Digital’ (or MTD) initiative for income tax self-assessment for self-employed and landlords came as a negative surprise. Per the announcement, the target date will now be April 2026, implying a two-year delay relative to the prior April 2024 target. For Xero, this reduces the immediate need for its software significantly – the phased approach will push a portion of demand (sized at >4m taxpayers ) into the first phase in April 2026, followed by a higher amount in the second phase in April 2027.

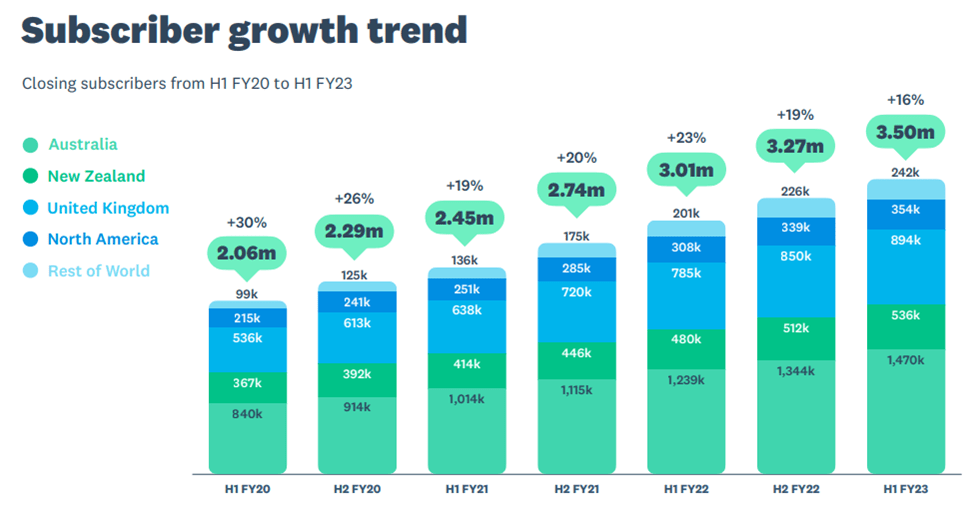

Net, the news will come as a blow to Xero’s growth plans in the UK – recall that the stronger H1 revenue result was helped massively by the UK business, which has seen better average revenue per user (ARPUs) than the group. Relative to management guidance for a further improvement in H2 subscriber growth in the UK, this delay could even see Xero fall short of its near-term growth targets, depending on the offsetting benefits from go-to market improvements and the MTD for VAT tailwind in H2 2023.

Beyond FY23, this news introduces uncertainty to the sub growth trajectory – with an election due before MTD implementation (likely in late 2024/early 2025), it remains uncertain if current policies will remain intact. With room in SMB budgets for more accounting software limited in the current inflationary environment as well, voluntary software adoption seems unlikely. So while bulls will argue for some degree of adoption in the meantime, I expect most potential subs will opt to delay until the deadline. In line with this view, I would underwrite a more conservative sub growth outcome in FY24/FY25 to reflect the delay of the next phase of MTD.

{kind=link}

Xero

Silver Linings from the MTD Announcement

While the MTD delay will be a headwind, there could still be potential upside to the UK subs growth trajectory as Xero Go gains traction, particularly on the freemium side. Xero Go growth will be ARPU dilutive in the near-term, though, so expect revenue momentum to slow before picking up in H2 2023, as further price hikes in North America (scheduled for November) kick in. Also positive is that the timeline for VAT-related MTD remains unchanged per the HMRC announcement - with penalty points effective January 2023 for non-compliant businesses, there is a clear tailwind (albeit a smaller one vs self-assessment) for adoption in the UK.

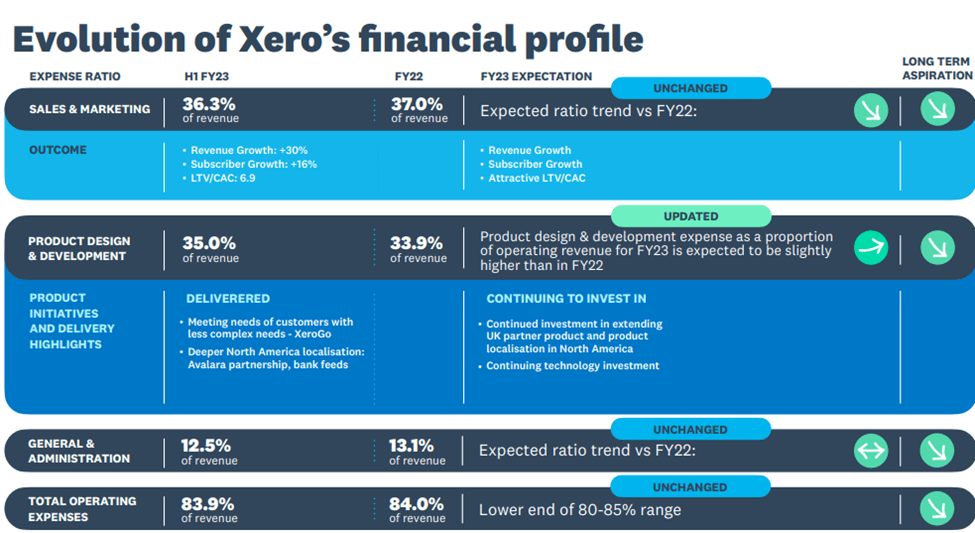

On the profitability side, the impact to Xero from the MTD delay could even be positive – while Xero will lose growth, it also has the option of scaling down sales and marketing spend, as well as related product development costs in the UK. More broadly, the company is also pulling back on headcount growth amid a renewed focus on efficiency, so EBITDA margins should be insulated through FY24. With guidance due at the upcoming H2 2023/FY23 results announcement, more headcount reduction could even pose upside risk to the margin outlook, in my view. Relative to the guided ‘lower end’ of the 80-85% opex target, the 84% result in H1 2023 leaves the bar fairly low for H2 2023; a very achievable <80% ratio would be sufficient to get the company to the full year ratio target.

{kind=link}

Xero

Not the Ideal Start for New CEO Sukhinder Singh Cassidy

The timing of the UK announcement could hardly be less favorable. Recall that Xero announced the surprise departure of prior CEO Steve Vamos and the subsequent appointment of Sukhinder Singh Cassidy alongside the H1 result. Backed by a Silicon Valley tech background, new CEO Singh Cassidy was likely brought on to expand the market beyond the Australia/New Zealand stronghold. As she will be US domiciled, this could be an indication of where Xero’s focus lies, although the recent strength of the UK market could point to it being an additional focus area as well.

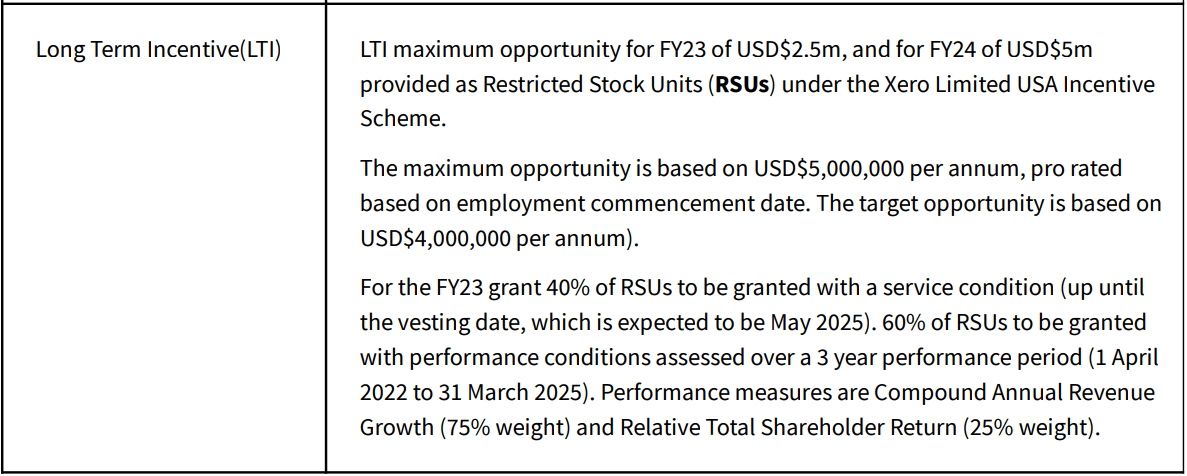

Plus, her compensation (see table below) has been aligned to growth, with ~75% of long-term incentives tied to revenue growth outcomes, suggesting the company’s path forward is on further expansion rather than optimizing earnings. For now, uncertainty remains over the three-year strategy – former CEO Vamos executed well on his plan through FY23 and the onus will now be on Singh Cassidy to follow up with her FY24-FY26 strategy. Pending clarity here, expect some overhang on the stock in the interim.

{kind=link}

Xero

All Eyes on the International Growth Potential

Xero’s leadership in cloud-based accounting software leaves it poised to capitalize on the secular SMB digitization trend globally. Leveraging a ‘platform’ strategy to replicate its success in Australia/New Zealand overseas, the company has also hired a new CEO with Silicon Valley experience to spearhead the execution. The recent MTD announcement in the UK is thus, a setback, given it had been a key growth market for the company, but the massive global addressable market opportunity means there remains ample opportunities to expand elsewhere. The key hurdle for me is the valuation – at ~7x fwd revenue (~10x trailing) for a <20% top-line grower, the stock is already priced for success. Pending a more attractive entry point, I am sidelined on Xero.

For further details see:

Xero: All Eyes On The International Growth Potential