INTU - Xero: Decelerating Growth With Expensive Valuations

2023-10-16 13:01:11 ET

Summary

- Xero needs to invest in its business to grow geographically and broaden its service offering, limiting profitability improvements.

- The company faces competition from global market leader Intuit and strong local players in Asia and Europe.

- Xero's growth is slowing, and its high valuation is not justified for a business with limited innovation and profitability.

Investment thesis

Xero ( XROLF ) needs to continually invest in its business to grow geographically as well as broaden its service offering to compete successfully against larger peers. This limits profitability improvements in the medium term, sales growth is already decelerating and valuations remain expensive. We downgrade to a sell rating.

Quick primer

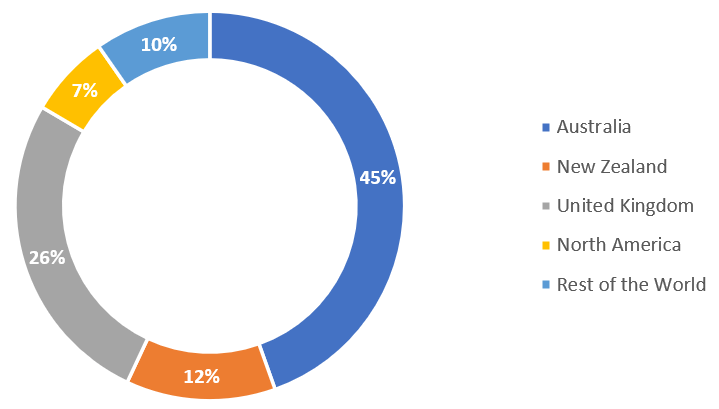

Founded in 2006, Xero offers a cloud-native accounting SaaS that has attractive entry-level pricing (although it has service limitations). Its core home markets of New Zealand and Australia made up 57% of total FY3/2023 sales, with the second key market being the UK; it has over 3.74 million subscribers.

Global software giant Intuit ( INTU ) is the undisputed market leader with its QuickBooks product which was launched back in 1983. Offering on-prem as well as SaaS, it is said to have around 80% share of the global market as it arguably has a first-mover advantage and has developed a large, loyal user base. However, we stress that this is primarily for the English-speaking world - there are strong local players in Asia such as Megi (unlisted) and Kingdee ( KGDEY ) in China, and native SaaS player freee ( FREKF ), ORIX ( IX ) and Obic Business Consultants (4733) in Japan. Other strong local players include Sage ( SGGEF ) in the UK and Europe.

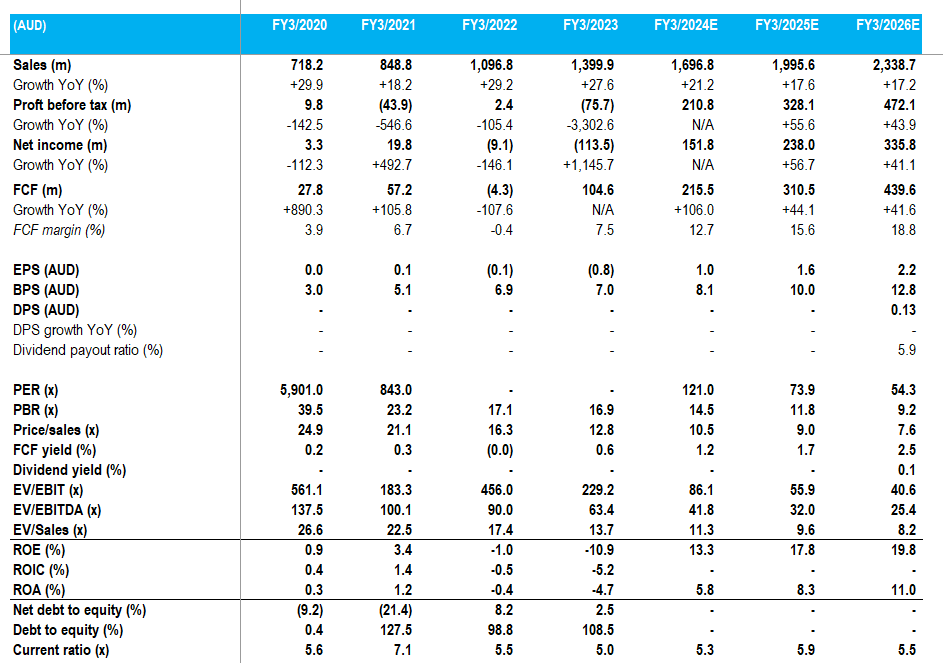

Key financials with consensus estimates

Key financials with consensus estimates (Company, Refinitiv)

{kind=link}

Sales split by geography - FY3/2023

Sales split by geography - FY3/2023 (Company)

{kind=link}

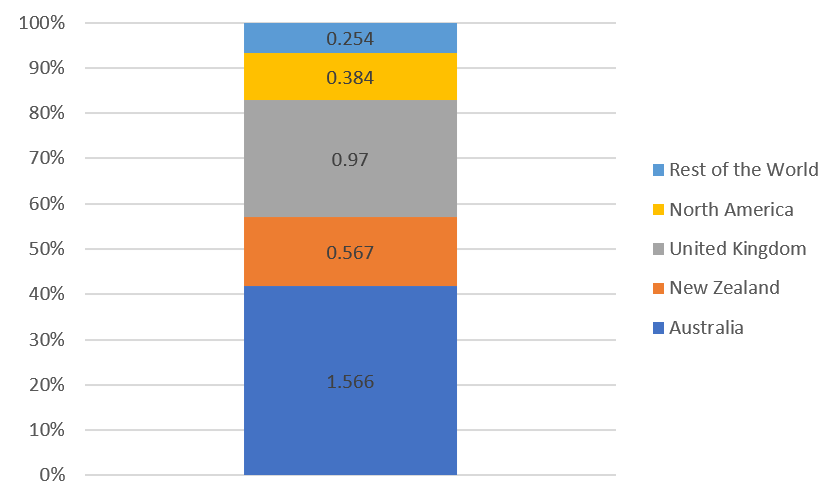

Subscriber split by geography - FY3/2023

Subscriber split by geography - FY3/2023 (Company (numbers are in millions))

{kind=link}

Updating our view

We are updating our view from March 2021 , where we had a neutral rating as the valuation appeal was limited. FY3/2023 results highlighted that the business has been relatively resilient despite volatile macro conditions, growing revenue by 28% YoY and subscriber growth of 14% YoY. User churn remained low at 0.9%, and the company expanded into providing a workforce management tool called 'Workday' as a cross-selling service. However, operating margins remained relatively low at 4.1%, and the company has guided for an improvement YoY into FY3/2024 by aiming for total operating expenses to be 'around 75%' of revenue compared to 80.7% in FY3/2023. It is noticeable that sales and marketing costs remained at elevated levels, making up 33.7% of total sales.

The company looks set for continued growth, and this should be expected with the high level of sales and marketing activity. Current consensus forecasts point to operating margins to reach approximately 20% in the medium term. We want to assess whether this is a realistic scenario and the risks behind achieving this goal.

Driving long-term shareholder value

Xero does not have official targets in terms of profitability and timeframe but states that its long-term aspiration is to continue improving its operating expense ratio. It does however state that these ratios and component parts will vary from period to period as it identifies opportunities for disciplined, customer-focused growth. Whilst this leaves plenty of maneuver for the company, it can leave some investors with questions about what the business wants to achieve.

When the company believes its TAM opportunity to be worth AUD45 million which is equivalent to over 30 times FY3/2023 revenue, prioritizing sales growth does make sense. However, given that consensus forecasts show sub-20% sales growth estimates for the next two years with a decelerating growth profile indicates to us that 1) the TAM forecast is perhaps unrealistic, 2) the company's prospective market share will remain in single digits, despite the shift to cloud services, and 3) the company is unlikely to reach high market share in its current form, and significant investment in service development or geographic expansion is necessary. These do not point to a simple case of creating long-term shareholder value.

Accounting services have barriers to entry for new markets as they need local expertise for local market accounting policies, financial reporting, and taxation regulations; upfront investment and continual service maintenance costs are necessary and consequently, we see Xero's resources have been focused on markets with similar systems - Australia, New Zealand and the UK. Scaling in the US and the Rest of the World will need significant investment.

We also feel that if Xero were to make a real impact on gaining market share, it would have to upscale from targeting small businesses to larger organizations. This will mean having to offer a broader suite of business tools, as well as making its systems fit all business sizes as well and making sector-specific versions. We believe Xero has a long way to go to address and meet this potential.

Risks in raising future returns

Investing in a company like Xero is about growth, driven by innovation and increasing competitiveness. Whilst we believe Xero was a pioneer in introducing easy-to-use accounting SaaS, this offering is no longer such a competitive product and has been replicated successfully by its peers.

Management has a long-term focus, but the pace at which accounting SaaS has advanced over traditional accounting services has slowed, market penetration has risen, and despite some game-changing aspects for streamlining financial processes, it is not a high-value-add business that enjoys high profitability.

We believe Xero has been successful at churn reduction and increasing its pricing. However, it has not successfully addressed slowing growth, and scaling its operations has so far led to limited economies of scale. Cost management is set to improve with total operating expenses to fall to 75% of sales, but we believe this is not attractive enough to show it has the right strategy to create shareholder value. Reaching 20% operating margins by FY3/2026 appear too optimistic.

Valuation

In a world where financing costs have risen and growth is set to slow, Xero may stand out as a relatively sustainable growth business. On consensus forecasts the shares are trading on PER FY3/2025 73.9x, a free cash flow yield of 1.7%, and an EV/EBITDA multiple of 32.0x. Despite pricing in a growth premium, current valuations look expensive for what we believe to be a slowing business demonstrating limited innovation.

Thesis catalyst

Decelerating growth and continual spending on sales and marketing costs to drive topline sales underline the business model's limited ability to raise margins, resulting in valuation multiple contractions.

Risks to the thesis

Customer acquisition steps up a gear as Xero begins to roll out new business tools, attracting more medium-sized enterprises. Sales and marketing costs are reduced without lowering the pace of new customer additions.

Conclusion

We believe Xero is set to grow its business, with a growing user base driving recurring revenues. However, our view is that the company needs to continue investing in its business in order to continue business expansion - both geographically as well as building out new tools to increase its market offering. As a result, management's ability to control operating costs will be limited and profitability is unlikely to improve materially for the medium term. With expensive valuations, we downgrade to a sell.

For further details see:

Xero: Decelerating Growth With Expensive Valuations