XES - XES: Oil Services To Benefit From Long-Term Upstream Spending

2023-11-19 20:28:26 ET

Summary

- Oil services companies have substantially underperformed since 2014.

- However, the long-term outlook for upstream spending looks favorable for the oil services sector.

- Despite the short-term risk of a global economic slowdown, buying XES ETF for the long term may be rewarding for investors.

The oil and gas industry has faced mounting pressure in the last decade amid a so-called "energy transition" from fossil fuels to renewable energy sources. However, despite the growing investments in renewables, sustaining capital expenditures in the O&G industry will be required to meet the growing needs for energy in the world.

SPDR S&P Oil & Gas Equipment & Services ETF ( XES ) is an affordable, liquid, and diversified pure-play oil services ETF that provides exposure to the sector that is set to flourish if the O&G capex keeps rising or at least stays the same sustainably.

About XES ETF

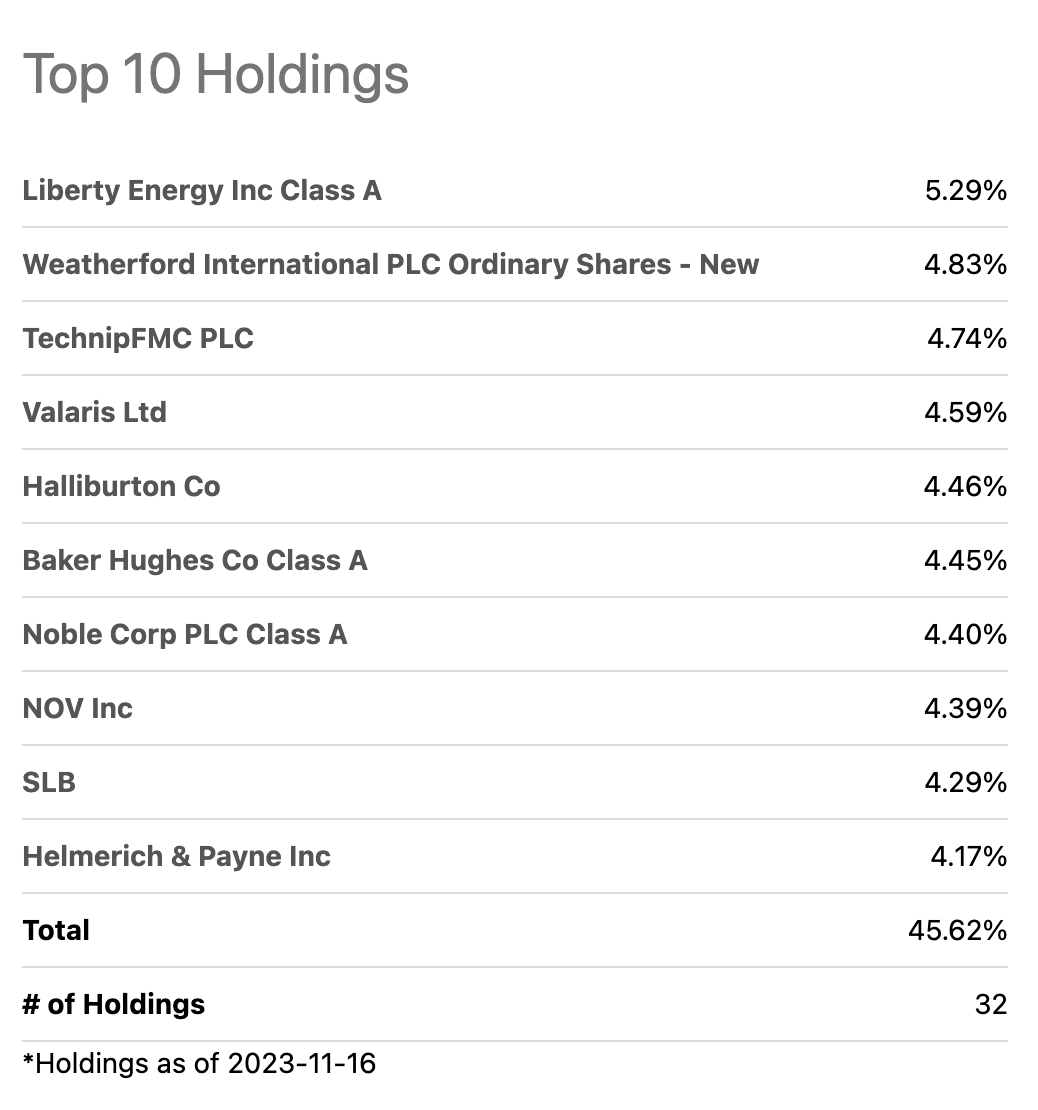

XES aims to replicate the performance of the S&P Oil & Gas Equipment & Services Select Industry Index. The ETF invests in stocks that are included in this index, which is representative of the oil and gas equipment and services segment of the S&P Total Market Index.

The holdings of XES are typically composed of mid-cap stocks of companies in the oil services industry.

{kind=link}

OIH and XES: Comparing Pure-Play Oil Services ETFs

There are plenty of ETFs that have oil services companies among their holdings. However, if you want to pick an affordable, liquid, and pure-play oil services ETF, then VanEck Oil Services ETF ( OIH ) and SPDR S&P Oil & Gas Equipment & Services ETF are primary options to consider, in my view.

I'd like to highlight the following key differences between XES and OIH:

- Mid-cap exposure: XES provides way greater exposure to mid-sized oil services companies compared to OIH's focus on mostly large caps. If you want more mid-cap exposure, XES may be preferable.

- Weighting methodology: OIH uses market cap weighting, so the largest companies get the biggest weightings. XES uses modified equal weighting, reducing single stock concentration risk.

- Liquidity: OIH has higher daily volume and tighter bid/ask spreads. If trading liquidity is important, OIH seems to be the better choice.

- Expenses: XES and OIH have the same 0.35% expense ratio, which is lower than a median expense ratio of 0.48% among all ETFs according to Seeking Alpha data.

Performance of XES and OIH has been very similar in the last several years, though in 2010-2015 there was a noticeable difference in performance in favor of XES.

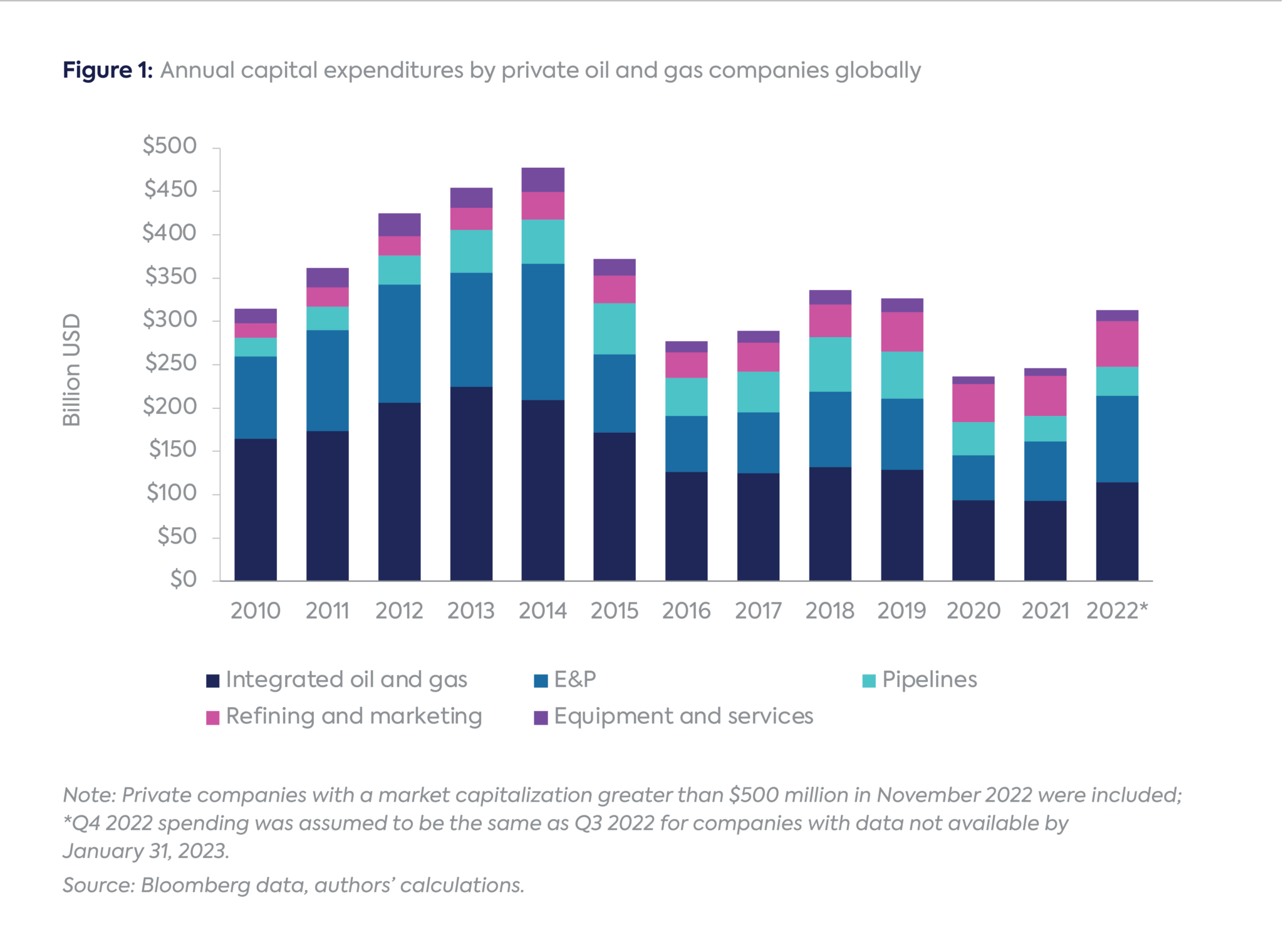

The thing is, the period of 2011-2014 was a golden era for the oil services industry, with the highest volume of global upstream capital expenditures in the 21st century so far.

Center on Global Energy Policy

{kind=link}

Considering that XES outperformed OIH during these bullish times for the oil services industry, mid-caps (the majority of XES holdings) seem to perform better in a bullish environment for oil. In this regard, XES may be a better option to invest for the long term.

The Outlook

First, let's start with a controversial statement made by the International Energy Agency (IEA) in its World Energy Outlook 2023 report :

There is no longer a need – in any of the scenarios that we model – for oil and gas investment in 2030 to be higher than it is today. Sentiment in the industry seems to be broadly aligned with this view: less than half of the available cashflows from record revenues in 2022 went back into new oil and gas investment, and current upstream spending remains below where it was in 2019.

Unlike, for example, OPEC, IEA has a much colder stance towards the O&G, clearly gravitating towards renewables. Nonetheless, as we will find out later, IEA is "technically" right in its assumption.

According to JPMorgan , global upstream oil and gas spending is tracking $545 billion this year, which is up from $497 billion in 2022, based on data from 140 public companies and JPM's estimate.

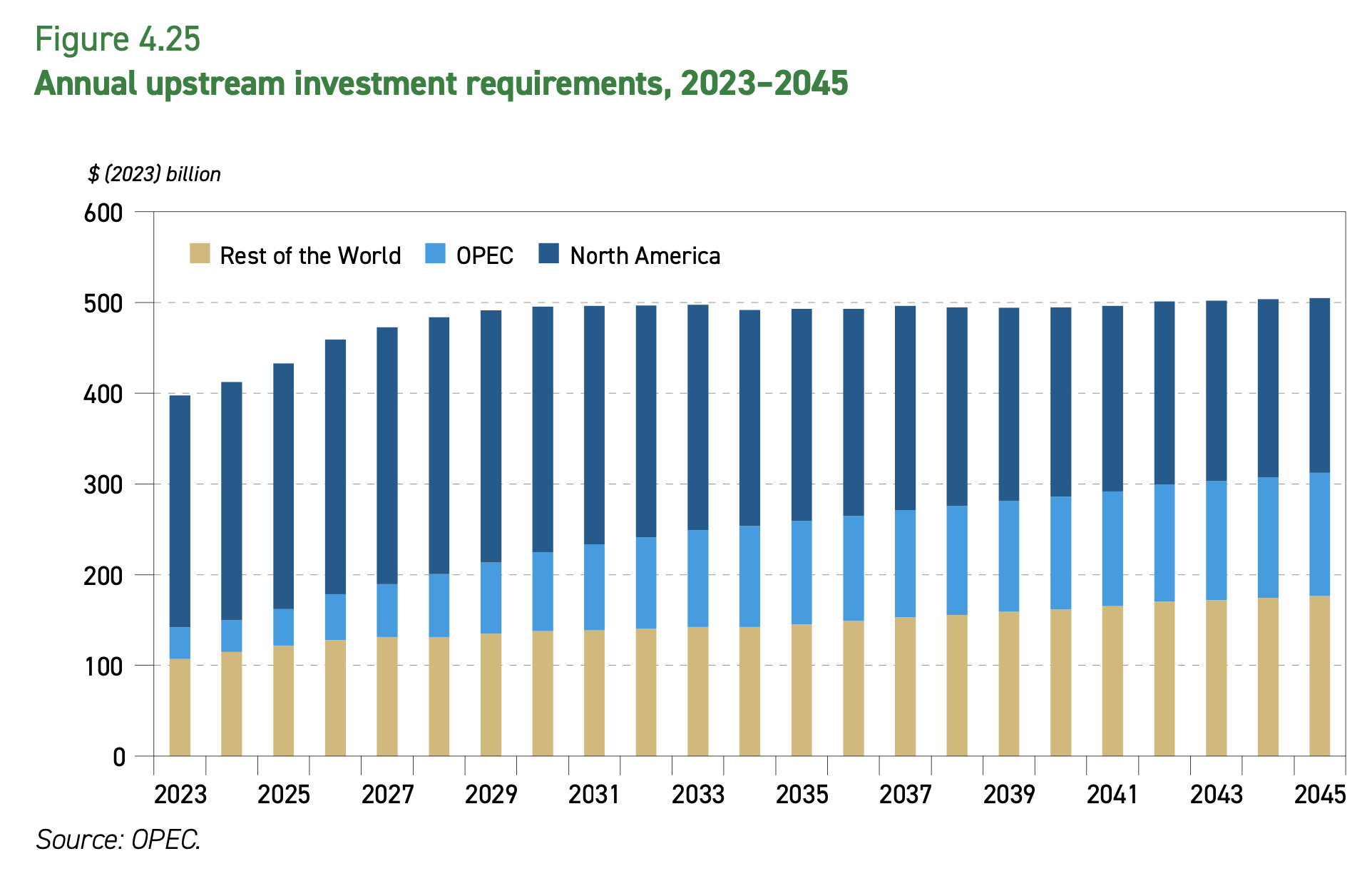

OPEC in its most recent World Oil Outlook 2045 report says that in order to ensure growing oil demand needs are met, cumulative oil-related investment requirements will have to remain substantial. Based on OPEC estimates, the upstream sector is projected to require $11.1 trillion in the 2023–2045 outlook period or $480 billion per year:

{kind=link}

Thus, IEA is "technically" right: there will be no need for higher yearly capex for oil. The tricky part, though, is that to guarantee a steady supply of oil, these investments need to be stable every single year, which is obviously unlikely given the volatile nature of the oil market.

Further on, OPEC specifies that 65% of the estimated upstream capex will be required in North America. Upstream investment requirements in the rest of non-OPEC, excluding North America, are set to rise from $107 billion per year in 2022 to $177 billion per year in 2045. Moreover, investment requirements in OPEC countries may quadruple from $35 billion per year in 2022 to $136 billion per year in 2045.

No matter what angle you look at it from, without sustaining upstream spending at the current (relatively comfortable) level, the world may struggle to secure a long-term supply of oil.

Risks

According to the latest projections of the International Monetary Fund, world economic growth will slow from 3.5% in 2022 to 3% this year and 2.9% next year. The global economic slowdown may affect demand for oil and lead to a decrease in upstream spending. Under such a scenario, oil services companies may underperform in the near term.

One of the best ways to address this risk is dollar-cost averaging . If you're going to invest for the longer term, simply spread out your purchases over the next couple of years to minimize the market timing factor.

The Bottom Line

Despite a clearly dismal performance since 2014, I stay bullish on oil services companies in the long run. The global appetite for oil implies the need for stable investments in the upstream segment, and higher O&G capex will be beneficial for the oil services companies XES ETF represents.

For further details see:

XES: Oil Services To Benefit From Long-Term Upstream Spending