OXLC - XFLT: DRIP At A Discount To Stream Your Income Into A River Of Cash

2023-08-28 14:00:19 ET

Summary

- XAI Octagon Floating Rate & Alternative Income Term Trust has increased its distribution by 16% and now offers a high yield of 15% annually.

- The closed-end fund's dividend reinvestment plan, or DRIP, allows for reinvesting dividends at a discount to the market price, further increasing total returns.

- XFLT's asset mix includes senior secured loans, CLO equity, and CLO debt, with a focus on generating attractive total returns and income.

I am a water guy. I grew up on the ocean, I learned to swim at an early age and later learned to surf and ski (on frozen water). I was born under the sign of Aquarius and my personality is shaped by the astrological aspects of the zodiac:

The symbol for Aquarius is the Water Bearer, symbolically and eternally giving life and spiritual food to the world. The water from the vessel washes away the past, leaving room for a fresh, new start. The sign of Aquarius is forward-looking and growth-oriented. Concerned with equality and individual freedom, Aquarius seeks to dispense its knowledge, and its vision of equality and individuality, to all.

In that context and using a water analogy, I am offering my knowledge of investing for income to those who seek to learn and grow their own knowledge base. My goal in income investing is to grow my future income stream to support my retirement years by continually reinvesting and compounding dividend paying stocks and funds like exchange-traded funds ("ETFs") and closed-end funds ("CEFs") that offer regular high yield distributions. In that way, I can grow my river of cash coming into my retirement account with an ever-increasing flow of income.

Some CEFs that I own and that offer high yield distributions also offer a DRIP (dividend reinvestment policy or plan) that allows for those regular dividends to be reinvested as shares at a discount to the market price when the broker who issues your shares supports it. One of those funds that I own and which I have previously written about is XAI Octagon Floating Rate & Alternative Income Term Trust (XFLT). I last wrote about XFLT in October 2022, and one of my followers requested that I write an update on the fund.

Since I last wrote about XFLT, the fund managers announced an increase in the distribution in May of this year by 16%, from a previous dividend of $0.07 to $0.085 monthly, now yielding 15% annually. And if you elect to participate in the DRIP and your broker (I use Fidelity) supports the discounted DRIP, you can benefit from an additional increase of up to 5% per month by reinvesting those dividends rather than taking them as cash. The DRIP policy is spelled out in the fund’s semi-annual report :

Under the Plan, whenever the market price of the Common Shares is equal to or exceeds NAV at the time Common Shares are valued for purposes of determining the number of Common Shares equivalent to the cash dividend or capital gains distribution, participants in the Plan are issued new Common Shares from the Trust, valued at the greater of (i) the NAV as most recently determined or (ii) 95% of the then-current market price of the Common Shares. The valuation date is the dividend or distribution payment date or, if that date is not a NYSE trading day, the next preceding trading day. If the NAV of the Common Shares at the time of valuation exceeds the market price of the Common Shares, the Plan Agent will buy the Common Shares for the Plan in the open market, on the NYSE or elsewhere, for the participants’ accounts, except that the Plan Agent will endeavor to terminate purchases in the open market and cause the Trust to issue Common Shares at the greater of NAV or 95% of market value if, following the commencement of such purchases, the market value of the Common Shares exceeds net NAV.

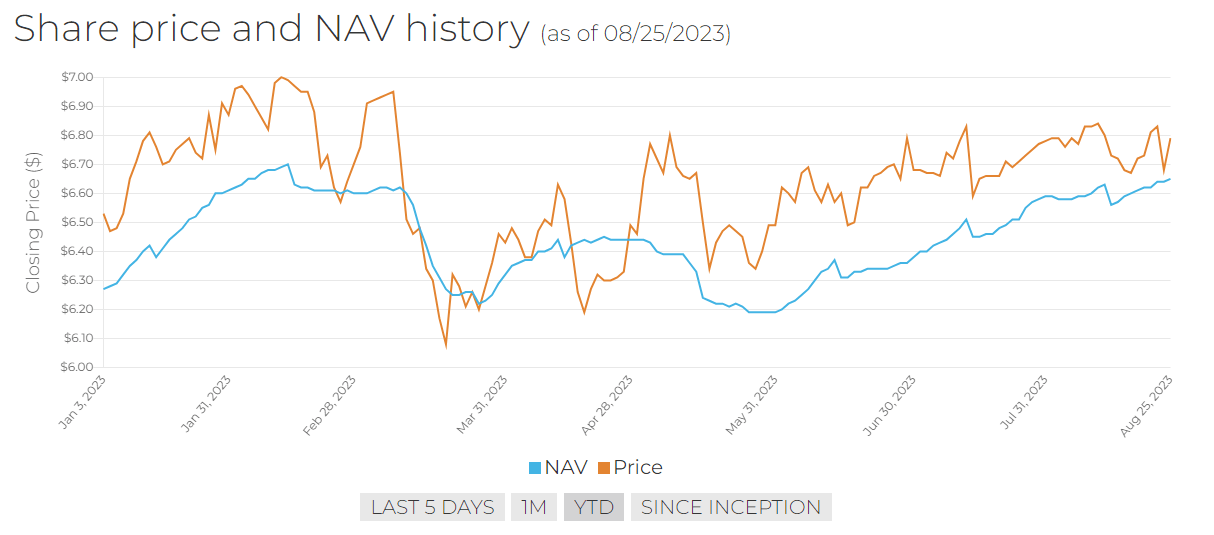

Currently, XFLT trades at a market price of $6.79 as of market close on 8/25/23 and the NAV is estimated at $6.65, resulting in a premium of about 2.1%, as shown on the fund’s website .

{kind=link}

Over the past year, XFLT has traded at an average premium of about 3%, so the current premium is slightly below the one-year average but is clearly trending upwards. The next distribution is payable September 1 for shareholders who owned shares prior to the ex-date of 8/14/23. Assuming that the premium remains at about 2% or higher over the next few trading days, investors who DRIP the shares will receive an additional benefit by reinvesting at a price slightly below market price – most likely at the NAV of $6.65 which is higher than 95% of the market price.

Fund Overview and Objectives

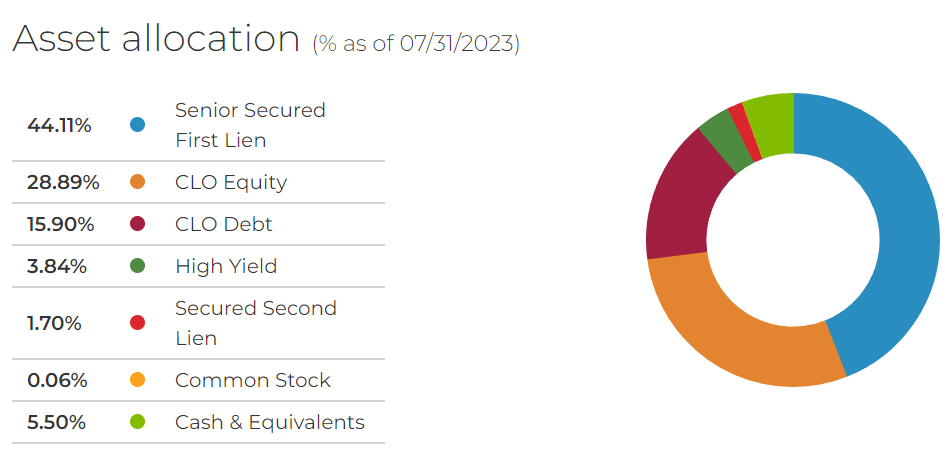

For those who are new to the fund or have not had a chance to read my previous coverage, XFLT is designed to achieve attractive total returns with an emphasis on income generation across multiple stages of the credit cycle. The fund managers will invest at least 80% of managed fund assets in senior secured loans, collateralized loan obligation ("CLO") equity, and CLO debt. As of 7/31/23, the current asset allocation shows about 44% in first lien senior loans, 29% in CLO equity, 16% in CLO debt, 5% in high yield and second lien loans, and 5.5% in cash.

{kind=link}

The amount of CLO debt was increased over the past 9 months or so due to extremely attractive discounts as explained by Gretchen Lam, Senior Portfolio Manager, in the Q2 earnings call transcript :

And as you can see on Page 10, in 2023 and really throughout the back half of 2022, we've increased our exposure to CLO debt in particular last year and over the course of this year, CLO debt was, in our view, extremely attractive on a relative basis versus loans and CLO equity, really because the low debt offered both very high current yields over 12% and also could be purchased at a very meaningful discount to par, which allowed for both additional what we call pull-to-par upside over time, and in the earlier parts of 2023, we were modeling out returns for many of our BB purchases in the high teens on a total return basis.

Now, over the course of the summer those discounts in CLO debt have been going away and the asset mix is shifting more towards CLO equity in the second half of 2023.

With respect to the loans that XFLT holds, the majority are floating rate instruments, which have, therefore, benefited from rising interest rates. This has enabled the fund to earn more income by increasing the holdings in higher interest loans as fund volume increases, supporting the increased distribution. In fact, since the distribution increase was announced in May, the fund has seen a lot of growth, with daily volume as of August 18 increasing to 292,000 shares per day compared to 123,000 share per day at fund inception.

Current State of the Credit Cycle

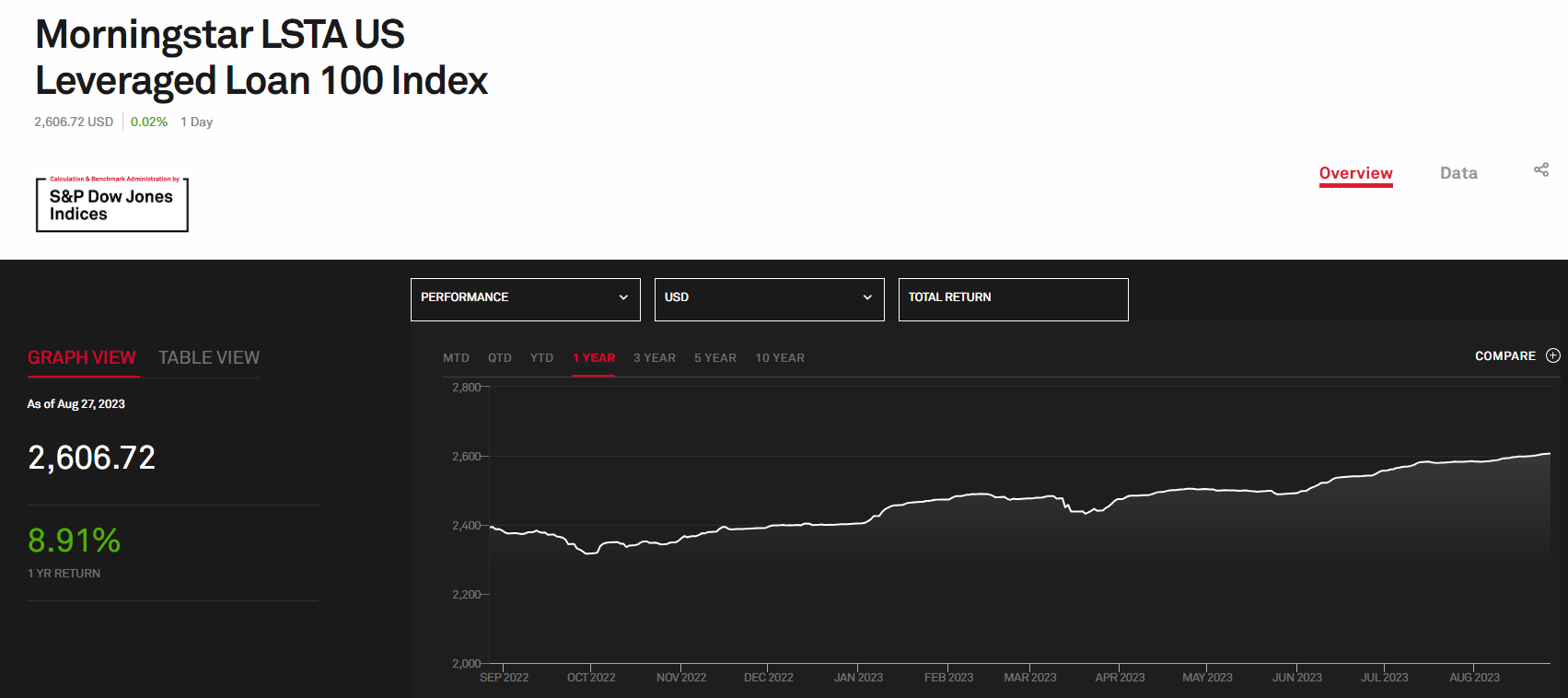

While doing some research for this article, I looked for updated information for both the leveraged loan markets and CLO investments. The Morningstar LSTA Leveraged Loan 100 Morningstar LSTA US Leveraged Loan 100 Index is a proxy that I used to analyze the current state of the senior secured loans that XFLT holds. After a tumultuous year in 2022, the index has performed well for most of 2023, with a few minor blips along the way, including the bank default scare in March, and the US credit default scare during the debt ceiling debate in May/June.

{kind=link}

And in fact, although we are seeing some recovery in credit markets in 2023, there are still some good discounts for loans and CLOs in the secondary markets as explained again by Gretchen Lam in the earnings call:

Nonetheless, even as they rallied in recent months, the loan and CLO tranches are trading at levels but certainly reflect many of the challenges that currently persist in the economy. Loans are still trading at discounts to par. The index is at 94.2% as of 6/30. And this is even as loan prepayments have picked up a bit in recent months. And as a reminder, these loan prepayments are really a big benefit to CLO equity as those par prepayment proceeds can be reinvested at new - into new loans at discounted prices.

Likewise, CLOs have experienced some challenges recently due to rising concerns of an increase in default rates from historically low levels. In one recent article that I found from Fitch Ratings , there is a heightened concern that refinancing CLOs could prove to be especially challenging going forward:

Fitch Ratings believes refinancing challenges for highly levered issuers will be exacerbated by an increasing number of U.S. broadly syndicated loan collateralized loan obligations exiting their reinvestment period. An estimated 40% of BSL CLOs will be out of their RP by YE 2023, meaning a subset of this market will have additional investing limitations. Issuers rated on the middle to high end of the non-investment-grade scale may be able to extend maturities, but lower-rated issuers are less likely to be able to do so, or on sustainable terms.

To address that concern, the fund managers have been looking at reducing CLO equity exposure for those CLOs that are beyond the end of their reinvestment period. This highlights another advantage of XFLT over other more CLO-focused funds such as Eagle Point Credit Company ( ECC ) or Oxford Lane Capital (OXLC). With a mix of basically 50% loans and 50% CLOs, the fund managers at XFLT have more latitude to make adjustments to the asset mix in their portfolio, which currently includes more than $484M in managed assets spread over 493 holdings (as of 7/31/23).

Another advantage that XFLT has over other funds like ECC and OXLC is their use of leverage. Although the leverage stands at about 40%, that leverage is achieved using a credit facility rather than being based on issuance of preferred shares as is the case with the other CLO Funds. That credit facility currently has an average cost of 6.34% as of June 30.

Additionally, XFLT does not pay any income incentive fees or performance fees, just a flat management fee. This is another advantage that XFLT has over the other CLO funds.

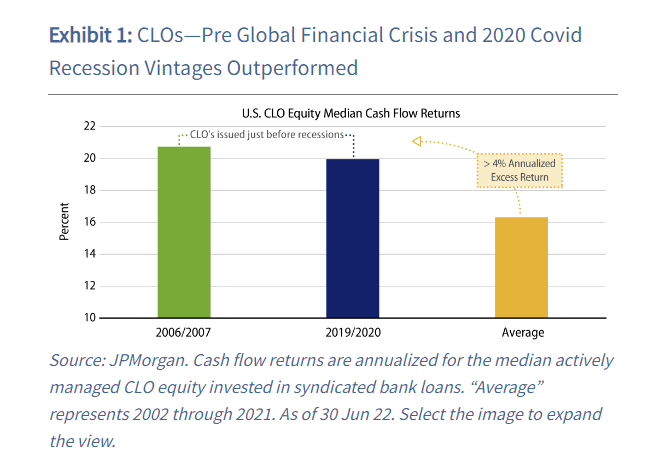

CLO funds in general offer investors attractive yields in both bull and bear markets. And if the economy should dip into a recession later this year or in 2024, CLO equity can offer outperformance compared to stocks or bonds due to the unique characteristics of the asset class. According to this blog from Western Asset Management, CLO equities issued just before the 2 most recent recessions outperformed other asset classes.

What may be counterintuitive when reviewing business cycles and the impact they have on market returns is that the equity of an actively managed CLO—which invests in bank loans—may outperform both credit and stocks should the US tip into recession. With history providing some guidance, it’s worth noting that CLOs that were originated before the last two recessions produced better returns for shareholders than in other years.

{kind=link}

Experienced and intelligent managers of CLOs will be aware of current market cycles and will adjust the holdings to take advantage of those peaks and valleys to reposition the portfolio. As I discussed in my recent article , "Eagle Point Credit: Analyzing Q2 2023 Earnings Results," the discounted prices being offered in the secondary market for CLOs offers an opportunity to increase the average weighted effective yield and help the fund managers to generate compelling risk-adjusted returns.

What are the Risks?

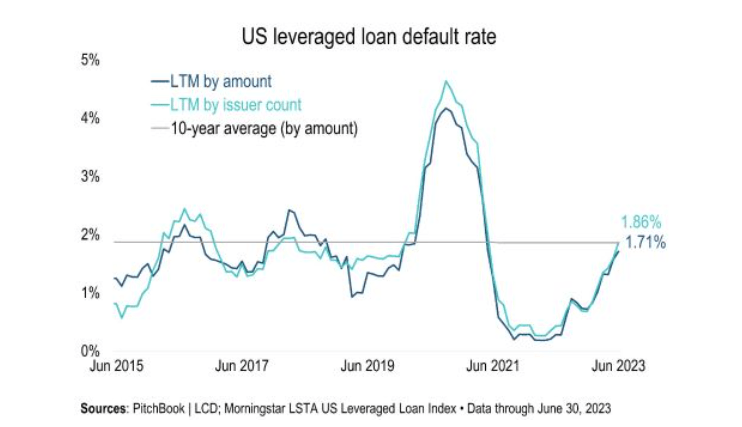

The most relevant risk to CLO equity returns is that the underlying loans will default. And although the loan default rate is currently higher than it was at the beginning of the year, it is still quite low based on historical data. According to Pitchbook , as of the end of June 2023, leveraged loan default rates are approaching the 10-year average of about 1.86% after reaching historic low levels in 2022. If the current trajectory should continue for the next 12 months, it is estimated that the default rate could rise to as high as 2.75% by mid-2024, slightly above the 20-year historical average of 2.7%.

{kind=link}

Another potential risk is that the fund sub-advisers, Octagon Credit Investors, LLC, a subsidiary of Conning Holdings Limited, may experience some changes due to a pending merger agreement. The parent company of Octagon, Conning, is being acquired by Generali Group, a global insurance and asset management provider. According to the press release, the merger should benefit all parties involved and may in fact strengthen the abilities of Octagon to support their clients.

Summary

The XAI Octagon Floating Rate & Alternative Income Term Trust closed-end fund is one that I hold as part of my income compounder portfolio, which you can read more about here . Currently offering a high yield distribution of about 15% based on a monthly distribution of $0.085, the fund trades at a slight premium to NAV of about 2%. When reinvesting the monthly distributions, the fund’s DRIP allows for those reinvested shares to be purchased at a slight discount to the market price, further enhancing the total return based on the discounted cost.

I own several other funds in my IRA that also offer high yields and allow the DRIP at a discount, which further increases my future income stream, leading to a river of cash to use for my retirement when I need it in the coming years. Some of those funds include ECC and OXLC, which I mentioned in this article, and which also invest in CLOs to generate high yield income.

If you are new to income investing and are seeking a solid source of high yield income for your own portfolio, I would recommend researching whether it makes sense to add XFLT if you do not already own shares. I do not know what the future will look like, but based on recent history including Q2 results and a recently raised distribution, I would be a buyer of XFLT at the current price if I did not already own shares. The share price may fluctuate by a few percentage points in the coming months depending on what happens with the broader economy and there may be a better buying opportunity ahead. However, if you wait to get a better price, you may miss out on collecting the dividends that are paid out in the meanwhile. Do your own research and come to your own conclusions and please let me know in the comments section if you have any questions or have additional information to add to the discussion.

For further details see:

XFLT: DRIP At A Discount To Stream Your Income Into A River Of Cash