XLF - XLF: Banks Are In Trouble Again

2023-03-10 14:58:30 ET

Summary

- Deposit withdrawals and possible bad loans could force banks to sell AFS and HTM bonds.

- Thus, banks would be forced to realize huge losses.

- I would not recommend buying the financial sector XLF in this environment.

The SVB Financial Group fallout

The SVB Financial Group (SIVB) fallout is creating a mini credit crunch, with the credit spreads spiking and the stock market dropping. This is what I have been describing as the Phase 3 selloff. But this could be just a prelude of the Phase 3 credit-crunch selloff. In fact, we are not fully even in the Recessionary Phase 2 selloff yet.

However, the SVB fallout reveals that banks are in trouble again. Whether this is anything even close to the 2008-type financial crisis, it's too early to say. But here is what's going on.

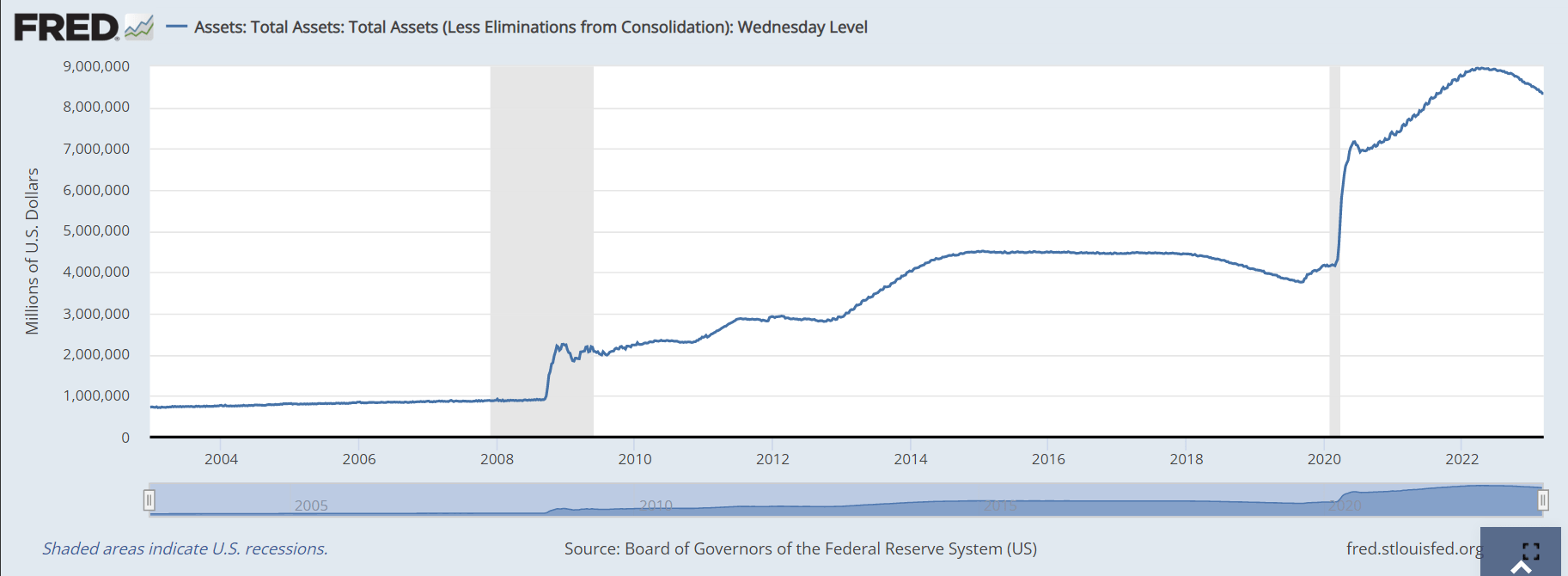

The Fed's COVID-related massive liquidity injection

The starting point to understand the current banks' troubles is the Fed's massive liquidity injection during in response to COVID. As the Chart below shows, the Fed injected around $4.7 trillion into the financial system from 2020 to 2022 via asset purchases or QE.

{kind=link}

Liquidity trapped on banks' balance sheet

However, most of that liquidity has been trapped on the banks' balance sheet. Instead of making the loans, commercial banks bought the safest assets - Treasury Bonds. Some of these bonds were classified (for accounting purposes) as securities held to maturity HTM, and some as securities available for sale AFS.

The chart below shows the about $2 trillion increase in the securities held to maturity for US banks from 2020 to 2022. These securities are by definition meant to be held to maturity, and any capital gain/loss is not included on the income statement.

The chart below shows that the US banks' holding of securities available to sale increased by about $1.5 trillion from 2020 to 2022, before falling in 2022. That's approximately $3.5 trillion combined.

The Fed study shows the $4.4 trillion increase in Fed's purchases and $4.2 trillion in increase in banks' balance sheet, but notes that this relationship is more coincidental than casual. But the fact is that banks significantly increased their purchases of the Treasury bonds as the Fed expanded the money supply.

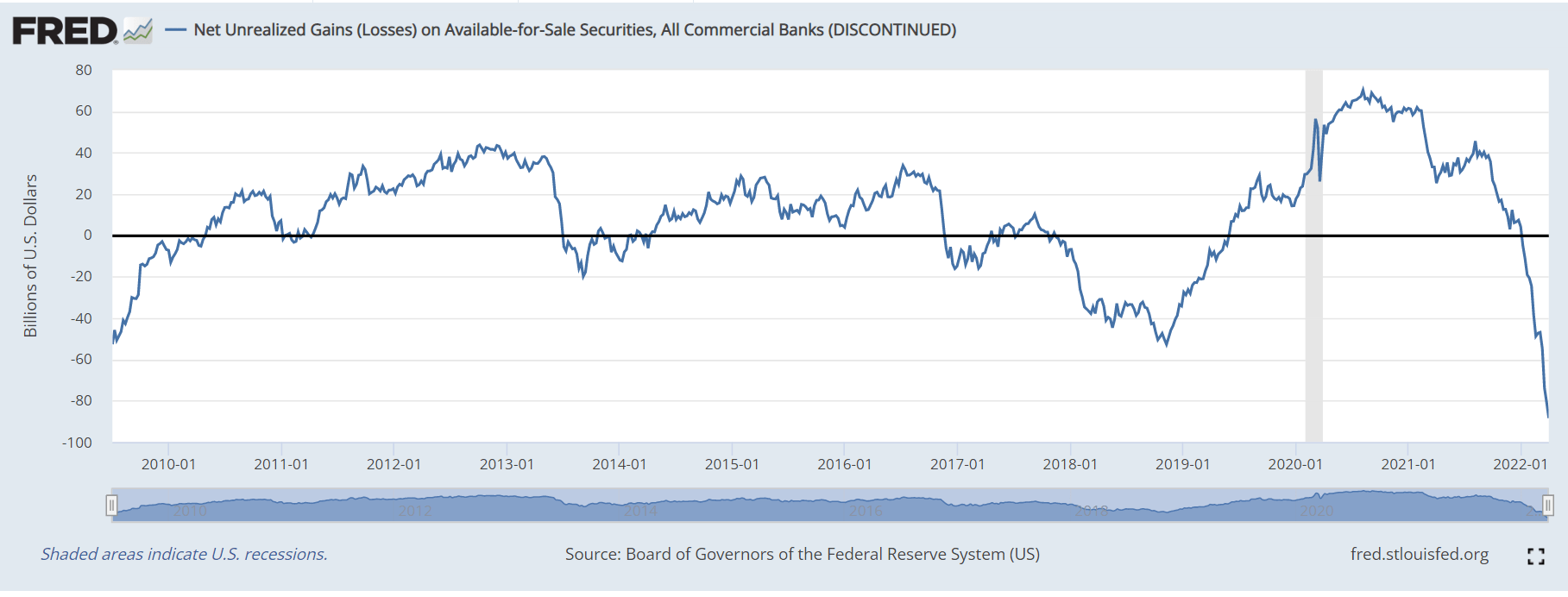

Huge unrealized losses

The securities available to sale are by definition intended to be eventually sold to raise capital as needed, and the realized capital gain/loss is recorded when the security is actually sold. Otherwise, the capital gain/loss is not included in the income statement.

The chart below shows that these securities available for sales have huge unrealized loss in 2022, as the bond prices fell and interest rates increased. The data on securities held to maturity would shows the same.

{kind=link}

Unrealized losses are not a problem, as long as the banks don't have to sell these bonds. If all of these securities are held to maturity, the capital loss would be zero, as bonds return the par value at maturity.

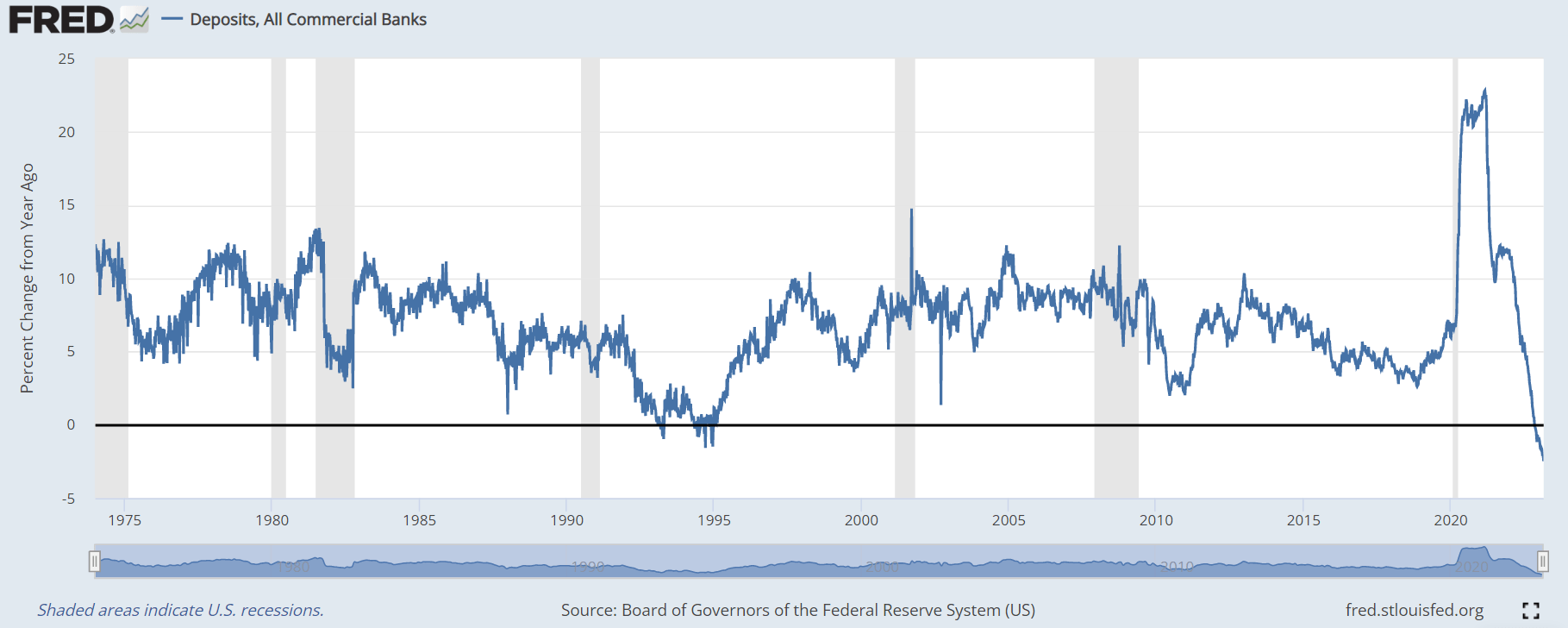

Deposit withdrawals

Parallel with the increase in liquidity, the banks' deposits surged post 2020 COVID crisis. The growth in deposits has peaked on March 10, 2021, and slowed in 2021. However, in November of 2022, the deposits started to decline, and currently, banks are losing about 2.5% in deposits per month, and the trend is accelerating, as the chart below shows. Note, this is first time that deposits are decreasing at this rate since 1970.

{kind=link}

Two things to worry about

US banks could be forced to realize huge losses if they're forced to sell their securities available for sale, and as the chart above shows this process has been underway. The problem gets bigger if some of the securities held to maturity also have to be pre-maturely sold.

So, what could force the banks to liquidate these securities?

1) Continued deposit withdrawals

Given the that short-term interest rates are above 5%, consumers and business have an incentive to move the funds from checking/savings and other transactional bank accounts that pay insufficient interest rate, to high-yielding US Treasury Bills. This trend is likely to accelerate as the Fed continues to increase short term interest rates toward 6%. As the deposits deplete, some banks might be forced to sell the securities, and realize the losses. Otherwise, the banks might have to increase the interest rates on savings accounts, which would equally negatively affect the profitability (as the cost of capital increases).

2) Bad loans

Given the sharp increase in interest rates on car loans, mortgages, and commercial loans, it's reasonable to expect a much higher default rates, especially once the unemployment rate starts to increase. This alone, but especially if combined with depleting deposits, could force the banks to raise the capital by selling the SAS and HTM securities.

Another bailout?

The potential combination of bad loans and the depleting deposits is the 1929 bank run scenario.

So, what can the Fed do? The Fed can simply lower the interest rates and push the bond prices higher. In fact, that's what the bond market is pricing in the SVB aftermath.

However, the Fed is obligated to fight inflation, so as long as inflation is above the 2% level, the Fed has to keep the monetary policy tight. The scenario where there is a "bank run" and still high inflation would put the Fed in a very difficult position. Financial stability vs. price stability?

Investment implications

The popular financial sector ETF ( XLF ) is heavily weighted toward the large banks, with Bank of America ( BAC ), Wells Fargo ( WFC ), and JPMorgan ( JPM ) account to over 20% of the index. Even though the current crisis is mostly centered on regional banks ( KRE ), large banks are not immune, as the risks are systematic, related to the monetary policy.

Since, the SVB fallout, XLF is down by 8% over two days, breaking the 200dma support, making the "lower low," and it looks like approaching the October lows.

Whether the current liquidity issue with SVB becomes a major "bank run" depends on the development on inflation front and the responding monetary policy. Higher interest rates accelerate the deposit withdrawals and increase the probability of bad loans. The market is currently betting in a bailout, but that's not certain. Remember Lehman Brothers.

For further details see:

XLF: Banks Are In Trouble Again