PEP - XLP: Consumer Staples Are Too Expensive Vs. High Interest Rates

2023-07-31 07:28:24 ET

Summary

- Consumer staples are often seen as a safe haven during recessions, but high inflation and interest rates still negatively impact the industry.

- Valuations in the consumer staples sector are too high compared to elevated interest rates and slowing projected earnings growth rates.

- The debt picture at many food/beverage and consumer product giants is not conservative, bringing weaker growth outlooks and falling margins vs. a decade ago.

- Technical momentum is waning, with underperformance vs. the S&P 500 the new normal since December.

U.S. consumer staples are often considered an intelligent place to hide during recessions and stock market turmoil. There is some evidence to back up this claim. However, during times of high inflation and interest rates, even blue-chip leaders in everyday goods manufacturing/processing tend to suffer like other equities.

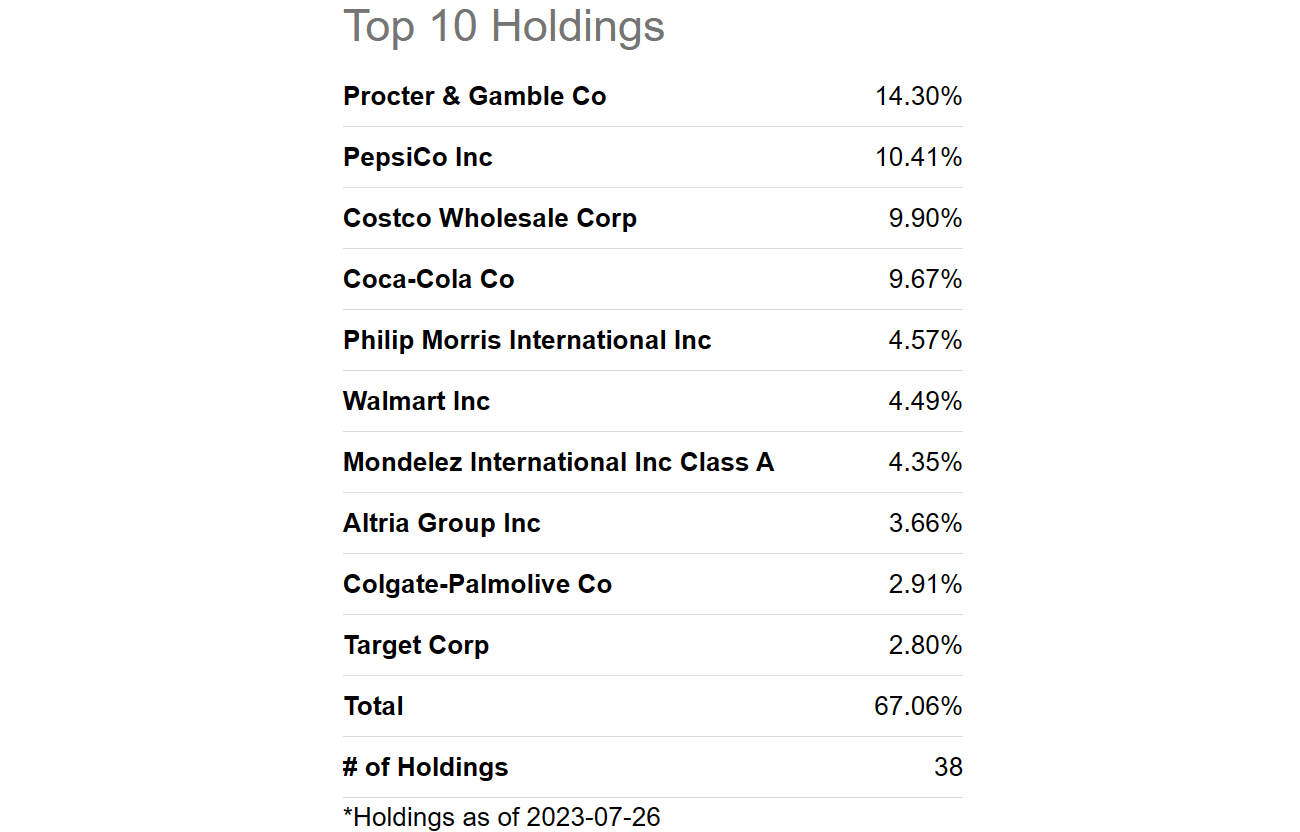

One of the poster children and top examples of investment performance in this space is the Consumer Staples Select Sector SPDR ETF ( XLP ). The Top 10 holdings represented a staggering 67% of net value on July 26th, and includes Procter & Gamble ( PG ), PepsiCo ( PEP ), Costco Wholesale ( COST ), Coca-Cola ( KO ), Philip Morris International ( PM ), Walmart ( WMT ), Mondelez ( MDLZ ), Altria Group ( MO ), Colgate-Palmolive ( CL ), and Target ( TGT ). All household product names and the places we regularly shop for them.

Seeking Alpha Table - Consumer Staples SPDR ETF, Top 10 Holdings, July 26th, 2023

{kind=link}

While I have also looked toward food, beverage, toiletry, snack, and cigarette makers to conserve capital, today I am not very bullish on the sector. In fact, I have written bearish articles on Costco several weeks ago here and PepsiCo in January here . Why?

The reasoning is two-fold. First, valuations are too high vs. rising interest rates. Second, high valuations do not match up well against super-slow projected growth rates for earnings.

Overvaluations vs. Interest Rates

Sector stock pricing already "outperformed" during the 2022 rise in inflation and interest rates. Consumer products and general retail actually outlined a terrific zigzag of beating industrial, cyclical, and Big Tech names during the bear market last year.

However, valuations on earnings are the same or HIGHER now than early 2021, when the jump in interest rates began in earnest. Typically, when interest rates rise as fast as 2021-23, all stocks endure a serious selloff in price. It's entirely logical. If I can capture a risk-free return from CDs or Treasuries well in excess of what's available for dividend yield or even earnings (or free cash flow) yield on investment, why should I take on the risk of any stock that can theoretically fall in price to zero in a deep recession or with a business mismanaged with too much debt and competitive challenges.

For example, the dividend yield payout from XLP is a good -3% lower than what I can capture today from 3-month Treasury bills. This is a far cry from the positive cash distribution returns (relative to interest rates and inflation) achieved during most of the last decade. Believe it or not, the dividend story today in July 2023 is now looking like the major market peaks of 2007-08 and 1999-2000 for consumer product leaders. Both of these periods proved great times to SELL the group, not buy.

YCharts - CPI Inflation, 3-Month Treasury Rate vs. Consumer Staples ETF Dividend, 12 Months YCharts - CPI Inflation, 3-Month Treasury Rate vs. Consumer Staples ETF Dividend, 10 Years YCharts - CPI Inflation, 3-Month Treasury Rate vs. Consumer Staples ETF Dividend, Since 2000

Of the Top 10 positions in XLP, only the two tobacco companies are paying cash yields higher than the 5% to 5.5% returns available from Treasury securities under 12 months in duration.

YCharts - XLP Top 10 Positions, Trailing Dividend Yield, 12 Months

Earnings yields on investment are not faring as well as you would like as an owner either. The median average earnings yield from the Top 10 XLP positions is under 4%. Where's the premium yield to offset the equity risk for price?

YCharts - XLP Top 10 Positions, Trailing Earnings Yield, Since January 2021

Really, only Altria is generating a free cash flow (or earnings) yield on investment beyond the risk-free bond rate in America. If your goal is to own businesses producing cash flow, earnings, and dividend yields better than the rate of inflation and risk-free Treasury yields, consumer staples as a group are failing to surpass this simple hurdle today.

YCharts - XLP Top 10 Positions, Free Cash Flow Yield, 3 Years

Low Estimated Growth Rates

If XLP's list of consumer giants maintained super-strong balance sheets, and robust growth rates for sales and income, sure I would be interested in owning extended valuations upfront. But that is not the case.

The debt picture for the majority of consumer staples is not the same as the 1970s or 1980s. This sector has "leveraged" brand-name awareness to juice returns on capital/equity, while stretching consumer product pricing at the retail level to create unsustainable profit margins, in my view. When you go to your local grocery store or general merchandiser, the price spreads on brand-name goods vs. nearly equivalent unbranded alternatives is often 30% to 50% wider. How much further can this premium go if a recession or years of weak consumer spending hits next?

Costco and maybe Walmart have strong to better-than-average free cash flow generation vs. debt levels, as measured against individual company historicals and what other blue-chips are delivering for shareholders. The median average is it would take five years of free cash flow to theoretically pay off all debt, shunning all dividends and share buybacks in the process. This number is not much different than the S&P 500 financial setup overall, representing the whole U.S. large-cap universe for investors. Why not buy a company or industry with lower valuations and higher growth rates is my question?

YCharts - XLP Top 10 Positions, Annual Free Cash Flow to Total Debt, 5 Years

Now that interest rates on debt are spiking and related expenses for big business are bound to climb materially, margins should fall even harder into 2024-25, all other variables remaining the same. Final after-tax profit margins (trailing 12-month determined) are only materially higher at Altria out of the XLP Top 10 holdings vs. January 2021, when interest rates began rising. Plus, only 2 of the 10 have better margins than a decade ago!

YCharts - XLP Top 10 Positions, Trailing Annual Profit Margins, Since January 2021

Yet, price to earnings ratios have stayed in nosebleed territory. Only the two tobacco companies have cash P/Es approaching the S&P 500 average under 20x.

YCharts - XLP Top 10 Positions, Trailing P/E Ratio, Since January 2021

Wall Street analyst estimates for industry EPS growth are quite weak, and not at all supportive of rich valuations. Measured from late 2021 and early 2022, only Costco is expected to reach for 10% growth yearly, and that forecast includes a big fiscal 2022, that should moderate to future numbers under 5% starting this year. As a group, EPS are expected to grow at a 6% to 7% compounded annual rate, just barely above current CPI inflation (cost-of-living) changes!

YCharts - XLP Top 10 Positions, Analyst Projected EPS Growth for 2021-25, Made July 28th, 2023

Final Thoughts

Expensive stocks, with "average" balance sheets, falling margins, and weaker-than-normal growth outlooks are not very appealing to me.

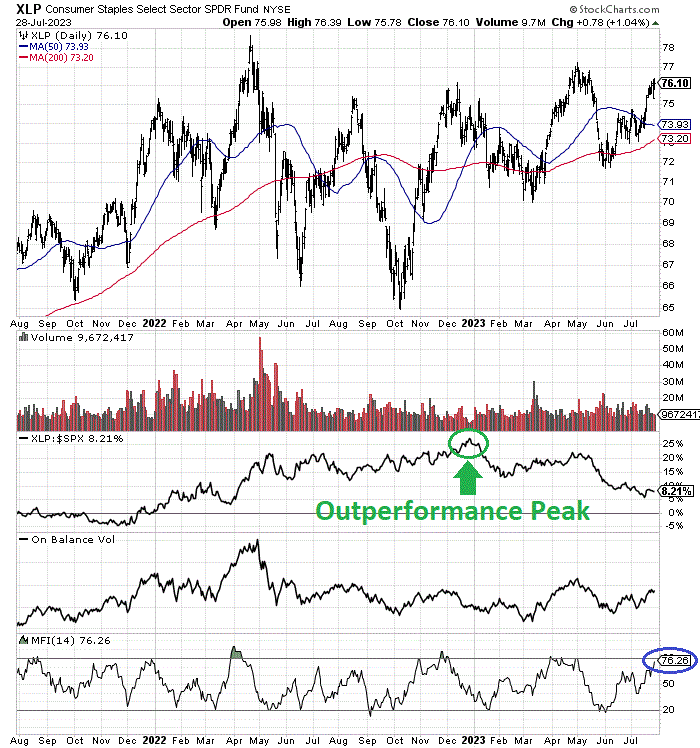

The technical trading setup does not scream buy either. XLP's peak performance vs. the S&P 500 index was reached in December, circled in green on the 2-year chart below. Since then, consumer staples have flatlined while industrial and technology names have spiked in a bullish manner. On Balance Volume trends indicate little net money is flowing into the sector. And, the 14-day Money Flow Index (circled in blue) could be signaling a minor +7% price advance from late May has nearly run its course.

StockCharts.com - Consumer Staples ETF, Daily Price & Volume Changes, 2 Years, Author Reference Points

{kind=link}

How could consumer staple equities rise in price? That's the question to focus on, as economic growth falters. If we get a recession with interest rates remaining high (my forecast is for stubborn inflation, especially if crude oil jumps into 2024), the brand-name food and toiletry leaders in America will suffer just like other investment selections.

The way out of the doghouse is through lower interest rates and far stronger economic (corporate) growth. At this stage of economic malaise, such is unicorn or goldilocks or "best-of-all-worlds" thinking. I am not saying it's impossible for the largest consumer staples to rise in price greater than +10% annually to produce total returns higher than +12%. What I am suggesting is the odds clearly do not favor this outcome.

I rate XLP a Sell . There are literally thousands of individual company setups that offer more upside potential vs. the risks you are required to take to find oversized rewards/returns. My projection is XLP and many of the holdings inside this ETF will continue to underperform the S&P 500 over the next 12 months. For conservative accounts, purchasing bank CDs and Treasury bills/notes may outline stronger returns than the consumer products sector, without any risk to capital.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

XLP: Consumer Staples Are Too Expensive Vs. High Interest Rates