CCI - XLRE: Real Estate Is In Trouble

2023-04-19 16:22:07 ET

Summary

- In this article, we dive into the fundamentals of the (commercial) real estate industry, which is suffering from a mix of headwinds.

- High inflation, rising rates, and related economic woes are likely to further cause deteriorating financial conditions and higher delinquency rates.

- While I expect real estate stocks to suffer further, I have started to buy high-quality REITs in the industry.

Introduction

In multiple articles in the past months, I have written that I'm looking to boost my real estate exposure, which is currently 9.1% of my dividend growth portfolio. Over the past few weeks, I have added to my exposure. However, I'm far from done.

The reason I started buying again is the fact that real estate stocks have weakened quite significantly. The Real Estate Select Sector SPDR Fund (XLRE) has lost roughly 30% of its value since the end of 2021.

FINVIZ

The interrelated mix of higher rates and high inflation is not only causing real estate stocks to drop, but it's also creating a very tricky situation that could result in even more weakness.

In this article, I will walk you through my thoughts on the bigger picture and explain how I'm dealing with this situation from a dividend growth investor's point of view.

So, let's get to it!

Real Estate Is In A Very Tough Spot

On April 18, I read the following article , which mentioned that the White House has started to keep a close eye on the commercial real estate ("CRE") sector as financial turmoil poses another challenge to the industry just a few years after the pandemic.

{kind=link}

As reported by Bloomberg:

The health of the commercial real estate sector has been in the spotlight in recent months, as it has been roiled by rapid rate hikes and vacancy rates amid the rise in remote and hybrid work. Regional banks, which have long dominated commercial real estate lending, may reduce risk-taking in the aftermath of multiple bank failures triggered by the collapse of Silicon Valley Bank last month.

Before I give you more details regarding these financial conditions, let me give you another gloom & doom headline , as Paul Marshall noted similar risks, especially with regard to the somewhat fragile banking sector.

{kind=link}

Mr. Marshall made the case that a weak banking system is likely to make access to credit even tougher, causing credit quality to weaken.

"We are now likely to experience a fairly severe credit crunch which significantly increases the risk of recession," Marshall said in the letter. "Commercial real estate, and especially office property, is the next shoe to drop."

The worst part is that weakness has gone well beyond the office space, which is the worst-hit sector at the moment. Even residential real estate is now feeling the heat after multiple apartment complexes owned by the Applesway Investment Group were foreclosed. The company borrowed close to $230 million to buy more than 3,200 units during the pandemic. Back then, the situation was much easier, as financial conditions were much more supportive of these investments. This is just one example, but it shows that some (weaker) companies are in a very dangerous position. Bear in mind, the residential real estate market is still relatively strong.

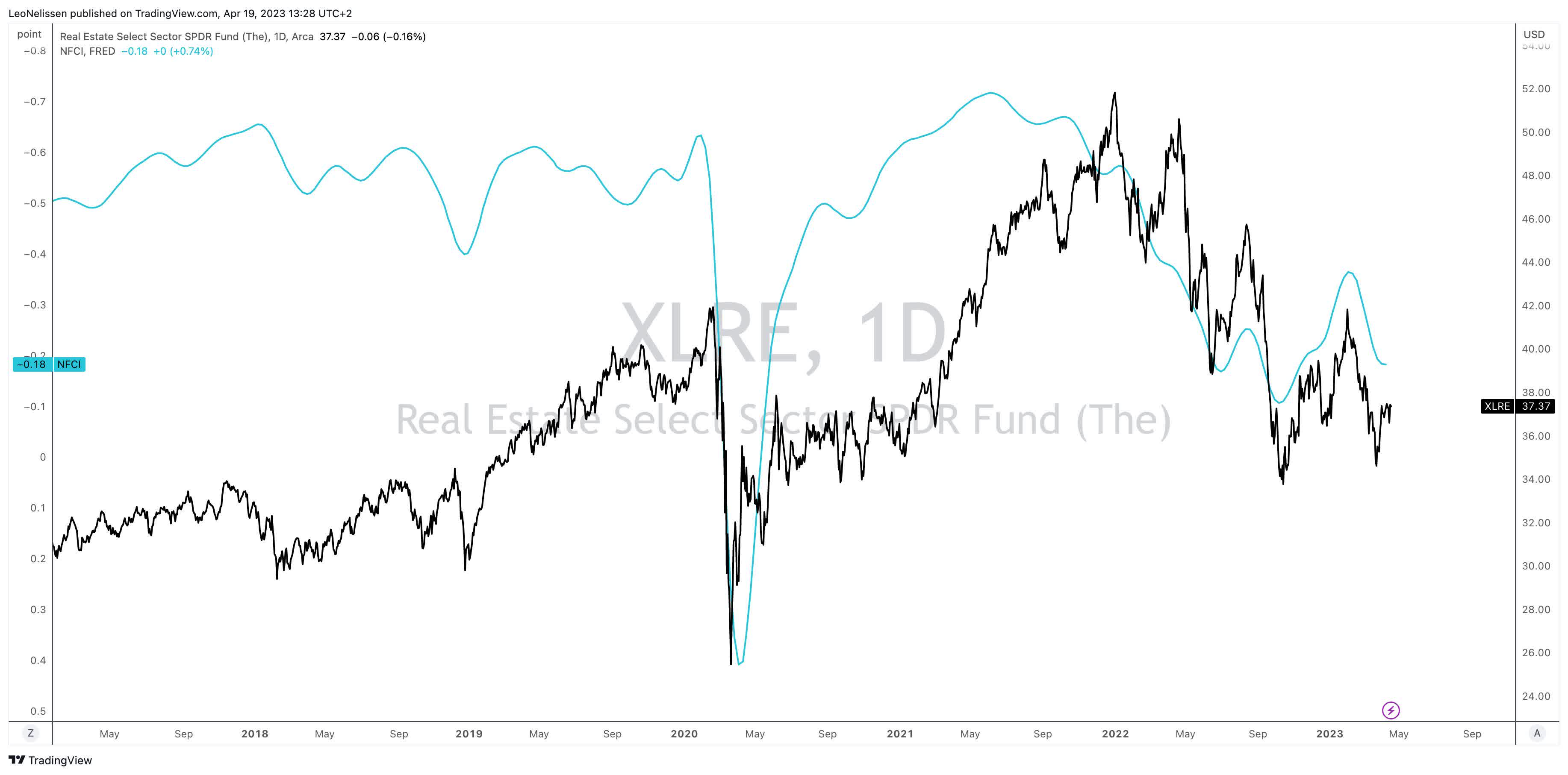

With that said, let's focus on financial conditions. The chart below compares the XLRE Real Estate ETF to financial conditions (inverted axis). Note that every uptrend and downtrend is supported by a similar move in financial conditions.

{kind=link}

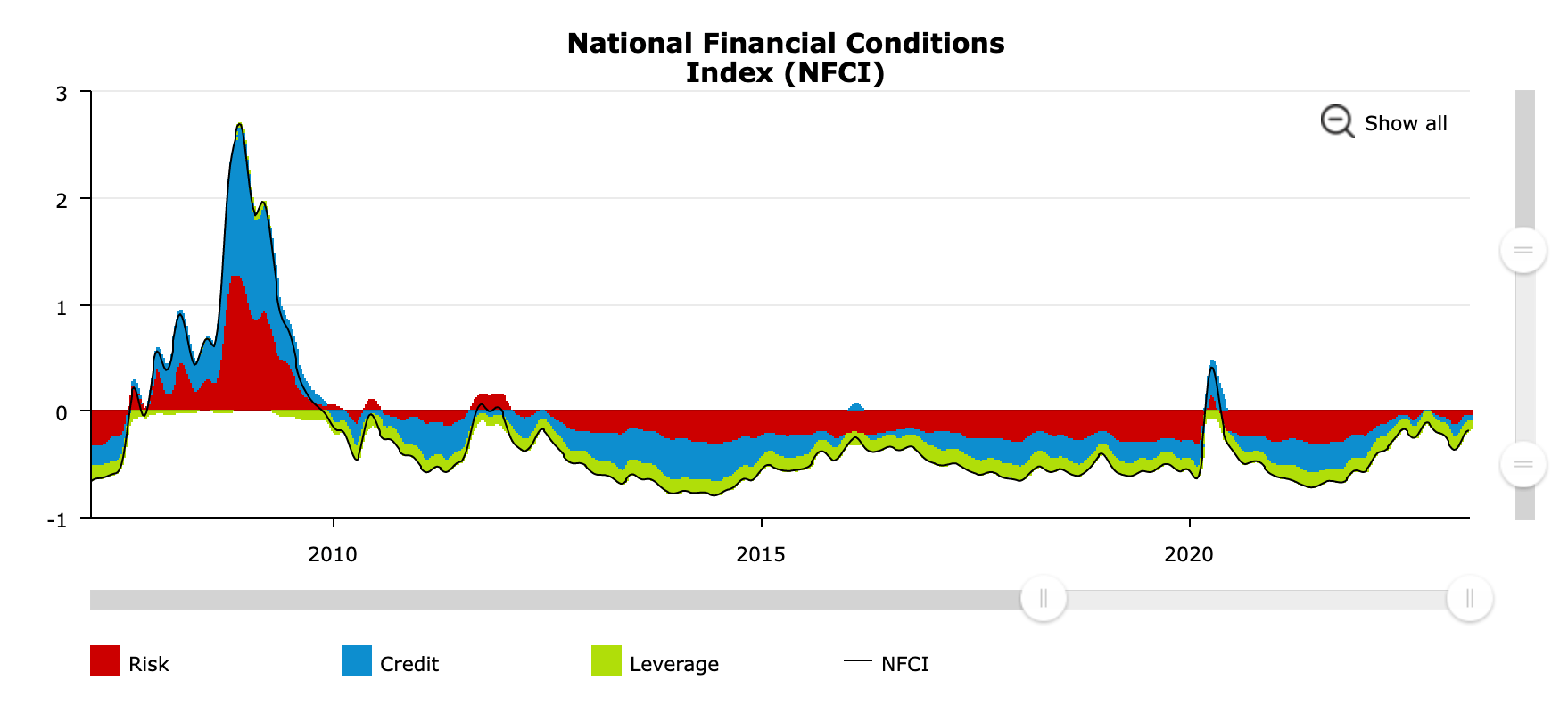

In this case, I used the Chicago Fed National Financial Conditions Index. The NFCI provides a weekly update on US financial conditions in money markets, debt, and equity markets, and traditional shadow banking.

While financial conditions are nowhere near as bad as during the pandemic (let alone the Great Financial Crisis), the trend is clearly in the wrong direction.

{kind=link}

This makes sense as the Fed is further tightening rates, inflation remains sticky, and economic growth is further slowing. In other words, for the past few months, the Fed has been hiking into a weakening economy, which further adds pressure on (commercial) real estate.

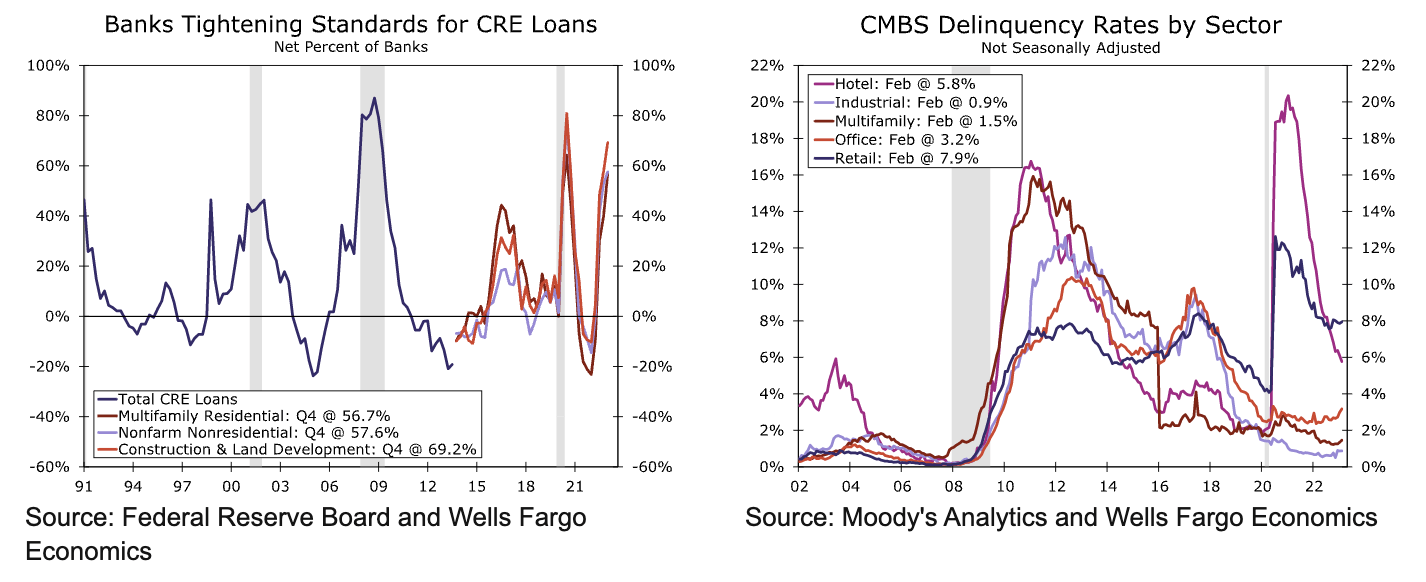

This month's Wells Fargo CRE report highlights the challenges facing the commercial real estate sector as it navigates a looming recession caused by the aforementioned headwinds.

The report notes that although CRE fundamentals remain in positive territory, recent trends indicate that they are moderating. Tightening credit conditions are becoming the latest challenge, and the report warns that more restrictive lending increases the odds of an economic downturn. Banks have been tightening CRE lending standards, and the report warns that increased scrutiny on regional banks, which have become more prominent CRE lenders in recent years, is likely to lead to even tighter credit conditions for CRE borrowers.

This is exactly what other sources (some are mentioned in this article) are telling us as well.

The charts below show tightening credit conditions and the impact this has on delinquencies. While delinquencies are still subdued, we're witnessing some upside momentum, which could accelerate in the months ahead.

{kind=link}

Wells Fargo warns that an increase in distressed asset sales could be forthcoming as more CRE loans mature over the next few years. The report also notes that if an economic downturn were to occur, it would weigh heavily on CRE fundamentals, pushing up delinquency rates and distressed asset sales and dragging on property valuations, which already appear to be declining from the elevated levels reached recently.

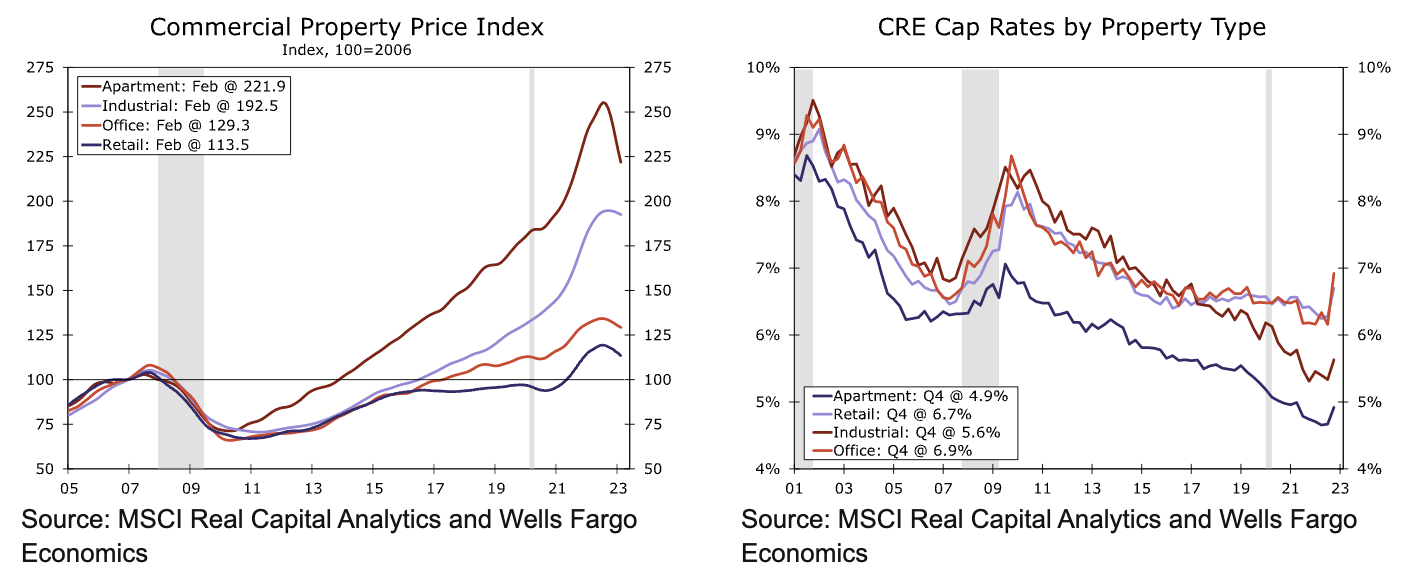

This also spells bad news for property prices.

In our view, property valuations appear to have further to fall. After generally taking a downward trajectory for much of the past decade, cap rates have increased in recent months alongside the leg up in long-term interest rates. Sales of commercial properties have downshifted notably, which means price discovery through appraisals on comparable properties has been minimal. Thus, private measures of property prices are likely not fully reflecting current market conditions.

{kind=link}

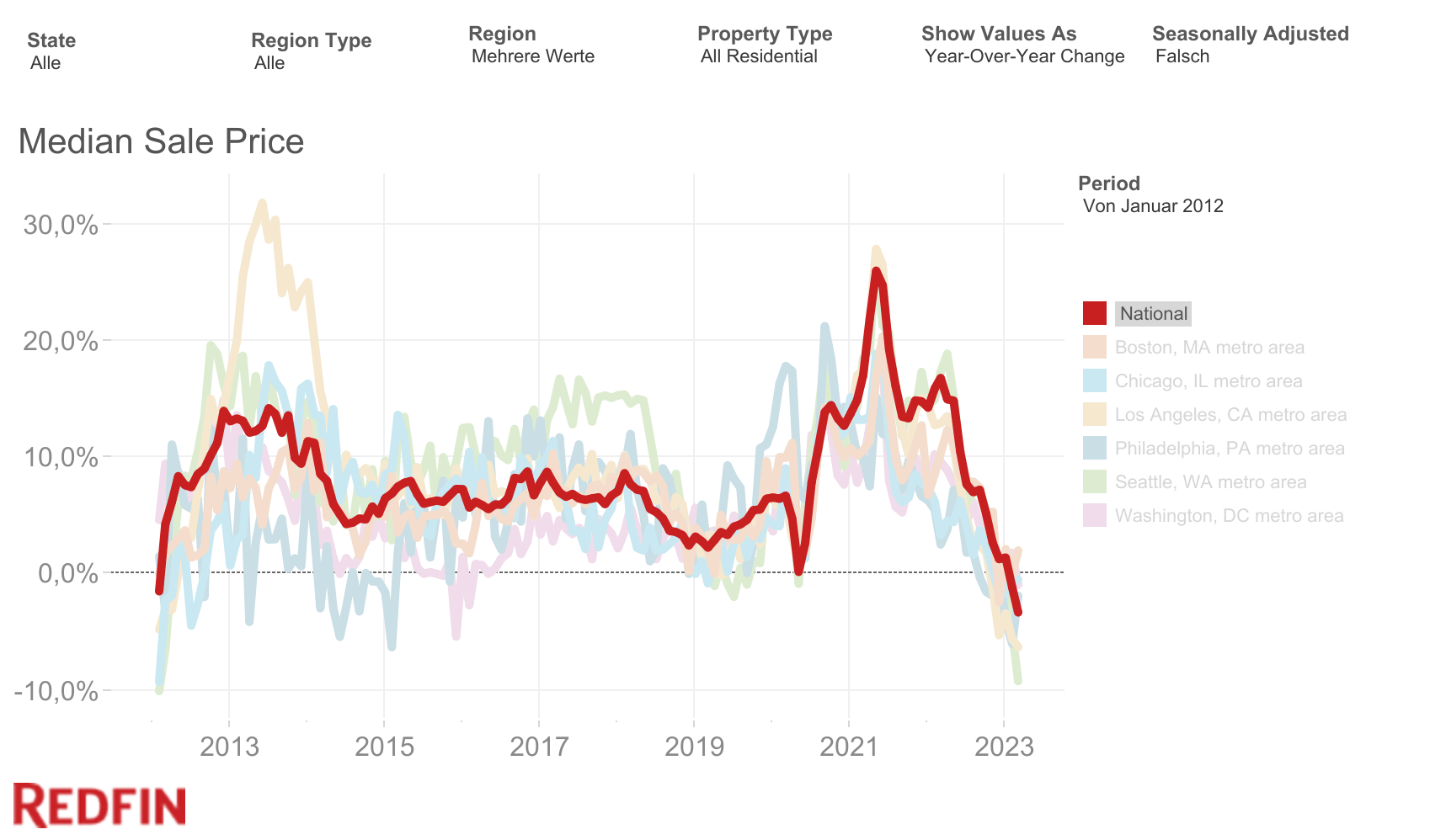

These challenges are also visible in the residential space. According to just-released numbers from Redfin , the median home sales price in the United States fell 3.3% in March, the steepest decline since the Great Financial Crisis.

{kind=link}

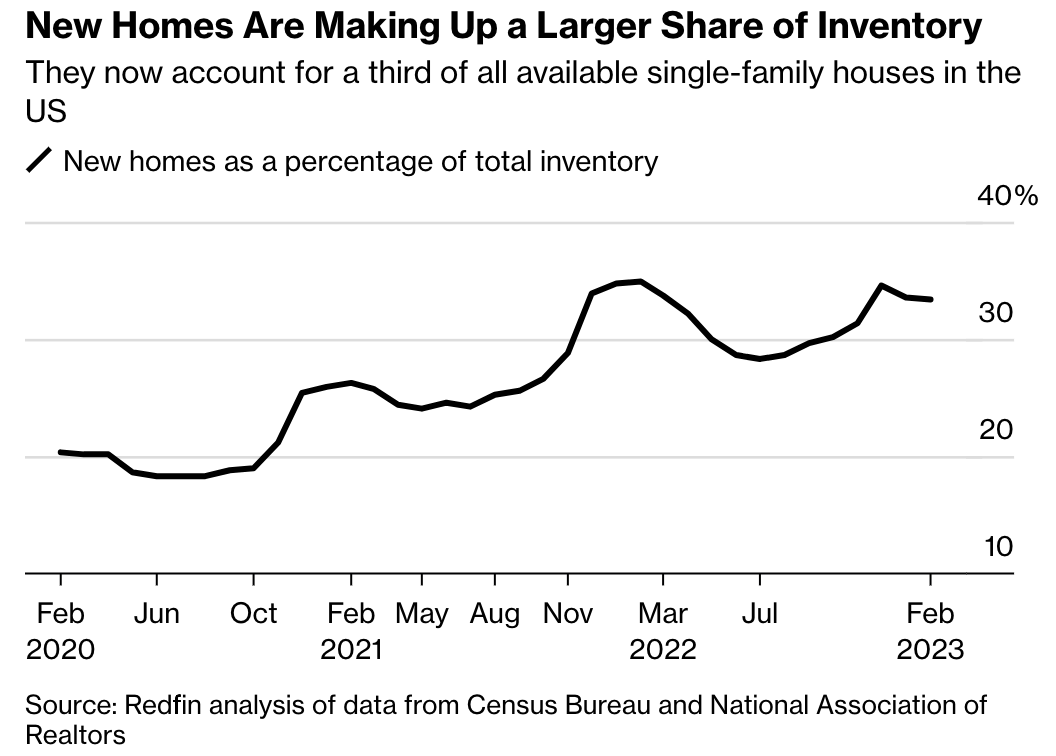

However, because high rates keep people from moving, the supply of new homes remains very low, triggering bidding wars in some areas, despite the aforementioned challenges.

One indicator that confirms this is the one below. Roughly 33% of all new home sales are from new homes.

{kind=link}

With all of this said, the market could be in for more weakness - on top of the ongoing issues highlighted by, i.e., Wells Fargo.

St. Louis Fed President James Bullard believes that rates need to be hiked by at least another 50 basis points. He cited a strong labor market as a reason to maintain a steady pace of hikes. He is not wrong, as labor fundamentals have proven over and over again to be robust. Unfortunately, this is largely due to structural issues, which are somewhat hiding the weakness of the economy - in my humble opinion.

"The labor market just seems very, very strong," Bullard said, according to Reuters. With the prospect of a hot jobs market supporting strong consumption, "it doesn't seem like the moment to be predicting that you have a recession in the second half of 2023," he said.

I also believe that this is one of the biggest issues facing the market. As I wrote at the start of this article, the Fed isn't as supportive as it used to be in prior cycles. It has no choice but to keep rates high until it has lowered inflation to 2-3%.

Even sudden rate cuts in the case of escalating banking fears would require the bank to quickly return to hiking, as it cannot risk a second wave of inflation. This was an issue also highlighted by the IMF earlier this month .

My Thoughts On Real Estate Stocks

In light of these risks, I'm very cautious. However, I'm not short anything. I always approach macroeconomic risks from a buyer's perspective, as weakness often comes with opportunities.

The aforementioned XLRE ETF is a well-diversified real estate ETF with $4.5 billion in assets under management. It has an expense ratio of 0.10%, which I believe is fair.

This ETF was incepted in 2015, and it has 30 holdings. The average weighted market cap is $51 billion, which indicates that it is overweight in some large companies.

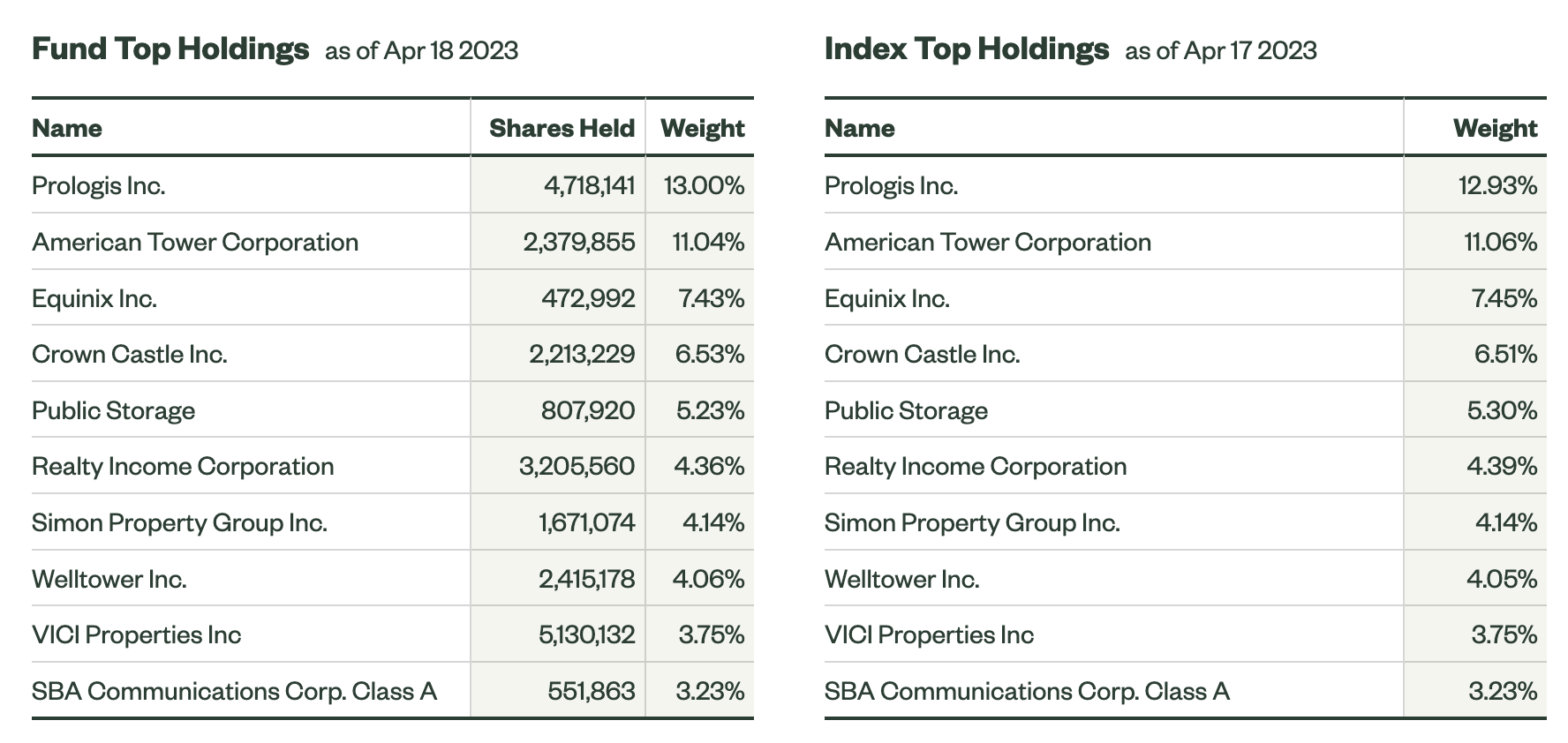

The ETF currently yields 3.7% and has significant exposure in the industrial REIT Prologis (PLD) and the cell-tower REIT American Tower (AMT).

In other words, it does have a satisfying yield, but it mainly focuses on REITs that are able to grow (a growth and value mix, so to speak).

{kind=link}

I like the ETF and I have a similar approach when it comes to investing.

I recently covered a few REITs that I have put on my watchlist. Feel free to read them if you want to know what I'm looking at (and why):

- Extra Space Storage (EXR) - I own it.

- Public Storage (PSA) - I also own it.

- American Tower - I don't own it, but I would like to buy it.

- Equity LifeStyle Properties (ELS) - no position, but looking for an entry.

- Prologis - no recent article yet, but attractive in light of re-shoring supply chains and automization.

- STAG Industrial (STAG) - same as Prologis.

I'm also monitoring Realty Income (O), Crown Castle (CCI), and several others that might become attractive when prices continue to fall.

With that said, I do believe that real estate stocks have more downside. Credit conditions are likely to deteriorate further, putting additional pressure on prices, financing, and tenant health.

FINVIZ

However, my strategy is not to wait until I believe that we're in for a bottom but to assess the stocks that I like individually. The odds of buying the exact bottom are very small. I buy whenever I start to like the valuation, even if I expect that prices have more downside. With a long-term mindset, I am able to average down if needed, but buy at prices that are way off their all-time highs.

This strategy worked really well for me since stocks peaked last year, and I will continue to apply it in what looks to become a rather troubled real estate sector.

So, if you have any questions regarding real estate stocks you like, feel free to ask them in the comment section.

Takeaway

In this article, we discussed my view on the real estate sector, using the XLRE ETF as a benchmark. Real Estate stocks have been in a consistent downtrend since the end of 2021, as a mix of high inflation and rising rates have caused a toxic environment for credit conditions. Even worse is that this is likely to continue, as the Fed is unlikely to start cutting rates soon and because tight credit conditions are just now starting to impact the health of CRE loans.

While I urge investors to be careful, which means assessing the credit risks of their REIT holdings, I am a buyer during corrections. In this article, I gave readers some of the stocks that I'm watching and a buy-on weakness strategy.

Using XLRE as a benchmark, I believe we could see 10-15% more downside. If that happens, I will deploy more cash from the reserve I've been building over the past few quarters.

Needless to say, going forward, I will focus on individual REIT picks and provide in-depth info, using this theoretical (big picture) article as a basis.

So, if you have suggestions or questions, please let me know in the comment section down below!

For further details see:

XLRE: Real Estate Is In Trouble