XMTR - Xometry: Reiterate Buy Rating As Recent Performance Suggests A Turnaround

2023-07-13 07:35:15 ET

Summary

- I recommend a buy rating for Xometry stock due to the growth potential in the digital manufacturing market.

- XMTR's integration with Alibaba 1688, a marketplace with around 30 million users per year, should boost revenue, with no margin dilution anticipated.

- XMTR should maintain strong revenue growth and eventually reach breakeven as it expands its gross margin.

Investment action

I recommended a buy rating for Xometry ( XMTR ) when I wrote about it the last time as I continue to see XMTR as a frontrunner serving a massive TAM, despite near-term volatility.

Based on my current outlook and analysis on XMTR, I continue to recommend a buy rating. I expect XMTR to continue to grow as guided given that the previous issues that plagued the business is not largely resolved (as seen from the results).

Business

Powered by AI, XMTR is an online marketplace for custom-made products. XMTR's innovative software has enabled the creation of a global marketplace for the sale and purchase of custom manufactured components and assemblies, allowing both buyers and sellers to benefit from the platform.

Industry & Peers

In 2021, the global market for digital manufacturing was estimated to be worth USD 320 billion, as reported by Straits Research . At a CAGR of 16.5% between 2022 and 2030, the market is projected to reach $1.37 billion by 2030. The market share held by North America is the largest, and it is expected to grow at a CAGR of 15.8% over the forecast period.

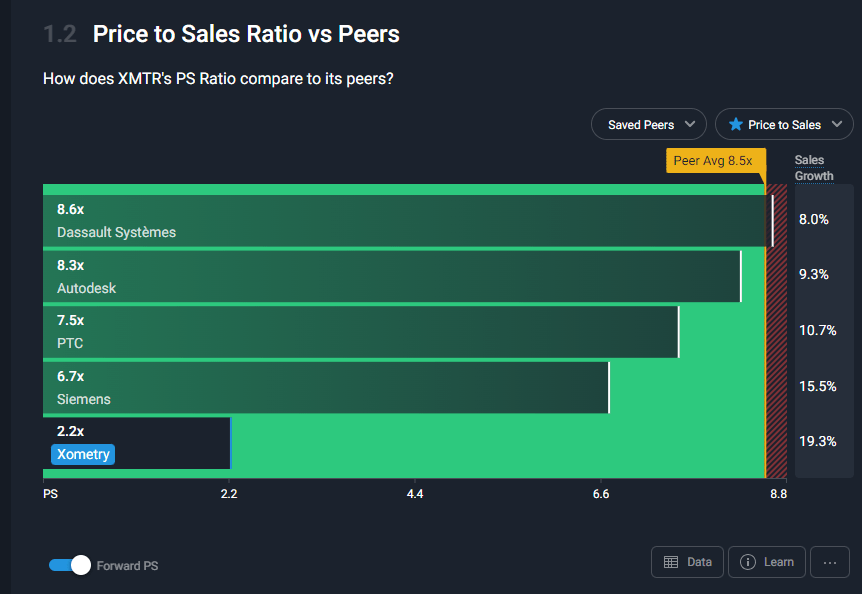

Dassault Systemes ( OTCPK:DASTY ), Siemens AG ( OTCPK:SIEGY ), Autodesk ( ADSK ), PTC ( PTC ), etc. are just a few of the major competitors in this wide market.

Because of benefits like reduced repetition and the elimination of human error, I predict that the use of digital technologies in manufacturing will continue to increase. The development and widespread use of innovative tools like 3D scanning, BIM, AR, and drones for building purposes should also contribute to the expansion of the digital manufacturing market.

Qualitative review

After months of precipitous decline, XMTR's stock has found support thanks to its performance in the most recent quarter. With a record number of buyers added and strong order growth in 1Q, it appears as though the core problem that has hurt the business—supplier engagement and buyer pricing issues—has been resolved.

I also have faith in the expansion plans. For example, XMTR's integration with Alibaba 1688 should be complete by the end of the current quarter. In the context of the 1688 marketplace, which sees around 30million users per year, XMTR technology is being used to provide instant quotes for custom parts. I think we could see a beat to guidance this year because management is not factoring in any revenue potential from this partnership in 2023. In addition, there will be no margin dilution because the 1688 margins profile is consistent with orders in the marketplace.

I continue to stay positive on the business.

Quantitative review

{kind=link}

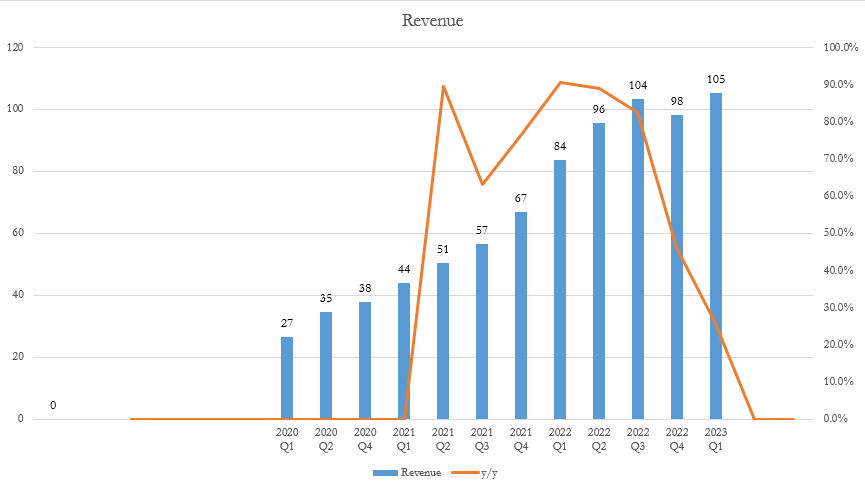

XMTR reported mixed 1Q results, with revenue growth of 26% Y/Y, well ahead of the guided range of 20 to 22%, but adjusted EBITDA came in below guidance. However, to be objective, the slight adjusted EBITDA miss was due to one-off items around SOX implementation and international investments. Putting these aside, the fact that Marketplace's gross margin improved 170bps is a positive takeaway.

I expect revenue growth to remain strong at the current trajectory, growing 20+% and hitting FY23 guidance. XMTR has clearly demonstrated its ability to grow revenue sequentially, as per the quarterly chart. While the 20+% growth is a slowdown from LTM levels, I think being conservative is safer here. Looking farther out, I see XMTR reaccelerating its growth as it continues to gain share in this fast-growing industry.

{kind=link}

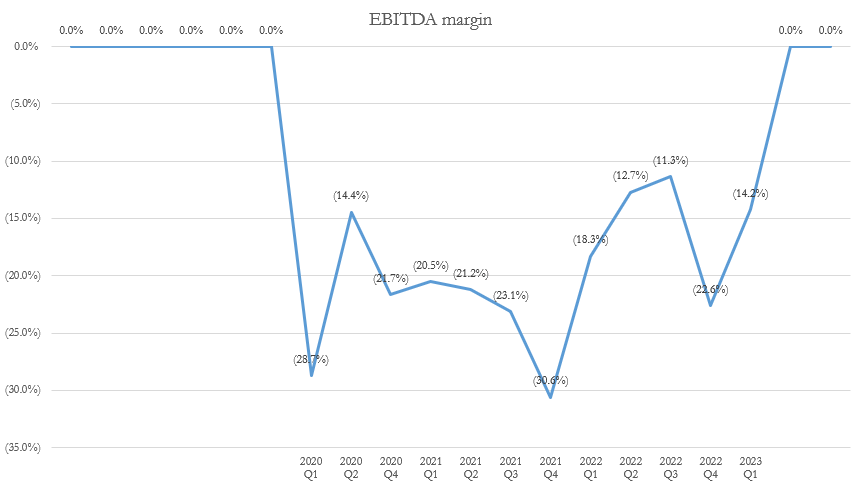

XMTR is unprofitable today, but it should be on the right track to breaking even as it continues to expand its gross margin, and one-off expenses taper off. XMTR has done a great job so far, I’d say, as it improved the EBITDA margin from -32% in 2019 to -14% today. Hence, I expect it to reach breakeven soon.

{kind=link}

{kind=link}

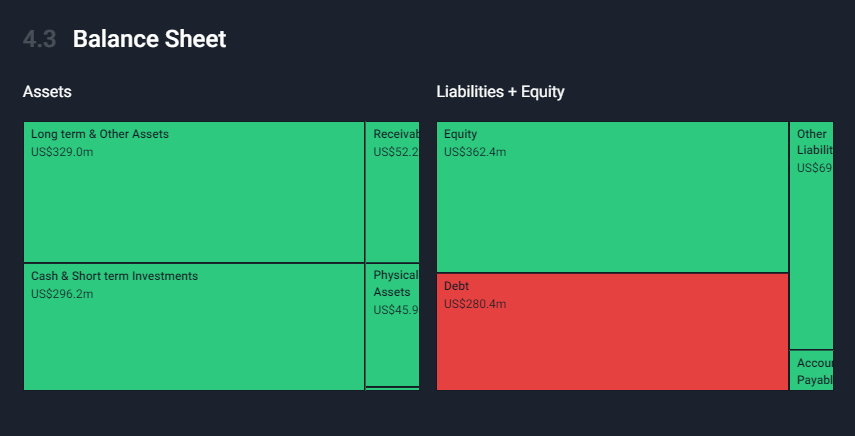

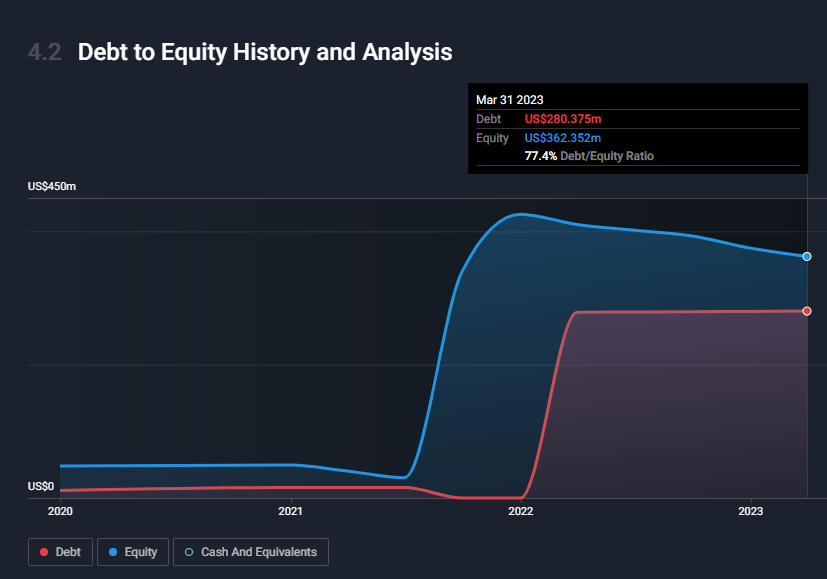

XMTR is in a net cash position with a similar ratio between the amount of cash and debt on hand. While there is no balance sheet risk today, if XMTR continues to burn cash, the net cash position will flip to net debt. This will put them in a riskier position, requiring a potential capital raise.

Valuation

As XMTR is not profitable today, using P/S ratio is the recommended way to value the business.

XMTR is trading at a steep discount to peers on a P/S basis despite having a faster growth profile. I believe this is due to XMTR's loss-making status and its relatively smaller size.

{kind=link}

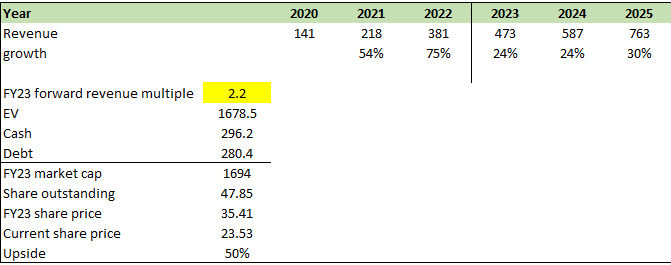

I believe XMTR will meet management's FY23 guidance given the rate of growth today and the 1688 partnership potential that is not embedded in the guidance. Post FY23, I made the conservative assumption that growth would remain slow for 1 more year before reaccelerating to 30% in FY25. While I think the multiple discount is too big relative to peers, I believe the market is unlikely to attach a premium as XMTR remains loss-making. Hence, I assumed XMTR P/S ratio to remain at 2.2x. This gives me a price target of $35.

{kind=link}

Risk

There is execution risk with XMTR given it is a relatively newly listed company. Companies that have only recently gone public tend to be younger and to grow more rapidly than more established businesses, making it all the more important to have proper mechanisms in place for hiring, training, paying employees, and monitoring management. Stock prices tend to fall when sales don't go as planned because of the unexpected drop in revenue that results.

Conclusion

Based on my analysis and outlook, I reiterate my buy rating for XMTR. Despite near-term volatility, XMTR continues to be a frontrunner in serving a massive TAM. The recent performance suggests a turnaround, with the core issues of supplier engagement and buyer pricing being largely resolved. The integration with Alibaba 1688 holds significant revenue potential and is expected to contribute to beating guidance. While XMTR reported mixed 1Q results, the strong revenue growth and improved gross margin are positive indicators. I expect XMTR to maintain strong revenue growth and eventually reach breakeven as it expands its gross margin.

For further details see:

Xometry: Reiterate Buy Rating As Recent Performance Suggests A Turnaround