XMTR - Xometry: Solid Growth Despite Headwinds

2023-12-11 13:12:03 ET

Summary

- Xometry is scaling its business and improving profitability, despite challenges in the manufacturing sector.

- The company's online marketplace connects buyers with manufacturing suppliers, offering improved supply chain resiliency and improved efficiency.

- Xometry's stock still looks undervalued on an absolute basis given near-term prospects, but it is beginning to look expensive relative to manufacturing technology peers.

Xometry ( XMTR ) continues to scale its business at a reasonably rapid pace, particularly given the headwinds currently facing the manufacturing sector. The company is also progressing towards profitability, with gross and operating profit margins steadily improving.

Given Xometry's status as a small and unprofitable technology company with exposure to manufacturing demand, it has been out of favor with investors over the past few years. With interest rates likely having peaked, and consensus growing regarding a soft landing, this could be set to change going forward. This is supported by the fact that the company is approaching profitability and growth is reaccelerating.

Market

Xometry offers an online marketplace to connect buyers looking to outsource manufacturing with suppliers of manufacturing services. This type of service is valued in the market, as it helps to reduce a number of common problems. The manufacturing base is generally fragmented, across both services and geography, making procurement inefficient. Supply chains can also prove fragile, as shown by the pandemic, and lead times are often long.

By aggregating supply and offering a centralized marketplace, Xometry hopes to offer buyers improved supply chain resiliency, shorter lead times, lower costs and higher quality production. Xometry can also lower customer acquisition costs for suppliers and provide access to greater demand, in addition to supplemental business services.

This type of service is not a universal positive for buyers and suppliers though. By aggregating demand, Xometry potentially increases its bargaining power with buyers, allowing it to charge higher prices. Reducing friction in the supply chain could also pressure smaller manufacturers, by exposing them to greater competition. In addition, Xometry intermediates suppliers, which commoditizes their services.

{kind=link}

Figure 1: Pain Points Addressed by Xometry's Platform (source: Xometry)

Through its network of suppliers, Xometry is able to offer its customer base a wide range of manufacturing services. As a result, Xometry is able to offer buyers services across prototyping and low-volume production, through to high-volume production. This helps to differentiate it from companies like Proto Labs ( PRLB ), which offer a far narrower range of services. Xometry outsources production though, which could be considered a positive or a negative. Outsourcing makes Xometry dependent on suppliers and reduces its role to intermediary. It also simplifies the business and reduces capital and labor requirements.

Figure 2: Core Manufacturing Capabilities (source: Xometry)

Xometry estimated that its addressable market was worth 260 billion USD in 2021, based on the manufacturing processes offered on its platform at the time. This estimate has now expanded to over 2 trillion USD though, due to the acquisition of Thomas Publishing. This estimate covers essentially all manufacturing activity though, and doesn't really reflect Xometry's true opportunity, which is much smaller. For example, Shapeways ( SHPW ) estimates that the digital manufacturing market was worth 39 billion USD in 2020, growing to 120 billion USD in 2030.

Xometry competes with service bureaus and brokers for buyers, including the service bureaus of OEMs like Stratasys ( SSYS ) and 3D Systems ( DDD ). Additive manufacturers offer a fairly narrow service with limited scale though. Proto Labs is more similar, and moving in the same direction, but currently offers a narrower range of manufacturing services. Xometry also competes with brokers and listing services for suppliers.

Xometry

Xometry operates an online marketplace which connects buyers with suppliers of manufacturing services. Buyers transact online, uploading a design file, which Xometry uses to provide an automated quote. Xometry isn't a pure marketplace though, instead, it sources from suppliers after providing a quote to buyers. It is an intermediary that bears the risk of a buyer not being satisfied or production costing more than expected. This means it reports higher revenue but lower margins than a pure marketplace. It could also help to prevent buyers circumventing the platform though. The majority of the company's revenue comes from buyers on the platform.

Xometry's platform supports a wide range of manufacturing processes and allows buyers to source parts for prototyping and low-volume production, through to high-volume production. This is supported by Xometry's network of over 10,000 suppliers, with access to an additional 500,000 suppliers through Thomasnet.

Xometry is supporting its marketplace business by both making it more scalable and increasing the range of services available through its supplier network. For example, Xometry introduced its Industrial Buying Engine in 2022, which helps customers source from over 500,000 suppliers on Thomasnet in a low-touch manner. Xometry recently announced a partnership with Google Cloud to leverage Vertex AI, enabling instant quoting for new categories on Xometry's AI-powered marketplace. This is supported by Xometry’s acquisition of Thomas Publishing, which provides additional data from suppliers that offer over 70,000 industrial processes.

Xometry launched its Teamspace collaboration tool in October . Teamspace moves Xometry beyond individual buyers and parts to procurement teams managing assemblies and products. This could support revenue growth and marketing efficiency going forward. Teamspace is expected to begin contributing to active buyer growth in the fourth quarter.

In addition to its marketplace business, Xometry also generates revenue by providing suppliers with services. Xometry Supplies was introduced in the US in 2019, enabling suppliers to access tools, materials and supplies through Xometry. The company also introduced financial services in 2020 to help support the capital needs of suppliers.

Xometry acquired Thomas Publishing and Fusiform in 2021, expanding its supplier services to digital marketing and data solutions. The company continues to develop the marketing solutions on the Thomasnet platform. This is a high margin source of revenue, but Supplier Service growth appears sluggish at the moment.

{kind=link}

Figure 3: Supplier Services (source: Xometry)

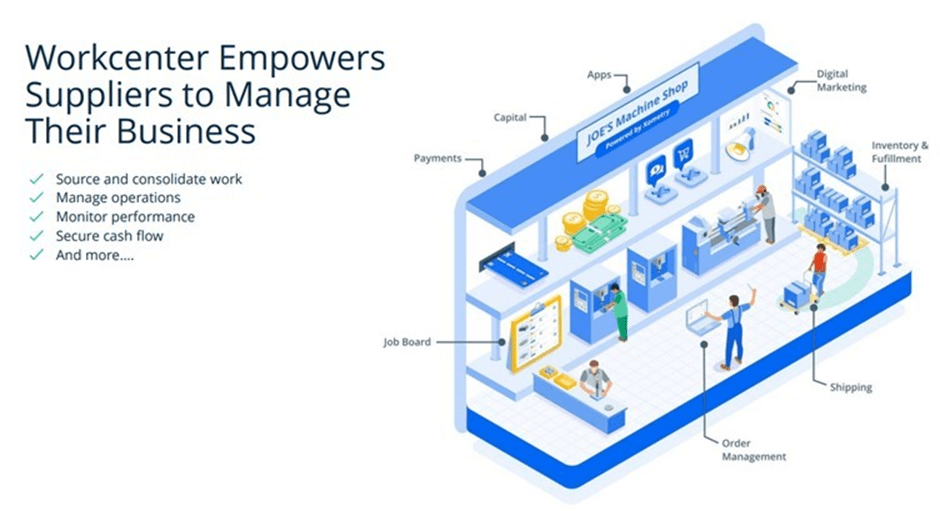

Xometry also offers suppliers Workcenter, a cloud-based manufacturing execution system that supports both Xometry and non-Xometry work. This could conceivably be a large business in its own right, but Xometry still needs to demonstrate customer adoption, which is likely being hampered by the difficult macro environment.

{kind=link}

Figure 4: Workcenter Supplier Service (source: Xometry)

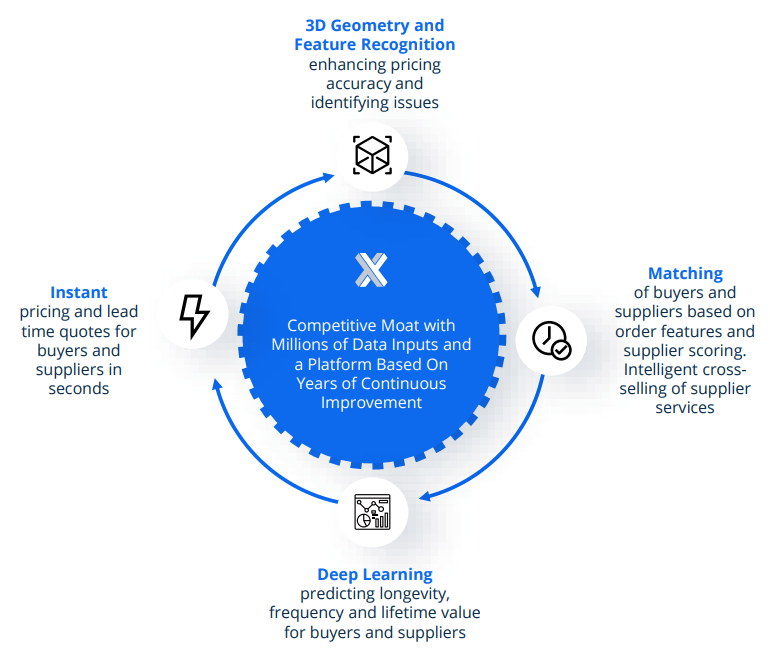

Xometry believes that its competitive advantage is based on its proprietary pricing and matching algorithms, data and network of buyers and suppliers. Xometry's ability to price accurately and effectively connect buyers and suppliers should improve with data and scale.

Xometry's marketplace potentially benefits from network effects, with suppliers attracting suppliers and vice versa. This is likely a weak competitive advantage though as there is little to stop buyers and suppliers connecting through competing platforms simultaneously.

{kind=link}

Figure 5: Xometry's Competitive Moat (source: Xometry)

Financial Analysis

Xometry’s revenue increased 15% YoY in the third quarter to 119 million USD. Marketplace growth of 22% was offset by a 16% decline in Supplier Services revenue, although this was primarily the result of the discontinuation of low margin tools and materials sales. Adjusting for the exit of the supplies business, revenue growth in the third quarter was 17% YoY.

Marketplace growth was driven by international markets, particularly Europe, where Xometry’s revenue increased 78% YoY. International markets are a focus area for Xometry, and customers and orders are ramping at a solid pace. Recently launched markets include the UK and Portugal. Through its websites, Xometry provides localized marketplaces in 14 different languages with a network of suppliers across Europe, Asia and North America. Xometry is also collaborating with Alibaba Group, recently launching its instant quoting technology on 1,688 B2B wholesale marketplace mobile apps. The Alibaba relationship is immaterial at this point in time though.

From a service perspective, growth has generally been solid, with injection molding an area of particular strength. Xometry has stated that this is being driven by investments in technology and processes.

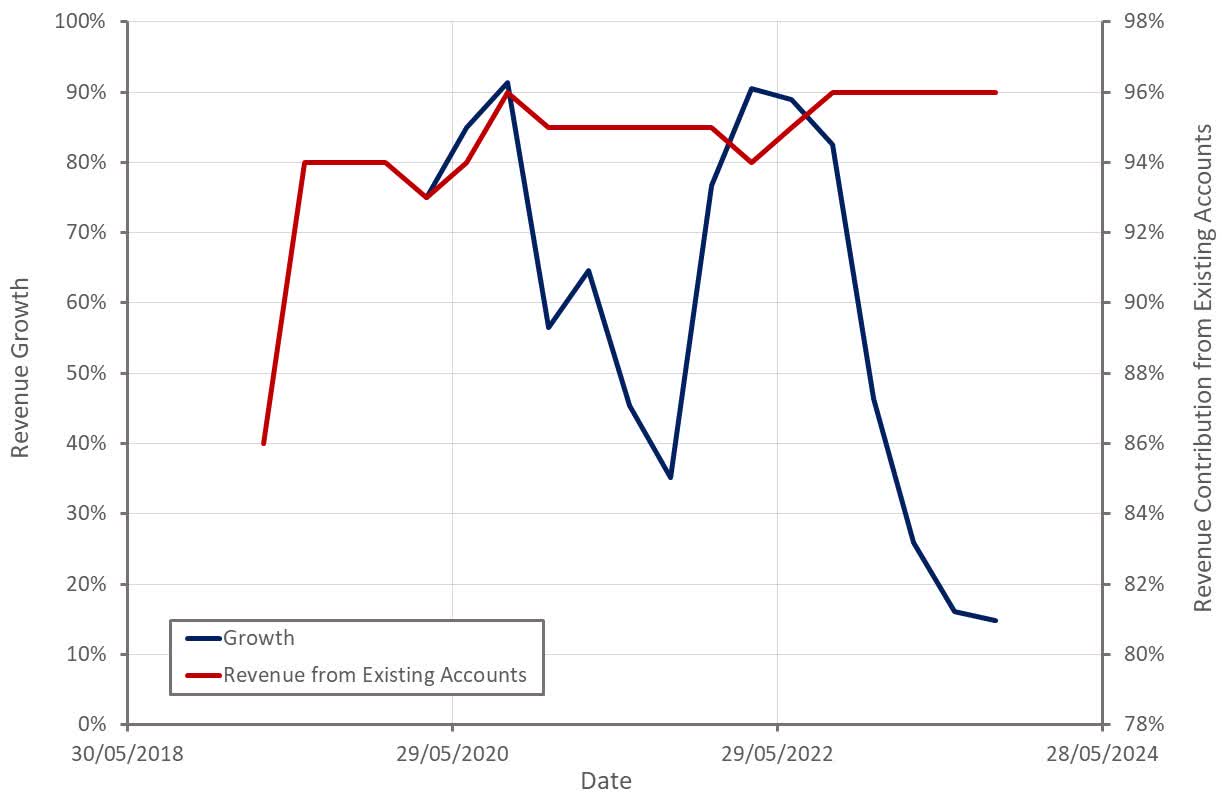

Marketplace activity has been robust, with both active buyers and orders growing over 40% YoY in the third quarter. Revenue growth is trailing this though as the average order size has been shrinking. Xometry expects revenue growth to converge with active buyer growth going forward. As a result, the company expects roughly 40% YoY marketplace revenue growth in the fourth quarter, along with fairly flat QoQ Supplier Services revenue. This should result in approximately 30% overall revenue growth, which will be aided by a number of orders which pushed out from the third quarter.

{kind=link}

Figure 6: Xometry Revenue Growth (source: Created by author using data from Xometry)

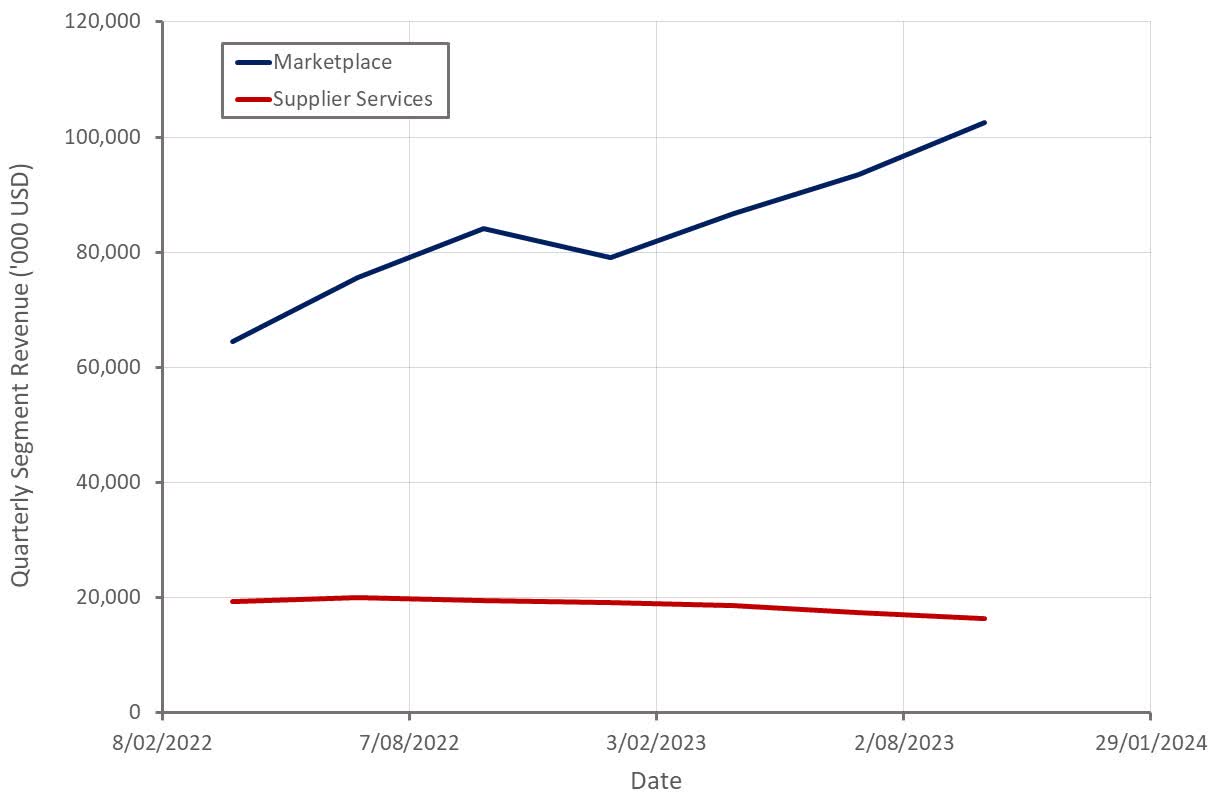

Xometry's Supplier Services business is not gaining traction like the marketplace business, which is weighing on growth and margins. The discontinuation of the sale of supplies in the US negatively impacted Supplier Services revenue by approximately 2 million USD in the third quarter. Even excluding this impact, revenue would have been down roughly 6% YoY though.

Advertising and marketing services revenue was stable sequentially and the number of active paying suppliers fairly stable YoY. Excluding the impact of the exit of the supplies business, active paying suppliers increased 4% YoY.

{kind=link}

Figure 7: Xometry Revenue by Segment (source: Created by author using data from Xometry)

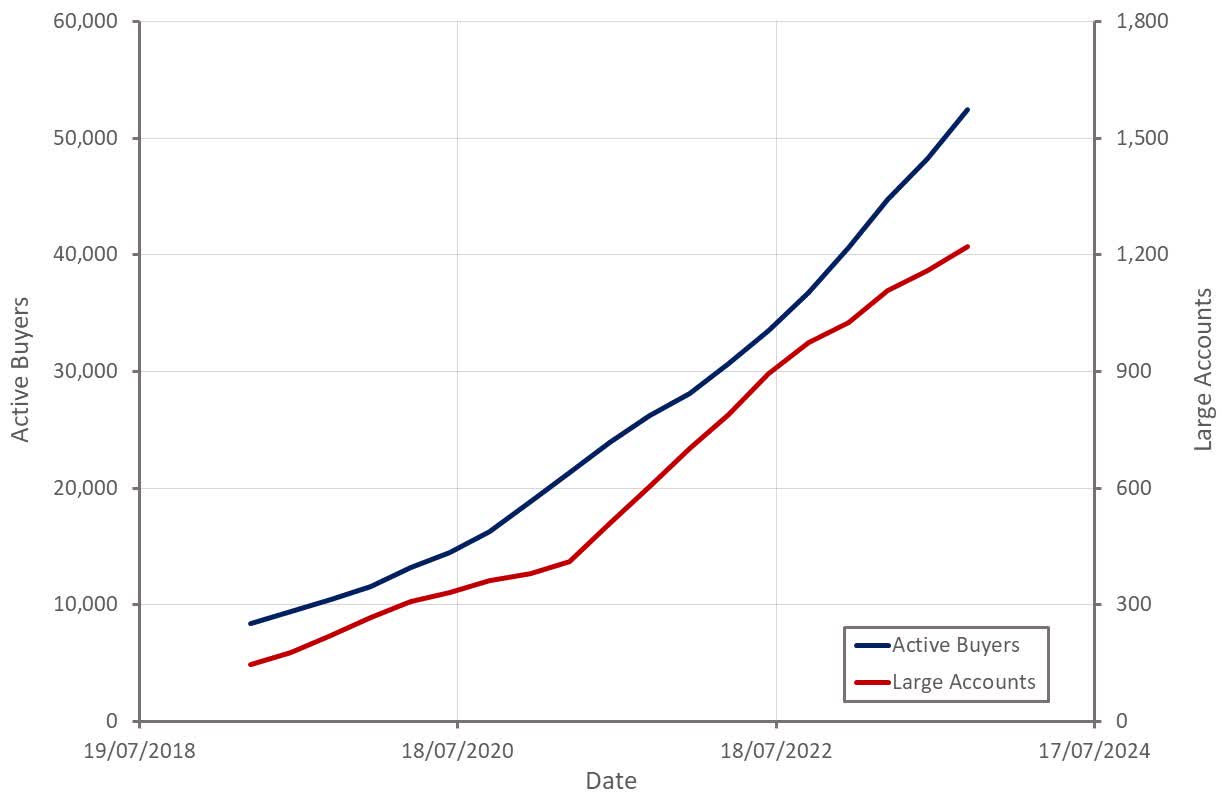

The number of active buyers on Xometry's platform increased 43% YoY in the third quarter to 52,467. Xometry classifies all individuals purchasing through its marketplace as a buyer though, meaning the actual number of organizations is likely to be much lower. While buyer growth has been strong, this has been partly offset by lower average revenue per buyer.

{kind=link}

Figure 8: Xometry Active Buyers (source: Created by author using data from Xometry)

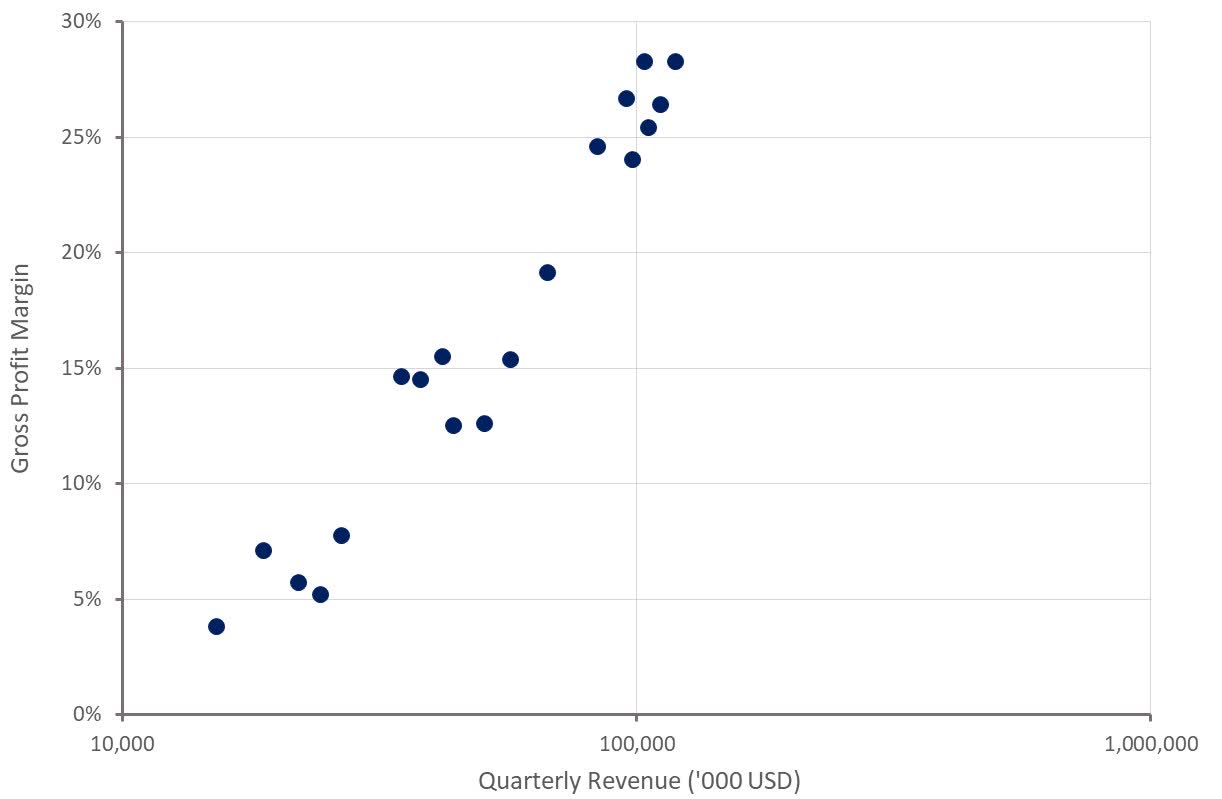

Xometry's gross profit margin was 38.9% in the third quarter. While Xometry counts operations and support expenses as an operating cost, I believe this is better treated as a cost of revenue. Operations and support expenses are the costs incurred in support of customers and sellers on Xometry's platform. While this lowers Xometry’s gross profit margins, it also indicates that gross profit margins are steadily increasing with scale.

In particular, Marketplace gross profit margins are improving as the business scales. Marketplace gross profit margin is currently around 31%, with Xometry having a long-term target of 35-40%. Rapid growth of the marketplace business is pressuring gross profit margins though.

Suppliers Services gross profit margin is around 87%, supported by the exit from the sale of supplies. The high gross margin of Thomas marketing and advertising services and growing financial services are also tailwinds.

{kind=link}

Figure 9: Xometry Gross Profit Margin (source: Created by author using data from Xometry)

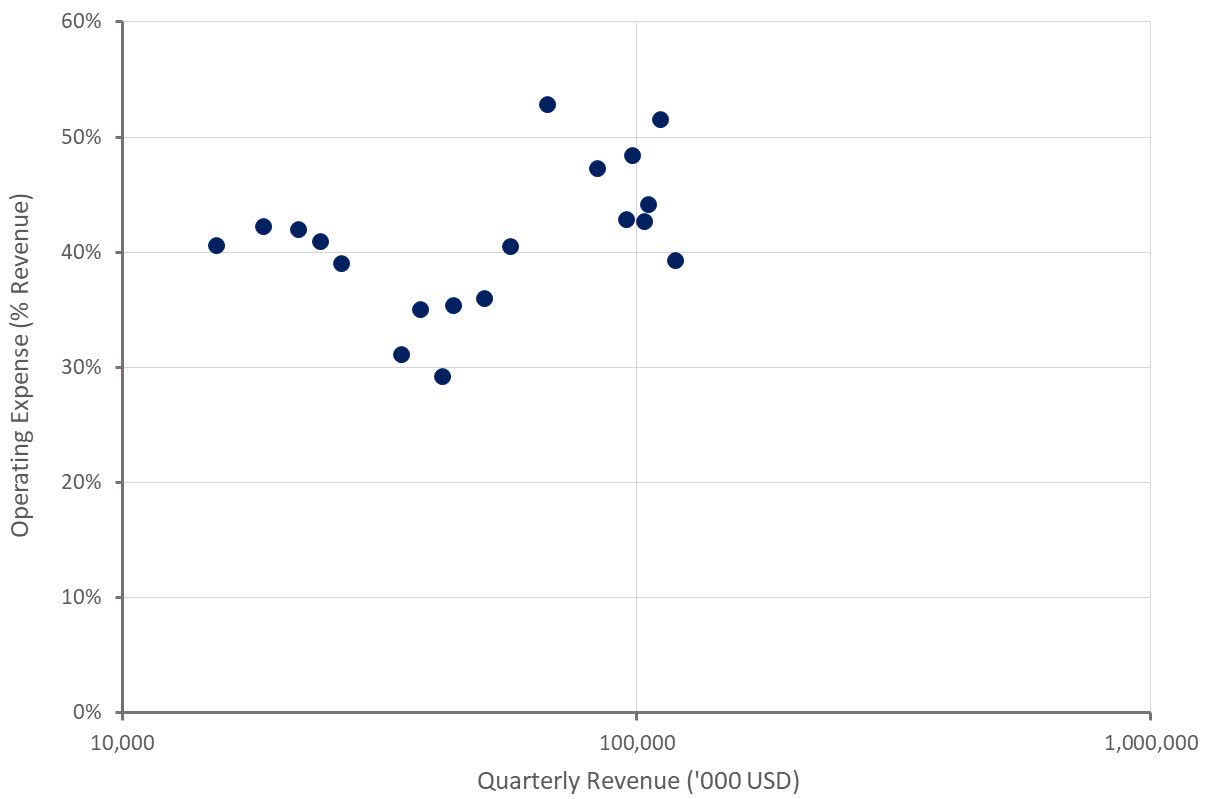

Xometry's operating expenses have been elevated in recent quarters, although this is now beginning to correct on the back of cost cutting initiatives (headcount reduction, consolidation of office space). Non-GAAP operating expenses declined 2 million USD sequentially in the third quarter.

Margins are also being pressured by expansion of the less mature international business. Xometry's US business currently has an operating profit margin of -7%, compared to -26% for the international segment.

Xometry believes it could achieve adjusted EBITDA breakeven in the fourth quarter of 2023 and is targeting adjusted EBITDA profitability in 2024. This seems feasible based on the recent performance, assuming growth is solid in 2024.

{kind=link}

Figure 10: Xometry Operating Expenses (source: Created by author using data from Xometry)

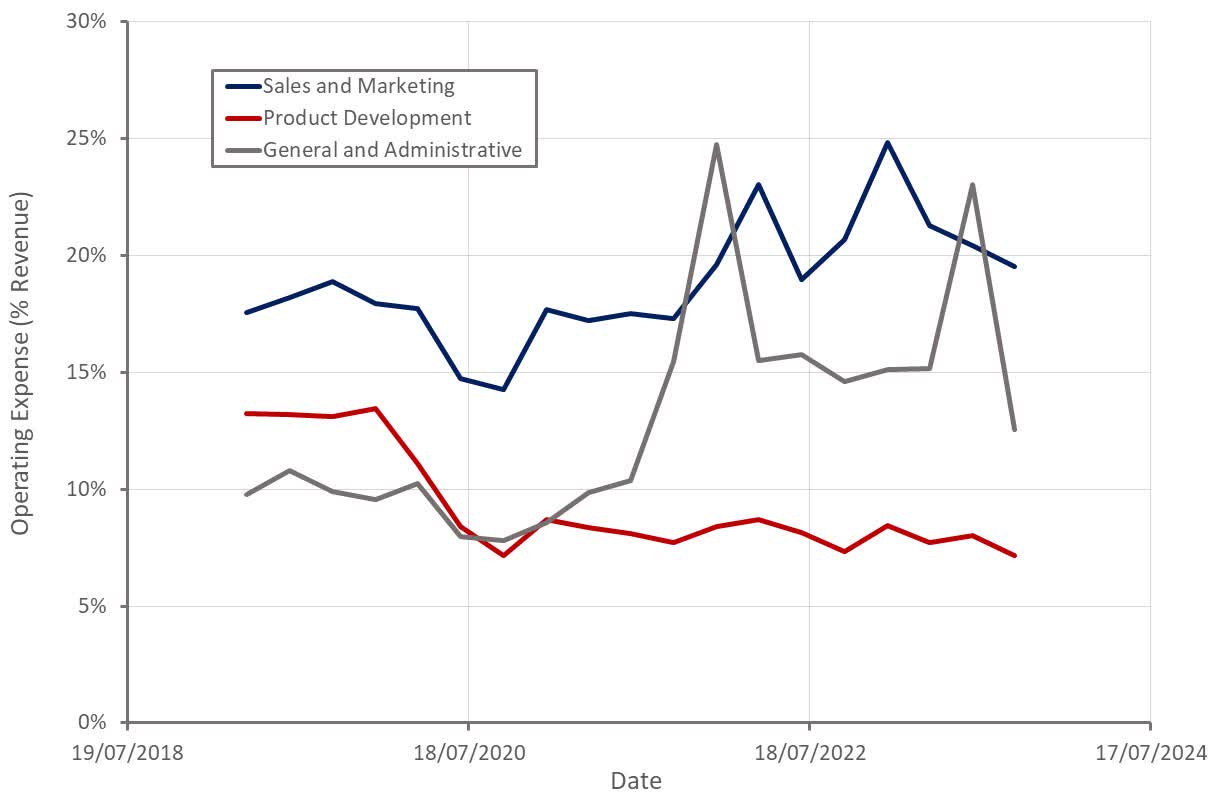

Recent operating cost increases are largely due to sales and marketing, and general and administrative expenses. Product development costs demonstrate that this isn’t really a technology business. General and administrative expenses have been elevated but now appear to be normalizing, which will go a long way towards helping Xometry reach profitability.

The key to the company’s long-term success is the efficiency of sales and marketing though, and on this front the jury is still out. Xometry has been pulling back on marketing to support its profitability goals, with ad spend down 7% YoY in the third quarter. As a result, Xometry estimates that its cost to acquire a net new active buyer declined 27% YoY in Q3.

{kind=link}

Figure 11: Xometry Operating Expenses (source: Created by author using data from Xometry)

Conclusion

Xometry's share price has declined significantly since it became a public company in 2021. This can partly be attributed to the company's high initial valuation and macro headwinds, but also appears to be due to excessively negative investor sentiment.

Xometry currently has around 277 million USD of cash and cash equivalents on hand, providing significant runway in which to achieve profitability. Outside of a serious deterioration in the macro environment in coming months, the company's current lack of profits should not be a large concern for investors.

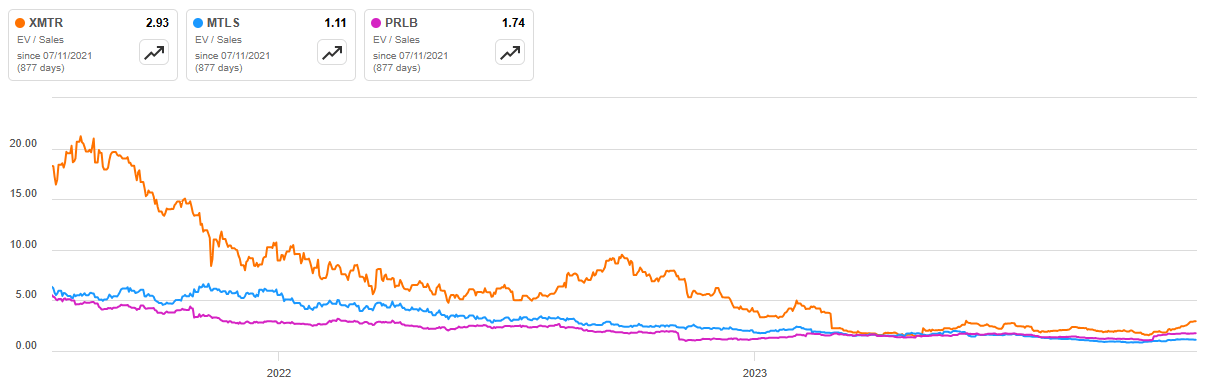

Xometry also continues to expand its business at a relatively robust rate. With profitability now on the horizon, investor sentiment appears to be improving, resulting in the stock rerating higher. Despite this Xometry's valuation is still only modest given its growth runway and potential profitability. Xometry is beginning to look somewhat expensive relative to similar companies though.

{kind=link}

Figure 12: Xometry Relative Valuation (source: Seeking Alpha)

For further details see:

Xometry: Solid Growth Despite Headwinds