FANG - XOP: M&A Exposure With Potential For 100% Upside

2023-10-29 11:39:08 ET

Summary

- SPDR® S&P Oil & Gas Exploration & Production ETF (XOP) provides exposure to the US oil & gas M&A scenario.

- The portfolio has the potential for 100% upside if valued at the average price of recent acquisitions.

- The sector is focused on deleveraging and capital return, with low growth expected.

Summary

SPDR® S&P Oil & Gas Exploration & Production ETF ( XOP ) is a near equal weight ETF with a focus on US oil & gas stocks. As I wrote recently in FENY ETF: U.S. Oil Sector Deleveraging Vs. Growth the sector looks modesty attractive from a deleveraging and capital return perspective vs. growth given the inability or unwillingness for the companies to invest in production expansion. However, the main caveat of this fund is that it may provide exposure to M&A activity as seen recently in the Hess ( HES ) and Pioneer ( PXD ) acquisitions, which I analyze in this article.

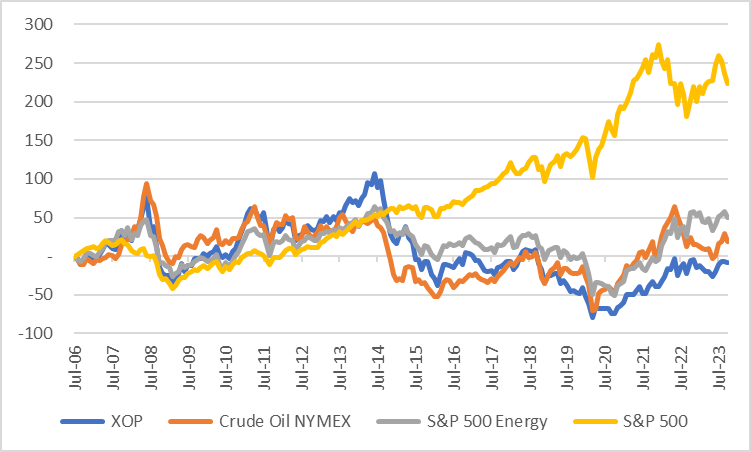

The ETFs performance has trailed Oil prices and the S&P 500 Energy index ( SP500-10 ) since the 2014 as the shale sector failed to deliver value, in my view.

{kind=link}

XOP vs Oil and SP Energy Sector (Created by author with data from Capital IQ)

A More Equal Weight Portfolio

XOP holds 58 stocks in the US oil and gas production sector with the top weighted being Southwestern ( SWN ) at 2.69% followed by Range ( RRC ) with 2.67% and Antero ( AR ) with 2.63%, not exactly household names. Exxon ( XOM ) is 2.4% for example, thus this ETF is a portfolio of mid-caps. The average market cap is US$37bn, excluding the majors, this falls to US$15bn.

I used consensus estimates for 90% of the portfolio (40 stocks) to calculate potential upside of 15% plus a dividend yield of 2% for YE24. This looks reasonable given the rebound in oil prices that should help drive EBITDA, if average oil is US$80bbl.

XOP Consensus Price Target Upside (Created by author with data from Capital IQ)

EBITDA Growth Challenged

On consensus estimates the ETF has 14% EBITDA growth in YE23 but then falls to 3% in YE24. This does not appear to be a growth sector. In fact, I compared the YE22 absolute EBITDA vs YE25 estimates, and most of the companies do not surpass YE22 results. This is calculated in the table below as EBITDA YE25/YE22, a ratio of 1 or less indicates lower EBITDA than in YE22.

The absence of EBITDA growth forecast by the market consensus is likely attributed to low production expansion i.e., capital discipline. Oil companies are more focused on maintaining production vs spending to grow. This strategy may be explained by a long-term view that oil demand is slowing as the world pursues de-carbonization and energy transition.

XOP Consensus EBITDA Growth (Created by author with data from Capital IQ)

Deleveraging Driver

As a direct consequence of low growth and capital discipline the sector should continue to reduce debt levels and payout free cash flow in dividends and share buy backs. The consensus net debt estimates point to a 28% reduction in YE24 and 20% in YE25. Leverage declines from .6x ND/EBITDA to .4x by YE25.

XOP Consensus Net Debt Reduction (Created by author with data from Capital IQ)

M&A option

I conducted a sensitivity analysis for the ETFs portfolio using the multiples at which Hess and PXD where acquired. Keep in mind that each company has fundamentals that may be more or less valuable i.e., accretive to the buyer. This is an exercise in food for thought.

Hess was acquired at an implied 8.4x EV/EBITDA multiple and PXD at 6.1x on YE24 estimates. I calculated what would be the price target for each stock at those valuations in the event of an acquisition and then averaged these two estimates to arrive at an upside potential. The first column is what the market uses to value the shares at current price target.

The ETF would have a 100% upside potential if all the stocks were acquired. An unlikely event but non the less an interesting analysis that may help identify some M&A candidates. I excluded the 3 majors given that its more likely they are buyers.

XOP M&A Scenario (Created by author with data from Capital IQ)

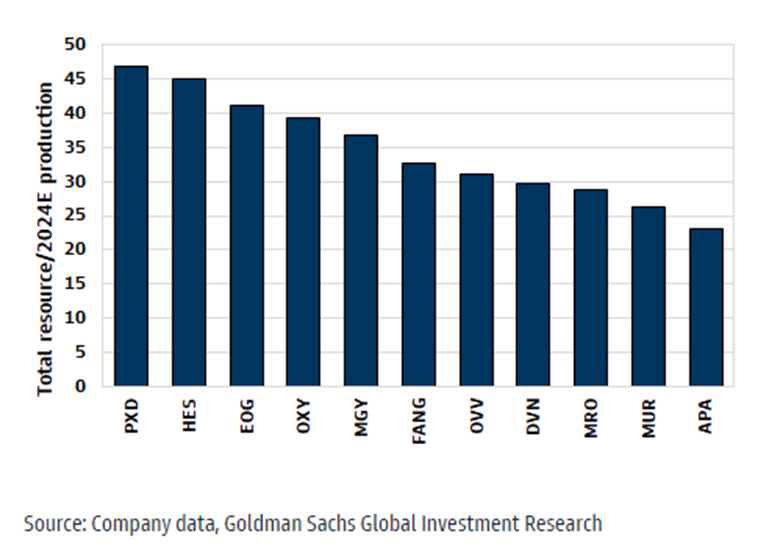

The chart is from a GS report that highlights oil reserves of a few companies that should be taken into consideration in an acquisition valuation. The buyer is not only acquiring current production but also the ability to tap into reserves at low cost. EOG ( EOG ), Magnolia ( MGY ) and Diamondback ( FANG ) are a few stand outs.

{kind=link}

Selected Oil Reserves by Company (Image by Goldman Sachs)

Conclusion

XOP is a buy. While oil price dynamics are likely to be volatile there seems to be rationality in global supply to support prices at which most US producers can generate free cashflow. At the same time the strategy to limit growth in pursuit of deleveraging and capital returns supports valuations. Finally, this ETF's structure provides added upside potential in an M&A environment.

For further details see:

XOP: M&A Exposure With Potential For 100% Upside