XOSWW - Xos Inc.: A Challenging Outlook

Summary

- Xos continues to be deeply unprofitable at the operating level despite ongoing turnaround efforts.

- While narrowing the product focus makes sense, the lack of new product development could impact its long-term competitiveness.

- Given the elevated funding risks, the discounted valuation is warranted here.

With its liquidity runway narrowing by the day, battery-electric commercial vehicle producer Xos, Inc. ( XOS ) has taken steps to refocus the overall product strategy around step vans while also driving cost cuts on the logistics side via recentered operations at the Tennessee facility and streamlined processes. The strategic pivot is a prudent move by management but presents significant opportunity costs - the heavy-duty XOS truck platform, for instance, gets minimum funding allocation and will be pushed out to FY24. The achievability of current P&L targets is a concern as well, particularly given the company's track record of overspending on staff and shelved projects post-SPAC listing. Overall, the stock screens cheaply for an EV name, but given the risk of execution missteps and more capital raises ahead, a discount seems justified.

Another Difficult Quarter Despite the Cost-Cutting Measures

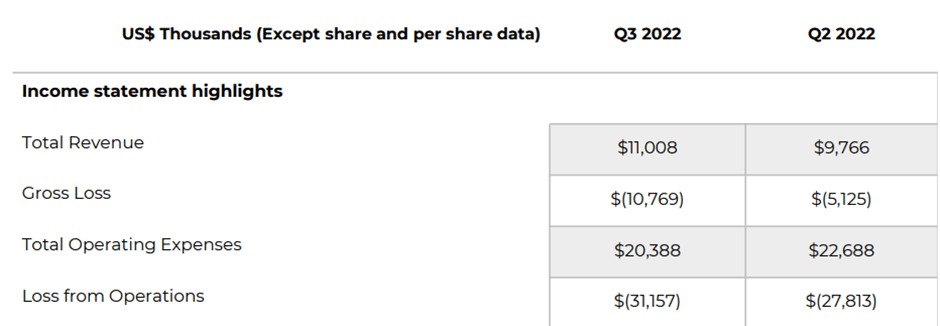

To recap, XOS ended Q3 with revenue ahead of a lowered consensus bar at $11m, supported by a QoQ acceleration in deliveries to 88 units (vs. 73 vehicles prior). The higher volumes came at the cost of lower selling prices, though, with the average price of 125k down sequentially from ~$134k last quarter. The big disappointment was the gross loss margin of -98%, a significant deceleration from -53% in Q2 as supply chain disruptions continue to weigh on profitability. Even after accounting for non-cash adjustments of ~$5m, the gross loss margin would still have been weak at -50%.

{kind=link}

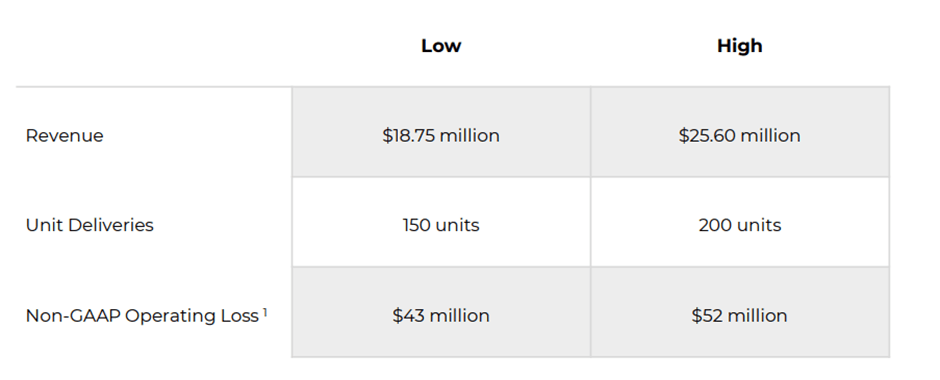

Yet, XOS maintains its guidance for positive gross profit by H1 2023 - for context, this is in line with the Q2 guidance update and a first for XOS as a public company. Similarly, the H2 2022 operating loss guidance range has been maintained at -$43 to -52m, implying -$12 to -$21m in operating losses for Q4, despite the ongoing cost cuts. While the reiterated guidance for 150-200 unit deliveries and $19-$26m in revenue for H2 2022 is more realistic, the high margin bar heading into Q4 results could drive more downward revisions in the upcoming quarter.

{kind=link}

A Prudent Strategic Pivot Toward Step Van and 'Hub'

The ambitious near-term outlook is based on the assumption that XOS' refocused core strategy will pay off. As part of the new plan, most of the R&D will be allocated to the step van product, as well as Hub products such as Xosphere, its proprietary fleet management platform customized for electric fleets. This decision makes sense, in my view, given the recent traction within the step van product (i.e., light to medium-duty commercial trucks). The recent Merchants Fleet deal , for instance, will see the acquisition of electric fleet vehicles as a part of its commitment to electrifying 50% of the fleet by 2030. Plans to implement the suite of 'Advanced Driver Assistance System' (ADAS) as a standard feature across XOS' step vans also bodes well for the order outlook.

As for Hub, the key focus will be on riding the secular growth potential of charging infrastructure. These efforts will see XOS develop a range of new battery configurations with varied chemistries to be introduced next year. Thus far, XOS has seen progress here as well - key products in the pipeline include its suite of DC Fast Chargers, while purchase orders from Morgan Linen and additional fleet customers also support the case for Hub being a significant mid to long-term growth driver.

A Narrowing Liquidity Runway Weighs on the Outlook

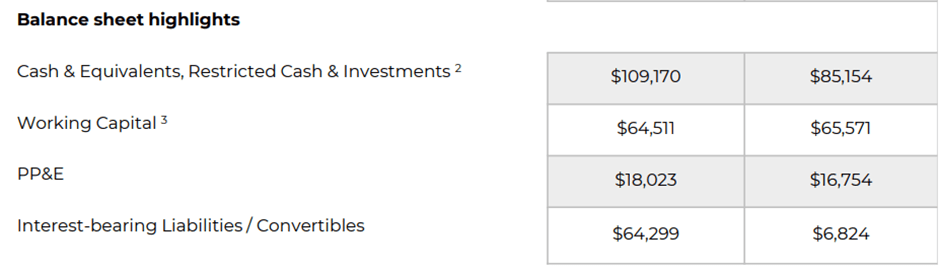

Growth comes at a cost, though, and XOS intends to fund it via more cost cuts in the coming quarters. Thus far, the company has already retrenched >15% of the staff and downsized the budget in line with the liquidity runway, so there likely isn't much room left. To fund the gap, XOS has most recently issued ~$55m of convertible securities, which gets the company to a ~$109m cash balance as of end-Q3.

{kind=link}

XOS also has access to additional debt financing through asset-backed loans, implying $60-70m based on its balance of inventories and receivables as of Q3. This may be enough to fund operating losses for a few more quarters, assuming a status quo scenario. Yet, the revenue impact of recent cuts could lead to some negative surprises down the line. Case in point - the recent delay of the medium to heavy-duty platforms to FY24, which will inevitably impact XOS' competitive position in a rapidly changing EV market. With fewer resources post-cuts, expect XOS' competitiveness to be further pressured as it focuses on existing product redevelopment over expanding the portfolio.

A Challenging Outlook

Following another disappointing gross margin result, XOS management's decision to cut costs and refocus the core strategy makes good sense, in my view. Whether this discipline has come too late is the question, though, as the years-long overspending on staff and shuttered projects have led to a narrowing liquidity runway. So while XOS has a product platform, the funding hurdles to a near-term production ramp-up are significant, with supply chain challenges further compounding the difficulties. Should the higher rates environment last into the mid to long-term, XOS will also have to contend with a highly competitive market for battery cells and vehicles with limited product development resources.

Thus, I am neutral on the stock, as any tailwinds from EV adoption in medium to heavy-duty truck applications are more than balanced by the execution risks. Given the prospect of further cash burn and more capital raises, the current valuation discount is justified.

For further details see:

Xos, Inc.: A Challenging Outlook