XP - XP Inc.: On Track For A Rebound

2023-05-25 09:48:11 ET

Summary

- Relative to an extremely low bar, XP surpassed expectations in Q1.

- The key drivers this time around were cost cuts and efficiency gains, though efforts to drive top-line growth are coming through as well.

- The stock screens very cheaply relative to its earnings growth potential and should lead a sector rebound as we enter a lower-rate environment.

Investor expectations had been depressed following months of rate-driven headwinds, so XP Inc’s ( XP ) steep rally post-Q1 outperformance was perhaps unsurprising. While all eyes had been on the shape of the revenue line, which continued to be weighed down by weaker trading activity and a one-off impact from the default of a large corporate, the upside surprise this time around was on the expense side. With its tech-driven investment cycle nearing an end and management also rightsizing the rest of the cost base, the lower end of the BRL3.8-4.4bn net profit guidance is now well within reach. Assuming inflation continues to decelerate, we are likely nearing a lower-rate environment as well, potentially reversing many of the revenue-side challenges that plagued XP over the last year. At ~11x fwd earnings vs. sustained ~20% ROE generation, XP stock has priced in too much pessimism, in my view, and at these levels, investors have many ways to win. Potential upside catalysts include higher capital returns (dividend increases or a renewed buyback program), as well as incremental revenue contribution from XP’s new verticals.

A Resilient Top-Line Despite the Broader Market Headwinds

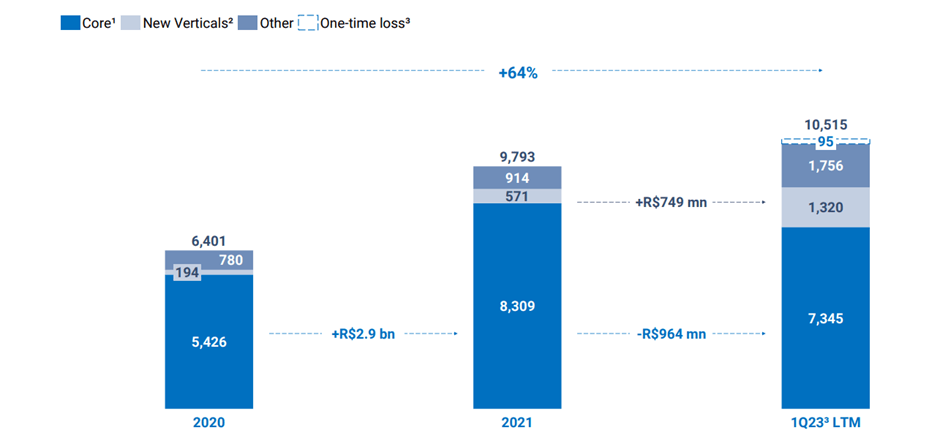

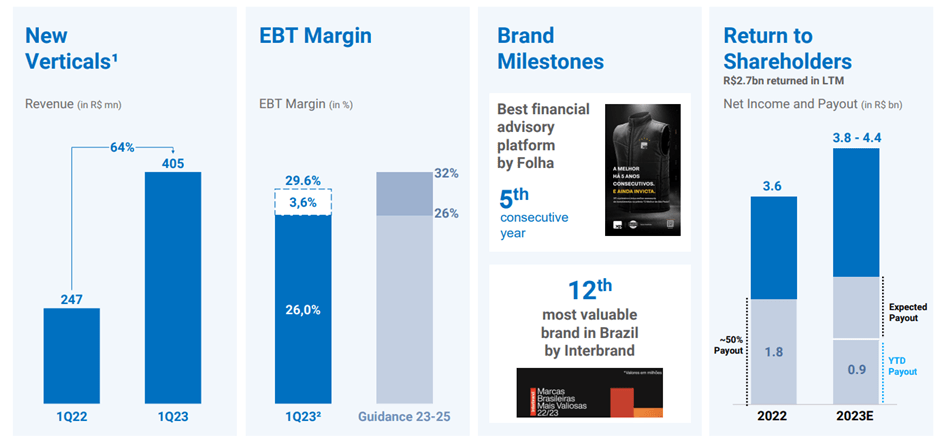

Despite the headwinds from ‘higher for longer’ rates, XP has continued to invest through the downcycle in expanding its product offering and creating cross-selling opportunities across its platform. As Q1 showed, the new verticals (i.e., retirement funds, cards, insurance, and credit) have gained traction, particularly with retail, which grew +1% QoQ (+5% QoQ excluding one-offs) due to stronger client activity despite the rate-driven pressures. Total assets also proved to be ‘stickier’ than expected, increasing +9% YoY on the more resilient retail business (+500k retail client adds to 4m in Q1). And with management targeting further share gains (20-25% retail market share vs.>10% currently), the growth runway remains compelling.

{kind=link}

XP Inc

But overall, XP has not been spared in a rising rate environment. Total net inflows in Q1 again decelerated significantly (down 48% QoQ) to ~BRL16bn, driving flattish net revenue growth (including one-offs). The silver lining is that contributions from new verticals have been growing (+64% YoY) to ~12% of total revenues. And assuming management’s guidance for +50-60% YoY growth this year holds, this will only rise in the coming months.

Whether the traction in new verticals will offset weakness on the institutional and corporate/issuer services side remains to be seen, however. In line with management noting limited investment appetite by clients (vs. liquid savings), I would expect a more gradual top-line recovery in a status quo scenario. A rising probability of a monetary policy pivot means this outlook could ultimately prove conservative, though. And with corporate activity also coming off a low base due to the Americanas default , there remains ample room for upside from here.

Lower Costs and Efficiency Tailwinds Support the Earnings Trajectory

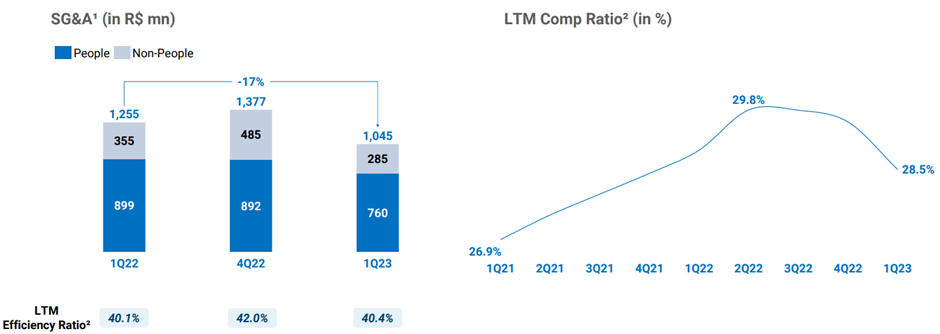

While there were positive takeaways from the top-line report, the key surprise in Q1 was XP’s cost control initiatives and efficiency gains, which drove expenses ~2% pts. lower as a percentage of revenue to 40% (down from 42% in Q4). Much of these gains are set to stick as well – the tech-driven investment cycle which ran through the pandemic is now at an end, along with the rightsizing of its employee base.

{kind=link}

XP Inc

Alongside more efficiency improvements in the pipeline, management is now confident in achieving the lower end of this year's BRL5-5.5bn expense guidance range. XP’s long-term incentive plan (comprising performance and restricted stock units worth up to 5% of outstanding shares) will be worth monitoring as well - despite the cancellation of these units in Q1, management has embedded a BRL160-170m/quarter headwind by Q4 2023. This may prove conservative. The combination of a lower expense run-rate and expansion into higher-margin income streams (e.g., more personalized services for higher-income clients) should prove accretive to margins over the mid to long term.

More Capital Returns in the Pipeline

Having come under investor pressure last year for its sub-optimal capital allocation policy, a higher payout (dividends or buybacks) could be on the cards for the upcoming years. But for this year, at least, XP has guided to another 50% payout. Given the size of the previous buyback program (BRL1.8bn repurchased last year), most of the distribution will likely be from buybacks, though management hasn’t yet made a firm commitment either way. Still, hitting its net income guidance of BRL4.1bn at the midpoint would imply total capital returns of BRL1.9-2.2bn (implying an attractive low to mid-single-digits yield at the current market cap).

{kind=link}

XP Inc

Beyond the shareholder return, XP management also appears to be following through with their commitment to investor engagement efforts, starting with increased participation on the Q1 earnings call. While less tangible than a higher capital return, improved investor relations should also go a long way toward improving the long-term valuation.

On Track for a Rebound

After consecutive quarters of disappointments, XP finally gave investors some cheer with a strong set of Q1 results. Unsurprisingly, revenue remains an issue amid weaker market activity, but management has stepped up on the cost side and is now on track to hit the lower end of its BRL3.8-4.4bn net profit guidance range. I don’t expect the rest of H1 will be any easier for XP, but with inflation pressures easing and lower rates potentially on the horizon, the H2 setup is compelling for asset flows. Alongside the potential earnings/ROE upside from the new verticals that XP has been investing in, the current ~11x fwd P/E valuation screens very favorably. Going forward, the size of XP's renewed buyback program will be worth looking out for, along with its progress on cost-cutting initiatives for the rest of this year.

For further details see:

XP Inc.: On Track For A Rebound