XPEL - XPEL: Great Business But Valuation Is Too High Amid Economic Downturn

2024-01-16 08:45:31 ET

Summary

- XPEL is known for its high-end Paint Protection Film, with a decent revenue growth rate and margin.

- The company is likely to face a number of risks in 2024 such as intense competition and economic downturn.

- XPEL's valuation is high compared to other peers in the automotive equipment sector.

Thesis

XPEL, Inc. (XPEL) is a company that focuses on self-healing PPF (Paint Protection Film) and provides software for the installation of its products. In my view, despite the company's growth capacity and brand power being attractive, the current timing may not be ideal for accumulating the company's stock. Due to its high valuation, I categorize XPEL as a hold.

Overview of the business

{kind=link}

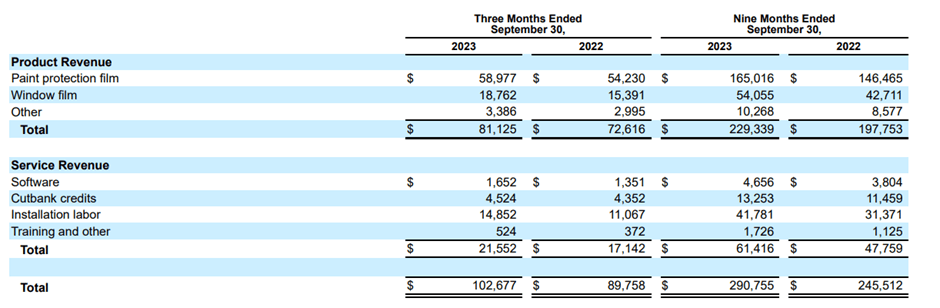

Xpel is one of the well-known companies for providing protective films mainly used for automotive applications including window protection film, surface protection film, and others. The company is particularly popular with the paint protection film, or self-healing film, which is applied to both interior and exterior surfaces to protect car from minor damages such as stone chips. I believe the reason why Xpel is well-known, despite being a smaller company compared to competitors like 3M, is that it was among the first to introduce a self-healing feature in PPF As a result, PPF is the main business of XPEL, contributing roughly 70% of its revenue in 2023. The company also offers window film, which is a protective film for automobile and building windows. Service revenue is highly correlated with product revenue as it is related to installing protective films such as labor cost.

Financials

When considering that Xpel is in the automobile industry, which is expected to grow in the low single to mid digits over the next few years, the company has shown stellar revenue growth since its IPO. Comparing the revenue recorded in 2018, which was about $100 million, it roughly tripled to $342 million in 2022. Even though the growth rate has slowed recently after the surge in revenue during the Corona pandemic, the company is still increasing its revenue steadily. When it comes to the margin side, the gross margin and operating margin in 2018 were 30% and 11%, respectively. In 2022, the gross margin and operating margin increased to 39% and 17%, respectively. I assume the company's higher margin comes from its brand power, allowing the company to impose higher prices than competitors.

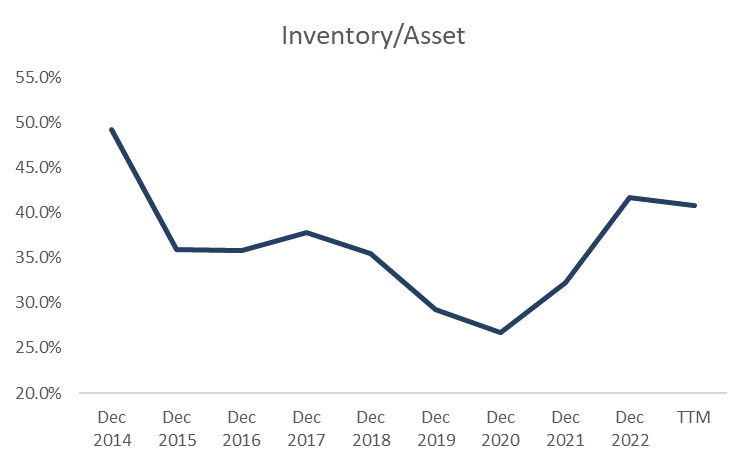

On the balance sheet, I believe it is highly unlikely that the company would go through serious credit events over the next few years. According to the recent quarterly report, the company recorded roughly $15 million of debt. It has $10 million of cash and cash equivalents and considering the high margin, debts would not pose a problem. However, one concerning point is that the company's inventory is increasing. During the pandemic, when the price of raw materials had soared and supply disruptions were a problem, the company's move to stock inventories was sound judgement. However, even though supply disruptions have been relieved, Xpel is still holding a substantial amount of inventories relative to its assets. If the inventory/asset ratio increases further, this may be a signal of sluggish sales due to the economic downturn, lower new car sales, and a decrease in consumption.

{kind=link}

Risk & Valuation

If XPEL continues to record a high revenue growth rate with a decent margin, then the market would likely accept high valuations compared to its peers in the automobile industry. However, when considering the economic downturn and intense competition, in my opinion, it would be difficult for the company to maintain its momentum in the revenue growth rate. Therefore, investors are recommended to factor in the risks in the valuation, which I would like to specify further in the article.

Risk: Economic Downturn & Intense Competition

I believe the narrative of an economic downturn would become stronger in 2024. Since November, the U.S. stock market has rebounded strongly as the Fed has changed its stance and signaled interest rate cuts in 2024. From a liquidity standpoint, rate cuts would be good news, but considering the background of Fed's stance change, the main reason would be the sluggishness of the U.S. economy. If consumers start to cut spending, they would first refuse to purchase new cars and install expensive films on their cars.

{kind=link}

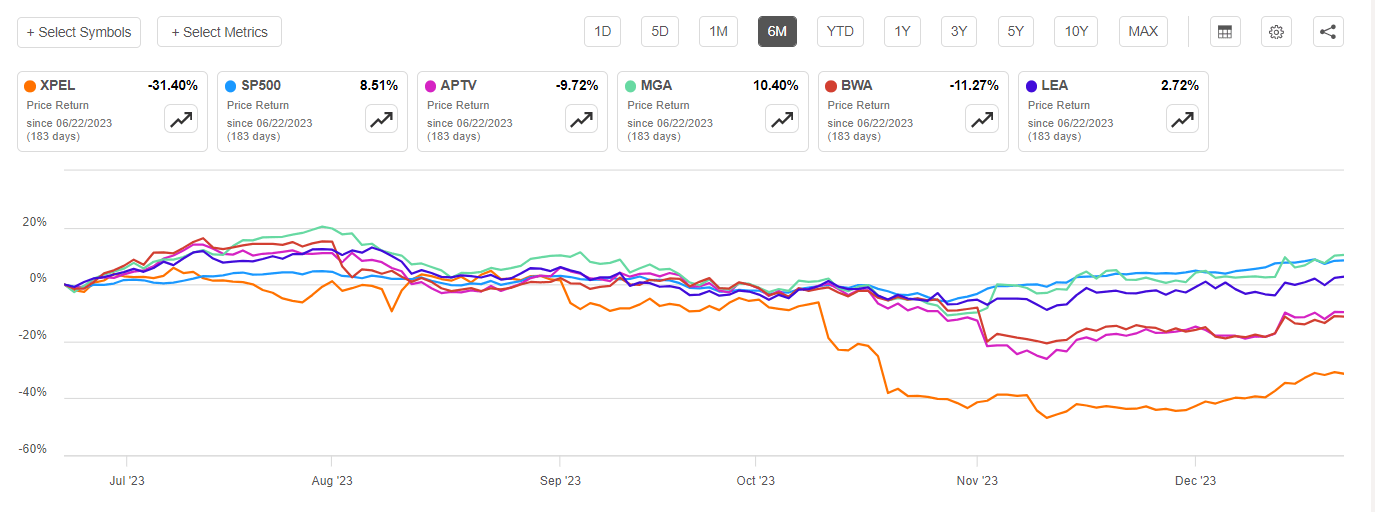

In my view, the market seems to have already taken the information into account. From November, many stocks recorded new highs, whereas automobile sectors didn't show good performance. Considering high interest rates and economic downturns, I think the automobile sector would not be the most attractive sector to invest in.

{kind=link}

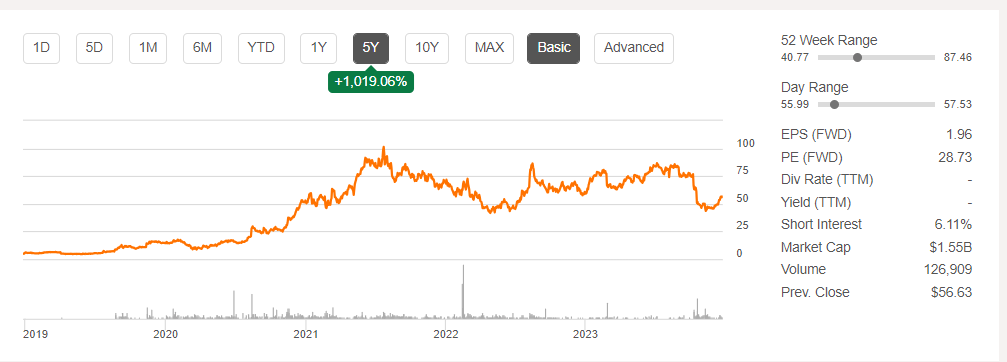

Moreover, the stock price of Xpel increased substantially during 2020 to 2022 when many consumers chose to purchase new cars with their savings. If I assume that car owners usually change their cars at five-year interval, it would take more time for Xpel to regain its high revenue growth.

Xpel is also facing intense competition and may not be able to maintain its high revenue growth rate.

{kind=link}

(Source: XPEL Paint Protection Services - Zaks Auto )

Installing PPF is an expensive option for car owners because they usually cover all the surfaces of vehicles for effective protection. XPEL products are among the highest-priced PPF in the market as it was an early starter of the field, establishing a leading position. Although prices vary among products, it costs thousands of dollars for full vehicle packages. A high price implies that the target customer would not be cheap, used-car buyers, but rather luxury, new car buyers. Thus, the PPF market is a lucrative market for automobile product manufacturers, attracting more players to enter. There are well-known brands such as XPEL, 3M, SunTek. In my opinion, as the PPF market is mature, and the technology is well-developed, distinguishing between high-end PPFs can be challenging. Also, customers can easily find cheaper options if they choose lesser-known producers. As a result, XPEL is likely to face intense competition within the PPF segment.

Valuation

In my opinion, given the company's high valuation compared to its earnings, it might be better for investors to wait for a further correction before accumulating its stocks.

Firstly, when compared to other listed companies in the automobile parts and equipment industry, the company is rich in valuation in terms of EV/EBITDA and P/E ratio. It is true that the direct comparison is difficult as there are no other publicly traded companies like Xpel that only operate business units related to PPF. However, it provides insight into the overall valuation of the sector.

As the automobile and automobile industry is mature and has a low growth rate except for the electric car sector, stocks in this industry usually have a low P/E ratio, For example, three companies (APTV, MGA, BWA) listed below have high competitiveness in their field and record decent margins. However, the market does not assign them high P/E ratios due to the outlook of the industry's growth rate. I believe it is highly unlikely for the automobile industry to record more than 40~50% yoy growth rate like software companies. This is why the industry has a lower P/E ratio when compared to high-growth industries. Considering that the company is in a cyclical industry and the revenue growth rate is likely to fall between 10-20%, the company's higher revenue growth rate does not justify twice higher valuation multiples.

| XPEL |

| APTV |

| MGA |

| BWA |

| EV/EBITDA (Fwd) |

| 17.98 |

| 10.4 |

| 6.1 |

| 5.8 |

| P/E GAAP (Fwd) |

| 25.95 |

| 10.4 |

| 10.8 |

| 11.8 |

Source: Seeking Alpha

Secondly, I believe the purpose of doing valuation of a company is not to calculate the exact future stock price, but to check whether the probability to earn money is higher than losing when investing in the stock. I would use the P/E method to check whether XPEL is overvalued.

1. I would use the Seeking Alpha annual revenue estimate of 2023 as a baseline, which is $387.39 M.

{kind=link}

2. For the revenue growth rate, I would consider three scenarios. The typical scenario assumes a 12% growth in revenue in 2024, the Seeking Alpha annual revenue estimate. In the best-case scenario, the revenue growth rate is 16%. Conversely, the worst-case scenario anticipates an 8% growth rate. In my perspective, the worst-case scenario is more likely due to intense competition and the sluggishness of new car sales. In fact, the recent 2023 3Q revenue growth rate has fallen to 14.4% YoY and 0.4% QoQ.

3. For the income margin, I used the five-year average to include the cycle of the company, which is roughly 12%.

| 2023((E)) |

| 2024((E)) |

| Income Margin (12%) |

| P/E ((FWD)) |

| Revenue Growth Rate 8% (Worst) |

| $387.39 |

| $418.3 |

| 50.2 |

| 27.9 |

| Revenue Growth Rate 12% (Typical) |

| $387.39 |

| $433.8 |

| 52.1 |

| 26.9 |

| Revenue Growth Rate 16% (Best) |

| $387.39 |

| $449.3 |

| 53.9 |

| 26.0 |

Source: Seeking Alpha

As a result, I project that the forward P/E in 2024 would be roughly 28, which is comparatively high within the automotive parts industry. If we assume that the stock price rises to more than $100, reaching roughly $3 billion in market cap, then the P/E ratio would exceed 50. In my view, the current valuation does not adequately compensate for the risks I outlined above. Additionally, Seeking Alpha factor grades also indicate that the valuation is still in the expensive range.

Seeking Alpha

Conclusion

Xpel has successfully increased its revenue with a good margin. As a result, the performance of the stock price outperforms that of the market. However, as the economy is expected to face a downturn and the valuation is high, it is not a good time to invest in the stock.

For further details see:

XPEL: Great Business, But Valuation Is Too High Amid Economic Downturn