XRMI - XRMI: A Strategy That's Not Working Out

2023-08-24 07:08:28 ET

Summary

- The Global X S&P 500 Risk Managed Income ETF is a covered call fund that uses a collar strategy for protection.

- The collar strategy limits upside potential and may not provide effective protection in most market scenarios.

- XRMI underperformed since January 2022, even though we experienced a bear market during this time.

- Covered call strategy limits your upside as it is, and this strategy limits it even further.

The Global X S&P 500® Risk Managed Income ETF (XRMI) is a high yielding covered call fund that is managed by the same company that released some well-known covered calls such as Global X NASDAQ 100 Covered Call ETF (QYLD) and Global X S&P 500® Covered Call ETF (XYLD). It employs a collar strategy, which includes a combination of writing covered calls and buying out of money puts as a hedge. The idea is similar to one of buying an insurance policy to protect your assets (such as your house) against unforeseen black swan events, but in this particular example, not only does it offer very little protection in most situations, it can also drag down the overall performance by quiet a lot.

Here is the problem. When you write covered calls against your existing stock positions, you are giving up upside in return of option premiums that you'll receive. In the event of an upside, you receive a share price appreciation up to your strike price plus any premium you've received. Many times covered call funds underperform overall markets because their upside is capped and bull markets can have those strong rallies where prices of stocks can appreciate very quickly. As if covered call funds don't already have very little upside as it is, you are limiting it even further by buying puts with part of the premium you've collected.

Think of a scenario where you bought 300 shares of a stock at price of $100. You divided these 300 shares into 3 positions where you kept 100 shares for yourself and held them straight, you wrote covered calls against another 100 with a strike price of $100 and collected a premium of $5 and you applied a collar strategy on the remaining 100 shares where you sold calls at a strike price of $100 and bought protective puts at a strike price of $90 for $2 per contract.

Let's see what happens under different scenarios.

Scenario 1: Stock price appreciates to $110. Your first position gains $10 or 10%. Your second position doesn't gain anything but you get to keep the $5 premium you collected on covered calls you sold so it has a gain of 5%. Your third position didn't appreciate either and you've collected a net premium of $3 ($5 from covered call minus $2 spent on protective call). You've gained only 3%.

Scenario 2: Stock price drops to $90. Your first position drops by $10 to $90. Your second position also drops to $90 but you've collected $5 premium so your loss is only 5% and in the third position your loss is $7 or 7% because your stocks dropped $10 but your collar only collected a net of $3 per contract after you've spent $2 on protective puts. Since the price level didn't drop below $90, your protective puts expired worthless and offered no protection.

Scenario 3: Stock price drops to $80, a sudden drop of 20%. This is the only scenario where a collar position would outperform. The first position would be out $20 or 20%, the second position would be out $15 or 15% and the third position would be out $7 or 7% because any drop below $90 would be protected so you'd only suffer a maximum drop of $10 minus the $3 credit you've collected in premiums.

The problem is that collars only work against big and sharp drops. In many situations, in order for a collar to kick in and offer protection, a stock would have to drop more than 10-15% in a month. This is very rare even during bear markets. Last year S&P 500 ( SPY ) dropped from top to bottom by about 28% (from $4800 to $3500) and it took 9.5 months to reach from top to bottom. We were looking at an average monthly drop of 3% which wouldn't trigger most collar protections.

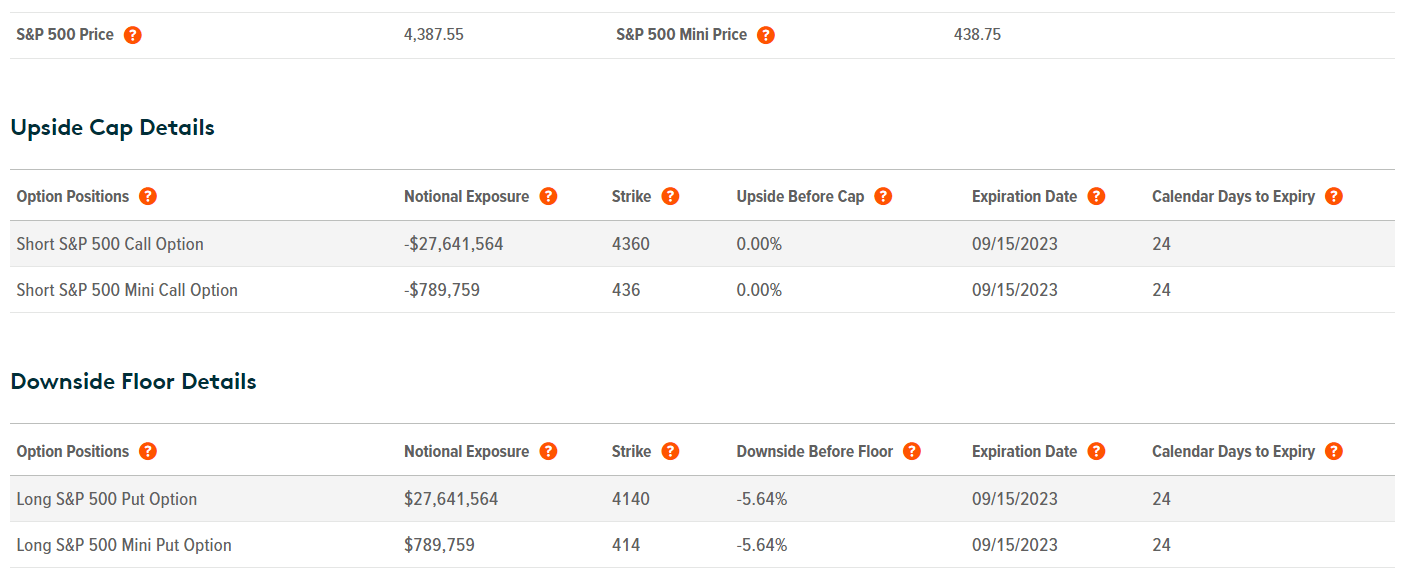

XRMI currently holds a collar position where its covered calls have a strike price of 4360 and its protective puts have a strike price of 4140. Keep in mind that both options expire on September 15th. In other words, the collar's protection won't even kick in until after S&P 500 drops below 4140 (or SPY drops below $414) in as little as 3 weeks.

XRMI current option play (Global X)

{kind=link}

As of writing this article, S&P 500 is already at 4400 level which means the covered call position is well in the money and put position has lost quite a lot of its value. When these options expire on 9/15, the fund will likely repurchase its calls and write new calls at a higher strike price and buy new put positions at a slightly higher position. Since VIX is currently at lower end of its multi-year range, one can buy SPY $420 puts a month out for $1.77 per contract. Meanwhile, at the money SPY calls that are a month out sell for $7.40. Basically you give up 24% of the call premium you collected in order to buy protection which won't even kick in until after SPY drops below $420. Keep in mind that selling covered calls already limits your upside greatly and now you are limiting it by another 25% for protection which may or may not kick in.

Up until now, we talked mostly theory and how the fund would be expected to perform under different scenarios. Now let us take a look at how this fund actually performed during last year's bear market as well as this year's recovery as compared to SPY as well as two other covered call funds by the same company. Since the peak of January of 2022, SPY is down by -5.5% in total returns. During this time, XYLD (100% covered calls) and XYLG (50% covered calls) performed similarly to SPY and they dropped about 4-5% in total returns after reinvestment of dividends. XRMI dropped by a whole -11% during the same period. The difference between XRMI and XYLD was close to 7% which also happens to be the amount I estimate that XRMI spent on protective puts during this period, so those protective puts offered no protection but significant amount of drag for the fund. To be fair the fund was slightly outperforming up until the bear market bottomed in October but it significantly fell behind after that as you can see below.

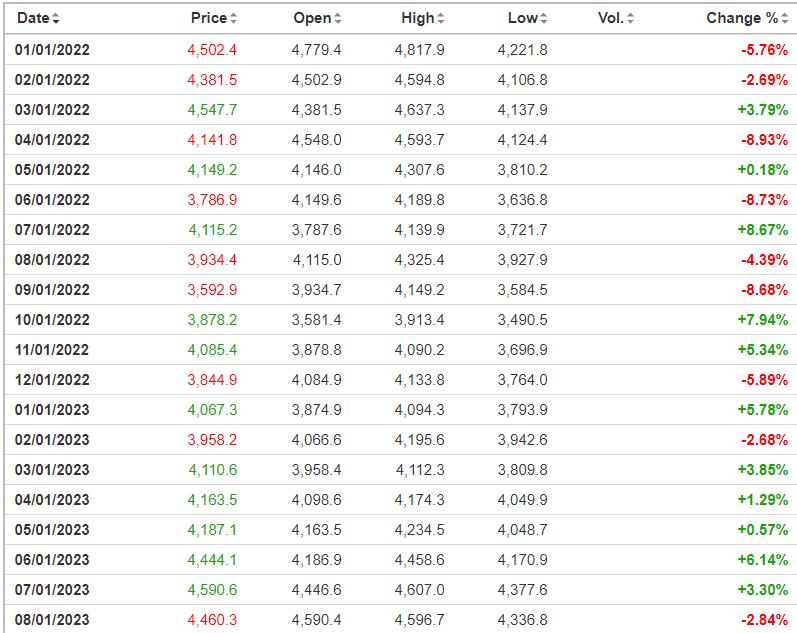

Below is how S&P 500 performed from month-to-month basis since January 2022. The worst month was April with -8.93% performance followed by June with -8.73% and September with -8.68%. Also since the index bottomed in October, the worst monthly performance it recorded was a -5.89% in December followed by a -2.84% in August 2023 which is still ongoing. As you can see, even during bear markets it's very rare for indices to fall enough to trigger a collar's put protection which usually kicks in after a drop of 7-10%.

S&P 500 Monthly Performance (investing.com)

{kind=link}

Bear markets are rare and they don't last long on average. Let's say you religiously bought protective puts every month for a period of 4-5 years. At the end of this period there was a bear market which caused stocks to crash -15% in one month. Your protective puts finally kick in and provide you with some protection where you suffered a drop of -5% instead of -15% that month which means you've outperformed by 10% during that month. Sounds great but when you consider all the put options you've bought over the years and all the premiums you've paid for year after year, it was far more than 10% which means you are barely breaking even on those puts.

What if you only buy protective puts during bear markets? Well, first you would have to know how to time the markets so that you know ahead of time that a bear market is coming. If you are that good at timing the market, you probably don't need protection anyways and you can just trade in and out of the market (hint: not many people are that good). If you buy your protective puts after the start of the bear market, you will notice that premiums on them are very pricey because VIX will be elevated, so you will pay far more money for this protection.

Don't get me wrong, I am not against using protective puts to hedge your position. I even suggested them a few weeks ago as a hedge as the markets looked toppy and VIX was low enough to allow buying cheap puts. One can also use put spreads instead of naked puts as a hedge since they are much cheaper to purchase. What I am against is combining buying puts with a covered call strategy because you are taking a strategy that already has very limited upside as it is and reducing the upside potential even more. It's like putting a bird in a cage and then putting that cage inside another cage.

This fund's collar strategy only protects you if the market crashes 10-15% in a month and those types of crashes are very rare and may not be worth buying an insurance policy for, especially one with a high deductible.

For further details see:

XRMI: A Strategy That's Not Working Out