XNET - Xunlei Is A Wildly Discounted Compounder For U.S. Investors

2023-06-21 11:18:26 ET

Summary

- Xunlei is a Chinese internet company that presents an opportunity for US investors to capture outsized returns as Chinese equities rebound.

- It is a durable business with the ability to reinvest capital at high rates of return while providing a wide margin of safety.

- The company has announced a share repurchase program and allocated up to $20 million in share buybacks.

Editor's note: Seeking Alpha is proud to welcome First Hill Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Xunlei (XNET) is an underfollowed Chinese microcap that trades well below net cash. I estimate the company is conservatively worth $500 million. I believe XNET represents a unique opportunity for US investors to capture outsized returns while their domestic market remains overpriced. Xunlei is a Strong Buy because of its ability to aggressively reinvest capital in new digital business ventures, and consumer products that are likely to endure the test of time.

(All figures in USD unless otherwise stated)

Company Description & Brief History

Xunlei is a leading innovator in the Chinese internet space. They operate in edge cloud computing infrastructure as a Service, Subscription, or Software-as-a-Service, and finally offer a live streaming platform for content creators. Although the shares are up nearly 45% from Chinese index lows, the company has still grown tremendously in strength and demonstrated its ability to consistently reinvest capital. With Chinese stocks shifting back into favor in US markets, investors should take a look at the most overlooked securities.

Founded in 2004, Xunlei gained early success with its download accelerator, Xunlei Accelerator, attracting a large user base of both free and paid subscribers. Since its founding date, the company has focused almost exclusively on improving the user's download experience. Paid users enjoyed faster downloads, new features, and more. Top Chinese smartphone manufacturer, Xiaomi was an original funder of Xunlei and has always been an important relationship for the company. Xiaomi currently owns 6.69% based on a look-through value of top shareholder Itui International Inc. Xunlei's mutually beneficial relations with Xiaomi have and will serve as a substantial tailwind for past and future growth. The company launched its IPO on the Nasdaq raising 88 million dollars under the ticker XNET. In 2015, the company made a strategic shift to focus on mobile consumers. This strategy, alongside an agreement to pre-install Xunlei Accelerator on all new Xiaomi smartphones, spurred the company's paid subscriber growth.

During the period from 2017-2020, the company brought in a former Tencent Cloud leader Lei Chen, to run the company. Chen had a different vision for Xunlei and redirected efforts toward blockchain technology. Specifically, a cryptocurrency coin " LinkToken " was created to reward edge cloud contributors (the company faced a lawsuit for this action and has since disbanded the segment). During this period, a once profitable Xunlei did not have positive operating earnings. Despite this, the market responded adversely. Short-term speculators pumped up the shares to a sky-high valuation. During this period, the capital allocation decisions were subpar. In 2019 , during an internal audit, they discovered that Chen was allegedly siphoning funds from Xunlei to the firm's bandwidth provider he owned. At this point, the current management team, led by Jinbo Li, took control of the company and redirected the business completely.

Jinbo Li was a member of Xunlei's founding team in 2004 and left the company in 2014 to pursue 2 successful Chinese Internet ventures. To this day, the company focuses on three revenue lines: Cloud computing, Subscription services, and Live Streaming & Internet Value-added Services. It is important to reconcile the company's history with the years of lousy operating results to truly understand Xunlei. One of the main arguments against Xunlei is the fear they will burn their cash hoard away on unprofitable business ventures. My argument for the contrary is to understand why the company was unprofitable for years under poor leadership. In 2 years (2020-2022), Jinbo Li has turned Xunlei profitable, and since 2021, spun out a business segment that is the fastest growing and highest revenue generating of any (International Live Streaming operations).

Operating areas

Subscription

Paid user subscriptions mainly come from Xunlei Accelerator, a cloud storage function, and other product offerings centered around user downloads. This flywheel has been going since 2004 and demonstrates its retained competitive edge over the years. Through new product and tier membership approaches, Xunlei has steadily grown its subscriber count and revenue per subscriber.

Cloud Computing

Xunlei offers cloud acceleration services that aim to compete with some of the largest internet companies in China by using the world's first proprietary shared computing network. In the first half of 2022, Xunlei was ranked 3rd with an 11.3% market share in public edge cloud service according to the IDC. This industry is projected to grow rapidly for the foreseeable future. This revenue line faces "fierce competition" from some of the largest companies in China. Despite this, Xunlei believes that through their IP and unique approach they can continue to hold and grow market share. This is fairly backed up by uninterrupted growth in the segment.

Live Streaming

Xunlei began investing heavily in live streaming operations, constantly updating their product and providing new features. The company found particular success in expanding to international areas such as the middle east. The live streaming segment serves as a benchmark for future capital allocation decisions, as this revenue stream demonstrates success. While the margin of this business is quite low right now, that is mostly due to higher revenue sharing to accelerate product adoption. Revenue sharing percentage is a variable cost that can be lowered as the product reaches maturity. 2022 Live Streaming Revenues: $122.3 million - Live Streaming revenue sharing $78.6 million = 43.7 million, a 35% gross margin not including server costs, employee headcount, and other costs. Although this segment is a lagger in margins, it trumps everything else in growth. In the first quarter of 2023, the segment increased 58.4% year over year.

Since Xunlei became profitable in 2022, its gross profit margin has declined steadily. This is not due to the erosion of competitive advantage as with many businesses, but rather an increased revenue portion of the Live Streaming business as a percentage of total revenues. As of right now, 63% of the revenue from this business's top line is given right back to the content creators. Remember that this is not a fixed cost but is chosen based on how the platform wants to incentivize users to join and start creating. In the mature stages of the live streaming segment, Xunlei can choose to reduce the percentage of revenue sharing with creators. Below, the rise in Cost of revenues is shown from 2020 to 2022, showing that costs associated with Cloud computing and Subscription services have remained under control.

ir.xunlei.com ir.xunlei.com

The true "cost" of R&D

Despite only achieving net profit in 2022, the core economics around Xunlei is very profitable. The total cost of Revenues in 2022 amounted to $200.05 million leaving $141.4 million in gross profit. Of this number, $39.7 million was spent on G&A, $24.8 million on S&M, and most importantly a whopping $67.6 million was spent on R&D which is 47.85% of gross profit. Some companies like Intel, need to spend large amounts of money on R&D to maintain a competitive position in the market. In the case of Xunlei, a portion of this R&D spend yields greater future cash flows. For example, throughout 2022, the R&D team has added new features for their subscribers, which added to subscriber growth & average subscriber spending. This is a wildly good use of shareholder dollars resulting in millions in positive value. The fruits of this labor can be observed over the long term in total topline growth.

Macrotrends.net

Xunlei's Reported Revenue since listing via MacroTrends

I believe if Xunlei wanted, they could drastically cut the size of their R&D efforts and cash out an extra 10-20 million per year to their bottom line. Instead, Xunlei has and will increase R&D spend with the size of the company so long as they can effectively employ capital. If you looked at Xunlei's operating profit of $10.06 million and added back $20 million of their R&D spend, you would get $30.06 million in theoretical operating income. At this point, you begin to realize how silly a negative enterprise value is. This is precisely what analysts fail to realize about Xunlei, the reinvestment efforts have been paying off, but the bottom line doesn't see the results because the R&D "cost" grows with the top line. The same is true of any company that aggressively reinvests capital. For most of its life, Amazon reported very little net income, despite plowing loads of cash toward R&D.

There are a few limitations to the observations I stated above. Firstly, as investors, we have no way of knowing what percentage of Xunlei's R&D spend is on maintaining their competitive position as opposed to reinvestment. Above, I conservatively speculate 10 or 20 million, but the true number may be lower or higher. As long as Xunlei's top line is growing at or above 15% and the bottom line is healthy, we can safely assume that capital is being used effectively.

We also know for a certainty that the management is positive about future growth because they are redeploying the companies' cash back into the business through share repurchases. For 2023, the Xunlei board has authorized up to $20 million in share repurchases. Buybacks are a bet that future cash flows will be higher than todays. Additionally, we have seen directors and executive officers accumulate shares between 2020 and 2022. They grew their stake in Xunlei from 159 million to 170 million and 47.7% to 51.6% in shares and percentage respectively.

ir.xunlei.com

2020

ir.xunlei.com

2021

ir.xunlei.com

2022

Management

Jinbo Li is an owner-operator because he owns 29% of Itui International which owns 42.7% of the company. Thus, Li is heavily incentivized to create value for shareholders. So far the capital allocation decisions have been very good to our knowledge, as it is difficult to determine the ROI of investments such as R&D in a short period. The company has devoted a large portion of gross profits to reinvestment while maintaining profitability. Xunlei will not require external capital and will use its cash pile to fund share repurchases as well as long-term investments.

Xunlei's share repurchase plan for 2022 resulted in 6.7 million in shares repurchased. The 2023 share repurchase plan allows a repurchase of up to $20 million.

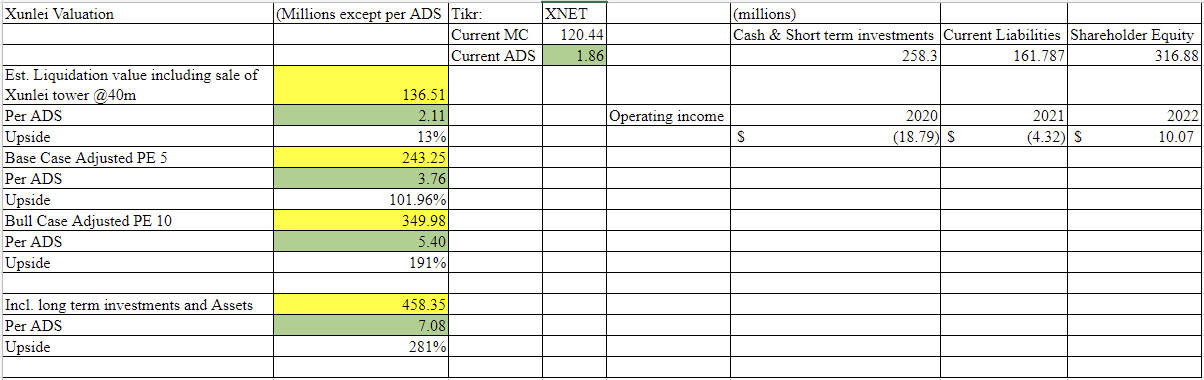

Valuation

Xunlei Valuation table (Author's Calculations) (Excel)

{kind=link}

The valuation I use above defines "liquidation value" as the value one could get if all assets were sold in a very short time frame. This includes the companies' cash and short-term investments net of debts and real estate sales at a reduced price. In the case of most securities, there is very little reason to be trading below this threshold. The "base" and "bull" cases are calculated based on a multiple of current earnings plus the book value (not the liquidation value). The multiples chosen, 5 & 10 respectively are based on current growth rates. Investors can choose to create a DCF model to demonstrate the upside possibility.

This valuation is intentionally conservative because the aim is to protect the investor's downside and provide a wide margin of safety. Simply put, the assets on the balance sheet of Xunlei provide a heads I win, tails I don't lose much situation.

Xunlei also owns an 8.73% stake in 360 camera maker Insta360. Since the company is private, the stake sits on the company balance sheet at cost, despite Insta360 bringing in 2022 revenues of over $281 million representing annual growth of over 50% over the past three years. Insta360 has been denied IPO several times now with the limiting factor being that 60% of sales are international. Some consider this a hidden "asset", but I include this stake at cost. You can see this in the annual report named "Yingshi Innovation Technology Co., Ltd."

Commentary on Q1 2023 results

In the first quarter of 2023 , Xunlei continued to adhere to the core thesis of this article. The operating profit of Xunlei fell from $3.9 million to $0.7 million. Despite the drop in profit, this must be reconciled with an increase in R&D expenditures from $16.3 million to $18.0 million.

Research and development expenses for the first quarter of 2023 were $18.0 million, representing 18.2% of our total revenues, compared with $16.3 million or 20.6% of our total revenues in the same period of 2022. The increase was primarily due to increased labor costs incurred during this quarter.

Xunlei remains growing, profitable, and reinvesting earnings into R&D. Without a re-rating in the share price, Xunlei will continue to grow book value per share for the foreseeable future, accelerated by share repurchases.

Downsizing Live Streaming Q2 2023

Xunlei recently filed a press release stating that:

The Company is downsizing its domestic audio live streaming operations due to lower gross margin of such business and the rapidly evolving and challenging industry environment.

Carefully note that the press release only applies to domestic audio live streaming. My interpretation of this release is that Xunlei faces competition in China, so the company will simply focus its efforts on the international segment. When prompted for further clarification, the Xunlei Investor Relations team had this to say:

Email correspondence with the Xunlei Investor Relations team (ir@xunlei.com)

In my opinion, if the business faces competition in one area, then redirecting the business elsewhere is good capital allocation. When a company opts to reinvest its profits, the shareholders trust the management will redeploy the capital at high rates of return. Therefore, it is part of the fiduciary duty for Jinbo Li to downsize business segments that are low margin, thus low return.

Risks

The obvious question is, what did we miss? Good companies rarely trade for below net cash, much less those that will churn out 10's of millions in cash flow. Of course, the company does not come without uncertainties baked in. For example, the company is only listed on the NASDAQ through VIE, not any Hong Kong or Shanghai exchanges. This poses some risks as in the case of delisting, as they cannot give investors Hong Kong shares in exchange, as is the case with companies like Alibaba. Xunlei would need to re-apply for a Chinese listing, which would be a long and costly process. There is also a question as to whether Xunlei would meet the stricter regulations of Chinese regulators.

Presently, company earnings fluctuate based on the relationship between the USD and RMB. Year to year, income can dampen or exaggerate financial performance based on exchange rates.

Delisting

Unlike Alibaba or Tencent, Xunlei does not list any comparable shares in Hong Kong or China markets. Since the US and Beijing have not yet developed a mutually agreed-upon auditing agreement, all China securities could be delisted. This could result in Xunlei being removed from the stock market entirely. Chinese securities listed in the US have a unique set of intricacies, too elaborate for this forum, and some further resources are listed below. My current view on this issue is that the SEC and Beijing should come to a rational agreement.

Conclusion

The fundamental conclusion of this article is the belief that Xunlei will continue to reinvest capital and grow for a substantial period. The colossal discount to book value provides a wide margin of safety. I would argue the risk-adjusted margin of safety is larger than any US security of similar size. If one understands delisting risks and has a positive outlook on US-China relations, an investment in Xunlei could be warranted.

For further details see:

Xunlei Is A Wildly Discounted Compounder For U.S. Investors