XYLD - XYLD Is Still Delivering On Its Core Strategy Of Providing Income

2023-10-10 09:00:00 ET

Summary

- The S&P 500 has declined, and there is no reprieve in the economic tightening cycle.

- Yields on risk-free assets have increased, impacting traditional equity proxies for bonds.

- XYLD continues to deliver monthly income and is a strong alternative to risk-free assets in the current environment.

Since my last article ( can be read here ) on the Global X S&P 500 Covered Call ETF (XYLD), the S&P 500 has declined by -1.35%, and there has been no reprieve in the economic tightening cycle. The price per barrel of oil has significantly increased, remaining above $80, while the United States Inflation Rate - September 2023 Data - 1914-2022 Historical has seen two consecutive months of increases. Yields on treasuries have gone gangbusters, and the 3-month, 12-month, and 2-year all have yields that exceed 5%, while the 30-year yields 4.96%. The rate of return for risk-free assets has impacted traditional equity proxies for bonds as there is less of a reason for investors looking for income to take on equity risk. Most Dividend Aristocrats and Dividend Kings have a yield that is less than a CD, Money Market, or treasury notes. XYLD continues to deliver on its core investment strategy of delivering monthly income, as its distributions are not predicated on generating dividends from its underlying assets. While other interesting income products have entered the market over the past several years, I am still bullish on XYLD for generating monthly income.

{kind=link}

Following up on my last article about XYLD

In my previous article, which was published on 6/28/23, I discussed XYLD's income structure, the consistency of its distribution, how it generates such a large yield, and how it was fairing against Global X's other covered-call ETFs. XYLD was following the markets higher, and while much of the upside was capped due to its covered-call structure, XYLD was slowly appreciating while delivering monthly income. These covered-call strategy ETFs from Global X have an income-first approach, and investors should not expect the share price to mimic what the market does during periods of appreciation. Since my last article, the macroeconomic environment has changed a bit, and I wanted to write a follow-up article on why I am still bullish on XYLD in an environment where rates could be higher for longer.

What's different since the end of June on a macro level that is impacting the market

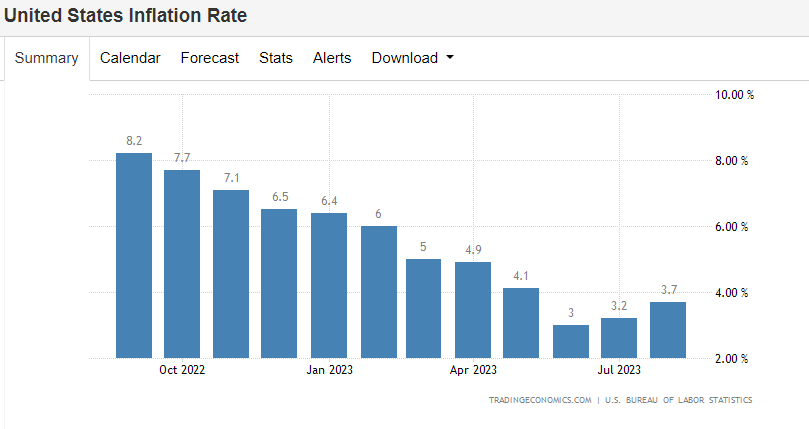

At the beginning of the summer, we received a CPI print of 3%. A portion of the investment community was indicating that inflation was no longer an issue and that the Fed would cut rates sometime in the fall. There were economists and financial pundits on both sides of the debate, but it seemed as if there was an overwhelming narrative being constructed that the Fed had done enough to reduce inflation and a pivot was imminent in the fall of 2023. Some of the conventional wisdom being used was the impacts of higher rates on consumer debt and refinancing debt on the corporate level. Despite CPI coming in at 3%, the Fed raised rates by 25 bps on 7/26, then paused at the September meeting. At the last Fed conference, Jerome Powell was explicitly clear on the Fed's stance regarding rates. The Fed will continue to be data-dependent, but the narrative of a Fed pivot in 2023 was crushed, and the door for additional increases was left wide open.

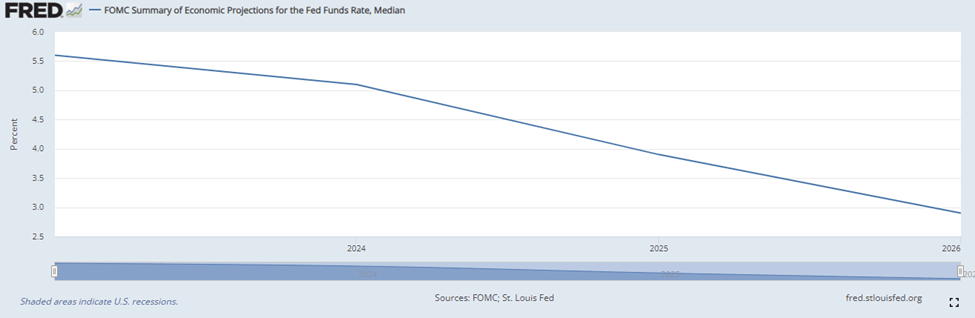

The market didn't digest the news well as the investment community came to the realization that reprieve from rates would not occur in 2023 and that the Fed wasn't just talking a big game. Despite what some had believed, the United States economy has endured the hiking period without breaking. Unemployment remains under 4%, and the labor market continues to be strong. Another rate hike rather than a pivot could be on the table as the CME Group FedWatch Tool is showing an 11.2% chance of a .25 bps increase for November and a 39.5% chance we see a .25 bps increase in December. The St. Louis Fed has projected that rates will be higher for longer as they see rates falling to 5.1% in 2024 rather than 4.6% and 3.9% in 2025 rather than 3.4% from the last projection.

{kind=link}

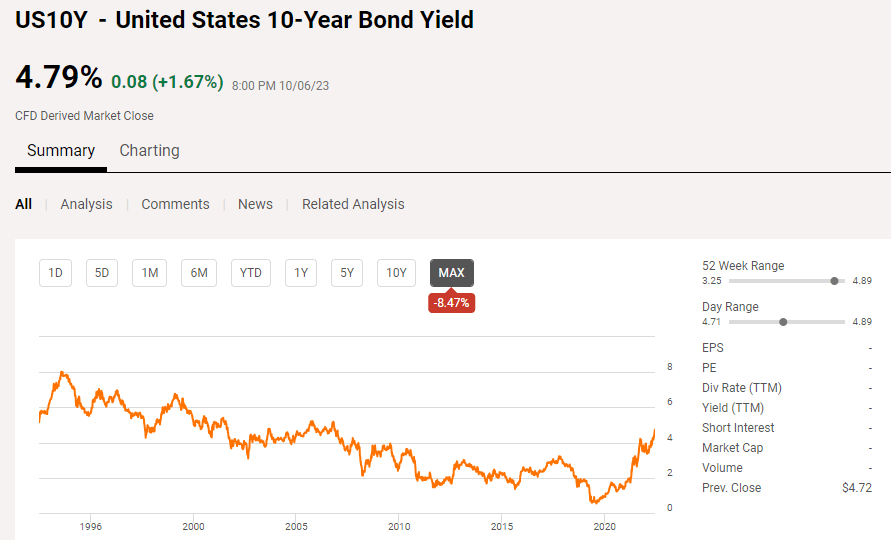

While there will always be companies that outperform the market and investments that generate above-average returns despite the economic or business cycle, a higher rate cycle for longer isn't bullish for dividend stocks. The reason isn't necessarily that their businesses are flawed, it's more focused on the investor's appetite for risk. If an investor's main focus is generating income on their capital rather than appreciation, the current environment has provided a risk-free rate of return not seen in decades. The last time we had 10-year treasuries yielding 4.79% was in 2007. I actually heard the phrase T-bill and chill on CNBC the other day, and for income investors, it may not be the worst idea. This environment hasn't been great for income stocks or ETFs that investors were looking for when we lived in a yield-starved environment. Below are some examples from 2023:

- ProShares S&P 500 Dividend Aristocrats ETF ( NOBL ) down -3.29% yielding 2.22%

- Utilities Select Sector SPDR® Fund ETF ( XLU ) down -18.79% yielding 3.7%

- Vanguard Real Estate Index Fund ETF Shares ( VNQ ) down -9.98% yielding 4.83%

- Verizon Communications ( VZ ) down -23.11% yielding 8.62%

- PepsiCo, Inc. ( PEP ) down -10.66% yielding 3.16%

The market has been fueled by big tech, and the markets could move higher, but the majority of companies are not participating in the gains. If the Fed keeps rates higher for longer or continues to raise rates, then there could be less of a reason for investors to add traditional dividend-paying companies to their portfolio, and a rotation out of risk-free assets into equities could be prolonged. This is why XYLD continues to look interesting, and I think it's a strong alternative to risk-free assets in the current environment.

{kind=link}

Why XYLD is still one of my preferred alternatives to generate income rather than treasuries

We're living in a completely different environment for income, and you can get over 5% of your money for not taking equity risk. From a long-term perspective, I don't believe bonds will ever replace stocks for building wealth, but from an income standpoint, it's hard to knock 5% risk-free. To take on equity risk in this environment, investors need to get paid a higher yield or see value in an underappreciated asset. On the income side of my portfolio, it's very hard for me to consider anything with a sub-5 % yield unless I feel shares are significantly undervalued, and it becomes a situation where I am getting paid to wait for my investment thesis to play out.

{kind=link}

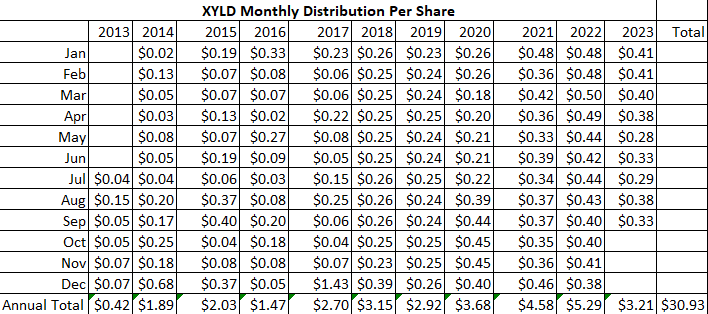

I still prefer XYLD over risk-free assets for two reasons. It owns the underlying assets in the S&P 500 and generates more than double the yield of T-bills. For those who are unfamiliar with XYLD , it utilizes a buy-write strategy and invests in all of the companies within the S&P 500, just like a traditional index fund on the buy side. XYLD then implements a sell-side where it writes or sells corresponding call options on the S&P 500. The options are written at the money on a monthly basis, and the premiums collected are used to fund its monthly distributions to shareholders. Covered Calls are written on 100% of the portfolio, so the upside is capped, while losses to the downside will follow the market.

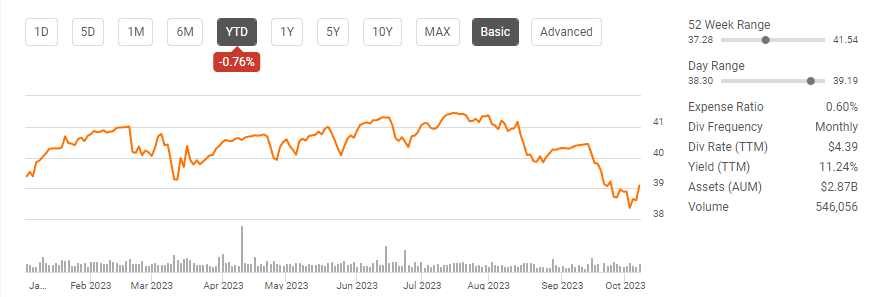

XYLD is basically flat on the year, as it followed the markets higher and fell in recent months due to the market volatility. At the beginning of the year, you could have locked in a 4.41% yield on the 2-year note , and as long as you can lock your money up for two years, the only downside is opportunity cost on another investment idea. At the beginning of the year, XYLD traded for $39.39, and now it's trading at $39.09. While XYLD has slightly declined in value, it generated $3.12 of income in the first nine months of 2023, which works out to an 8.14% yield on invested capital. After accounting for the reduced principle, an investment in XYLD would still be in the black by 7.38%, with three more distributions coming in 2023. If the markets rally into the end of the year, XYLD could finish in the black on a YTD basis, and the income generated would be more than double, maybe even triple, what someone could have locked in at the beginning of the year on the 2-year note.

{kind=link}

I think stocks could have a rocky road in the near term, especially if the Fed increases rates again. While we can speculate, nobody knows what the magic number will be where rates make something break. Maybe the economy can endure another .25 or .50 bps, but if it can't, the ramifications could be drastic. The St. Louis Fed is projecting a higher for longer rate environment, but they are forecasting that rates will eventually start to come down. For now, I want to be in companies that can withstand another hike, and XYLD focuses on the S&P 500, which companies lead with the strongest balance sheets. I think big tech is going to lead the way for the markets, and XYLD has a 28.57% portfolio weighting toward big tech.

{kind=link}

Conclusion

I would still rather allocate money toward XYLD than bonds at this point in time. Sure, I could lock up money in a 2-year note at 5.08%, but that means I am generating 10.16% in income over two years on my investment with no gains on the principle. XYLD has generated an 8.14% yield on invested capital since the beginning of the year, and if I look on a TTM basis, shares have generated $4.39 in income, which is an 11.24% yield on the current price. I don't have a crystal ball, but in the fall of 2025, I would expect the markets to be higher than where they are now, as rates are projected to be somewhere between 3.9% and 2.9%. Even if the markets go into a bull market and XYLD follows the markets higher, it should still generate a larger yield than the 2-year note, and I would get some appreciation out of the principle. Risk-free assets are certainly attractive, but I think XYLD is a better bet for investors who are willing to take on equity risk because they are being paid more than double for the risk.

For further details see:

XYLD Is Still Delivering On Its Core Strategy Of Providing Income