XYLD - XYLD: Why Covered Calls On The S&P 500 Is A Bad Strategy

2023-06-30 06:23:17 ET

Summary

- The Global X S&P 500 Covered Call ETF is structured to replicate a covered call option strategy on the underlying S&P 500 Index.

- We explore the covered call strategy on the S&P 500 Index specifically in more detail, assessing its potential for enhancing returns and assessing the risks and trade-offs associated with the strategy.

- Overall, we see no real advantage in employing a covered call strategy for most investors, unless one is absolutely confident of timing the markets with a high level of precision.

The covered call is a popular options strategy that has often been touted as an effective way to enhance returns on an asset. Financial innovation over the years has also made such options strategies more accessible to retail investors with exchange-traded funds (ETFs), offering covered call strategies on major indices.

Below are some examples of covered call ETFs that focus on equity indices:

- Global X S&P 500 Covered Call ETF ( XYLD )

- Invesco S&P 500 BuyWrite ETF ( PBP )

- Global X Russell 2000 Covered Call ETF ( RYLD )

- Global X Nasdaq 100 Covered Call & Growth ETF ( QYLG )

But there are also ETFs that use different option strategies or focus on different asset classes:

- Invesco S&P 500 BuyWrite ETF ( PUTW )

- Credit Suisse X-Links Crude Oil Shares Covered Call ETNs ( USOI )

- Global X NASDAQ 100 Collar 95-110 ETF ( QCLR )

- iShares 20+ Year Treasury Bond BuyWrite Strategy ETF ( TLTW )

- Nuveen NASDAQ 100 Dynamic Overwrite Fund ( QQQX )

The wide variety of strategies available, however, usually do more harm than good for investors. Financial market veterans know only too well that what often appears to be a free lunch in investing, usually masks hidden risks and trade-offs.

Unfortunately, a deep dive into the mechanics of different options strategies and the individual characteristics of the ETFs listed above is beyond the scope of this article.

Instead, we shall explore the covered call strategy on the S&P 500 Index specifically in more detail, assessing its potential for enhancing returns while emphasising the hidden risks and trade-offs associated with the strategy. We believe that the insights gained from this discussion are transferable and that the same basic principles can be applied when analysing other option strategies.

The Global X S&P 500 Covered Call ETF ( XYLD )

For our specific purposes, we will focus on one of the largest covered call ETFs. The Global X S&P 500 Covered Call ETF ( XYLD ) is structured to replicate a covered call option strategy on the underlying S&P 500 Index, simplifying execution while shielding investors from the complexities of derivatives trading, at a reasonable cost. At the time of writing, XYLD had over US$2.8 billion in assets under management ((AUM)).

According to information provided by the fund issuer , XYLD seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the underlying Cboe S&P 500 BuyWrite Index. This is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the S&P 500 Index. (A covered call strategy and a buy-write strategy refer to the same options strategy and the two names are often used interchangeably by traders.)

XYLD invests at least 80% of its total assets in the securities of the CBOE S&P 500 BuyWrite Index, which consists of two parts: 1) all equity securities that constitute the S&P 500 Index weighted by float-adjusted market capitalization and (2) short call options on up to 100% of the S&P 500 Index. To maintain a persistent short call options position, XYLD sells new S&P 500 Index call options that will expire in one month on the third Friday of each month.

XYLD distributes a portion of the income from writing/selling the S&P 500 Index call options to shareholders. The monthly distribution of XYLD is capped at half the premiums received or 1% of net asset value ((NAV)), whichever is lower. Any excess in premiums earned is reinvested back into the fund.

We will avoid discussing the basics of options trading here. But readers who are new to options may consider looking up this helpful infographic on how XYLD works.

In short, by writing/selling call options on a basket of stocks constituting the S&P 500 Index, an investor is able to earn a premium immediately. And if those call options are not exercised upon expiration, the investor retains ownership of the underlying asset and the profit from this strategy would be the premium that was earned from selling those call options. The call options are "covered" because the investor actually holds the underlying asset.

In the alternative scenario in which the price of the underlying asset is higher than the strike price of the call options upon expiration, the investor who sold those call options will be obligated to deliver the underlying asset to the option holder, which effectively translates to selling the underlying asset at the strike price.

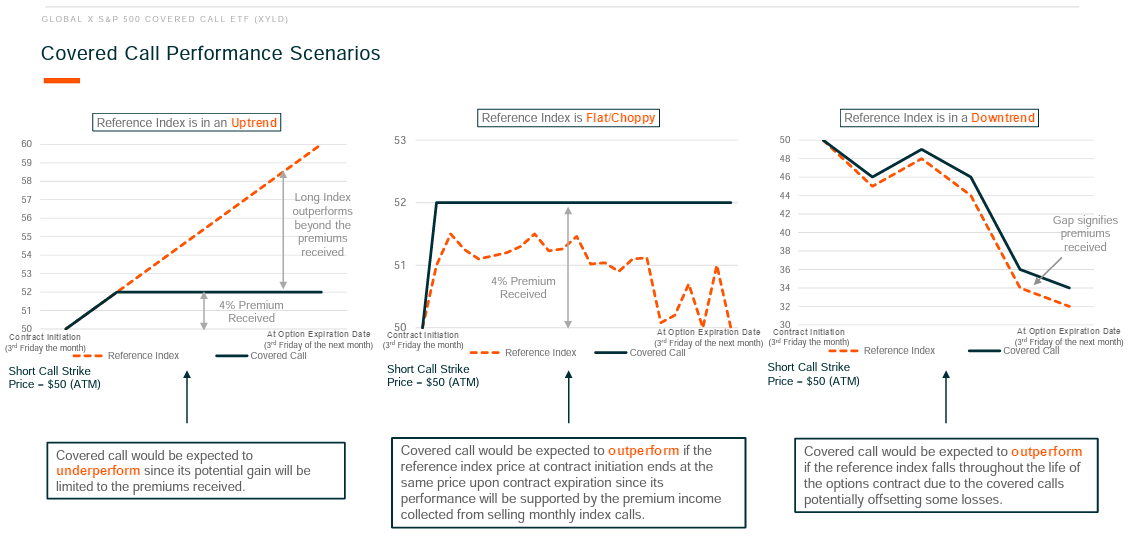

Three Scenarios And None Are Good

When an investor purchases shares of XYLD, he essentially takes a long position on the S&P 500 Index and short call options on the same index. There are then three possible scenarios that will determine the outcome of the established position on the expiration date.

Below is a diagram demonstrating the three possible scenarios, assuming that the call options fetch a 4% premium.

Global X - XYLD Presentation Materials

{kind=link}

In the first scenario in which the underlying asset's performance exceeds the premiums earned from selling the call options, the investor is worse off. He only makes a 4% gain in premiums and has to forgo any excess returns from the performance of the underlying asset.

In the second scenario in which the underlying asset's performance is flat, the investor is better off. He makes a 4% gain from premiums while the underlying asset is flat. As long as gains on the underlying asset do not exceed the premiums earned, the investor is better off.

In the third scenario in which the underlying asset moves lower, the investor is better off. Because the 4% in premiums earned helps to offset losses on the underlying asset.

Crucially, we need to ask ourselves. Is the investor truly better off in the second and third scenarios? If you are having doubts about the covered call strategy being an effective tool for enhancing returns, then you probably have a keen sense for risk-return trade-offs. Let's try to break down the strategy further by thinking in terms of risk and return.

In terms of return, scenario 1 is clearly a bad outcome. The investor has sacrificed all potential upside in the underlying asset in exchange for a 4% premium. Given that there is no theoretical limit as to how high stock prices can rise (buyers are free to pay or offer any price for a stock), and that it is not that unusual to see double-digit gains, giving up the opportunity for those gains in exchange for a 4% premium seems like a bad trade-off.

Global X - XYLD Presentation Materials

How about the risks associated with holding the underlying asset? The investor holding the underlying asset remains exposed to any downside risk. Even if the premium earned helps to offset some losses on the underlying asset, the investor remains exposed to losses exceeding the premium.

In scenario 3, the investor outperforms the typical buy-and-hold strategy on the S&P 500 Index. This outperformance is possible due to the premiums earned. As the accompanying diagram demonstrates, the investor is only in some sense better off because the 4% premium would help offset some losses should the underlying asset decline. The investor is nonetheless at risk of suffering substantial losses.

Global X - XYLD Presentation Materials

Investors should also weigh the magnitude of potential returns with the potential risks. In this scenario, the investor merely offsets losses by 4%. But there is no telling how large potential losses could be! Was it worth sacrificing all that potential upside in the underlying for the sake of a 4% cushion on the downside?

Another way to rationalise this trade-off is to consider why a rational investor would bear equity risk (potentially a 100% loss) in the first place. It is because investing in equity offers the potential for substantial returns. Investors accept the risk of loss, in exchange for the prospect of returns. From this perspective, does it really make sense to limit the prospect of returns to the premium earned, while still bearing most of the downside risk?

Finally, let's consider scenario 2. Here the investor is clearly better off. In the event that the underlying asset trades sideways. Selling call options would give the investor a 4% premium.

Global X - XYLD Presentation Materials

But remember that this gain didn't come for free. The investor remained exposed to the risk of potentially forgoing significant upside gains on the underlying asset, as well as the risk of potentially suffering significant losses on the downside. Taking on all these risks just for 4% doesn't seem like a good deal.

Covered Call Strategies Require Precision And The Illusion Of Precision Is The Enemy

By now, if you are still somewhat optimistic about the covered call strategy as a tool for enhancing returns, then it is probably because you believe you could predict how the underlying asset was going to move. You might even argue that earning 4% in premiums in a single month is a fantastic result since that would add up to 48% in returns a year with no compounding!

And this is the real selling point of covered call strategies such as the XYLD. Just like many other speculative trading strategies out there, the promise of returns rests upon the weak assumption that the investor is a rare genius capable of predicting exactly where markets will go in the short term.

If one is certain that the market would rise, one should use all the leverage he could get and bet the house. If one is certain the market would crash, one should use leverage to short it. And if one is certain that the market would move sideways, then a covered call option strategy or a short straddle strategy would work well. Life is easy for stock market geniuses.

Successful market timing, especially over short time frames, typically demands extraordinary precision. One first has to know which direction the market will go, and then one needs to know exactly when it will move. There is no shortage of traders who claim to be capable of timing markets with precision, and we have met many throughout our careers in the investment industry. But experience has also honed our scepticism towards these claims. In fact, veteran derivative traders would understand that there is no such thing as a superior option strategy, it all depends on how and when one uses them.

Don't get us wrong, options strategies are powerful trading tools and can be extremely helpful for constructing unique payoffs to suit a trader's view of the market and desired risk-reward profile. As demonstrated with XYLD, a covered call strategy on the S&P 500 Index can indeed alter the risk-reward profile of a traditional asset, allowing the trader to achieve returns even during a sideways market, or to manage downside risk.

Regardless, option strategies in the wrong hands typically encourage short-term speculation and market timing, distracting the investor from sticking to time-tested investment strategies.

Covered Calls On Equity Are The Worst

There are other reasons why using a covered call option strategy on the S&P 500 Index is a bad idea. Because equity markets naturally drift upward over time, establishing a covered call strategy on the S&P 500 Index means that the odds are already against you.

In fact, a buy-and-hold strategy on the S&P 500 Index would have given investors roughly 10% in annual compounded returns based on historical data on asset class returns from 1995-2022 .

Perhaps a covered call strategy on commodities or foreign currencies would make more sense, given that commodity prices do not exhibit that natural upward drift like equities do over sustained periods of time. Many modern currency regimes are also managed to some extent with the aim of maintaining relatively stable exchange rates.

Premiums Are Subjected To Implied Volatility

In the examples we have used, we assumed that XYLD was able to generate 4% in premiums by selling call options. However, there are several factors that could affect the level of premiums that XYLD is able to earn in the options market.

One of the most important factors affecting call option premiums is implied volatility. Generally, higher volatility means options are more valuable due to the asymmetric payoffs that options provide. Thus, expectations for short-term volatility have a significant impact on options pricing.

As the accompanying chart shows, premiums earned by XYLD tend to have a positive correlation with the Chicago Board Options Exchange's CBOE Volatility Index ( VIX ). Since XYLD is structured specifically to earn call option premiums, XYLD's monthly distribution is heavily dependent on the level of premiums it could earn in the options market.

Global X - XYLD Presentation Materials

{kind=link}

Thus, XYLD would generate better returns when implied volatility is high. This presents another problem for investors. Recall the three possible scenarios that we have discussed previously. Only in the second scenario where the underlying asset is flat do investors truly benefit from XYLD by earning a premium in a sideways market. However, high implied volatility tends to occur during periods of heightened risk and uncertainty, when markets are more likely to swing one way or the other.

In Conclusion

We believe that we have adequately highlighted the key risks and trade-offs associated with trading a covered call options strategy like the XYLD.

Overall, we see no real advantage in employing a covered call strategy for most investors, unless one is absolutely confident of timing the markets with a high level of precision.

Then again, if one knows for sure how the market is going to move, then a covered call strategy for earning a small premium would be rather pointless. The genius is better off just waiting for the next big swing and betting the house.

For further details see:

XYLD: Why Covered Calls On The S&P 500 Is A Bad Strategy