XYL - Xylem Is A Good Buy At The Current Levels

2023-08-18 12:41:37 ET

Summary

- Xylem has good growth prospects driven by backlog, end market demand, government stimulus, aging water infrastructure, AMI technology, and revenue synergy from the Evoqua acquisition.

- The company reported strong revenue growth in Q2 2023, driven by organic growth and benefits from the Evoqua acquisition.

- Xylem's margins are expected to improve due to volume leverage, easing inflationary headwinds, cost synergies from the Evoqua acquisition, and productivity initiatives.

Investment Thesis

Xylem ( XYL ) has good growth prospects driven by healthy backlog, good end market demand, government stimulus funding, aging water infrastructure, continued adoption of AMI technology and potential revenue synergy from Evoqua acquisition. Volume leverage, easing inflationary headwinds and cost synergies from Evoqua acquisition should help margins. The company is not seeing any slowdown so far and raised its revenue and adjusted EBITDA margins guidance when it reported its Q2 2023 results earlier this month. The stock is trading below its historical average and looks like a good long-term buy at the current levels.

Revenue Analysis and Outlook

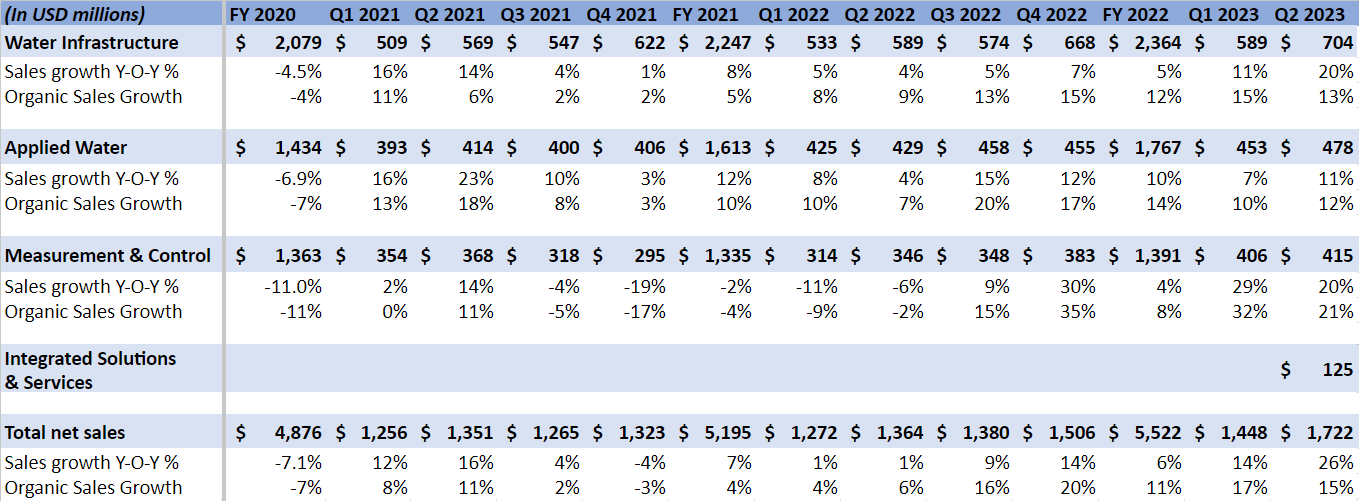

I previously covered Xylem in March this year where I talked about the strong growth that the company’s Water Infrastructure and Applied Water business has seen in the recent years. While its Measurement & Control Solutions (M&CS) segment faced issues due to chip shortages from mid-2021 to mid-2022, I expected the situation to improve and the segment’s sales to see good growth. The company has reported its Q1 and Q2 results since then and the organic growth for MC&S segment in these quarters came in strong at 32% Y/Y and 21% Y/Y, respectively, validating my thesis.

In the second quarter of this year, the company reported ~26% Y/Y increase in revenue, driven by 15% Y/Y organic growth and the benefits from the recently completed Evoqua acquisition. Segment Wise, Water Infrastructure revenue grew ~20% Y/Y helped by ~13% Y/Y organic growth and ~$53 million contribution from Evoqua’s Applied Product Technologies segment which is now integrated in this segment. Organic revenue growth was driven by effective price realization and healthy demand across all end markets and geographies. Applied Water Segment revenue grew 12% Y/Y organically driven by strong price realization and strength in commercial building and industrial end markets, partially offset by the decline in residential end market. As discussed earlier, the Measurement and Control segment revenue increased 21% Y/Y organically due to the improvement in chip supply. Chip shortages easing facilitated the backlog execution, helping revenues. The segment also saw a good demand for pipeline assessment services. Finally, the company’s new segment Integrated Solutions & Services ((ISS)), which became a part of the company as a result of the recent Evoqua acquisition and has a significant recurring revenue base (~75%), also saw strong price realization and backlog execution.

XYL’s Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company ended the quarter with a strong backlog of ~$1 billion, which was up ~15% Y/Y. This gives good visibility on the company’s near-term growth prospects. In addition, demand for the company’s products remains healthy across its end markets despite concerns about the macroeconomy, as is evident from a 4% Y/Y growth in orders last quarter and book-to-bill of greater than 1.0. The defensive nature of the company’s products/end markets and price increases are helping it weather the broader macroeconomic slowdown.

Further, the company is also well poised to benefit from government stimulus programs like Inflation Reduction Act and other legislation in the medium-term. Aging water and wastewater infrastructure in North America and Europe is another demand driver for the company’s products. Additionally, according to management, we are still in the early phase of AMI adoption in the U.S. and that continues to show up in the company’s bidding pipeline and new order wins.

While there seems to be some skepticism surrounding the potential revenue synergies from the Evoqua acquisition among bears (that partly explains why the stock is available at a significant discount to its historical valuation), I believe just the fact that Xylem has a good international presence, and it can use its network there to sell Evoqua’s products means there can be meaningful revenue synergies in the years ahead. Note that Evoqua derives ~82% of its sales from U.S. while pre-Evoqua acquisition Xylem used to derive ~55% of its sales from non-U.S. geographies.

So, I am bullish on the company’s revenue growth prospects. Further, the company has a strong balance sheet with 1.4x net debt to EBITDA and $700 million in cash and cash equivalents at the end of the last quarter. So, further M&A cannot be ruled out, providing additional inorganic growth avenues.

Margin Analysis and Outlook

In the second quarter of FY23, the company’s adjusted EBITDA margin increased 250 bps Y/Y to 19.1% helped by volume leverage, productivity gains, and strong cost price dynamics which more than offset the impact of inflation, increased strategic investments, and an unfavorable mix. The acquisition of Evoqua also provided 50 bps tailwind to the margin.

XYL Segment-Wise Adjusted EBITDA margin (Company Data, GS Analytics Research)

XYL Total Adjusted EBITDA margin (Company Data, GS Analytics Research)

Looking forward, I expect supply chain constraints and inflation to continue easing. This coupled with volume leverage and productivity initiatives by management should help margins. Management is also anticipating $140 million in cost synergies from Evoqua integration. According to them, the company has seen good early momentum in these plans and Xylem should exit this year with ~40 million run-rate savings. The company is targeting these cost savings across procurement, Footprint & Network optimization and other areas. So, I expect the margins to continue improving.

Valuation and Conclusion

The company is trading at 27.42x FY23 consensus EPS estimates and 25.05x FY24 consensus estimates, which is a discount to its 5-year historical levels of 35.15x. Usually the companies exposed to water end-market trades at high multiples given the long-term secular growth opportunity in this market. For example, Tetra Tech ( TTEK ) trades at 29.95x FY23 consensus EPS estimates, while Badger Meter( BMI ) trades at 53.07x FY24 consensus estimates.

I believe at the current valuation, investors are not pricing in much synergy from the Evoqua acquisition and there is the potential for positive surprise. Even without it, the company’s strong execution history and secular growth prospects leaves a substantial room for upside for longer term investors. Hence, I have a buy rating on the stock.

For further details see:

Xylem Is A Good Buy At The Current Levels