BMI - Xylem: Strong Growth Potential

2023-03-29 07:51:08 ET

Summary

- Xylem should benefit from the high backlog, resilient end markets, and medium to long-term drivers like aging infrastructure and government stimulus.

- The acquisition of Evoqua water technologies is also expected to be a good growth driver for the company.

- Cost reductions in materials, labor, and freight should positively impact margin expansion.

- Currently trading at a discount to its historical levels, Xylem is a good investment.

Investment Thesis

Xylem ( XYL ) is poised to do well in the current economic cycle due to the critical nature of its solutions. The strong backlog level, price increases, and resilient end markets are expected to drive revenue growth in FY2023. The long-term growth potential is strengthened by benefits from IIJA, the acquisition of Evoqua Technologies, and secular trends such as aging infrastructure.

The adjusted EBITDA margin is expected to improve in FY2023, driven by declining inflation in material, labor, and freight costs. This, along with cost synergies from the Evoqua acquisition, should be a positive factor in margin expansion. Currently trading at a discount to its 5-year historical P/E, Xylem presents a good investment opportunity.

Revenue Analysis and Outlook

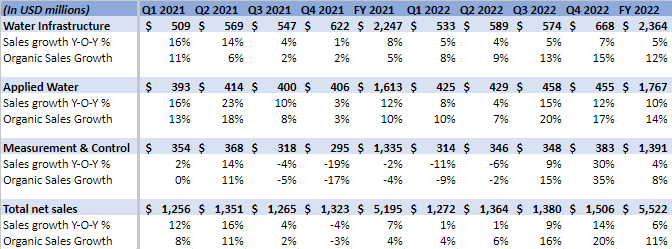

The company's Water Infrastructure and Applied Water segments have experienced strong growth in recent years. However, its Measurement & Control Solutions (M&CS) segment faced challenges from mid-2021 to mid-2022 due to chip shortages. Fortunately, the chip shortage situation improved in the latter half of 2022, supporting revenue growth in the M&CS segment. This, combined with sustained demand in the Water Infrastructure and Applied Water segment, resulted in solid net sales growth of ~14% YoY and organic sales growth of ~20% YoY in Q4 FY2022, and net sales growth of ~6% YoY and ~11% YoY organic growth in FY2022.

XYL's Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

In the current fiscal year, Xylem's revenue growth should be driven by strong backlog levels, price increases, and improvement in the chip supply situation in the M&CS business which should increase backlog conversion. In addition, the continued OPEX strength in the wastewater business and large installed base should help the company's revenue. The long-term growth potential of the company is supported by secular trends, benefits from IIJA, and the acquisition of Evoqua Technologies.

High Backlog and Price Increases

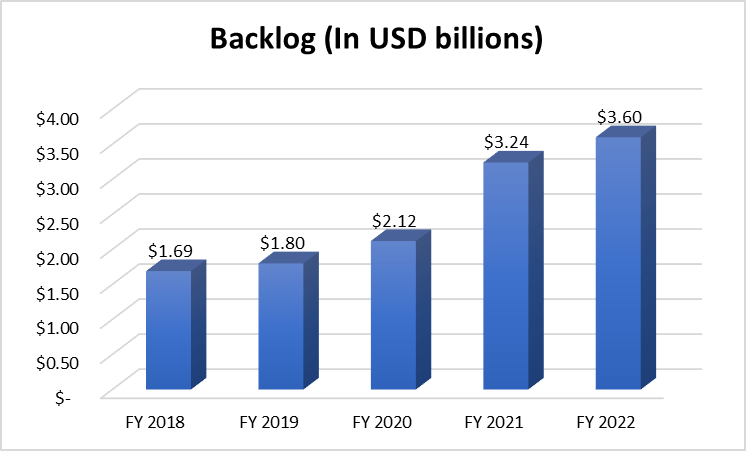

The supply chain constraints and chip shortages over the last several quarters have led to a high backlog of $3.6 billion for the company at the end of FY2022. The backlog in the Measurement & Control Solutions (M&CS) segment at the end of FY2022 was high at $2.1 billion, up 14% Y/Y. However, the company has started seeing some improvement in these challenges in the latter half of FY2022 and I expect them to continue in the coming quarters. This, in turn, should result in a higher backlog-to-sales conversion rate and support revenue growth in FY2023. Additionally, Xylem increased its product and service prices in late 2022, and the benefits from the carryover impact of these price increases are expected to contribute to increased revenue YoY in the upcoming quarters.

Xylem's Backlog (Company Data, GS Analytics Research)

{kind=link}

Resilient End Market Demand

Further, while there are a lot of worries around the broader macroeconomic slowdown, Xylem is much better placed versus other companies.

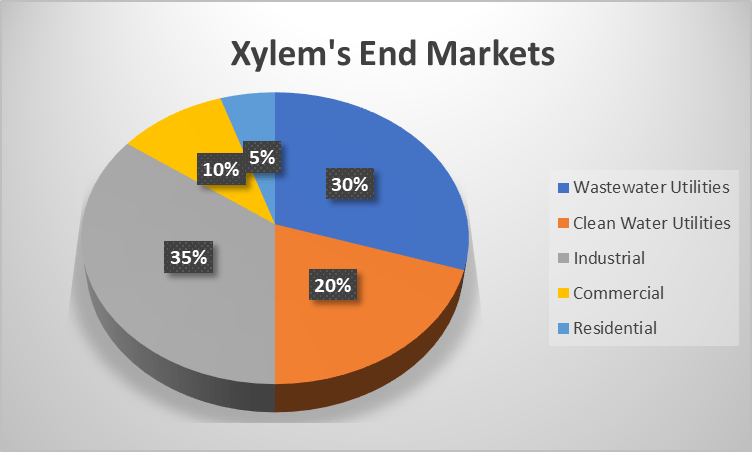

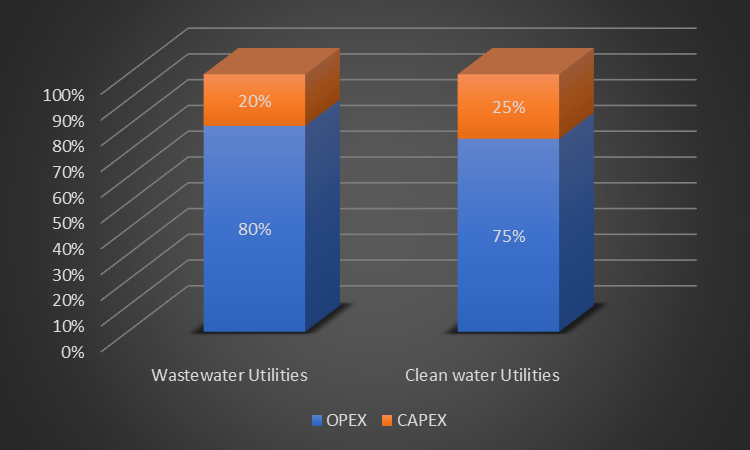

XYL's End Market (Company data, GS Analytics Research) XYL's Utilities End-Market Exposure (Company's Investor Presentation)

{kind=link}

{kind=link}

Xylem's utility end market is divided into clean water utilities and wastewater utilities, with the latter expected to benefit from continued healthy operational expenditures by its customers. The company provides mission-critical applications to help its customers with their complex problems like aging pipes on the brink of collapse and sewer lines leaching waste into groundwater, etc. Such repairs cannot be usually postponed. By leveraging its large installed base of 80 million installed devices and over 20,000 customers (particularly in the US and Western Europe), the company is well positioned to continue generating a steady stream of recurring revenue in the coming year.

Xylem is under-penetrated in the international clean water utilities end market, but with an increased focus on aging infrastructure and climate change, new opportunities are emerging. The continued growth of Advanced Metering Infrastructure ((AMI)) systems, which gather information through a network of data collectors or gateway receivers and eliminate the need for manual meter readings, should benefit the company internationally as well, and help gain market share. While chip shortages impacted growth in the clean water business in the recent past, the situation has improved. The company's value proposition and the improvement in chip shortages bode well for increased revenue in the coming quarters.

The industrial end market is getting impacted by macroeconomic uncertainty. However, I expect demand for Xylem's product to remain resilient in this market as well. According to the management, Xylem offers equipment that keeps its customer's businesses up and running and is not related to output generation. For eg., Xylem manufacturers pumps which help in moving industrial fluids waste. Even if the output is cut, a factory will still need that pump to remove the waste fluid. So, considering the nature of its products, Xylem's business should remain resilient even if the industrial output is decreased. Further, the demand for dewatering services is expected to remain high especially in the mining industry due to high commodity prices. This should also aid the growth of this business.

The company's commercial and residential end markets are expected to slow due to high-interest rates. However, ~70% of sales in the commercial end market and ~90% of sales in the residential business are from the aftermarket which is usually less cyclical. Further, after the recent banking fiasco, the Federal Reserve is likely to become less hawkish paving a path to recovery for the new construction portion (where the exposure is very small anyway) of these businesses in FY2024.

Overall, the company's end markets are much better positioned compared to a lot of other industrial companies, and its high backlog and improving backlog conversion along with strength in wastewater and clean water utilities should more than offset the slowdown in the company's new construction business related to commercial and residential end markets.

Long-Term Growth Drivers

In addition to resilient end market demand and a good near-term revenue outlook, the secular growth trends of aging infrastructure in the US and increased investment in water infrastructure in emerging markets present significant growth opportunities for XYL in the future. There is an increased focus on addressing the challenges related to safe drinking water, sanitation, hygiene, and irrigation in emerging markets, leading to increased investment. To seize these opportunities, XYL is localizing its products by manufacturing in these markets, allowing them to create fit-for-market products and services that meet market requirements and price points.

XYL is also set to benefit from funding related to IIJA in FY2023 and beyond. The US government has allocated $50 billion towards Resilient Water Infrastructure and $55 billion towards Clean Drinking Water projects, creating significant growth opportunities for the company. Furthermore, the State Revolving Fund ((SRF)) program, which offers low-interest loans for constructing or repairing wastewater and drinking water plants, is also a potential source of growth for XYL.

End market Revenue (Company's Investor Presentation) Revenue by Geography (Company's Investor Presentation)

{kind=link}

{kind=link}

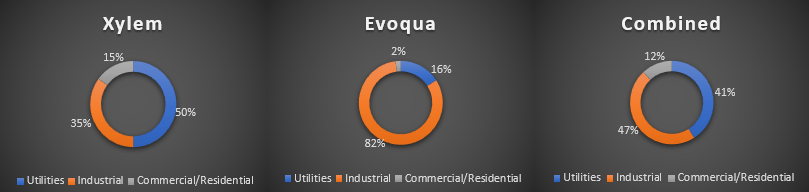

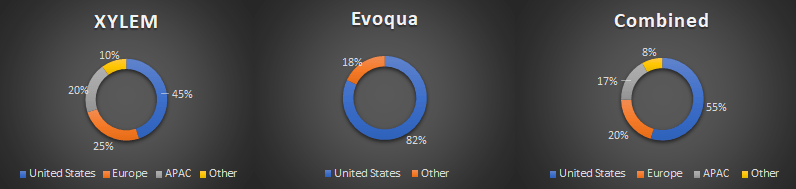

Recently, XYL acquired Evoqua Technologies in an all-stock transaction worth $7.5 billion. Both companies present exciting revenue synergy opportunities that should benefit them in the coming years. Evoqua's strong presence in the industrial end market (accounting for 82% of its total end market) should bolster XYL's relationship with customers and expand the reach of its products and services, particularly in North America. Additionally, XYL's international footprint and established customer base should help extend Evoqua's global reach and drive future revenue growth. Despite Evoqua having the largest team of treatment service professionals in North America, its global market exposure is only 18%. So, I believe that with its market presence in Western Europe and the Asia-Pacific region, XYL should bring further benefits to Evoqua in terms of international expansion.

Margin Outlook

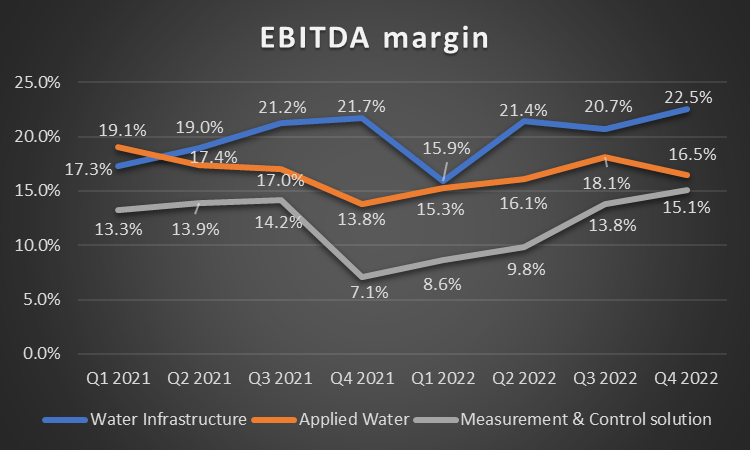

While the adjusted EBITDA margin was negatively affected by higher inflation, supply chain challenges, increased strategic investments, and volume deleverage in the M&CS segment in late 2021 and early 2022, things improved in the latter half of 2022 and strong price realization and productivity savings offset the inflationary pressure on the material, labor, freight, and overhead costs. This, combined with a moderate improvement in supply chain constraints, led to a margin expansion in the fourth quarter, with an adjusted EBITDA margin of 18.7%, an increase of 250 basis points YoY.

XYL's adjusted EBITDA margin (Company data, GS Analytics Research)

{kind=link}

Looking forward, I anticipate that the adjusted EBITDA margin will show improvement in the near future, due to favorable price-cost dynamics and the integration of Evoqua into the company.

The inflation in material, labor, and freight costs is easing. This, combined with the residual effects of previous price hikes from late last year, should lead to margin expansion in FY2023. Further, even if inflationary pressures arise in the future, management has indicated that they will raise their prices to more than compensate for the cost impact.

XYL has also identified $140 million in cost synergies with its recent acquisition of Evoqua Technologies. These synergies are expected to be realized within three years and will help drive margin expansion. The synergies will come from three main areas: procurement, footprint and network optimization, and back-office functions. By leveraging the enhanced purchasing power of the combined base, XYL plans to realize scale efficiencies and procurement cost savings. Footprint and network optimization will be achieved through consolidating offices and branches where opportunities exist. Lastly, the company plans to reduce SG&A costs by eliminating duplicative public company costs and functional overlaps in back-office functions.

Valuation and Conclusion

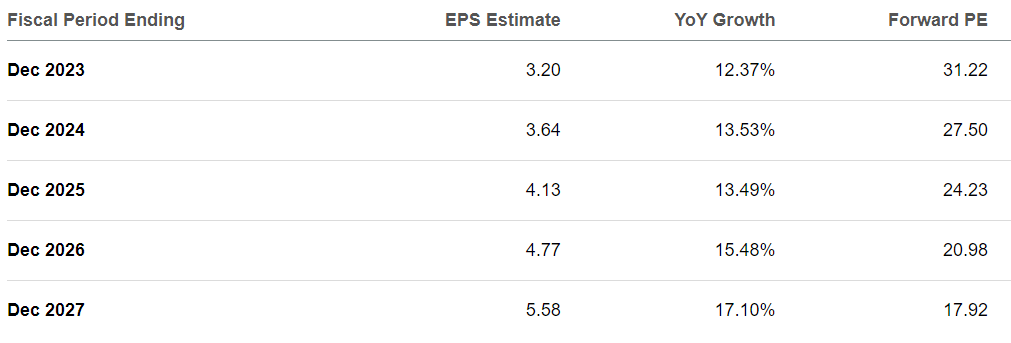

XYL is currently trading at 31.04x FY2023 consensus EPS estimates of $3.20 and 27.34x FY2024 consensus EPS estimates of $3.64. This is a discount to its 5-year average ((FWD)) P/E of 34.57x. If we look at high-quality companies with good execution history and exposed to the water end market, they usually trade at high valuations. For example, Badger Meter ( BMI ) is trading at 45.95x FY2023 consensus EPS estimates while Tetra Tech ( TTEK ) is trading at 28.82x FY2023 consensus EPS estimates. The reason behind high valuations is a secular growth opportunity and the defensive nature of water-related services.

{kind=link}

XYL is expected to post double-digit EPS growth for the next several years and once macroeconomic concerns wane, I believe its P/E multiple should again re-rate to near historical levels. This should drive long-term outperformance and hence, I have a buy rating on the stock.

For further details see:

Xylem: Strong Growth Potential