YGRAF - Yangarra Resources: Absurdly Cheap

2023-03-27 06:29:14 ET

Summary

- Despite increases in production and G&A costs due to inflationary pressures, FFO increased 95% YoY while net debt fell 34%.

- 2022 profitability is unlikely to be repeated in the lower commodity price environment.

- Using conservative estimates, YGR still trades at 1.22x 2023 FFO and is absurdly cheap.

All figures are in CAD unless otherwise noted as that is the company's reporting currency.

Introduction

Yangarra Resources ( YGR:CA ) (YGRAF) is a junior oil and gas company engaged in the exploration, development and production of natural gas and oil with operations in Western Canada, with a main focus on the Cardium region in Central Alberta, where the Company has extensive infrastructure and land holdings.

The Cardium region was uneconomical to drill until the last ten years until advances in horizontal drilling took off. One of my favourite junior E&Ps in the region is InPlay Oil ( IPO:CA ) who I have written on numerous times.

YGR has been known for being a little more indebted than its peers but has taken advantage of the commodity bull run to put excess cash flows towards debt reduction. In fact, net debt fell 34% YoY from 2021 to 2022 putting them at less than 1:1 Net debt/TTM EBITDA. The higher than average leverage is acceptable given that YGR's operating costs per barrel are fairly modest at only $7/bbl.

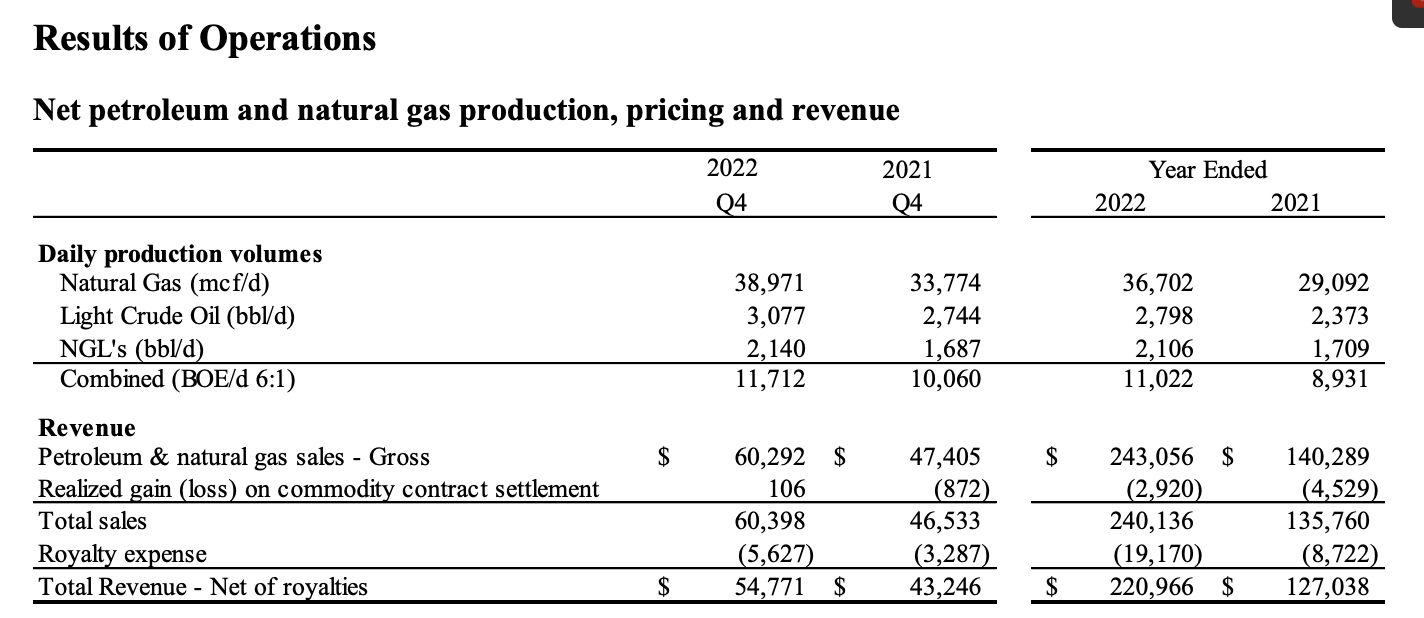

2022 FYE MD&A (Yangarra Resources)

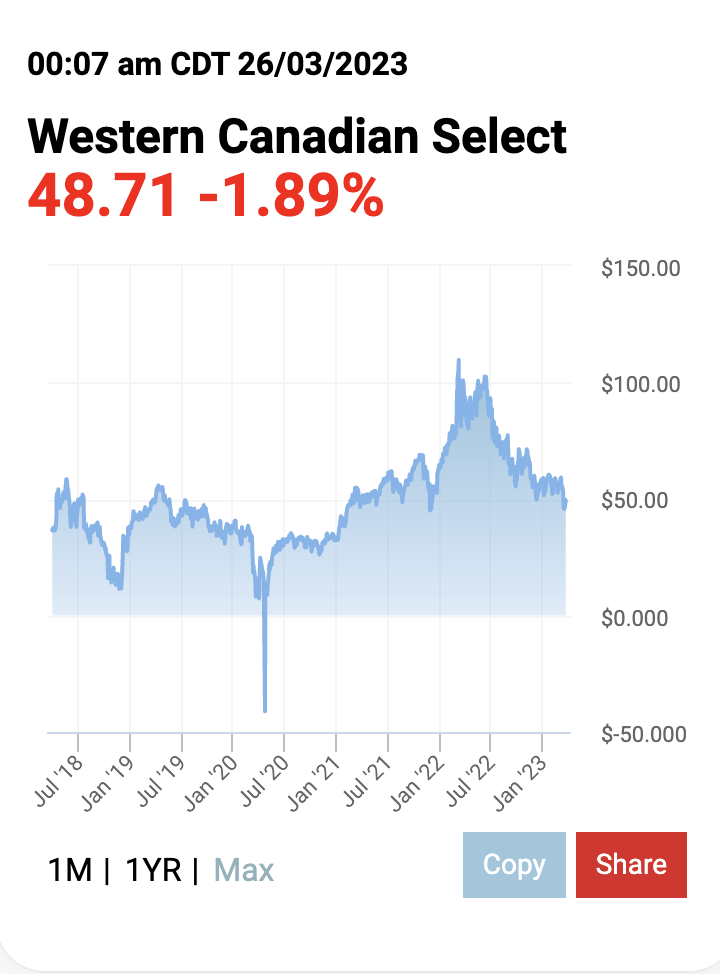

55% of YGR's production is from natural gas which averaged well over $5.50/mcf in 2022 but light crude contributed substantially to revenues in 2022 as a result of record high West Canadian Select Pricing on their light crude oil which was well over $100/bbl throughout most of 2022.

2022 FYE MD&A (YANGARRA RESOURCES) Western Canadian Select (Oil Price Charts)

{kind=link}

{kind=link}

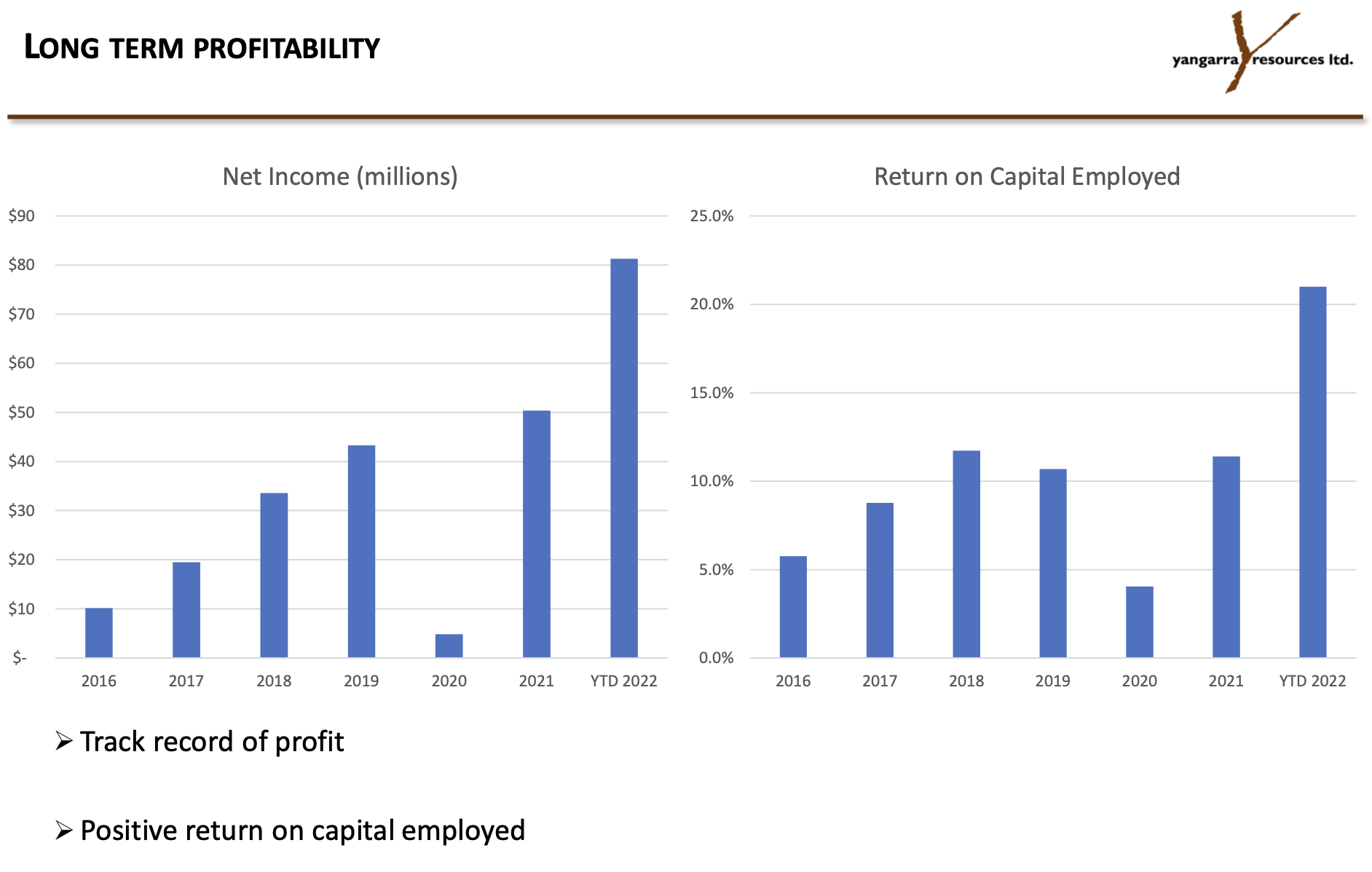

Despite increases in production and G&A costs due to inflationary pressures FFO increased 95% YoY from $90 Million to $177 Million which mostly went towards repaying debt rather than returning cash to shareholders. YGR also realized record high operating netbacks as a result of taking advantage of higher commodity prices.

The low cash costs allow for incredible profitability in any economic environment. Even in 2020 when the average WTI price was $38/bbl and AECO prices were $2.30 which were among ten year lows, YGR still produced positive net income and an ROCE of ~4% while most of its peers lost money. ROCE has averaged over 10% since 2018 YE.

Q3 2022 Investor Presentation (YANGARRA RESOURCES)

{kind=link}

Outlook

Despite YGR having a record year in fiscal 2022 the share price has declined 38% since its fiscal YE and has done a lot worse than its peers since that time as a result of being more leveraged to commodity prices. In fact, YGR has almost no hedges in place for 2023 unlike its peers.

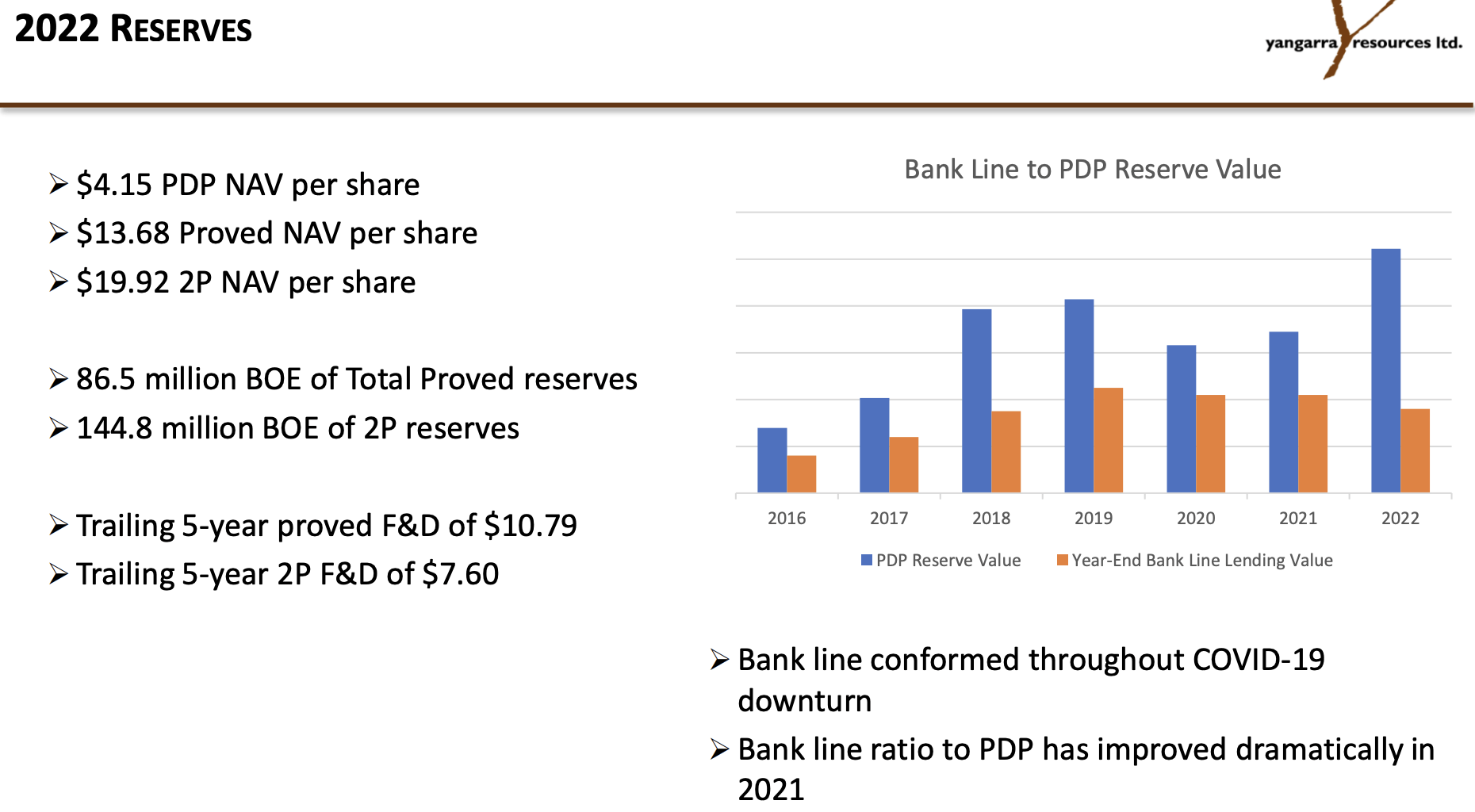

YGR certainly looks cheap on a trailing and liquidation basis. In fact, management has valued 1P reserves alone at $4.15/share which is 2.4x its current share price and just screams cheap. Essentially management is saying by buying shares in the company you are buying a $69/bbl barrel of oil for only $12/bbl which seems like a steal.

Corporate Presentation February 2023 (Yangarra Resources)

{kind=link}

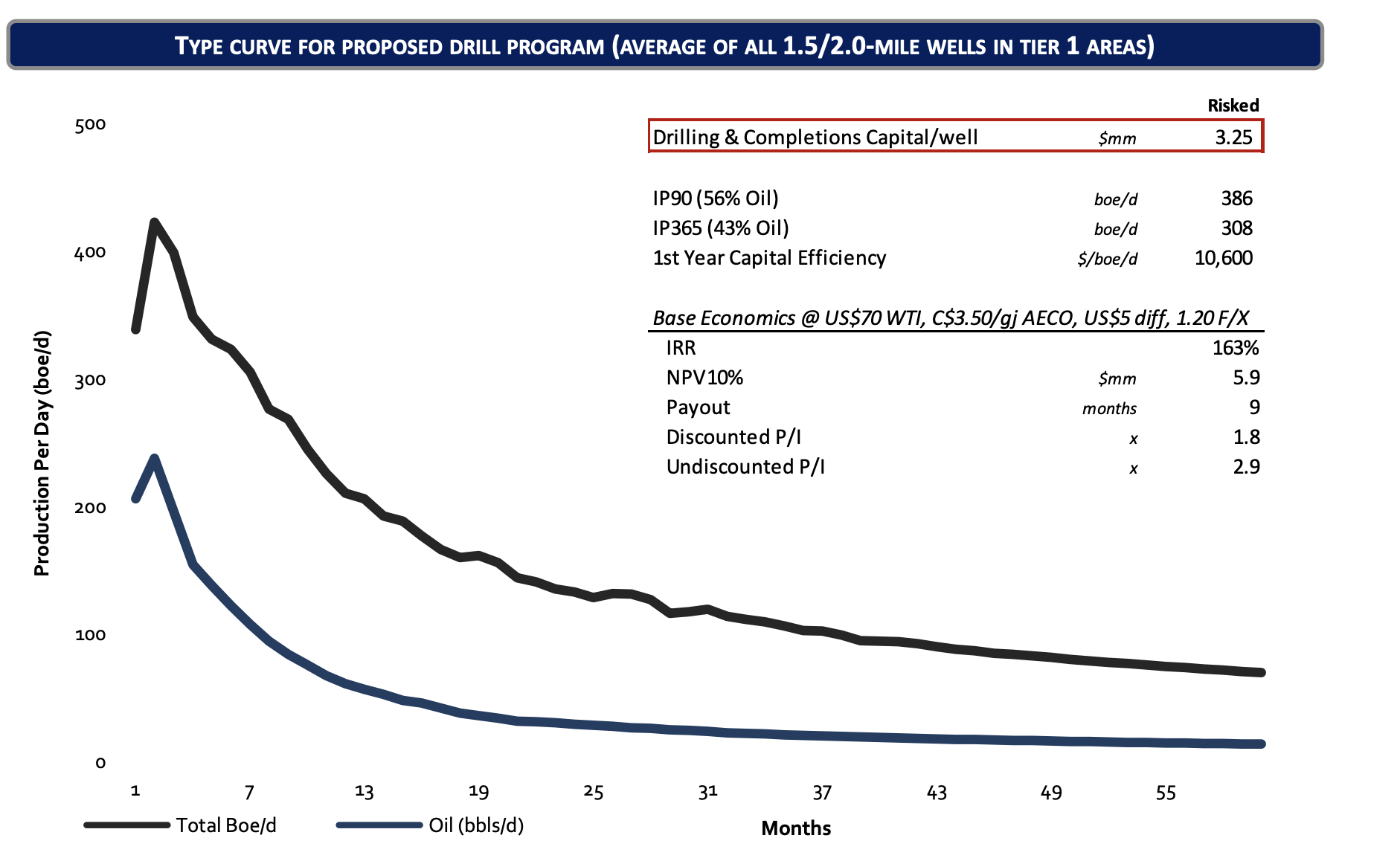

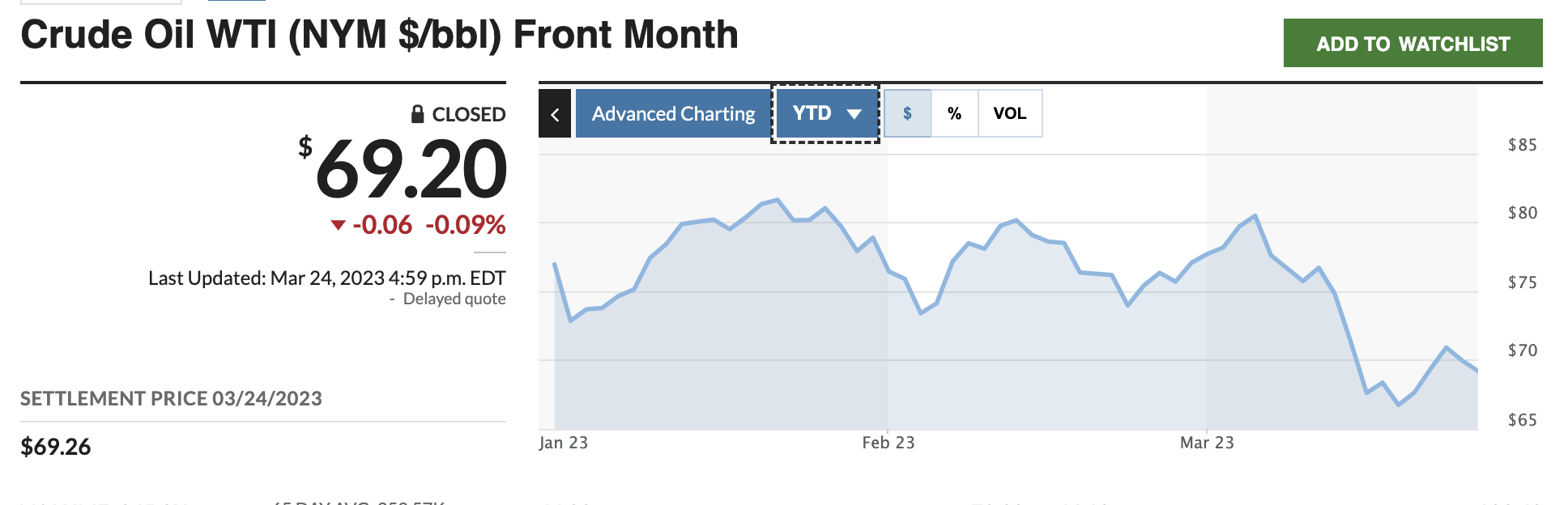

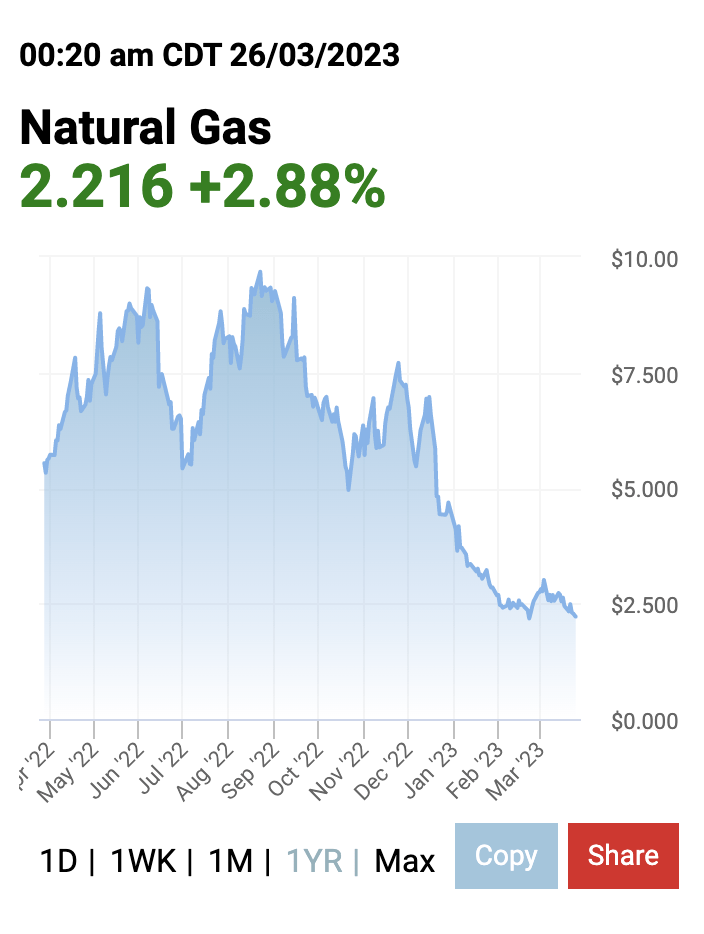

Unfortunately, the commodity environment has changed since management valued their reserves at 2022 YE. First, let's take a look at YGR's production curve. On the positive side the relatively low percentage of capital needed to grow production at only $3.25 Million per well is very low. The curve declines at a slower rate than an unconventional well, which allows capital costs to become a small portion of the cash flow which is what helps boost their ROCE even in weak commodity environments. YGR can keep exploration expenses low as these wells have long lives. On the negative, half of oil production is typically realized in the first five years, after which point the production mix gets extremely tilted towards natural gas which is why their production mix is typically more than 50% in natural gas and liquified natural gas. Not only are oil prices down 14% since earlier in the year but natural gas prices have fallen like a rock going down to $2.20/mcf currently. YGR's realized gas prices were over $5.60/mcf in 2022 so current prices are less than half what they were one year ago.

Q3 2022 MD&A (Q3 2022 Investor Presentation) WTI Prices (Market Watch) AECO (Oil Price Charts)

{kind=link}

{kind=link}

{kind=link}

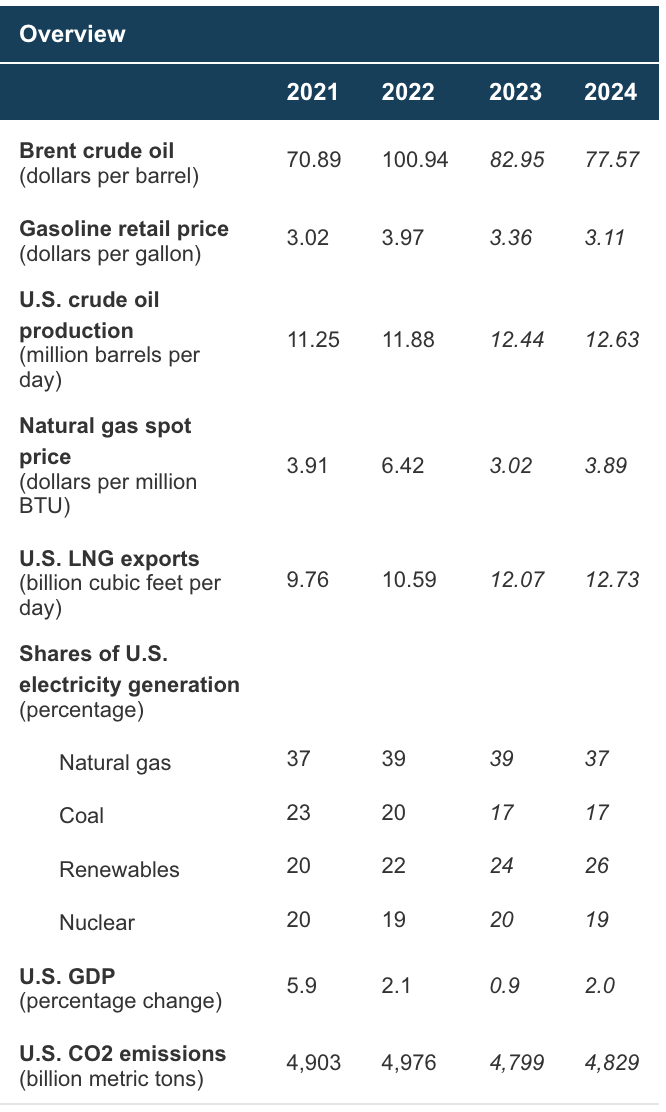

The EIA's recent energy forecast suggested weakened commodity prices in 2023 and 2024:

U.S natural gas consumption would average 99.1 billion cubic feet per day, down 5% from 1Q22 due to milder temperatures that have reduced demand for space heating. Residential and commercial consumption, would fall by 11% YoY. Global liquid fuels consumption would increase by 1.5 million barrels per day in YoY and by an additional 1.8 million b/d in 2024. China is the main driver of growth in 2023 as the country shifts away from its zero-COVID policy. Russia recently announced a crude oil production cut of 0.5 million b/d for March, and we expect declines to be more than that, with Russia’s production falling by 0.7 million b/d in March. Despite the declines in March, recent petroleum exports from Russia have outpaced expectations, and we have revised our oil production forecast for Russia upwards by 0.4 million b/d in 2023. Overall, we expect global oil and liquid fuels production will average 101.5 million b/d in 2023, up 1.6 million b/d from 2022.

Source: Short-term Energy Outlook

EIA Forecast (EIA )

{kind=link}

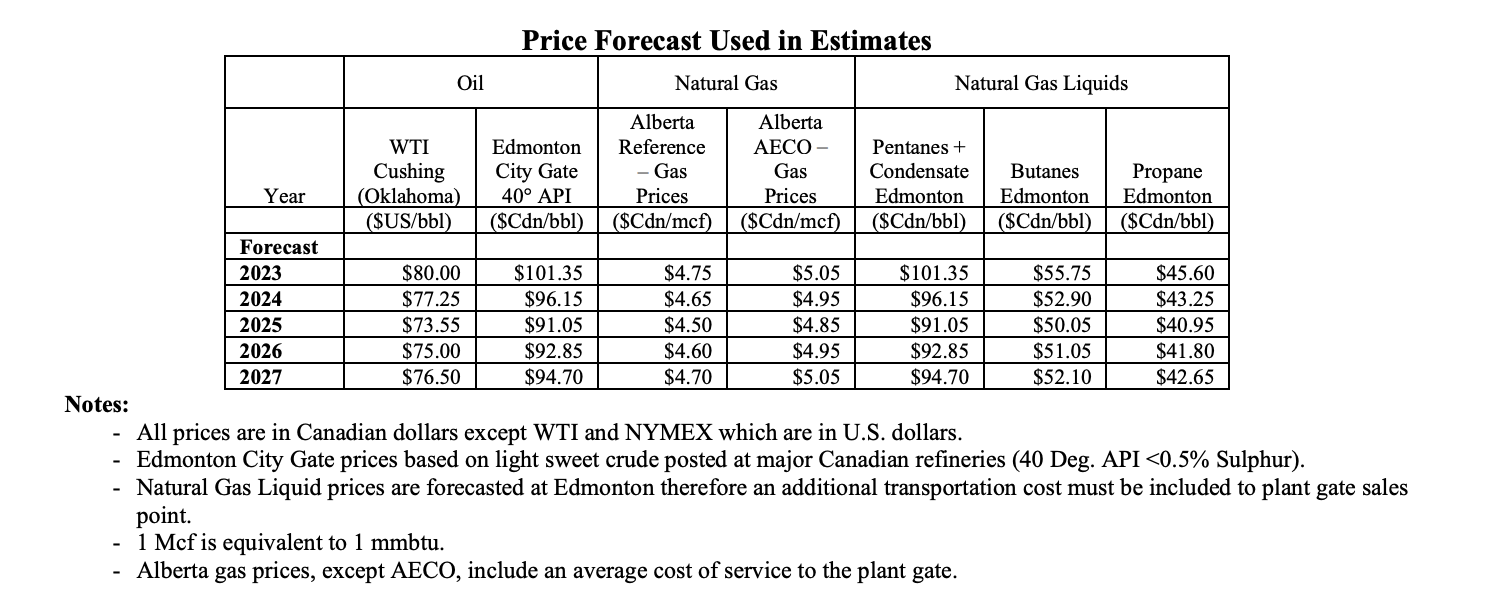

Therefore, management estimates for at least 2023 and 2024 appear a little too aggressive with WTI prices averaging $80/bbl and AECO prices averaging $5/mcf. Management has also used this pricing for their CAPEX budget in 2023 as the Board of Directors has approved a capital budget of $125 Million for 2023, which includes the drilling of 33 wells which will keep one drilling rig fully utilized for the year. The budget is expected to increase YGR's production to 13,000 boe/d. At 2022 pricing FFO would easily cover this at $180 Million but that FFO is reachable at WTI prices of $85/bbl and $3.50/mcf AECO prices which are not available in the market today.

{kind=link}

Using more conservative pricing assumptions below, most notably WTI prices of $75/bbl and $3/MCF AECO pricing, I estimate a $27/bbl operating netback, $126 Million in FFO, and FFO of $1.38/share for 2023.

Production Crude Oil bbls/d 3,300 Natural Gas bbls/d 2,484 NGL mmcf/d 43,289 Total boe/d 13,000 Pricing WTI bbl $75 AECO mmcf $3.00 CAD/USD $1.30 $/BOE Sale Price $43.34 $203 Royalties (8% of revenue) $3.47 $16 Transportation $1.21 $6 Production $6.07 $28 G&A $1.01 $5 Corporate Tax $0.43 $2 Interest Expense $2.79 $13 Total $14.98 $70 FFO $133 CAPEX $125 Net Debt/FFO 1.02 FFO/share $1.44 Price/FFO 1.22x Data by YCharts

Key takeaways:

- Pricing/BOE will be in line with fiscal 2021 in the lower commodity price environment but higher production should still lead to higher FFO despite higher production and G&A costs.

- FFO will likely barely cover planned CAPEX, so should not expect major debt reduction and shareholder returns via dividends or share buybacks in 2023. This would explain the rational for the recent $15 Million Bought Deal as additional capital would be needed for CAPEX plans.

- FFO/share will fall as much as 27% YoY as a result of the lower commodity price environment.

- YGR still trades extremely cheap at just 1.22x my 2023 FFO estimate. The analyst community agrees that it trades at a very cheap multiple at this year's expected cash flow indicating tremendous downside risk.

- Although management guidance may look aggressive. With more conservative pricing assumptions, the stock is still cheap.

As of March 6th, 2023 YGR announced it entered into an equity financing agreement, on a bought deal basis, with a syndicate of underwriters led by ATB Capital Markets Inc. and CIBC ( CM ). YGR would issue 5,905,600 common shares at a price of $2.54/share. YGR also granted to the Underwriters an option to purchase additional shares, equal to 15% of the number of shares sold pursuant to the offering at the offering price. The total aggregate gross proceeds were $15,000,224 and up to $17,250,257 pursuant to the full exercise of the Over-Allotment Option. Proceeds will assist in developing the Chambers region which is a 15 mmcf/d compression facility.

The stock was issued at a 10% premium to the then market price of $2.30/share so would hardly say the shares were dilutive to shareholders. CM and ATB seem to think the company is undervalued as well.

Conclusion

Although the commodity bull run witnessed since the end of 2020 may have stalled out and fiscal 2023 may not be as strong for YGR, the junior E&P company can still produce massive profits at current prices and in pursuing more aggressive CAPEX plans should be able to boost free cash flow available to shareholders in later years.

Although the company is not as screaming cheap as management has suggested, the market has clearly overreacted to the prospect of reduced profitability which has made the stock absurdly cheap. Downside protection is immense as remember YGR was still ROCE positive in 2020.

For further details see:

Yangarra Resources: Absurdly Cheap