YGRAF - Yangarra Resources: Back To Normal

2023-10-13 11:54:03 ET

Summary

- Yangarra Resources Ltd. faces delays in growth due to weather interruptions and wildfires. This El Nino winter promises to be far less challenging.

- Despite challenges, the company has made progress in reducing debt and growing low-cost production.

- Management's experience and ownership of shares mitigate some of the risks associated with investing in a small company.

- The company is unusually profitable.

- A company like this just needs to grow to attract more investment attention.

Yangarra Resources Ltd. (YGRAF)(YGR:CA) wanted to repay debt while accelerating growth in the current fiscal year. Mother Nature had other ideas. The second quarter report listed the latest delays in a very frustrating year for company management. Of the items listed, Spring Breakup happens every year without fail. But the wildfire issue rarely reaches the heights of industry disruption that happened this year. Generally, wildfires are an issue that is over with as fast as it begins. But not this fiscal year. This happens after a brutal winter slowed operations to a crawl. The future appears to be very different.

Upcoming Winter

This upcoming winter apparently will have an El Nino effect. El Ninos are known for keeping the polar vortex up where it belongs without the "leaks" South that mark a La Nina (three years in a row no less). Therefore, management can work uninterrupted.

The high price of oil is likely to provide a little more cash flow than planned. It may not make up for shut-in production and delays caused by all the challenges in the first part of 2023; however, it will give management the opportunity to "make up for ground lost." That makes this coming winter forecast the complete opposite of a very frustrating current fiscal year so far.

The forecast for this coming winter is a welcome relief. As soon as fall comes, management will likely see if they can work a little more on the acreage to begin the catching-up process.

The Growth Quarters Are

Normally, the fourth quarter and first quarter are fairly busy quarters for the Canadian industry. The second quarter often has a Spring Breakup slowdown. The company operations get going again either late in the second quarter or early in the third quarter at the latest. The first quarter interruption in the current fiscal year cost production increases that normally would have been a relatively "sure thing." But then the second quarter compounded matters further.

The net result was that the bought deal financing ended up reducing debt, with not much else in the way of results so far. Without that offering, the company could have reversed at least some of the debt progress made in the previous fiscal year. The company could have afforded that. However, sometimes is wise to be conservative in case more years like the current one makes an appearance. This is a low-visibility industry.

However, the second half of the fiscal year promises to have fewer weather interruptions (so far anyway) than was the case in the unusual events of the first half of the fiscal year.

Management may yet get that accelerated production increase that was wanted at the beginning of the fiscal year. The nice thing about drilling in the area management is developing is that the risk of dry wells is extremely low. So, if operations can just get back to normal, then the delayed plans of management should get to the completion stage.

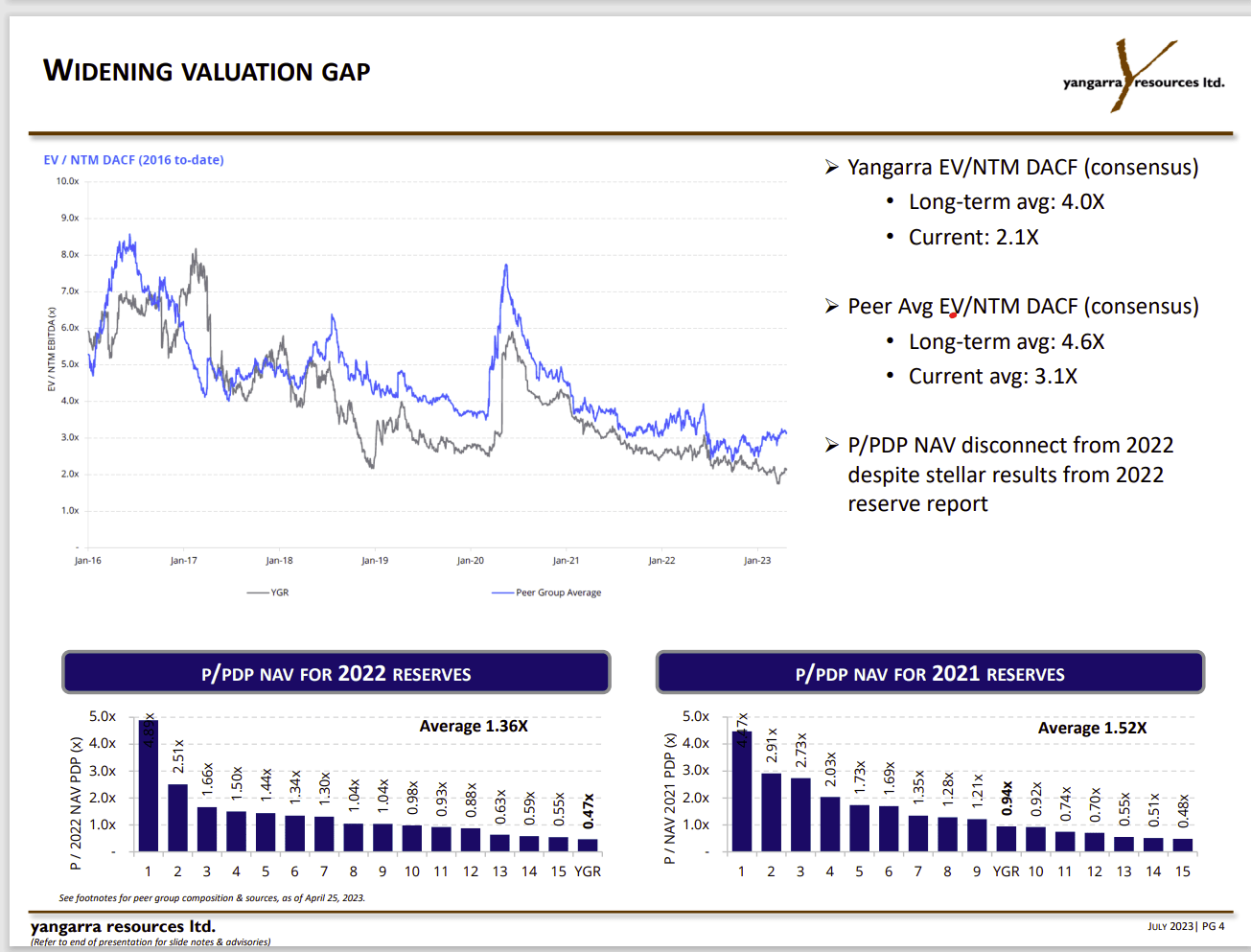

Yangarra Resources EV Comparative Valuation (Yangarra Resources Corporate Presentation July 2023)

{kind=link}

The slide itself demonstrates just how cheap the industry is in general. This company in particular has had some issues out of its control. That seems to warrant a discount in excess of other companies in the eyes of the market.

The stock price has gone down all year with one fiscal disappointment after another due to the weather events. Management was able to purchase a crane to save money and then could not use it as planned. You just have to love the low visibility of this industry (not).

But this is one of the very few companies that dug itself out of a debt hole because the wells drilled were profitable enough for that strategy to work.

(Canadian dollars unless otherwise stated.)

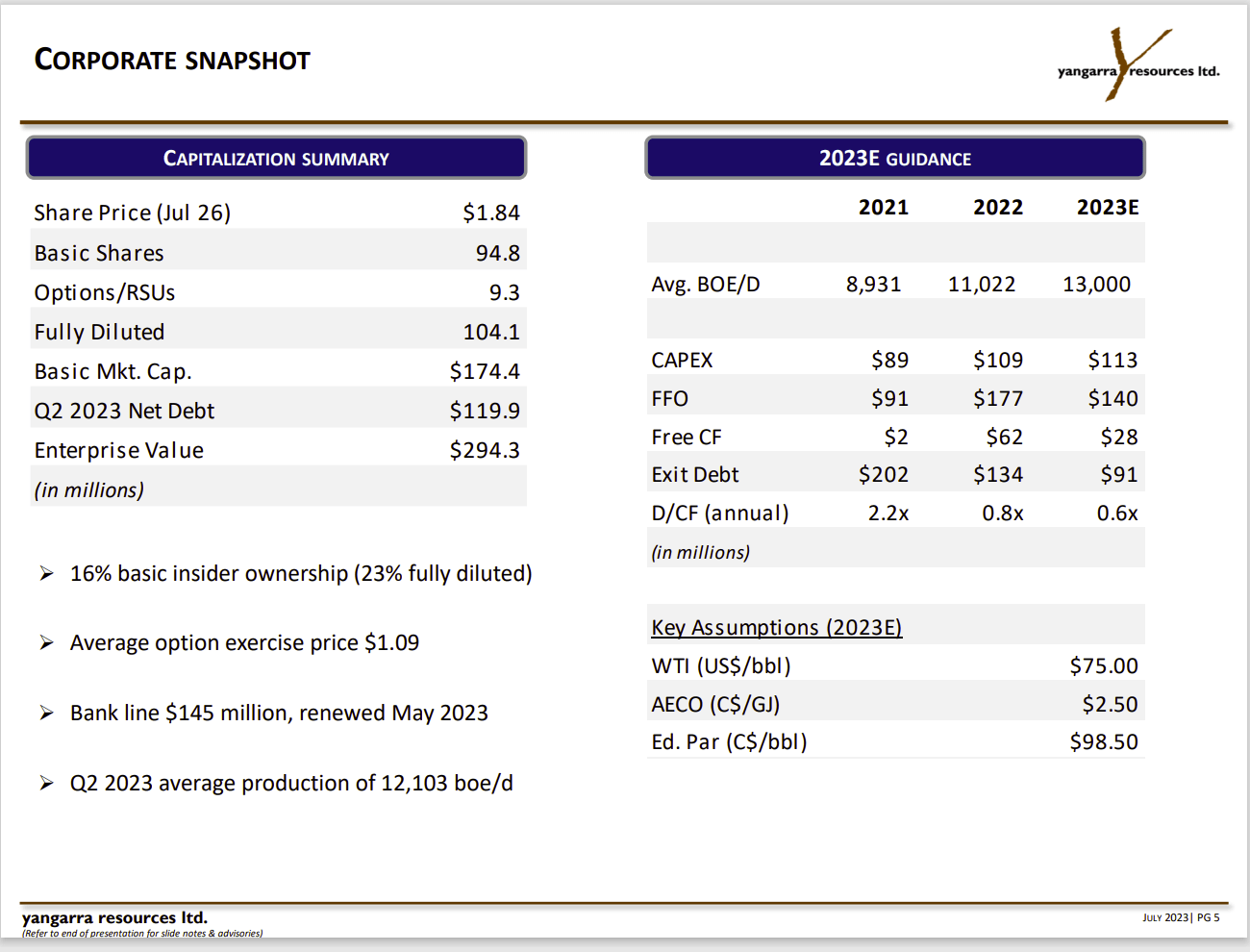

Yangarra Resources Corporate Financial Valuation Measures And Summary (Yangarra Resources Corporate Presentation July 2023)

{kind=link}

This company repaid roughly one-third of the debt load last year. The weather and wildfires combined with weaker commodity prices "put a dent" into the expected cash flow in the current fiscal year. However, maintenance costs appear to be low enough to allow for cash flow if lenders were to demand more repayments.

Management will likely firm up guidance once production is totally restored (if still needed) and the wildfires are not an issue. By repaying a lot of debt last year, management was able to build some flexibility in the current fiscal year with all its unexpected challenges. Let's see how management deals with the situation going forward.

As it is, the company made more progress on debt levels in one fiscal year than probably most of the companies I follow. There are several that could not have reduced debt that much over several fiscal years.

Nonetheless, the market appears to be focused on the current challenges rather than the overall progress made here. That should change as the year continues, and the wildfire issues begin to fade.

The debt ratio shown above is conservative even if commodity prices were considerably lower. Nonetheless, management has a lower goal for debt levels. Nothing wrong with that idea at all, because in this low visibility industry, it is hard to be too conservative when it comes to small companies.

The stock price is so low that one would think the company suffered a financial setback. While I am sure the challenges did cost something, finances here have always been conservative. Management has kept the bank line conservative as well.

It looks as though Mr. Market is worrying that the Wildfires and nasty winter will happen all over again. But that is very likely. Therefore, the stock likely has an asymmetrical return to the upside at the current price.

The debt level is now low enough to allow management to grow production even if the debt level does not decline this fiscal year (any more than it did in the first quarter). That growth should improve the debt level as it would increase expected cash flow.

(Canadian dollars unless otherwise stated.)

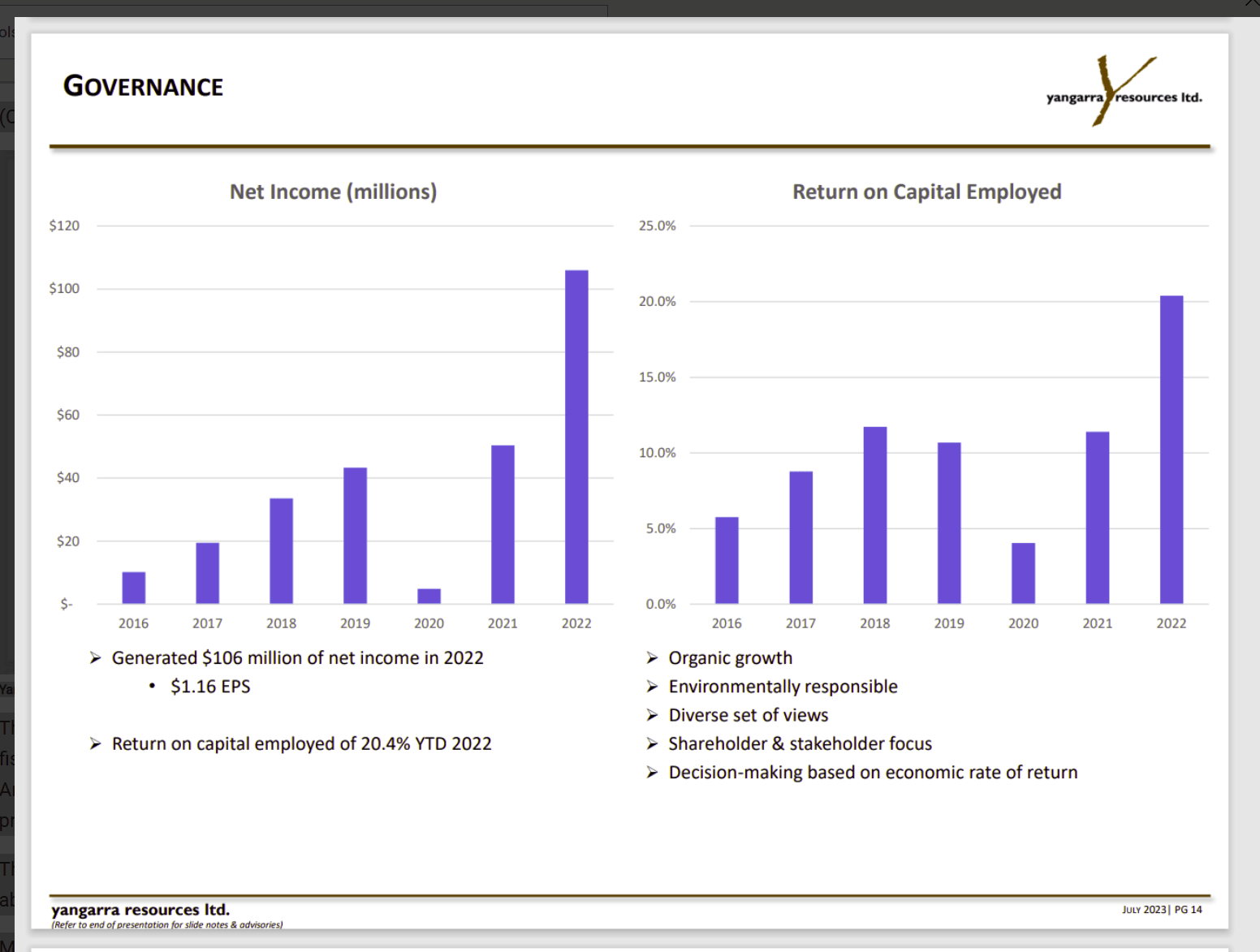

Yangarra Resources Profitability History (Yangarra Resources Corporate Presentation July 2023)

{kind=link}

The company is already very profitable compared to many in the industry. That profit reported in fiscal year 2021 is in sharp contrast to a lot of large losses posted throughout the industry. Anything that approached breakeven was a major accomplishment in fiscal year 2021 (let alone a profit).

This fiscal year, the market is concerned about losses due to the severe winter followed by the wildfires. Yet this company has been so profitable that it made a little money in 2021. The challenges, this fiscal year, daunting as they were, are nothing like what happened in fiscal year 2020.

Furthermore, once the challenges of fiscal year 2020 are over, the future is unlikely to have something like that again, as the combination was a rare occurrence. But the market has treated this like a perennially ongoing disaster. That should make this a good contrarian opportunity. It has always been a strong buy. But now it is a darn cheap strong buy at a very likely one to two times next year's earnings and probably less than two times cash flow. Yangarra Resources Ltd. may be the cheapest company that I follow.

This is also backed up by the "Return On Capital Employed" shown next. Those numbers are far above average.

Most likely, investors need to be patient with a company like this and just wait until it attracts the size that brings more attention and a better valuation. Sometimes with small companies, it can be excruciating to wait for that day.

But the management has built and sold companies before. That reduces the small company risk considerably, the conservative balance sheet likewise reduces the small company financial risk. There are quite a few larger upstream companies that will be riskier than this one.

Probably the biggest risk for this investment is the loss of a key officer combined with an insufficient replacement. But even the board has considerable industry experience. So, there is a lot here that has been done to reduce that small company investment risk.

The above-average profitability of Yangarra Resources Ltd. is most likely due to the leases chosen. That will likely lead to a long-term profitability advantage. Eventually, that should lead to a premium valuation.

Management does own a significant amount of shares outstanding. Therefore, management is motivated to continue growing the company until this company receives a better valuation.

Key Takeaways

The market appears to be focused on some environmental challenges that will pass. That alone could lead to a better valuation than is the case now.

Long term, this company needs to grow in size to attract more institutional attention. That will take some investment and patience to achieve. But management can grow the company while reducing debt.

The major long-term story would be to build a company that can be sold for a good price. The market generally likes that story every bit as much as the current emphasis on balance sheet repair while return capital to shareholders.

There are managements that have gone overboard on returning capital to shareholders to the point that production is not growing. This is likely to be met by the market with lower valuations in the future. It would be very shortsighted to cater to Mr. Market's current demands without considering Mr. Market's future demands.

Yangarra Resources Ltd. is offering general guidance to probably a base dividend in the future. But a strong balance sheet and production growth are likely to remain a priority for the foreseeable future. Income shareholders can look elsewhere. However, the relatively conservative strategy chosen by management will appeal to those looking for an upstream company with relatively low upstream risk.

For further details see:

Yangarra Resources: Back To Normal