REI - Yangarra Resources: Forget Downside Risk And Jump In

2023-03-27 11:22:59 ET

Summary

- The Yangarra Resources Ltd. Price-Earnings ratio as of the beginning of March is about 2.

- The debt balance was reduced by about one-third.

- Yangarra Resources reported positive earnings in fiscal year 2020.

- Yangarra Resources is a rare company that can grow production while reducing debt at the same time.

- The net income is a high percentage of revenue, which points to a low cost structure and a low breakeven point.

(Note: This article was in the newsletter on March 2, 2023. This is a Canadian company reporting in Canadian dollars unless otherwise noted.)

Yangarra Resources Ltd. ( OTCPK:YGRAF ) recently reported its year-end numbers to bring its price-earnings ratio to about 2 at the beginning of March 2023. Management also noted that the company reduced its debt by about one-third and aims to pay down a similar chunk in the coming fiscal year. Meanwhile, the company is profitable enough to grow production while repaying debt. That unusual accomplishment will reduce the debt ratio from two directions (and faster, too). A company that is that profitable with that low a price-earnings ratio has a very low long-term downside risk. In fact, the risk is likely forgettable unless you, the investor, predict a disaster ahead.

Management further issued nearly 6 million special common shares that allow Canadian investors to deduct the development expenses incurred (rather than the company) with the money raised. Management expects to be in a position later in the fiscal year to guide to a production increase. That further cement the idea of both significant debt reduction and production growth. It would appear that leverage ratios will significantly improve yet again (and they were already pretty good).

This is a company that marginally reported a profit in the pandemic and right after while much of the industry reported "losing their shirts." There has not been a losing year since the company began drilling to develop the leases (as opposed to drilling for testing purposes). In addition to the debt paydown, the growth ahead maximizes the upside potential while minimizing whatever downside potential is left. When the price-earnings ratio heads to about two, then Mr. Market sees nothing but catastrophe ahead. This management has navigated some impressive challenges so far. One would think that would impress the market.

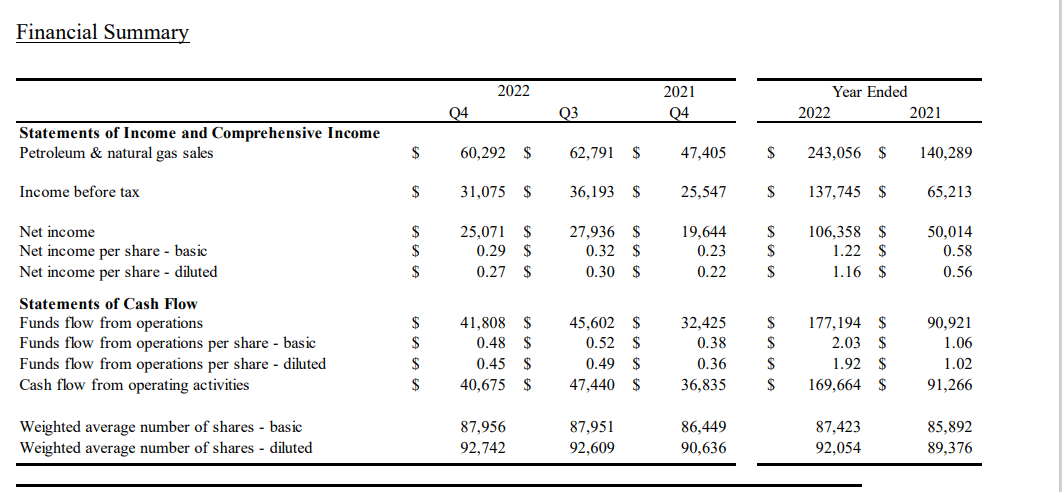

Financial Summary

Earnings took a big jump in the current fiscal year. But if the company can barely pass breakeven in a challenging year like fiscal year 2020, then the future is very likely to be a comparative cakewalk.

(Canadian Dollars Unless Otherwise Noted.)

Yangarra Resources Annual Financial Summary (Yangarra Resources Fourth Quarter 2022, Earnings Summary Press Release)

{kind=link}

As a result of the earnings in fiscal year 2021, the price-earnings ratio was already low to begin with. Then the stock price made little to no progress to bring the price-earnings ratio even lower. The larger funds flow also made for a very conservative enterprise value-to-funds flow ratio.

Back in fiscal year 2020, this company earned C$.06 per share. One would think that alone would get this little company some respect. So far, no dice. But the continuing growth and profitability are likely to attract attention at some point in the future. The market is always on the lookout for little gems like this. The steady growth ensures a notice at some point.

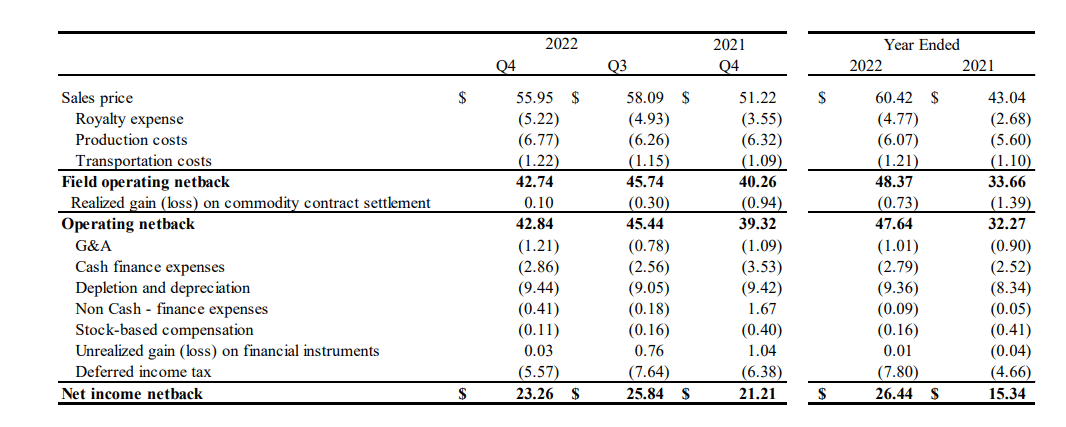

High Net Income Netback

This company is profitable enough to show investors the cost per barrel all the way to net income (rather than stopping with field netback or something close to that).

Yangarra Resources Cost Per Barrel Breakdown To Net Income (Yangarra Resources Fourth Quarter 2022, Earnings Press Release)

{kind=link}

The costs to the field operating netback are far more typical of a natural gas producer than an oil producer. This company does produce a fair amount of natural gas. But there are enough liquids in the production mix to make this production extremely profitable.

After that come the controllable costs. Now this management was far more lucky than some other managements I follow like Ring Energy, Inc. ( REI ) in that it had more cash flow in the process of converting to an operating model when the pandemic challenges hit. Therefore, when commodity prices soared after the pandemic, this company was able to repay a fair amount of debt on its own without resorting to digging itself out of a debt hole by way of a series of acquisitions. That is another very unusual accomplishment that points to the unusual profitability of this company and the wells drilled.

A side observation would be that in both fiscal years, net income is an unusually high percentage of revenues. This obviously points to a very low corporate breakeven that enabled the small profit in fiscal year 2020.

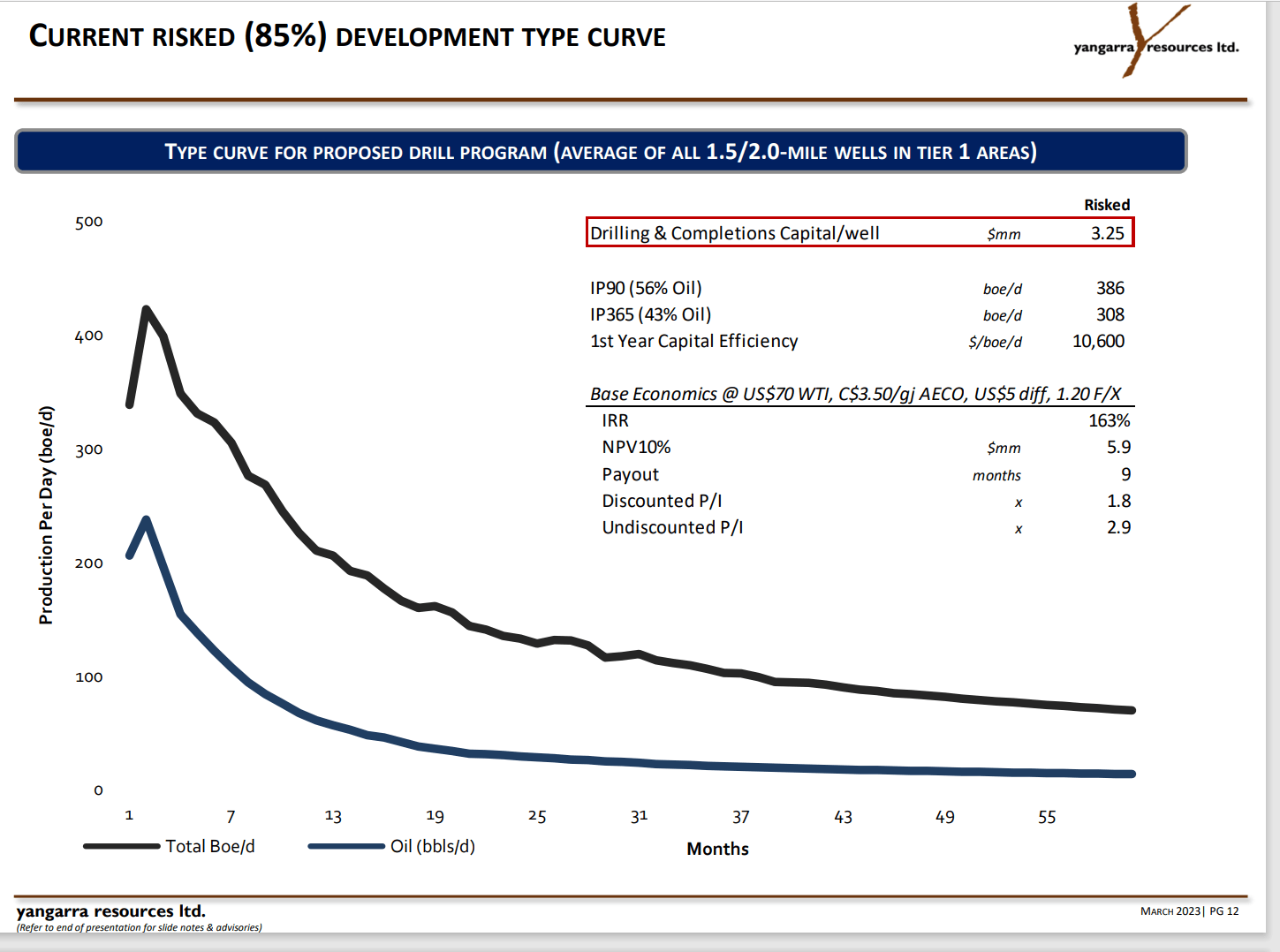

Well Performance

These wells pay back very fast in comparison to much of the industry.

Yangarra Resources Well Performance Summary (Yangarra Resources March 2023, Corporate Presentation)

{kind=link}

(Note: The company presentation is down for the time being. This is most likely due to the recent share issuance.)

As shown above, the wells pay out in less than one year. That is considered excellent by industry standards. The other thing to note about these wells is the lower decline rate of production. So, cash flow is relatively robust in the first few years compared to the more typical unconventional decline rate many investors are used to.

That is a huge aid to keeping maintenance capital relatively low. The hurdle for some decent growth is also respectively lower as well. Management reports a very healthy backlog of future drilling possibilities that exceeds two decades.

Many of the Canadian fields have several intervals that could provide some speculative (currently) upside potential in future years.

Going Forward

Management had already reported that production for the fiscal year just ended increased by more than 20%. Management is also guiding to a slower production increase in the current fiscal year.

Canadian companies have an advantage over United States companies in that a lot of activities have to stop during the Spring Breakup. This gives management a period of time to reassess substantial parts of the second half capital expenditure during a period that has typically lower activity levels.

Of course, activity will re-activate towards the end of the second quarter or the beginning of the third quarter. That means most of the production growth happens typically in the first and fourth quarters. Weaker earnings comparisons in the second and third quarters can be very much influenced by the weather rather than operational conditions that investors generally expect in other geographic areas (or even other industries).

The debt ratio is already in what many would consider conservative territory. The debt ratio never "exploded" in fiscal year 2020 as was the case elsewhere. However, management is still going to lower debt levels so that the debt levels remain comfortable to management in any future downturn.

The risk of downside here is offset by management (and board of directors) experience in building and selling companies. That experience showed itself when the company was profitable in fiscal year 2020 along with the debt ratio remaining under 3 all of that fiscal year. The low debt levels combined with the ability to grow the business while repaying debt also help to protect against downside loss of investment principal long-term.

Yangarra Resources Ltd. is a typical small company stock that can be very volatile due to the small number of shares outstanding. But overall, the company appears to be far safer than many larger upstream companies. The profitability shown here by Yangarra Resources Ltd. is typical of much larger (more integrated) and financially much stronger rated companies.

For further details see:

Yangarra Resources: Forget Downside Risk And Jump In