YGRAF - Yangarra Resources: Too Cheap To Ignore

2023-04-04 11:36:48 ET

Summary

- Yangarra Resources is a Canadian small-cap producer of gas and light oil. However, the market appears to have misconstrued the company's acreage, operations, and business strategy.

- In this article, I analyze Yangarra Resources' assets and growth trajectory, with the aim of shedding light on its risk-reward profile.

- After conducting my analysis, I have come to believe that Yangarra represents an exceptional deep-value investment opportunity in the Canadian E&P space at this time.

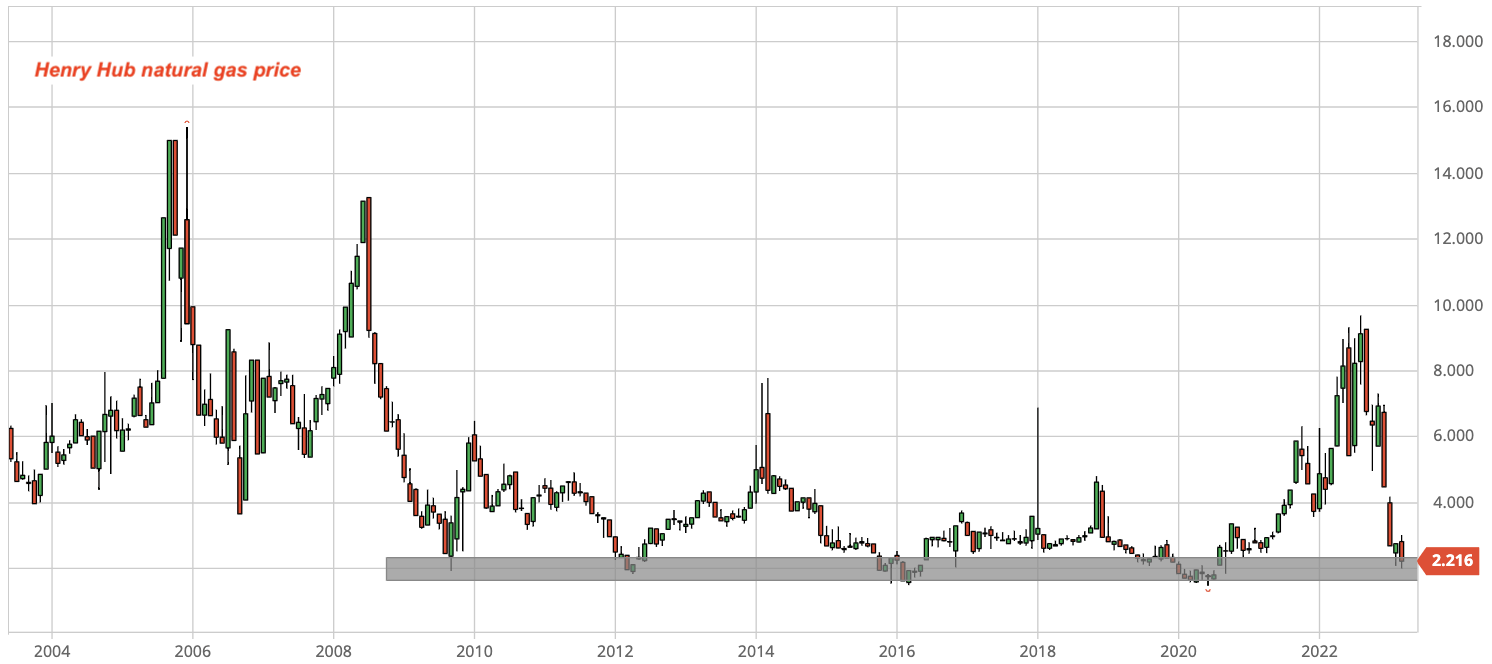

Recently, the U.S. natural gas price benchmark Henry Hub and Canadian benchmark AECO have both reached historic lows. This can be attributed primarily to the warm winter weather in North America, which has reduced demand for natural gas, and delays in restarting the Freeport LNG terminal. As illustrated in Figure 1, these factors have contributed to a significant drop in natural gas prices in both markets.

Fig. 1. Historical prices of Henry Hub natural gas with support level since the shale gas revolution (modified after Barchart and Seeking Alpha)

{kind=link}

Given the recent decline in natural gas prices, some investors may be considering contrarian opportunities in the market. In this context, we will take a closer look at Yangarra Resources Ltd. ( YGRAF ), a small-cap Canadian natural gas producer that may warrant attention.

An overview of Yangarra

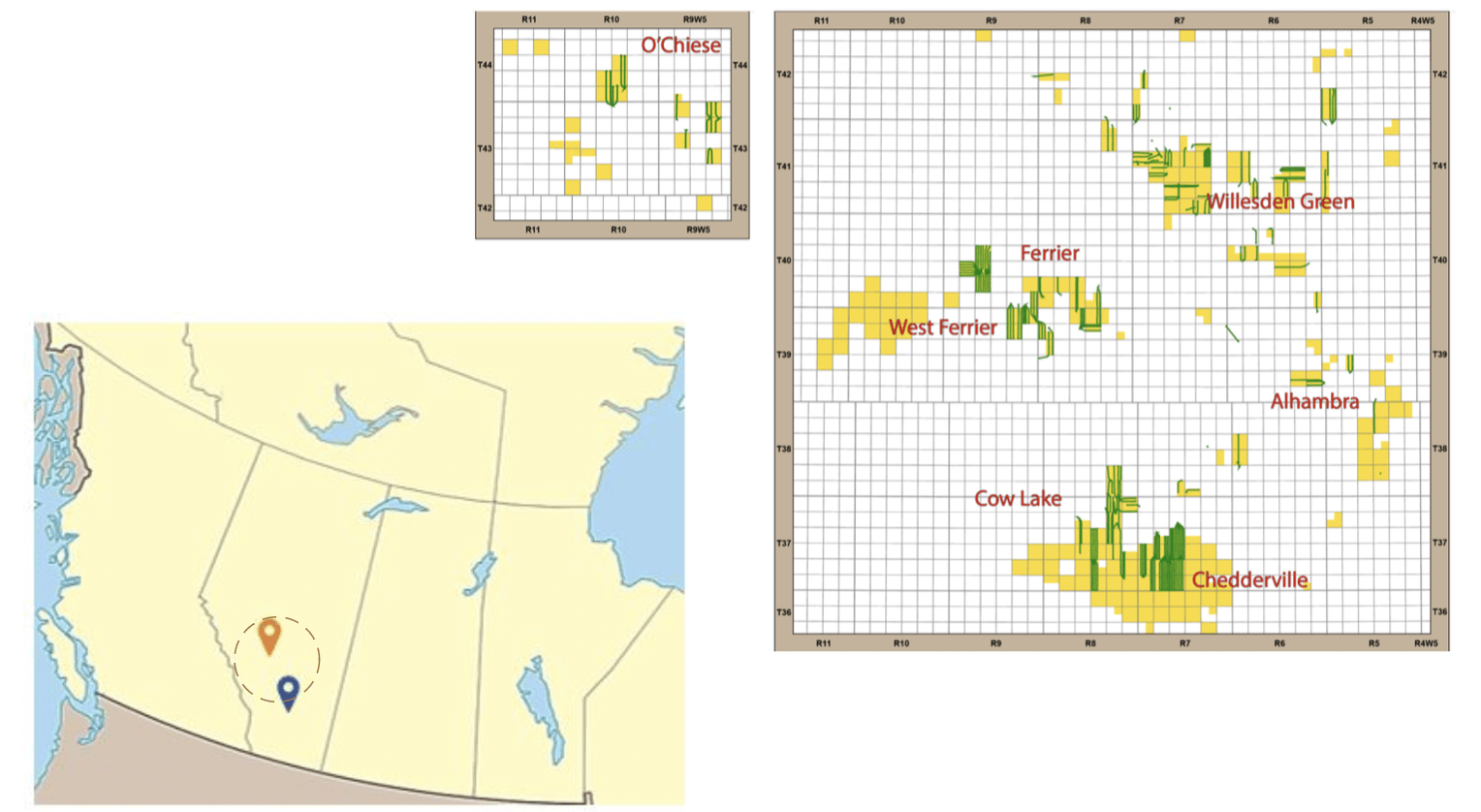

Yangarra owns 118,080 acres located in central Alberta, where the company targets the halo Cardium play at various sites including Ferrier, Chedderville, Cow Lake, Chambers, O’Chiese, and Willesden Green. These locations are located around the town of Rocky Mountain House, as illustrated in Figure 2.

Fig. 2. Land holdings of Yangarra Resources in central Alberta, Canada, targeting the halo Cardium play (modified by Laurentian Research for The Natural Resources Hub based on Yangarra Resources materials)

{kind=link}

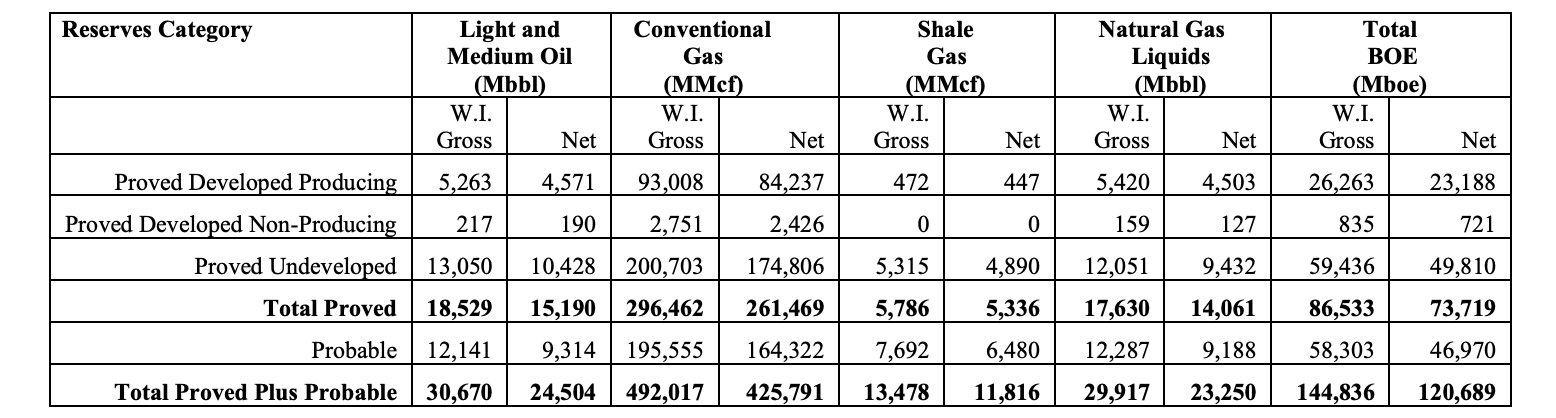

In 2016, Yangarra Resources made a discovery that fracking in the bioturbated zone leads to the extraction of a substantially greater amount of oil and gas than targeting the upper Cardium. This is attributed to the gas-charge that drives higher oil and NGLs recoveries. As a result of this finding, Yangarra accumulated halo Cardium acreage and experienced rapid growth in both reserves and production. As of the end of 2022, Yangarra's net proved and probable reserves total 120.69 MMboe , comprising approximately 60% natural gas and 40% liquid hydrocarbons, as summarized in Table 1.

Table 1. Oil and gas reserves of Yangarra Resources as of December 31, 2022. Please note, net reserves are Yangarra's working interest share after deduction of royalty obligations and any royalty interests. PDP, proved developed producing; 1P, proved; 2P, proved and probable (Yangarra Resources)

{kind=link}

In 2022, Yangarra produced at an average rate of 11,022 boe/d from approximately 216 wells, with 45% of the production being in liquids.

In order to overcome the challenge of accessing infrastructure and oilfield services, which may not always be readily available to small-cap operators, Yangarra made strategic investments in infrastructure and established an in-house oilfield service team, particularly between 2018 and 2019. This has enabled the company to achieve exceptional operational resilience , even in an inflationary environment, which is not commonly observed among small producers. Moreover, this has helped Yangarra secure high margins by realizing higher commodity prices and lowering operating costs.

Growth

Between 2016 and 2022, Yangarra Resources took strategic steps to position itself for production growth and financial stability. The company delineated the bioturbated Cardium play and expanded its acreage, while also building out its gathering and compression infrastructure, and fluid hauling capabilities. In 2020 and 2021, Yangarra further strengthened its in-house oilfield servicing group by adding earth moving, road maintenance, and rig hauling equipment. In 2022, the company executed a disciplined drilling program, using a single rig to drill 30 wells and generate significant free cash flow while reducing debt. With a healthy balance sheet on the horizon, Yangarra is poised to initiate shareholder reward initiatives.

Reserves

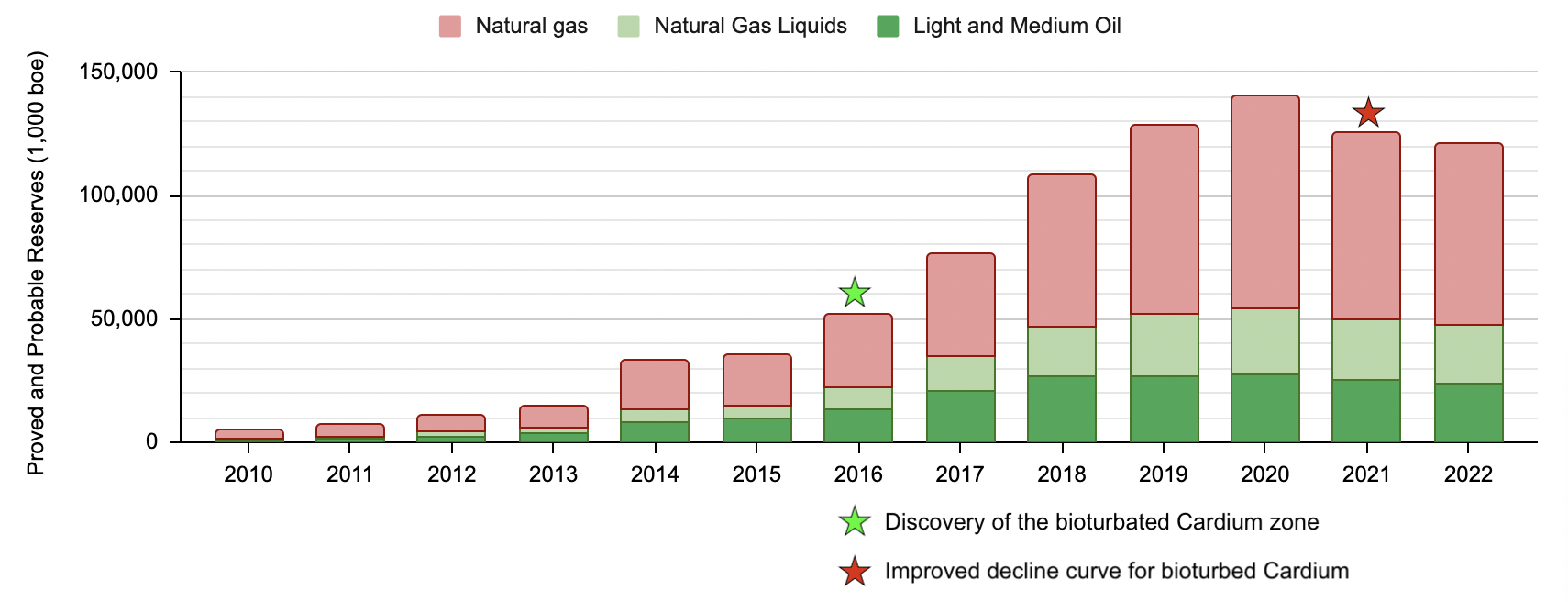

Yangarra has spent the last six years learning about the bioturbated Cardium formation. Initially, decline curves were determined without the benefit of production history as this was a newly discovered resource. However, armed with a better understanding of production history and updated decline curves, Yangarra made technical revisions in 2021 .

Between 2015 and 2022, Yangarra increased net proved and probable reserves by 242% (Figure 3). As of 4Q2022, the gross proved developed producing (or PDP) reserve life is estimated to be 6.1 years, while the proved (1P) reserve life is projected to be 20.2 years, and the proved and probable (2P) reserve life is expected to be 33.9 years.

Yangarra's reported 5-year average finding and development (F&D) costs as of 2022 were C$15.69/boe for PDP reserves, C$10.79/boe for 1P reserves, and C$7.60/boe for 2P reserves.

Fig. 3. Net proved and probable reserves of Yangarra Resources by hydrocarbon types, shown with major events in the company's history of reserve booking (compiled by Laurentian Research for The Natural Resources Hub based on Yangarra Resources released data)

{kind=link}

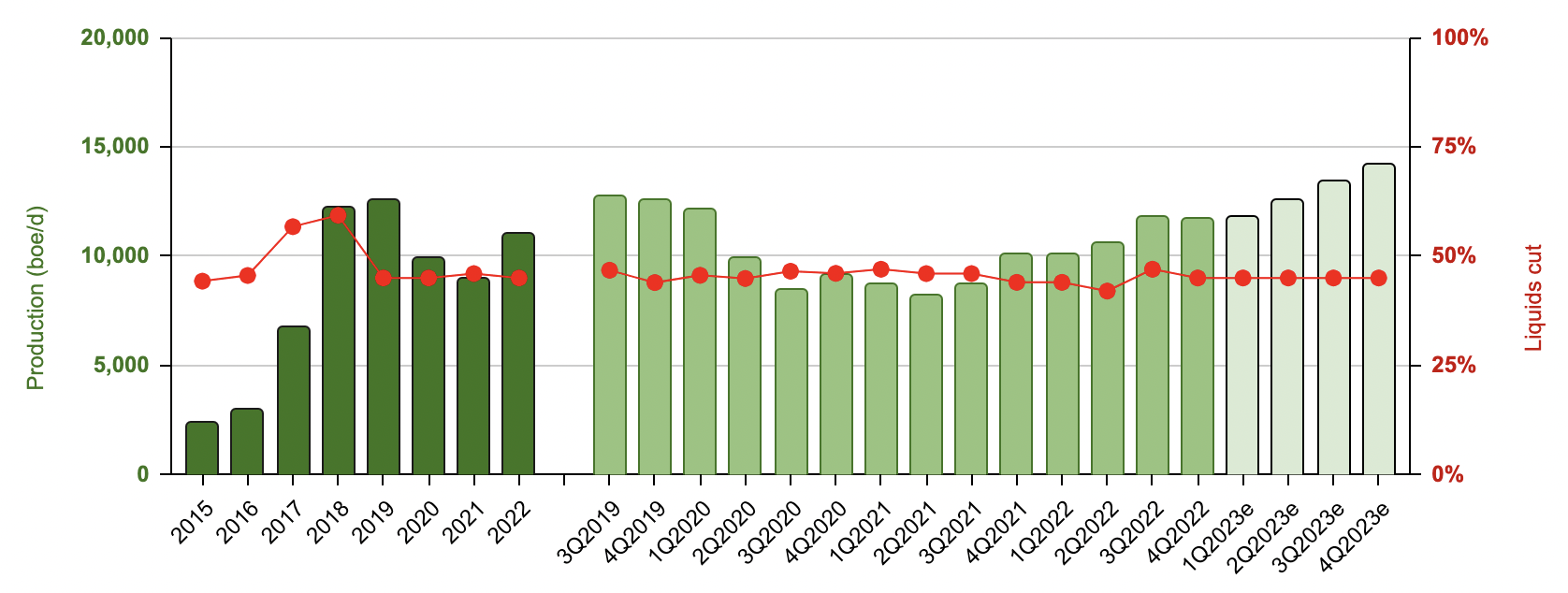

Production

Yangarra experienced a significant increase in production between 2017-2019 by developing bioturbated Cardium, as shown in Figure 4. Production declined in 2020 and 2021 due to capital discipline in response to the Covid-19 pandemic. In 2022, Yangarra increased average production by 23% over the previous year by drilling 32 wells running one drilling rig throughout the year.

In 2023, Yangarra plans to keep one drilling rig fully utilized with a C$125 million capital budget, aiming to achieve an all-time high average production of 13,000 boe/d.

Fig. 4. Production profile of Yangarra Resources, by year and by quarter, actual and projected, shown with liquids cut (compiled by Laurentian Research for The Natural Resources Hub based on Yangarra Resources released data)

{kind=link}

Financials

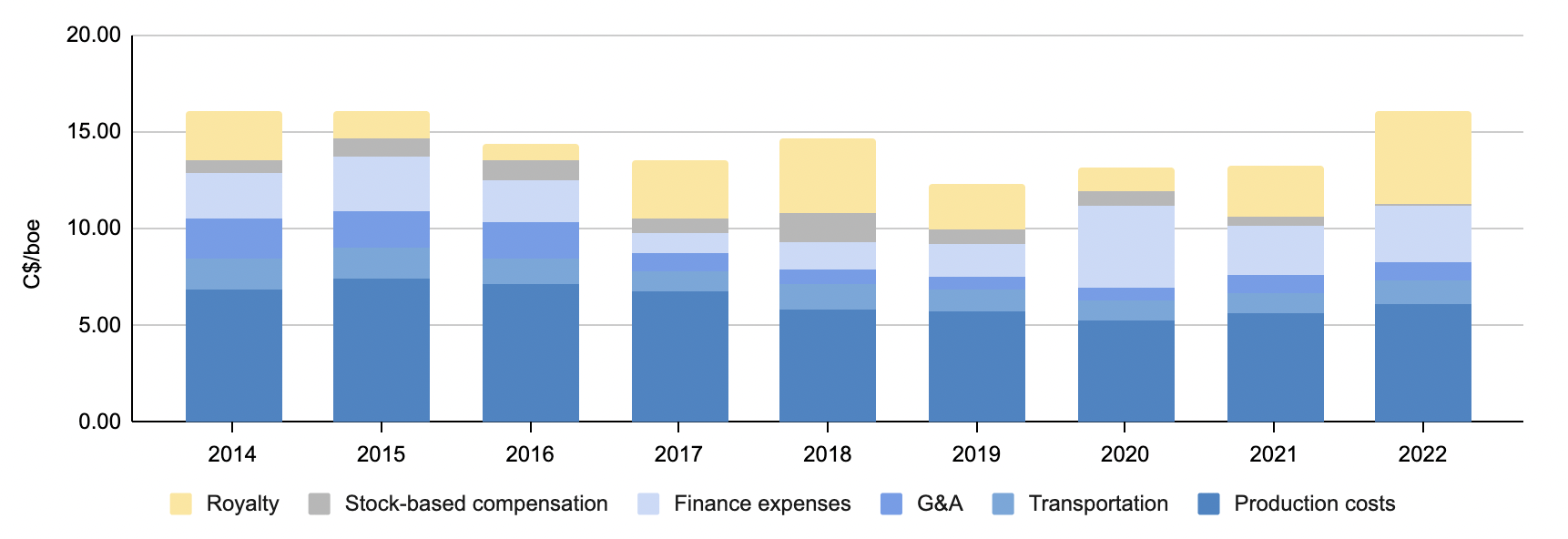

The discovery of the bioturbated Cardium play allowed Yangarra to take advantage of economies of scale and reduce operating costs. Investments in gathering infrastructure and owning a tanker truck fleet minimized operating costs. From 2015 to 2020, operating costs decreased by 30% (Figure 5). Although operating costs increased by 15% in 2021 and 2022, Yangarra's vertical integration strategy by establishing in-house oilfield services provided a hedge against inflationary pricing in oilfield services. As of Q4 2022, the company maintained its operating costs at C$7-8/boe .

Fig. 5. Unit cash costs of Yangarra Resources (compiled by Laurentian Research for The Natural Resources Hub based on Yangarra Resources released data)

{kind=link}

Yangarra captures a C$3-4/boe oil price premium over neighboring operators by blending oil at its truck terminals. With low costs and advantageous commodity price realization, Yangarra achieved an operating netback of C$42.84/boe, an operating margin of 77%, and a funds flow from operations margin of 69%.

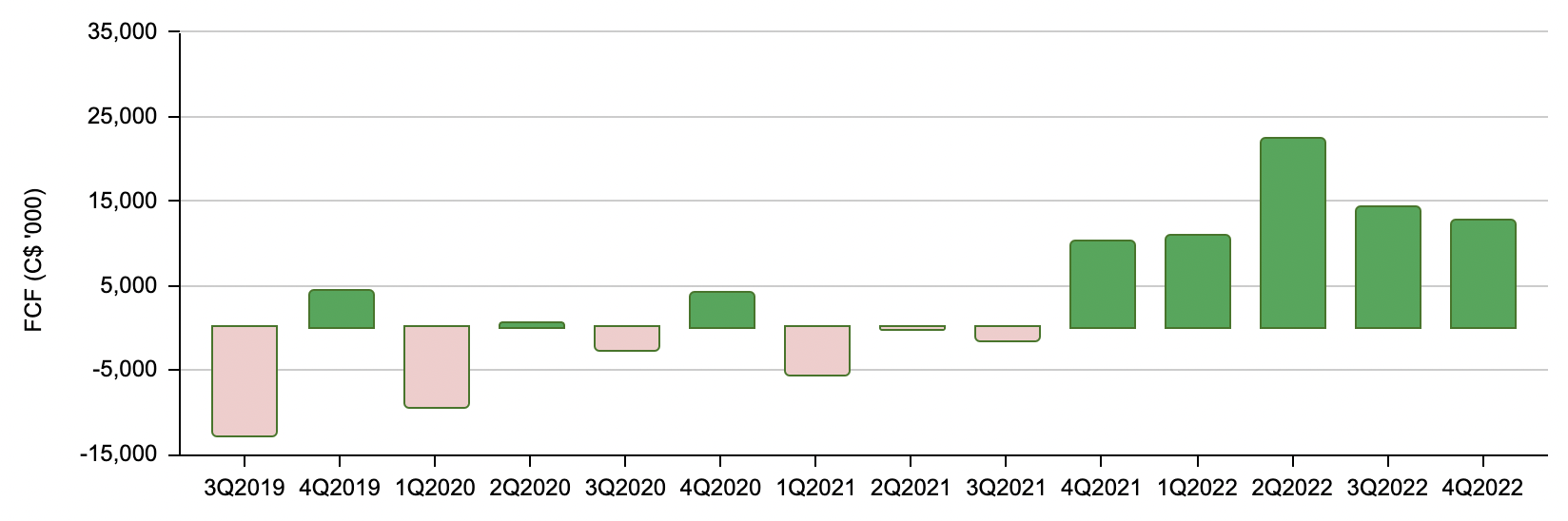

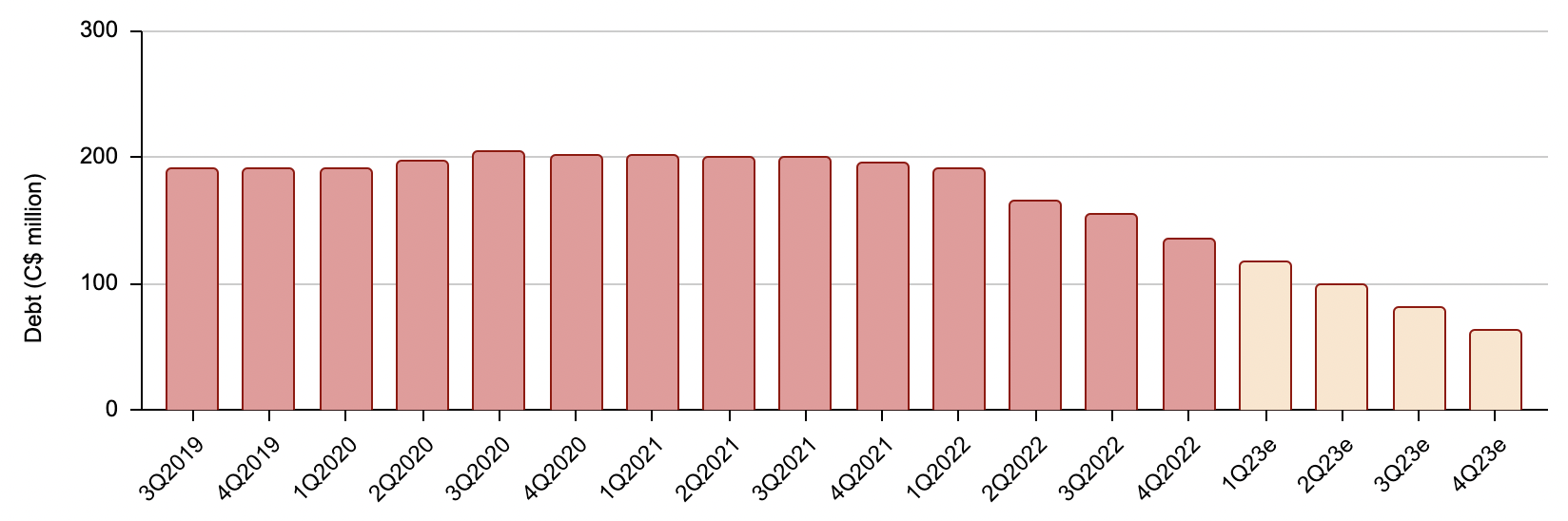

Yangarra has achieved five consecutive quarters of free cash flow, as shown in Figure 6. The company used this cash flow to pay down debt, reducing adjusted net debt by $62.4 million in 2022 compared to the previous year. It is expected to exit 2023 with a debt of C$63 million and an extremely healthy balance sheet (Figure 7). On March 27, 2023, Yangarra raised C$17.25 million of flow-through capital through an equity financing round, further strengthening its capital liquidity.

Fig. 6. Free cash flow of Yangarra Resources by quarter (compiled by Laurentian Research for The Natural Resources Hub based on Yangarra Resources released data) Fig. 7. Debt owed by Yangarra Resources at end of quarter (compiled by Laurentian Research for The Natural Resources Hub based on Yangarra Resources released data)

{kind=link}

{kind=link}

Valuation and risks

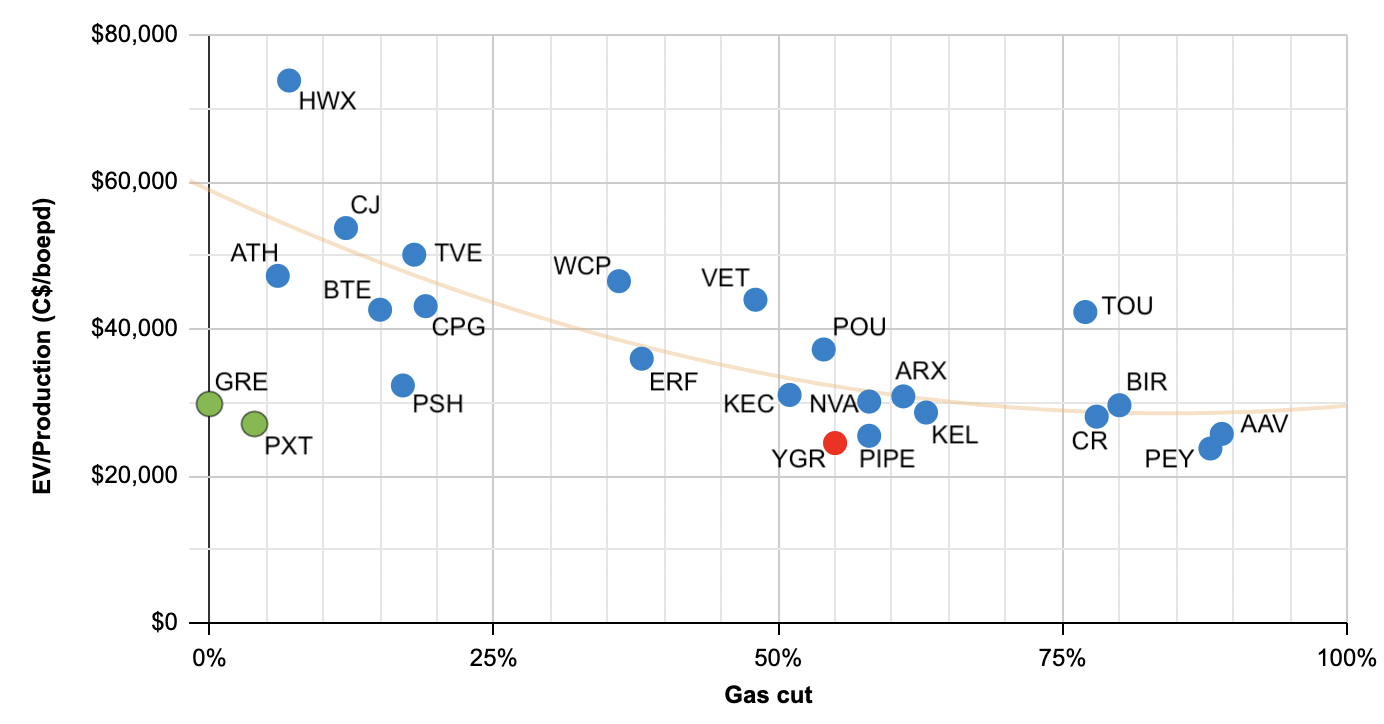

I believe Yangarra Resources is one of the most deeply undervalued stocks in the Canadian E&P space based on various valuation metrics. Firstly, it is cheaper than the net asset value of its reserves, with a P/NAV of 0.60X for proved developed producing reserves, a P/NAV of 0.20X for proved reserves or a P/NAV of 0.14X for proved and probable reserves, which is rare among producers. Secondly, Yangarra is one of the cheapest among Canadian E&P stocks in terms of EV/Production, as shown in Figure 8. Thirdly, it trades at a forward P/FCF multiple as low as 3.6X.

Fig. 8. EV/Production vs. gas cut variations for Canadian E&P companies, shown with a trendline. Two operators in Colombia (GRE and PXT) are excluded from the calculation of the trendline (compiled by Laurentian Research for The Natural Resources Hub based on data released by various companies and retrieved from Seeking Alpha)

{kind=link}

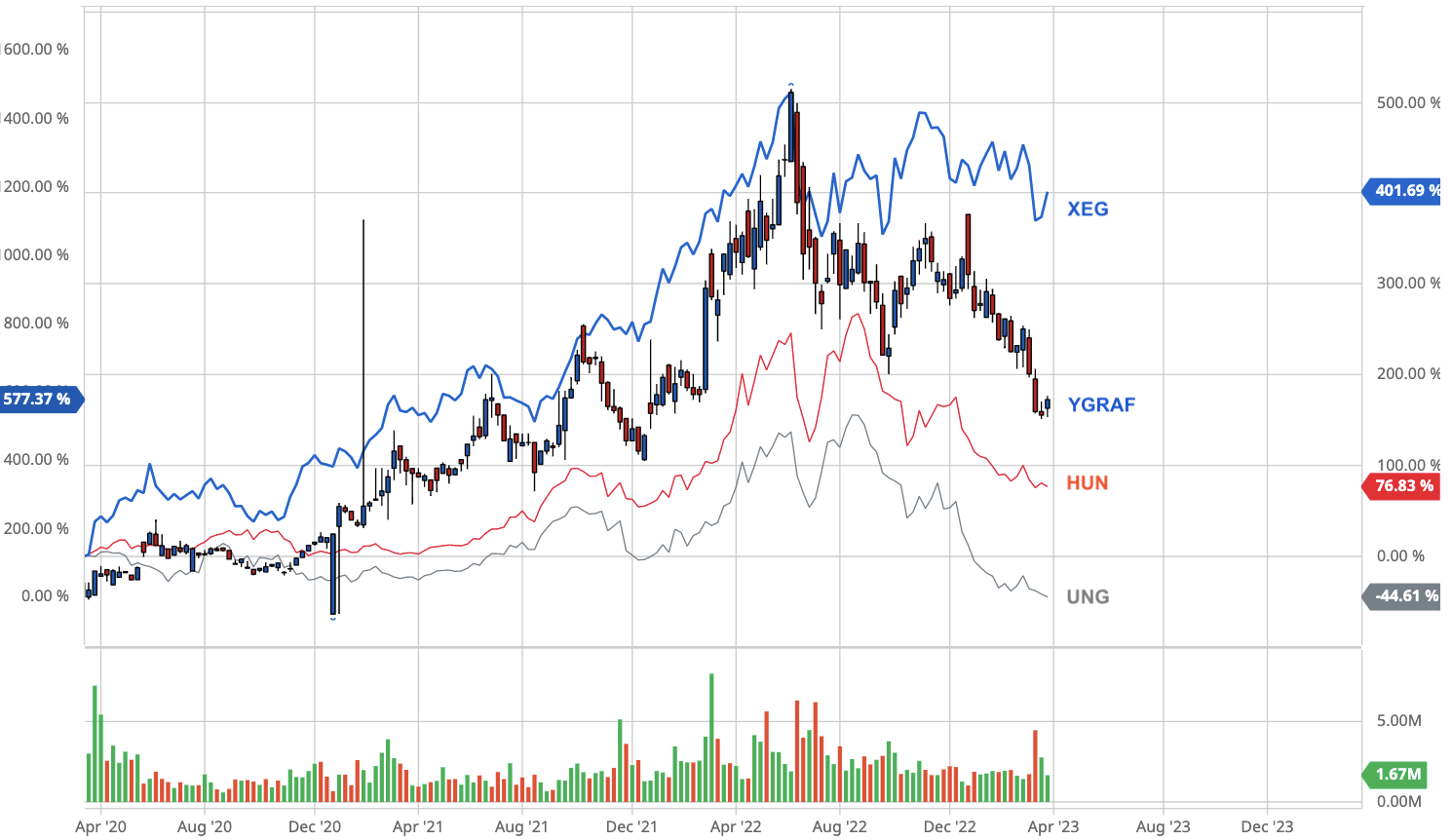

The recent decline in Yangarra's stock price is likely due to the weakness in natural gas prices (Figure 9), but there may also be misunderstandings regarding its assets and operations. The market may still be cautious following the 2021 reserve revision (Figure 3), even though the improved knowledge of the bioturbated Cardium play means that the risk of further revisions is relatively low. Additionally, some investors may be hesitant to invest in small-cap producers due to the perception of higher operational risks, as discussed in a previous article . Finally, some investors may not fully understand the rationale behind the decision of Yangarra's management, led by CEO Jim Evaskevich, to vertically integrate into oilfield services, which has provided the company with a competitive edge in managing costs and services.

Fig. 9. Stock chart of Yangarra Resources, as compared with Horizons Natural Gas ETF (HUN), The United States Natural Gas ETF (UNG), and iShares S&P/TSX Capped Energy Index ETF (XEG) (modified from Barchart and Seeking Alpha)

{kind=link}

The insider ownership of Yangarra Resources is significant, with insiders owning 16% of basic shares or 22% on a fully-diluted basis. This level of ownership aligns the interests of management with those of shareholders and provides an incentive for them to deliver positive outcomes.

Investor takeaways

Overall, Yangarra Resources represents an exceptional deep-value investment opportunity in the Canadian E&P space. Despite its abundant reserves, low-cost operations, high margins, and growth prospects, the market undervalues the company in my view.

Although I have held a significant position in Yangarra Resources since March 2020, I could not resist the opportunity to buy more shares when its proved developed producing reserves were offered to me at a 40% discount, with a FCF yield of 27.5%, 23% production growth, and a balance sheet that is rapidly being de-risked.

As a result, I plan to take advantage of any dips in the stock price and add to my position between C$1.83 and C$1.60, particularly as the stock approaches its 200-day moving average, as shown in Figure 10.

Fig. 10. Stock chart of Yangarra Resources, shown with its 200 DMA (modified from Barchart and Seeking Alpha)

For further details see:

Yangarra Resources: Too Cheap To Ignore