YARIY - Yara: The 400 NOK Level Is A Solid BUY After Q2 2023

2023-09-02 03:50:44 ET

Summary

- Yara International is a long-term investment with positive trends in the fertilizer sector.

- 2Q23 saw falling prices in the fertilizer field, but Yara managed strong cash generation and improved demand.

- Yara's financial performance is not comparable to last year's strong periods, but the company remains stable and well-positioned for long-term profitability.

Dear readers/followers,

Yara International ( OTCPK:YARIY ) ( OTCPK:YRAIF ) is a company I've been writing about for some time - years at this point. It's a successful investment, up well above single and even double digits if we include dividends. I am a long-term holder of this company, and believe in the long-term positive trends of this sector, and of Yara which I consider to be sector-leading.

Since my last article in June, we have the latest quarterly report, which I believe cements the thesis that below or around the 400 NOK native mark, this company makes for a very good investment.

I wouldn't touch my position for a sale unless the price was above the 500 Mark, or at the very least had a "5" as the first number. That's not something we see at this time, but that's where I would be looking at the company with the intention of trimming my position.

Let's look at 2Q23 ( Source ) and see what we have going for us here.

Yara International - Plenty to like, the upside is still very much present

Last time, I considered the company a "BUY" after the 55 NOK ex-dividend drop, which put the company well below 400 NOK/share. Because I believe Yara has the ability to continue paying an attractive dividend even on the assumption of somewhat reduced income. We need to remember that part of the reason why the company has been yielding so much is a significant amount of extraordinary payouts for the past few years.

I remain very convinced with Yara. It happens to be one of the largest overall positions in my entire portfolio, accounting for both commercial and private investment portfolios. My stake here, over 4%, is fully representative of my conviction in the company's long-term viability, which in this case is for continued profitability and solid results.

That doesn't mean you shouldn't expect volatility. But whenever you look at a business, and that business drops, the question you should ask yourself and try to decipher is what the reason for the drop is. Usually, that reason isn't as serious or grounded as you might believe.

Anyway, 2Q23.

I have been expecting for some time to see falling prices in the fertilizer field. Those prices have now been falling, and 2Q23 is the first quarter where we see a real massive impact here. Still, Yara has continued to manage very strong overall cash generation despite those results.

However, I've been following trade publications and trends in the fertilizer field. And premiums as well as overall pricing is likely to see stabilization and some recovery for 3Q23, which means that I don't consider 2Q23 to be the likely start of a significant downward development.

That may come later, or not at all.

Instead, lower prices generated higher volumes on the part of Yara, as well as improved demand. if you recall my last articles, despite Yara's solid earnings, there was a volume drop-off because many could no longer afford Yara's product. This has now changed, and both the tighter market for Nitrogen, as well as falling prices, have resulted in very positive trends.

{kind=link}

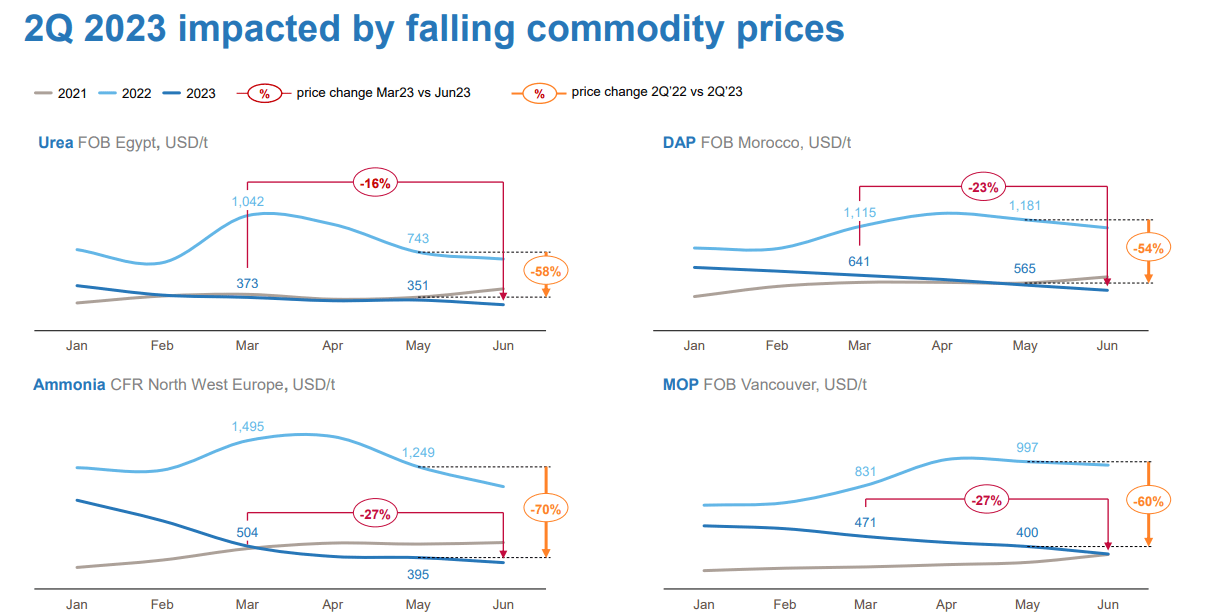

Commodity prices are going down, which means both improvements for Yara, but also different industry dynamics than we've seen over the past year, which has mostly been characterized by very high levels. Take a look at some of these numbers.

{kind=link}

These positive pricing deltas also mean that the company's curtailments in Europe are over. It's now possible again to produce profitably in Europe. Yara is now up to 90% in Operation, with only 10% curtailed, compared to 30% curtailment as of the 1Q23 period - so a 20% variance in as little as 3 months (Source: Yara Earnings Call 2Q23)

The company's financial performance naturally isn't comparable to the extremely strong periods of last year. We have EBITDA positive, and good operating cash flows, but ROIC is down to 10.5% and EPS is actually negative due to margin. This goes some way to explain the momentary share price pressure Yara is currently experiencing - by which I mean the share price, not product prices.

Segment results were weak. Only the Americas really came in well - but ROIC was solid in most areas, except in Europe which was hit hard by the aforementioned margin and macro trends. Still, in Europe, we saw a strong recovery in volume - and what's more important is the quality of those sales.

And the quality of those sales here, those are very impressive. We're seeing an increased percentage of premium products in the mix, with significant premium growth above all in Europe (79% from 71%) and Total crop overall (57% from 50%). However, the positives in deliveries in Europe were offset by delivery shortfalls elsewhere. This is the reason things weren't more positive.

The company continues to apply very strict financial discipline. Improvements are made in operating capital, with operating capital at a 98-day cycle, down from 113 in 2020 but up from 87 in 2022. This was due to inventory days and slower recovery demand - but the company believes itself to be on target to deliver its 2025E target of 92 days.

Nothing about the company's long-term or fundamental targets has changed. The company is well-positioned from a long-term macro perspective. Investing in food production combined with some of the most ESG and climate-friendly products makes perfect sense in this segment. That's why this company is the largest singular position in both of my portfolios and why I don't see that changing until we see at least a 500+ NOK share price for the company.

Likely in the near term?

I do not believe so. The nitrate/NPK premiums and the overall macro situation do not lend themselves well to another "spike" in valuation, due to dividends or sales here. I would say we're more likely to see price stabilization than growth, which also to me translates to EPS stabilization, not growth.

Energy costs are thankfully on the way down again - this was one variable that we could not properly account for when they started spiking towards the end of 3Q21 and reached their apex in 3Q of last year - but we're now down to 2021 levels again, perhaps moving down further.

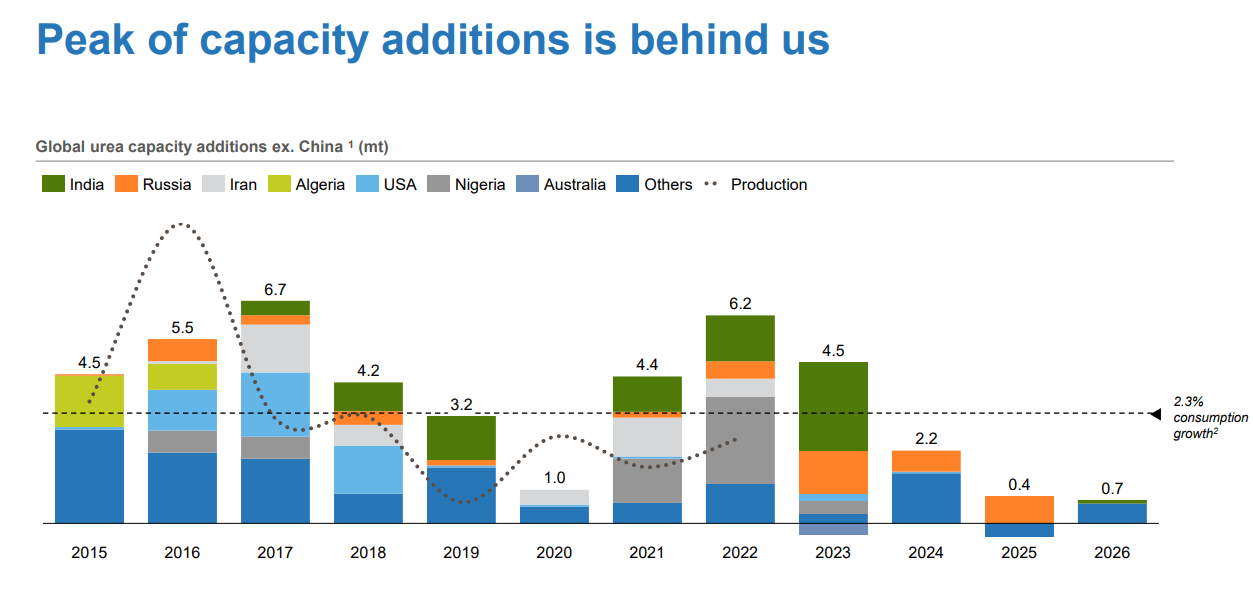

Also, from a global industry CapEx perspective, because it was these investments and additions that were dragging Yara down for a long time, the peak is behind us, and there is very little capacity being added in the near term. With Russia and Belarus curtailed when it comes to fertilizer, this further improves the demand situation here.

{kind=link}

Yara remains a play on premiums and pricing. During 2022, we had some of the highest prices for commodities, but also for fertilizers in history. That naturally translated into high costs, but even better margins and earnings for Yara.

Going forward, I reiterate my case for stabilizing but lower prices, and give you valuation prospects and thesis going into the 2H23 and the 2024 period.

Valuation for Yara Remains compelling, despite not being at trough cheap levels

Yara is one of the better companies I own both from a qualitative, ownership, and from a potential stability perspective, despite its exposure to commodities. Long-term stability for food production-adjacent companies is likely to remain positive - and the company is not expensive here even on the most basic of multiples.

On a P/E level, the company is below 10x here, and on a P/S level, it's below 0.5x. This article came about due to a drop of almost 50 NOK to where the company is below 400 NOK, which from a pure upside perspective, makes it well worth investing in. It's absolutely realistic that we won't see 2022 numbers ever again. Those came in over 100 NOK of GAAP EPS on a per-share basis (Source: S&P Global). But even to a normalized 2024-2025E forecast going up to around 50 NOK per share, yields of 8-10% are still possible here, if the company continues with its dividend tradition.

That combined with the fact that we're seeing very attractive fundamentals and trends for this company's segment, food production, makes this a company worth considering. S&P Global analysts certainly think so. 18 analysts following give it a range from 320 NOK to 520 NOK, with an average of 420 NOK, down from about 503 average about a year back. due to that, 9 analysts out of 18 are still at a "BUY" or equivalent here - though a fair share are also saying "HOLD".

It's the uncertainty about the near-term market. You can see this bounce up, and back down here.

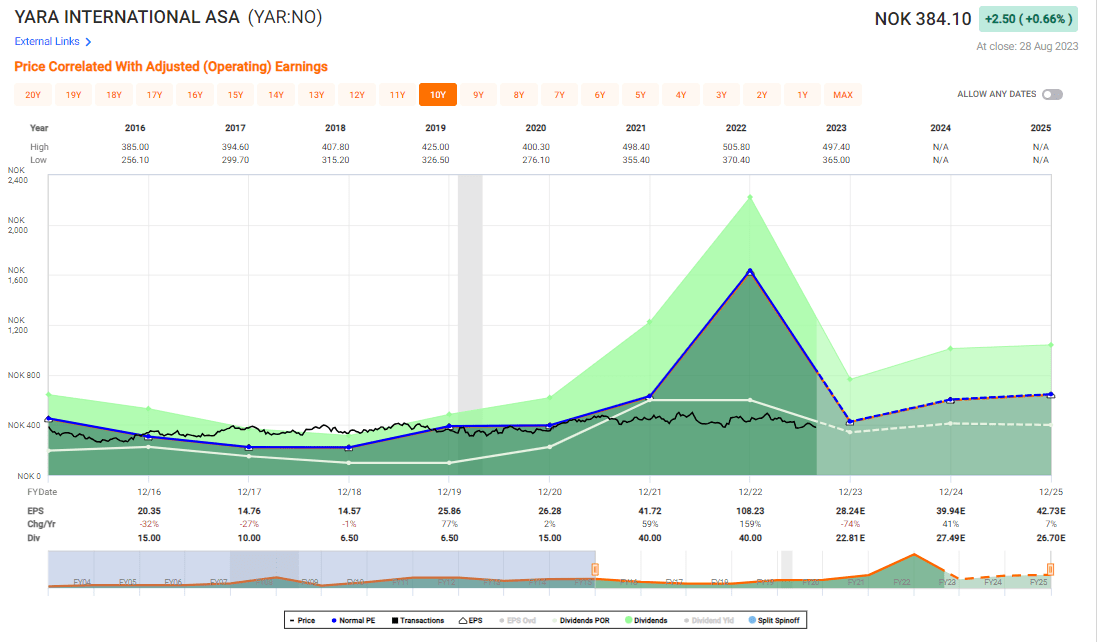

Yara International Valuation (F.A.S.T Graphs)

{kind=link}

You can see that the company almost ignores its own valuation. It doesn't go up when it sees higher earnings, or expects them - but it also doesn't go down when it expects several years of poor earnings. It stays at the 280-480 NOK/share level and doesn't shift much from here.

So even if I say that based on a 15x P/E on a 2025E basis, we should see a 650 NOK price for the company due to the forecast of 44 NOK/share for that year, I say that while the company does beat estimates 30-40% of the time, this does not mean that we see a massive increase in valuation. I don't believe we'll see 650 NOK at that time simply because the company historically doesn't move that much from its typical range no matter the results.

I instead say the upside we can see here is above or around the 15% mark based on a high yield and otherwise excellent operations - and that this is good enough for me to both invest in, if I had less in the company, but also good enough for me to hold onto and continue to enjoy the "fruits" of this investment.

Based on this, I give you my following, updated thesis for the quarter of 2Q23 for Yara International. The big change here is that I now consider the company to be "cheap".

Thesis

- Yara is one of the best/most appealing fertilizer businesses on earth and by far the most attractive with a combination of quality/fundamentals and upside that I see. The company combines legacy appeal with future-proofing, and I see only limited downside at any sort of conservative valuation.

- That is why Yara re mains the biggest single position in my entire portfolio.

- This goes for both my private investment account, as well as my commercial/corporate account where I invest proceeds and profits from my business dealings.

- Yara is a "BUY" here, though every investor, of course, needs to look at their own targets, goals, and strategies. I would also always consult with a finance professional before making investment decisions such as this.

- I give the company a PT of 450 NOK for the common.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I will call Yara cheap for what it offers at levels of about 391 NOK/share. Based on current dividend trends, it calls for a yield of almost 16%. Even normalized and at half this level, which is unlikely to me, that's a very solid yield for a superb company.

For further details see:

Yara: The 400 NOK Level Is A Solid BUY After Q2 2023