AFMC - Yes The Cycle Still Cycles

2023-04-18 03:10:52 ET

Summary

- Traditional leading economic indicators place a heavy focus on data from the construction and manufacturing sectors.

- The shrinking share of the cyclical economy has led many people to question the validity of traditional leading indicators.

- It’s clear that the composition of traditional leading indicators remains appropriate.

Traditional leading economic indicators place a heavy focus on data from the construction and manufacturing sectors.

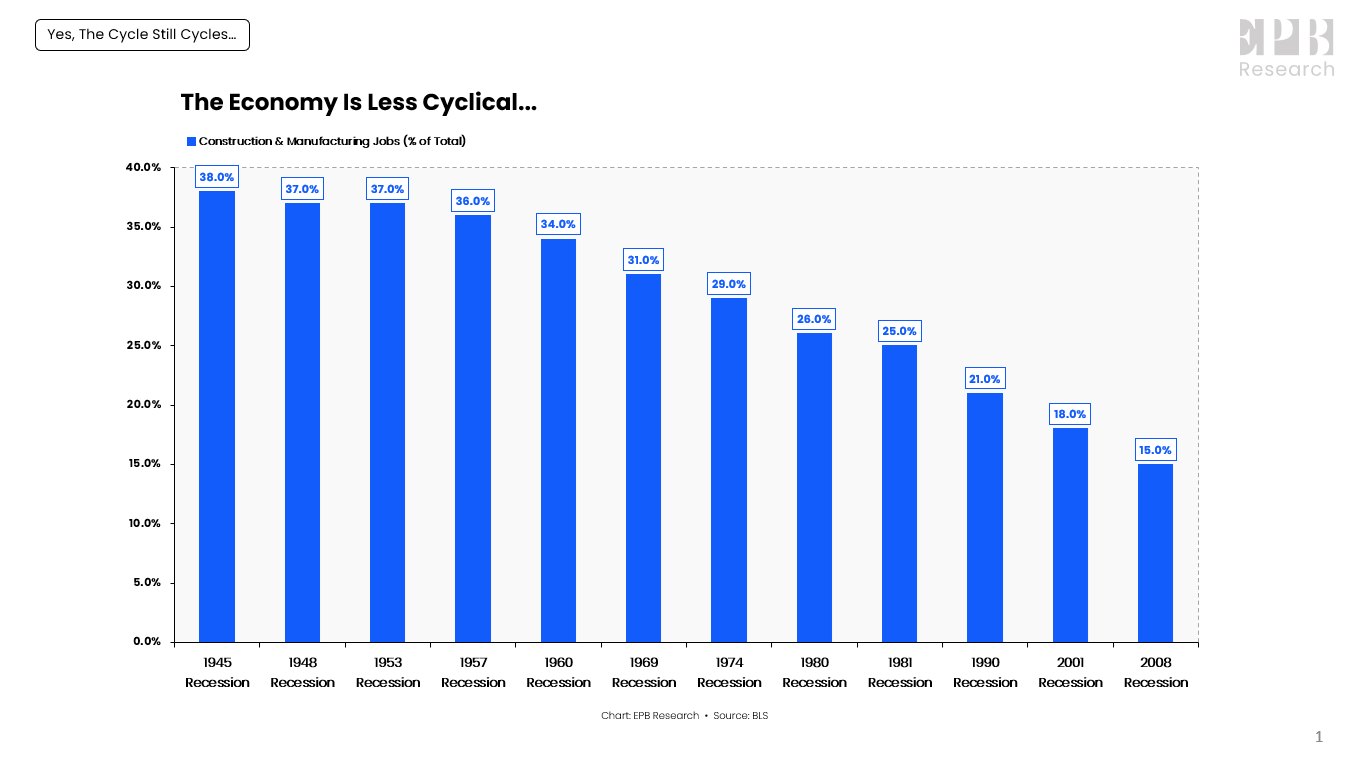

Over the last several decades, the US economy has become less cyclical, with more service sector jobs and fewer construction and manufacturing payrolls.

The shrinking share of the cyclical economy has led many people to question the validity of traditional leading indicators that still focus on the construction and manufacturing sectors.

Construction and manufacturing jobs have declined from almost 40% of total employment to 13% today.

{kind=link}

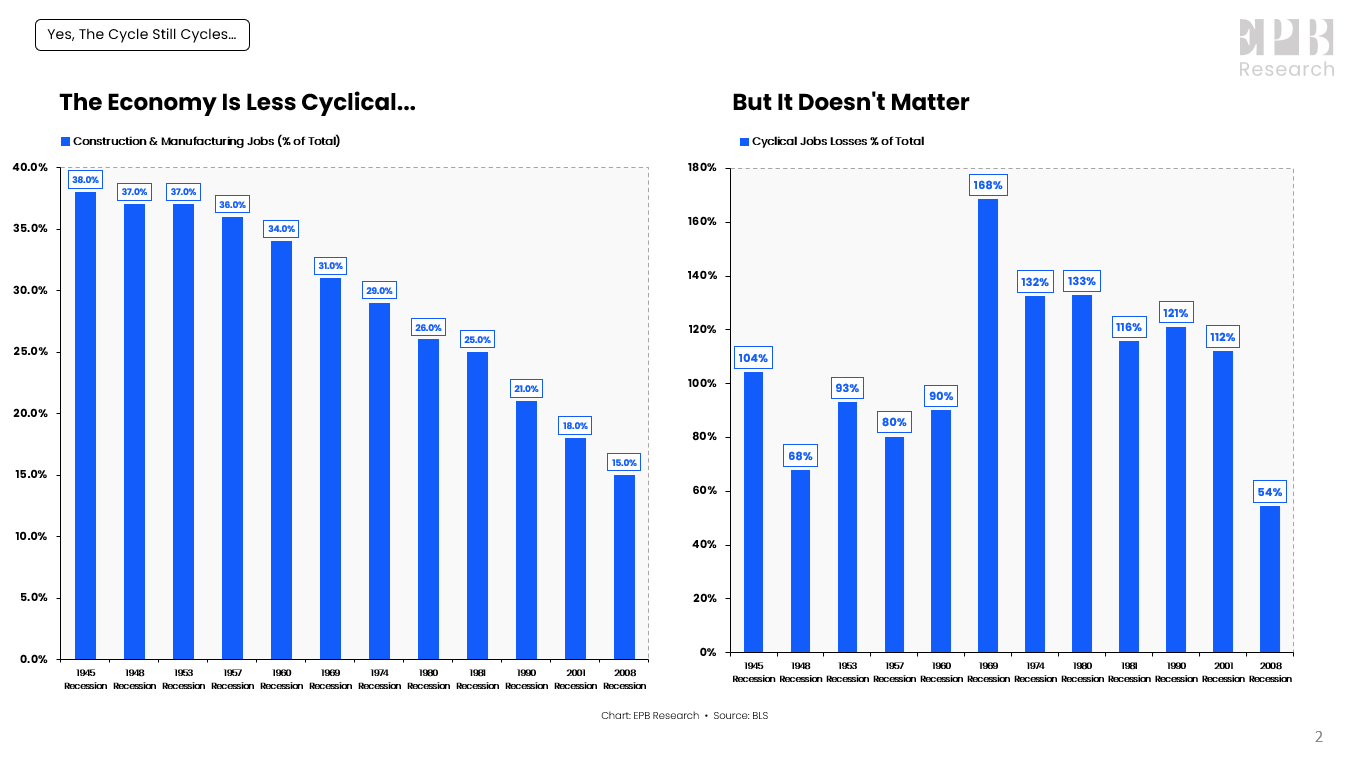

While the construction and manufacturing sectors are a relatively small share of total employment, the data proves that the cyclical economy still drives almost all the job losses around recessionary periods.

Even as the share of construction and manufacturing jobs declined, reaching 18% ahead of the 2001 recession, job losses from these two sectors during that recession were more than 100% of the total.

{kind=link}

Construction and manufacturing jobs accounted for more than 50% of all job losses around the 2008 downturn, even as that recession morphed into a banking crisis and caused significant job losses in the financial services sector.

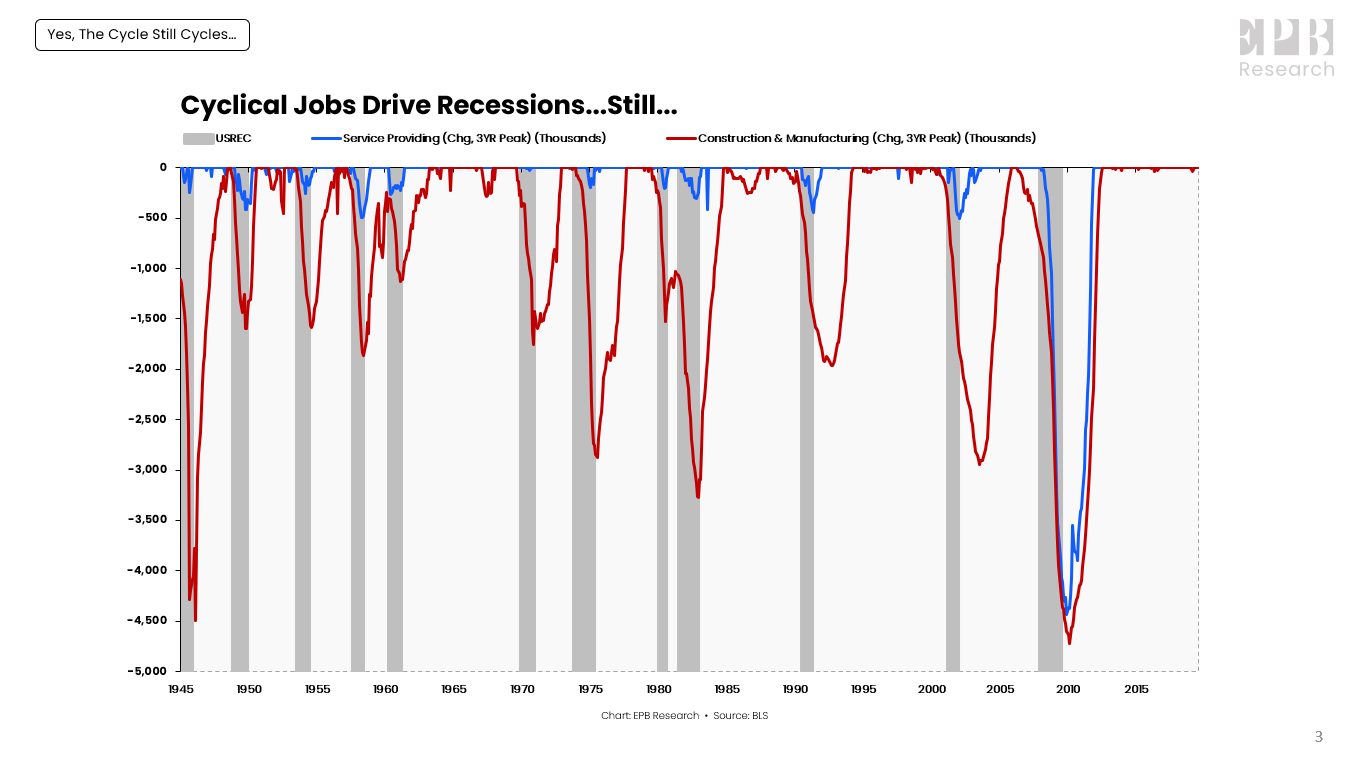

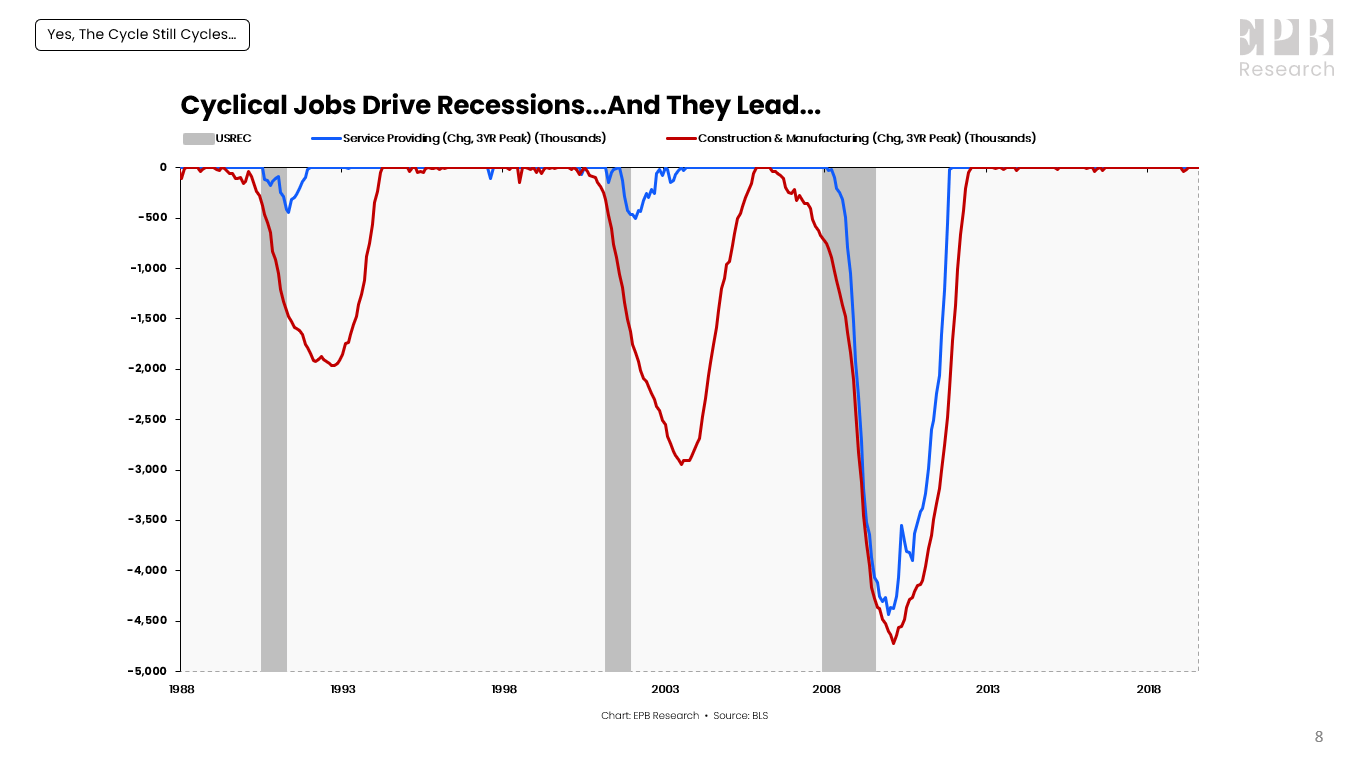

The following chart shows the level of job losses from the cyclical economy and services economy. Excluding the COVID recession for obvious business cycle reasons, job losses from the services sector exceeded job losses from the manufacturing and construction sectors zero times.

{kind=link}

Job losses from the manufacturing and construction sectors consistently make up most of the job losses around recessionary periods.

Job losses in other sectors usually result from the secondary damage caused by the earlier decline in the cyclical economy.

{kind=link}

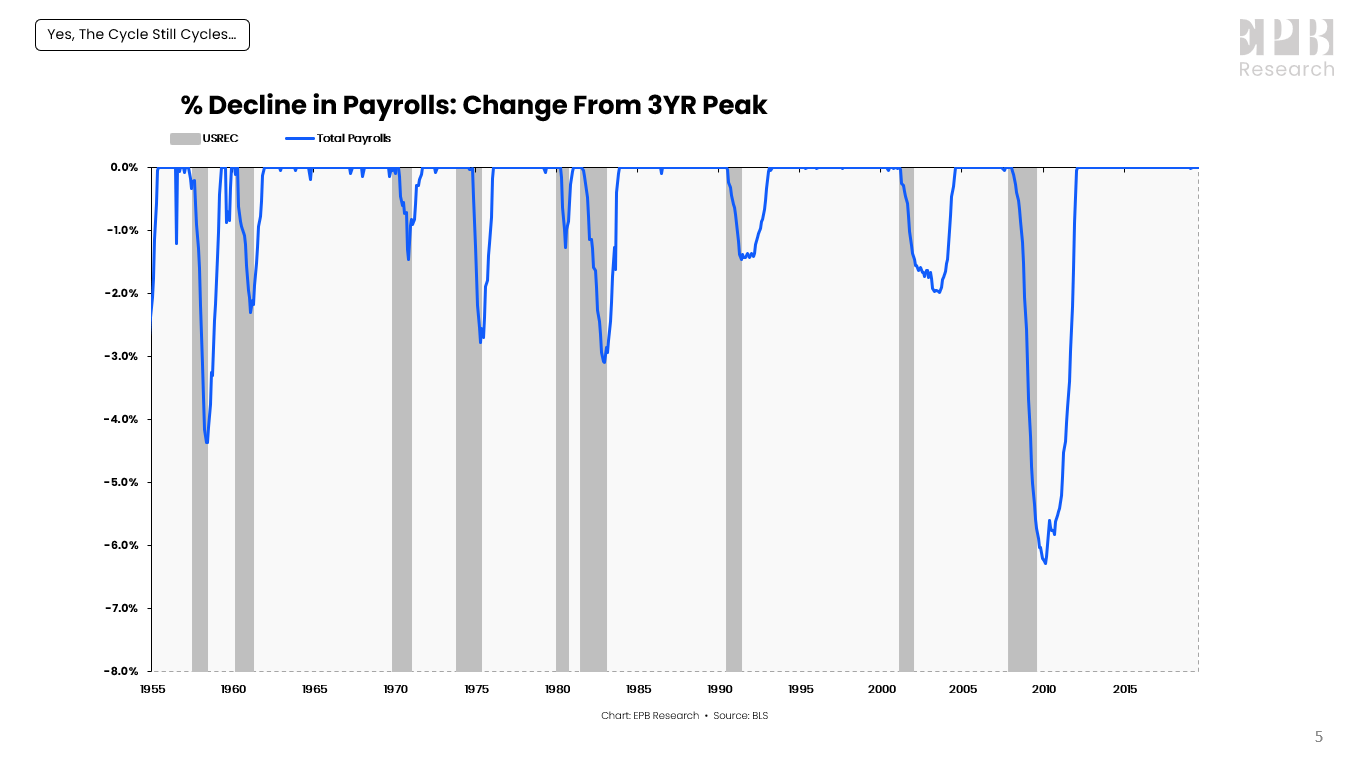

During the average business cycle recession since 1955, total payrolls declined roughly 2%-4% from the 3-year peak. On today’s payroll level of 155 million, an average recession would cause about 3-6 million job losses.

{kind=link}

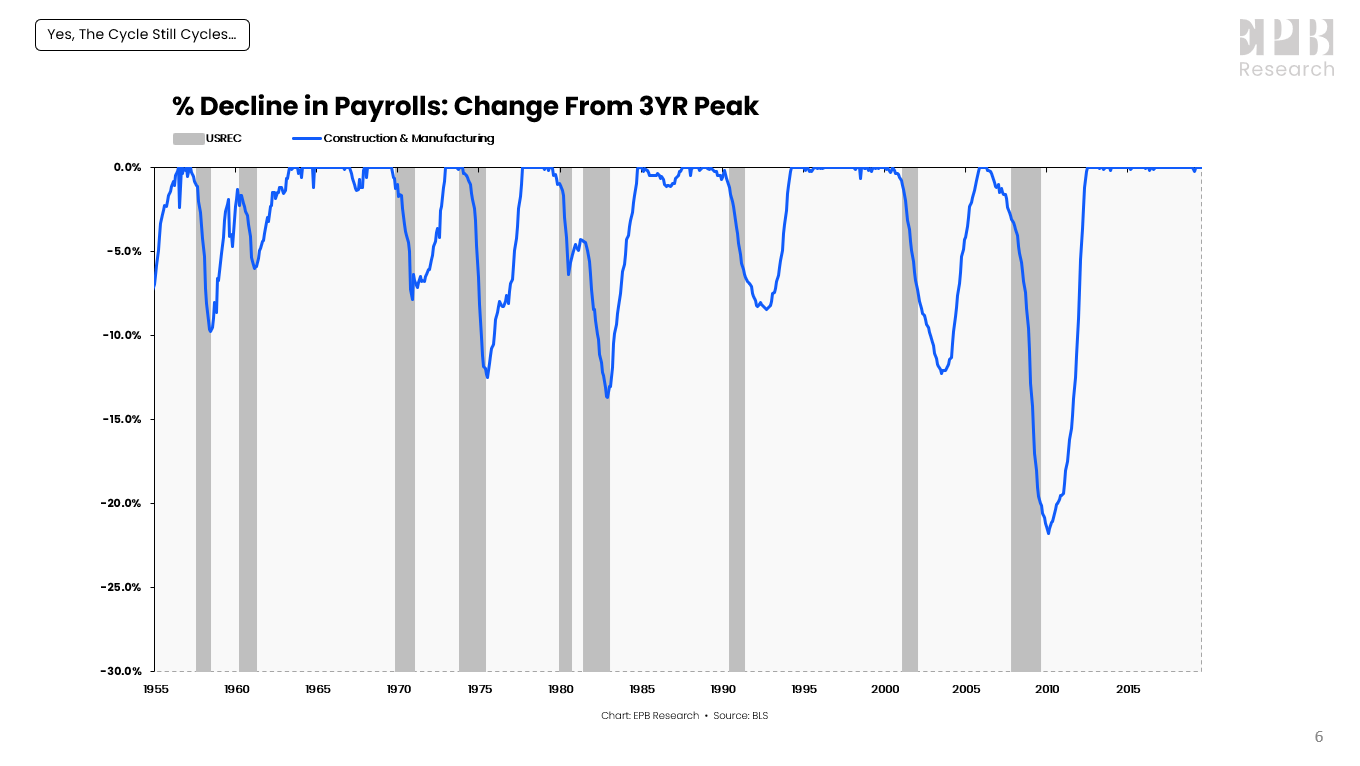

The average recession causes payrolls in the cyclical economy to decline by 10%-20%.

Construction and manufacturing account for roughly 21 million payrolls. The average recession would therefore cause 2-4 million cyclical job losses.

This shows how even though the cyclical economy has fallen to just 13% of total employment, it’s still possible to see most job losses come from these two sectors.

In other words, construction and manufacturing should clearly be the focus of any recessionary labor market analysis.

{kind=link}

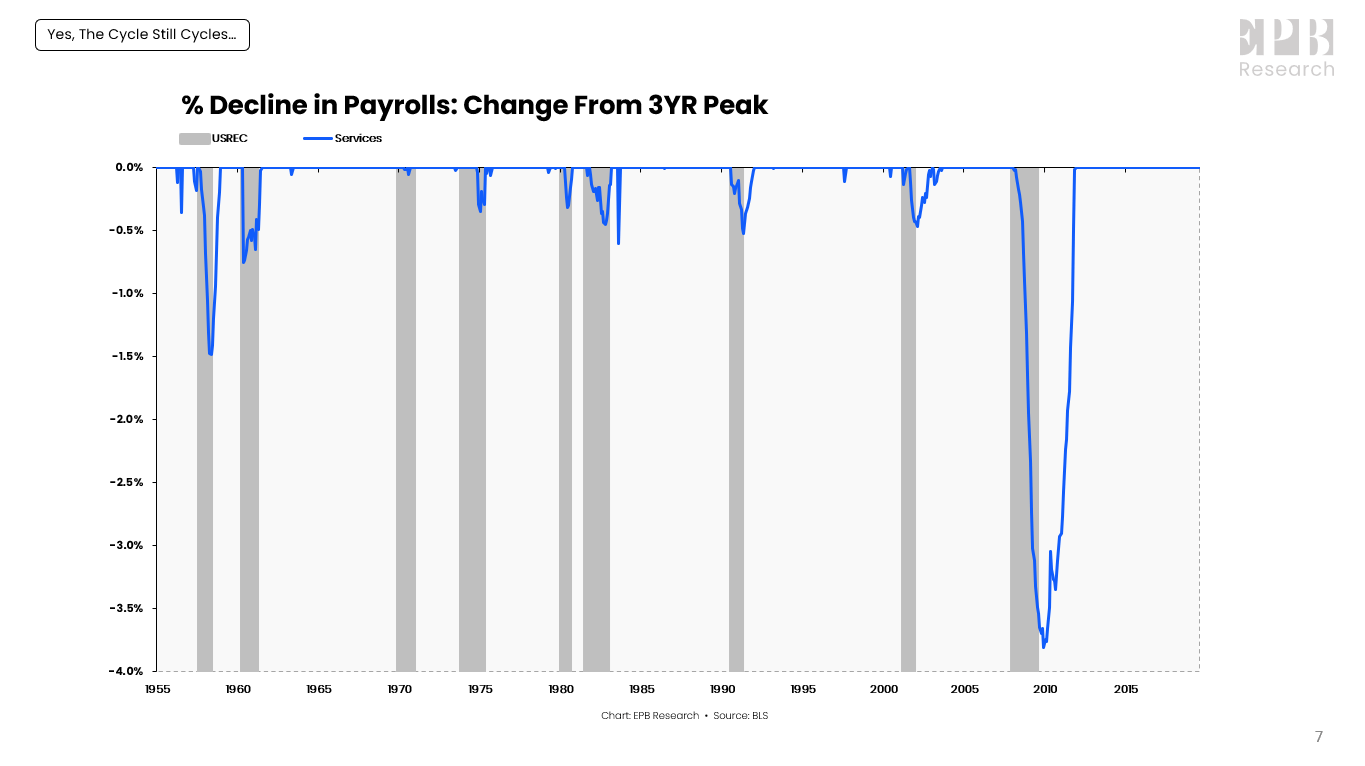

In most recessions, services employment doesn’t decline much more than 0.5% from peak levels.

Mild recessions come with virtually no service-sector job losses, while more severe recessions do proliferate into the services economy.

{kind=link}

While the deeper recessions do come with service-sector job losses, even those recessions see cyclical job losses appear first.

In the last three business-cycle recessions, cyclical job losses exceeded service-sector job losses, and cyclical job losses appeared first, which validates the traditional leading indicator approach.

{kind=link}

Business cycle analysis must remain heavily focused on the cyclical economy. Despite the shrinking size, the construction and manufacturing sectors will more than likely drive the majority of job losses in the next recession.

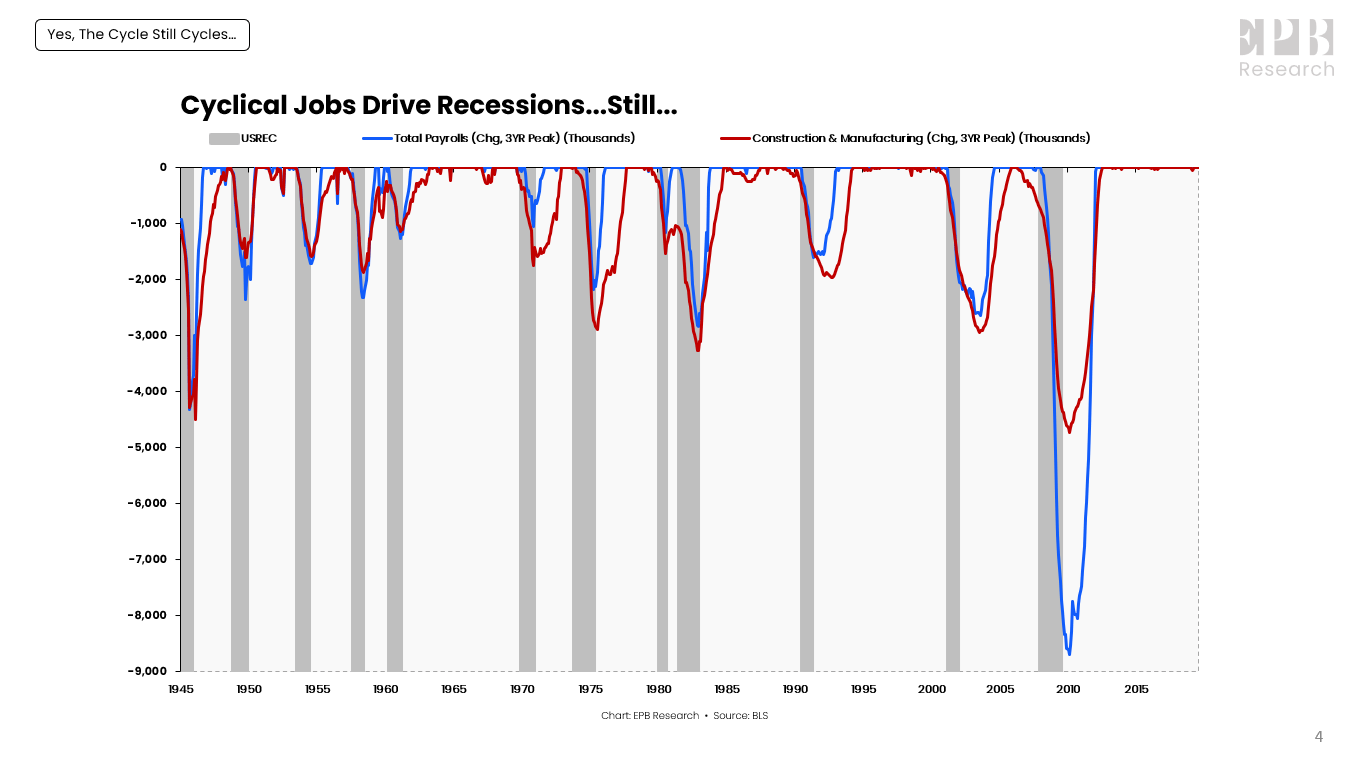

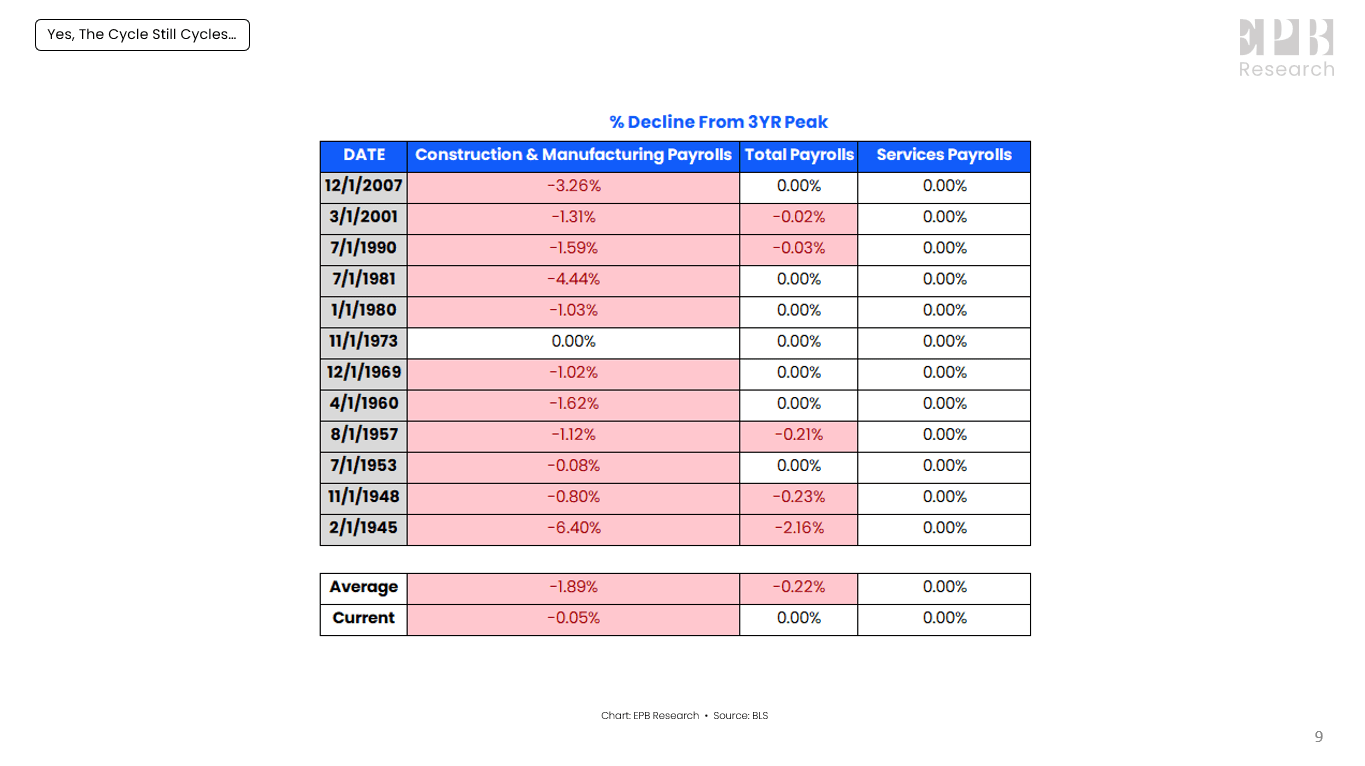

In fact, at the start of the last 12 business-cycle recessions, service payrolls were at a peak. Services payrolls never decline in advance of recessions or at the start of recessions.

This table shows the decline in employment for the cyclical economy, total economy, and services economy at the start of each recession.

{kind=link}

92% of the time, job losses were underway in the cyclical economy when the recession started. 58% of the time at recession start dates, total payrolls were at a peak. 100% of the time, services payrolls were at a peak.

Why focus on the services economy at all if there has never been a recession where services payrolls proved to be a warning signal?

It should be noted that the 1974 recession started without any job losses, so a recession can technically begin without any decline in the labor market.

The cyclical economy has just started to shed jobs today, and leading indicators signal the recession is likely underway.

To get advanced warning of recessions, you must look at the construction and manufacturing sectors, even though these two sectors are only 13% of the labor market. The services economy does not help spot recessions.

It’s clear that the composition of traditional leading indicators remains appropriate, and thus, the current resounding recessionary signal should not be ignored.

For further details see:

Yes, The Cycle Still Cycles