GOODN - Yields Up To 9%: 3 Top Dividend Stocks For 2024

2023-12-04 09:00:00 ET

Summary

- Preferred shares are today heavily discounted.

- As a result, they offer high dividend yields and upside potential.

- We present three of my favorite opportunities.

There are lots of opportunities in preferred shares ( PFF ) right now.

Most of them have crashed because of two main reasons:

- Inflation was hot and it reduced the appeal of preferred shares since they don't participate in the growth and offer limited protection against inflation.

- Interest rates have been surging for the past year and this also made preferred shares less desirable because higher rates lower their value.

But things are now changing rapidly.

Inflation has been brought back to zero... and the consensus expectation is that we have reached peak interest rates and the Fed will cut rates in 2024.

CNBC via Refinitiv

Therefore, I think that now is a great time to accumulate preferred shares while they are still priced at large discounts to par and offer dividend yields of up to 9%.

Here are three examples that we are accumulating:

Gladstone Commercial Series O Preferred Shares

The Series O preferred shares of Gladstone Commercial Corporation ( GOODO ) are currently priced at just $17.88 per share, representing a ~30% discount to par, and offer an 8.4% dividend yield. I wouldn't expect the share price to return to par any time soon, but eventually, a return to par could unlock up to 40% upside potential - in addition to the yield. This could happen as interest rates eventually return to lower levels, or it could recover closer to par if GOOD announces another share buyback program. Last year, when the company announced that it would buy back some of its preferred shares, the share price rapidly rose to $22 per share, and the same could reoccur again.

Here is what the management said back then (emphasis added):

"After thorough analysis and in consultation with our board of directors, we are announcing a share repurchase authorization as part of a capital allocation strategy that we believe is in the best interest of our shareholders and our business. We believe that, with the current market volatility due to macroeconomic conditions, there is an attractive buying opportunity for our preferred stock. We believe using capital to repurchase our preferred shares at appropriate prices represents a favorable strategic use of capital," said Buzz Cooper, President of the Company.

But now the shares have dropped back to lower levels, offering an 8.4% dividend yield in addition to 20-40% upside over time.

We think that this reward prospect is very compelling coming from a fairly defensive REIT.

After selling a lot of office buildings over the past years, it now generates about 60% of its NOI from industrial properties that enjoy growing cash flow:

Gladstone Commercial

Most of its properties are under triple net leases that generate consistent and predictable cash flow. The REIT managed to collect most of its rents even in 2008-2009 and it has today 7 years left on its leases:

Gladstone Commercial

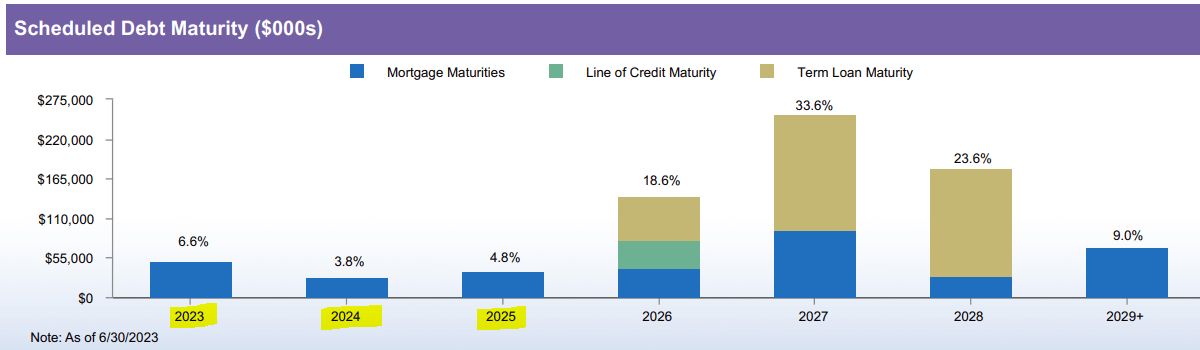

The REIT has also significantly deleveraged its balance sheet over the past years, and it is now in a good position with a 45% LTV and no major debt maturities before 2026:

{kind=link}

Finally, the REIT is well-managed and insiders have a lot of skin in the game.

Therefore, we think that its preferred dividend is sustainable. The REIT owns mostly industrial properties that generate steady cash flow from long-term leases with credit-worthy tenants, and it has a good balance sheet in today's rising interest rate environment.

With that in mind, the 8.4% dividend yield coupled with 20-40% upside potential is very compelling for our Retirement Portfolio.

As we noted earlier, the upside will likely occur as GOOD returns to share buybacks and/or as interest rates drop back to lower levels.

Another potential catalyst is GOOD's continued efforts to sell office properties to become a pure-play industrial net lease REIT. It has made a lot of progress over the years and as it eventually becomes overwhelmingly industrial-focused, the market will likely reprice it at a smaller discount.

In the meantime, we will collect the 8.4% dividend.

KKR Real Estate Finance Trust Inc. ( KREF ) Series A Preferred Shares ( KREF.PR.A )

KREF.PR.A is our Top Pick among the preferred shares of mortgage REITs ( MORT ).

Its loan portfolio is mostly collateralized by multifamily, industrial, and life science buildings. Moreover, 100% of its loans are senior secured and have a floating rate that's today resulting in growing interest income.

The preferred equity (which is what we are buying) also represents only ~5% of the total capitalization and enjoys a >7x dividend coverage. Finally, while the leverage is a bit high, it is important to note that the company has no debt maturities in 2024 or even 2025.

Despite that, its preferred shares have recently pulled back to the same levels at which we initiated our position earlier this year:

{kind=link}

At these low levels, the dividend yield is 9.2% and the discount to par is about 30%. The market is worried about 1/4 of the loan portfolio, which is collateralized by office buildings, but keep in mind that practically all of these are Class A properties and there's a strong case to be made that Class A offices will survive the current crisis as tenants make a "flight to quality" in the years to come.

There will likely be some defaults and the market hates such headlines, but we believe that those defaults won't be significant enough to hurt the preferred equity, which enjoys great coverage.

Even then, it has dropped in association with the common equity and we view this as a compelling opportunity for higher yield-seeking investors.

Arbor Realty Trust, Inc. ( ABR ) Series F Preferred Shares

Earlier this year, we initiated a position in the Series F preferred shares of Arbor Realty Trust ( ABR.PR.F ) because it had sold off due to a short report that had little merits in our opinion.

Shortly after, the share price recovered significantly and we were happy to simply hold it to milk the dividend.

But we are now once again presented with the same opportunity. Another short report has come out and it has pushed the preferred shares back to where they were when we first initiated our position.

In short, we believe that the common stock of the company is risky and the short sellers are right to point out that ABR will face some losses in this challenging environment.

But we think that the preferred equity should be fine because it is just a small slice of the total capitalization and enjoys strong asset and dividend coverage. Despite that, it has dropped with the common stock and now trades at a near 30% discount to its par value and an 8.5% dividend yield.

What's uniquely attractive about ABR.PR.F is that it is very likely to get called back by October 2026 because that's when its 6.25% fixed rate will turn into a floating rate of 3-month SOFR plus 5.442% with a floor of 6.125%.

This would result in a ~10% floating rate at par based on today's interest rates.

That's so expensive that ABR.PR.F would likely decide to call back the preferred equity, resulting in 30%+ upside by October 2026 on top of the 8.5% dividend yield. And in case they decide to not call back the preferred, its dividend yield would rise to about 14% given how heavily discounted they are relative to par. This should push the share price closer to par even if they don't get called back.

So the risk-to-reward seems very compelling to us.

I would add that ABR's insiders have been making heavy purchases of the comment stock in recent months. Its CEO already has the bulk of his net worth invested in the stock, and he just bought another $1+ million worth of stock over the past weeks:

{kind=link}

ABR also just reported strong Q3 results. Here are the CEO's closing comments on their recent earning call (emphasis added):

"In summary, we had another great quarter , and we believe our unique business model clearly demonstrates our ability to generate strong earnings and dividends in all cycles. We understand very well the challenges that lie ahead, and we are very well positioned to manage through this cycle. Our earnings significantly exceed our dividend run rate. We invested in the right asset class with very stable liability structures, highlighted by a significant amount of nonrecourse non-mark-to-market CLO debt with pricing that is well below the current market. We are well capitalized with significant liquidity, which has put us in a unique position to be able to manage through the downturn and take advantage of accretive opportunities that will exist in this environment."

They even noted that their business is doing so well that they could have increased their dividend again (emphasis added):

"We've produced distributable earnings of $0.55 per share, which is well in excess of our current dividend, representing a payout ratio of around 78%. The dividend policy that we have implemented with our Board of keeping such a wide disparity between our earnings and dividend has provided us with a large cushion and was very strategic knowing full well that we're entering to a market dislocation. And we certainly could have raised our dividend again this quarter based on a substantial cushion and continue to show earnings, the Board decided to keep it flat since we believe we are not getting credit for raising it in this environment and will be more prudent to preserve a large cushion as we head into the most challenging part of the cycle."

This isn't just talk. They have a fantastic track record of dividend growth (emphasis added):

"We're also the only company in this space that has been able to consistently grow our dividend with approximately 40% growth over the last 3 years, all while maintaining the lowest dividend payout ratio in the industry. Just as importantly, in a time of tremendous test, we've managed to maintain a book value of our according reserves for future losses, which clearly differentiates us from our peers."

Now, obviously, today's environment is far more challenging, but they are confident that they won't need to cut the common dividend, let alone the preferred dividend (emphasis added):

"And we believe our diverse business model uniquely positions us as one of the only companies in the space with the ability to preserve our book value and continue to provide a very stable protected dividend even in this extremely challenging environment."

Again, this is not just talk. The management is heavily invested and buying more shares with their own money.

So all in all, I really like the risk-to-reward of the preferred equity and I am glad that we are getting to buy a bit more at these low levels.

The short seller is claiming that multifamily cap rates should be 7% and that would put ABR at risk of substantial losses as loans go into default. I don't buy into that. I agree with them that the value of the collateral has decreased and some losses are inevitable, but I don't expect cap rates to rise anywhere that high. I believe that the short seller may ultimately be right and make some money on their short call. But we are buying the preferred equity, not the common equity, and we like the risk-to-reward at these levels. We expect 15-20% average annual total returns over the coming 3 years.

Bottom Line

Such high yields obviously come with some risks.

But the risk-to-reward of these preferred share opportunities is very attractive in our opinion.

For further details see:

Yields Up To 9%: 3 Top Dividend Stocks For 2024