OWL - You Can Find Value Growth And Yield Within Apollo Global Management's Tickers

2023-06-21 18:57:09 ET

Summary

- Apollo Global Management has recovered from the banking crisis and is trading at a 52-week high, while Athene's preferred stocks remain undervalued.

- Apollo's innovative business model, which creatively uses insurance, is one reason for optimism about the company's future.

- The company is well-positioned to benefit from the banking crisis by increasing its share in investment-grade debt at the expense of banks.

- Several issues of Athene's preferred stocks remain attractive due to the combination of 7%+ yield and probable outsized capital return once the credit cycle turns. Series D is expected to deliver the highest return.

Apollo Global Management ( APO ) is a holding company that comprises alternative asset manager Apollo Asset Management ("old Apollo") and life insurer Athene Holding Ltd. ( ATH ) ("AHL"). This structure has been in place since Jan 1, 2022, when ATH and AAM merged.

Three months ago, in the middle of the banking crisis, I published about Apollo and separately about Athene's preferred stocks . At that time, due to indiscriminate selling, many financial issues were suffering. Athene may resemble a bank more than any other financial company, and its preferred stocks and APO itself were trading low. I argued that the banking crisis would not affect Athene and considered the company safe with excellent growth potential. Consequently, both APO and Athene's preferred stocks appeared attractive.

Since these publications, APO has more than recovered and is trading at a 52-week high, while Athene's preferreds are still in the bargain bin.

In the following discussion, I will try to avoid repetitions of my previous posts and will refer to them instead whenever is appropriate.

Apollo

I became bullish on APO two years ago, immediately after the merger between Apollo and Athene was announced, and took a substantial position in Athene. Upon the all-stock merger closing, these shares were converted into APO. My target was 15-20% in total annual return over many years.

It did not go smoothly. Only after the May-June rally, my return has reached the target. Currently, my annualized IRR is ~18% vs. ~4% for the index. Skeptics would ascribe it to a pure beta effect and there might be a deal of truth in it. However, beta alone cannot explain why APO has been handily beating the index always since the merger announcement both in good and bad markets.

The future is not expected to be smooth either - alt managers are notoriously volatile. But apart from valuations, there are two fundamental reasons for being firmly bullish on APO.

Today, Apollo's business model seems logical and simple to me but it was not so when I started researching the company two years ago. The progress was gradual and I published on Apollo quite a few times hoping to share insights with my readers. In its turn, each of the publications advanced my understanding as well. It takes time to internalize what Apollo is doing. Management tirelessly repeats the same message over and over to win investors and these efforts, combined with actual results, slowly bear fruit.

In short, Apollo introduced a new way to creatively use insurance. There are traditional insurers, there is Berkshire Hathaway ( BRK.A ) ( BRK.B ), and now there is Apollo and Athene.

Surely, many readers have discounted the last paragraph and the comparison with BRK. It is understandable. But what if I am right? My best attempt to explain this new business model was in "Why Brookfield And Peers Followed Apollo Into Insurance and What's In It For You" published several months ago.

So, a superior business model that takes time to conquer skeptical minds is one reason for my optimism. Additionally, for favorable conditions unforeseen, this business model has become more attractive than it was originally planned.

You may know that after the recent banking crisis, banks have become more reluctant to lend. Even before the crisis, banks were burdened with Dodd-Frank and similar regulations that made them less agile and more risk-averse. The crisis has exacerbated these trends.

Credit demand meanwhile keeps growing in line with GDP. Alt managers are well-positioned to partially replace banks providing private credit. Several big players specialize in private credit including Oaktree (now a part of Brookfield Asset Management ( BAM )), Ares ( ARES ), and Blue Owl ( OWL ). However, they primarily issue low-grade debt using BDCs, private funds, and other vehicles. Apollo, on the other hand, can do everything of the above but is focused on investment-grade debt which is much safer and has a bigger addressable market. Apollo may become the biggest beneficiary of the banking crisis increasing its share of investment-grade debt origination at the cost of the bank's debt.

Out of ~$600B of Apollo's AUM today, ~$450B is in private credit with most of them being investment-grade. Most of the investment-grade private debt is on Athene's balance sheet which is growing quickly and organically . Apollo's growth today is more related to organic growth and safer growth of Athene's balance sheet expansion than to the heroic deeds of private equity actors.

Perhaps, the realization of these facts by some investors has propelled APO shares as well as beta.

Before finishing this section, I need to touch upon APO's valuations. APO can be valued as a sum of old Apollo with its fee-related earnings ("FRE") and carry and Athene with its spread-related earnings ("SRE") less interest expenses, Holdco's costs, and taxes. I have done it several times in the previous posts and will simply repeat my conclusions here without going into detail.

Old Apollo is easy to value. One can be very conservative with carry (its input is rather small anyway) and focus on valuing FRE only. A straightforward comparison with asset-light and management-fee-centric companies like Ares or BAM produces at least 25 multiple for after-tax FRE. In my valuations, I used 20-25 multiples. For SRE, I used 10-15 multiples.

This exercise produced $69-94 for APO's value on Dec 31, 2022. The company (as late as on June 1, 2023, during CEO Marc Rowan's presentation ) forecasts ~25% growth in 2023 for both FRE and SRE which translates into an ~$84-115 valuation range towards the end of 2023. At today's $77, APO still appears somewhat undervalued. Please note that even a fairly valued APO still promises 15-25% annual growth.

I would like to emphasize an important issue here: while most investors would agree on how to value old Apollo, there is a major disagreement on how to value Athene. Life insurers are often valued at 6-8 multiples. But I am not familiar with a life insurer that has produced 16-17% ROE every year for more than a decade like Athene. Moreover, Athene has achieved it in a very conservative way being underleveraged and carrying excess capital. My low-end multiple for Athene is 10 (which I justified here ) but even it may underestimate the company.

If you are interested in value and growth combined with a decent 2%+ dividend for peace of mind, APO may be the right stock for you.

Athene and its preferred stocks

Technically Athene belongs to life insurers but in reality, it does not insure anything. Athene is a retirement specialist focused on issuing fixed annuities to (future) retirees. Apollo invests funds that Athene receives from retirees at higher interest rates than promised to retirees. The difference (after deducting Athene's opex) becomes SRE. For its services, Apollo charges Athene fees that become part of FRE. SRE is calculated AFTER deducting these fees. Thus, the expansion of Athene's balance sheet provides growth for both FRE and SRE.

Fixed annuities are always popular as a tax-deferred retirement vehicle. Today, with interest rates at ~5%, fixed annuities are particularly hot. The number of retirees keeps growing as well. All this makes retirement services a growing and lucrative industry. Athene is the number one issuer of fixed annuities in the US.

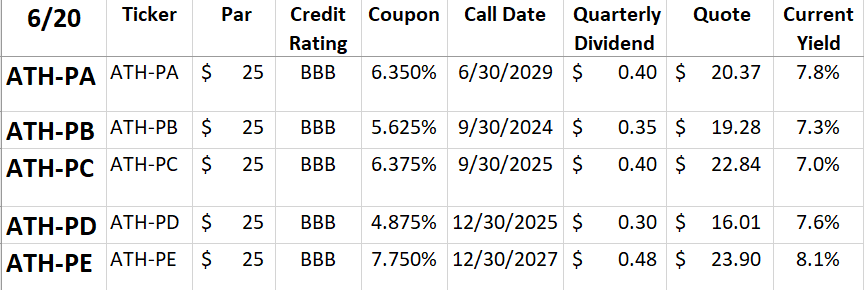

You can participate in this industry indirectly via APO or directly via Athene's preferred stocks listed in the table below.

{kind=link}

Some comments are needed to this table:

- All issues are perpetual and non-cumulative.

- All issues are qualified for a 15-20% maximum tax rate.

- All issues went ex-dividend on Jun 15 and their stripped yields are not that different from the yields in the table.

- Series A will become floating at the call date, with a dividend rate of 3-month LIBOR+4.253%.

- Series C is resettable on its call date and every 5 years after that at the rate of 5-year Treasury+5.97%

- Series E is resettable on its call day and every 5 years after that at the rate of 5-year Treasury+3.962%.

- We will ignore some terms and conditions that might be triggered by rare events such as a change of control, etc., because of their low probability.

- We are not considering other preferreds related to APO that start with either AAM or AHL tickers (AHL relates to an affiliate of Athene but I have not found any filings for it).

I published a similar table in my previous article on Athene preferreds three months ago during the banking panic. What strikes me is that almost all preferreds are selling at about the same price as three months ago. But the risks are lower today! Let me explain it.

In the previous article on preferreds, I analyzed credit risks and found them extremely low. Nothing has changed since - please check the previous article for details. Ditto for the interest rate risk and the risk related to the non-cumulative nature of preferreds.

There is only one change since the previous article and it relates to surrender risk. Three months ago, I considered annuities' mass surrender as the most significant risk. It was still quite unlikely because of tax penalties imposed on premature surrenders and additional protection via hefty surrender charges and market value adjustments.

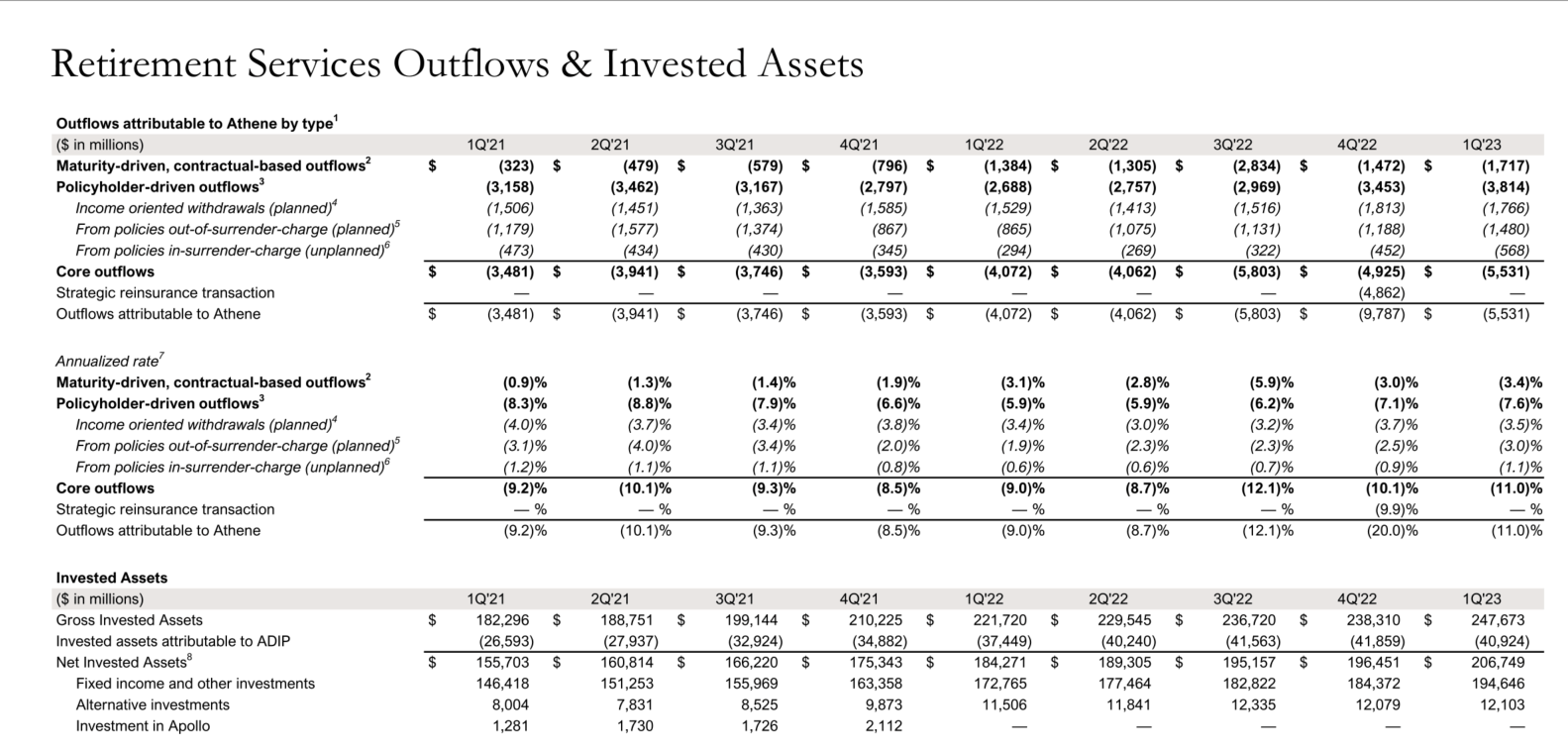

In sync with its Q1 earnings calls in May, APO released a slide illustrating the rate of surrenders over the last couple of years. I pasted it below even though the font is quite small.

{kind=link}

There are three reasons for retirees to withdraw funds from annuities. Firstly, they withdraw funds because of RMDs; secondly, they withdraw funds that are already outside of the surrender period; and thirdly, for various life-changing reasons (divorce, health, long-term unemployment) they withdraw funds that are subject to surrender charges. Only the last scenario is unplanned and represents a risk. But the rate of these unplanned withdrawals has varied little over the last two years including Q1 23 when people were panicking about their bank deposits. In fact, this rate in Q1 23 was slightly lower than in Q1 21!

The same point was further reinforced in Apollo's presentation on June 13, 23, when the company was fully aware of what is going on in Q2. After these disclosures, unplanned withdrawals/surrenders appear less probable today than three months ago.

I am a bit puzzled by this situation: Athene's progress seems to be recognized and reflected in the rise of APO shares and risks related to Athene's preferreds appear lower than three months ago. However, preferreds keep trading at the same level as three months ago. My only explanation of this is that investors perceive interest rates to stay higher for longer today as compared with three months ago. It would put preferreds under pressure but only temporarily until the credit cycle turns. If you are committed to holding preferreds for several years, it should not affect your decision.

I consider three preferred issues particularly attractive. The surest and simplest bet is ATH-PC. Unless Athene calls it in 2 years, its coupon will skyrocket. This is extremely unlikely. But if Athene calls at $25, investors will pocket a ~4.5% of annualized capital return in addition to a 7% yield for a total annualized return of ~11.5%.

ATH-PA combines an attractive 7.8% with a substantial capital return 2-3 years down the road when the credit cycle turns. The total annualized return may reach 13-14%.

ATH-PD remains my favorite issue because of outsized probable capital return. It is trading at only $16 today. If interest rates become lower in, say, 3 years, it can easily add ~12% in capital return on top of a 7.6% yield.

If you are interested in income and value, Athene's preferred stocks might be of interest to you.

For further details see:

You Can Find Value, Growth, And Yield Within Apollo Global Management's Tickers